The Future of Income-Share Agreements Policy and Politics

Photo: BrianAJackson / iStock / Getty Images Plus

This paper is part of the Manhattan Institute’s initiative, Reinventing Higher-Education Finance: Solutions from Beyond the Beltway—a series, curated by MI senior fellow Beth Akers, that aims to generate fresh solutions to some of the persistent challenges in U.S. higher education.

Introduction

In a 1955 essay, economist Milton Friedman highlighted a market failure in the finance of higher education: unlike most types of debt, such as mortgages or auto loans, education debt gives the borrower no physical asset to put up as collateral. This lack of security for the lender, combined with wide variation in the fortunes of individual students, would require usurious interest rates on education loans despite high returns to schooling, he observed, leading to widespread underinvestment in higher education and untapped potential among America’s youth.[1]

Politicians over the following decades heeded Friedman’s warning and created the federal student loan program, which has existed in one form or another since 1958.[2] While the design of the program has evolved, a consistent theme has been a large role for the federal government in ensuring the continued provision of low-interest student loans. Today the federal government originates nearly 90% of the $106 billion in student loans disbursed annually.[3]

But boosters of a federal student loan program to counter this market failure have ignored the second part of Friedman’s analysis—that debt is an inappropriate instrument to finance education, regardless of whether the government or the private market originates the loans. Policymakers should turn instead to the standard instrument to finance risky ventures that has long served the interests of investors as well as those in need of financing: equity.

Friedman argued that the education-finance market could benefit from an analogue to equity. He proposed that an investor could “advance [a student] the funds needed to finance his training on condition that he agree to pay the lender a specified fraction of his future earnings.” Rather than fixing payments at a set amount every month, an individual would repay more of his obligation if he were financially successful and less if not, just as shareholders in a corporation receive larger returns when the company does well. Today, we call this concept an “income-share agreement” (ISA).

In recent years, ISAs have gained popularity as a means to finance education. Major universities such as Purdue have created ISA programs for their students, while new educational models, such as short-term coding academies, look to ISAs as a financing tool. The idea has proved popular with students and parents, too: in contrast to a fixed debt obligation, the borrower is guaranteed a flexible, affordable payment. If the borrower’s income drops because of recession or personal circumstance, so does his ISA payment; if the borrower’s income increases, the reverse is true. Lawmakers from both parties have sponsored legislation to speed the introduction of ISAs into the private market, while policy experts have proposed replacing the federal student loan program with a government-run ISA.

ISAs have a strong theoretical foundation; but it is only in the last few years that ISA programs have begun to operate in the real world. It is worth examining how ISAs are used by students, investors, and academic institutions—for the sake of evaluating their performance and for informing how they might be expanded to a larger scale, perhaps even as a replacement for government-backed student loans. The federal student loan program has enough shortcomings that alternatives should be welcome.

The Failure of Federal Student Loans

Government-backed student loans have reached one of their primary goals: to expand access to education finance and, with it, access to college. The share of high school graduates who attend college has risen from 45% in 1960 to 70% today.[4] Yet completion rates are dismal. Among students who began college in 2012, just 58% earned a degree within six years.[5]

Friedman noted that even though the expected returns to education are high, the variance of those returns is also high. Differences in student ability, the quality of the education, and random luck mean that some students will use their education to achieve great success while others will fail. “The result,” Friedman wrote, “is that if fixed money loans were made, and were secured only by future earnings, a considerable fraction would never be repaid.”[6]

This prediction has come true. The U.S. Department of Education (ED) estimates that 26% of federal undergraduate student loans made in 2018 will enter default at some point.[7] Within five years of entering repayment, 49% of student borrowers have negatively amortized (i.e., their loan balance has increased since they entered repayment).[8] Many of those borrowers will never fully repay their loans, leading to financial distress, damaged credit, and losses for taxpayers.

Some of the student loan nonpayment problem is avoidable. Default rates would be lower if more students enrolled in income-based repayment plans, which adjust borrowers’ payments according to income and family size.9 But such plans also run the risk of lowering borrowers’ payments so far that they will no longer cover accrued interest and will lose money for the government. Income-based repayment will cost taxpayers $13 billion for loans issued in 2017 alone.[10]

A large portion of the nonpayment problem is structural. Borrowers who do not complete a degree are far less likely to repay their loans, since dropouts have the burden of debt but none of the benefits of the degree.[11] Absent large reductions in the college dropout rate, non-completion will continue to drive high levels of student loan nonpayment.

It is doubtful that policymakers can eliminate nonpayment while maintaining the current framework of the federal student loan program. The reason is that federal student loans are open-access: in most cases, students do not need to pass a creditworthiness test. The federal government also does not restrict student lending based on observable predictors of future success, such as high school GPA or SAT scores. An open-access program may serve key policy goals. But one that keeps a debt model for education finance, with subsidized interest rates, will continue to experience high rates of nonpayment, lead to unaffordable debt burdens for many students, and act as a drag on the federal budget.

ED also has a poor track record of administering the student loan program. It has engaged in practices that would probably not survive regulatory scrutiny at a private bank, including presiding over high rates of negative amortization, providing confusing or inaccurate information to borrowers,[12] and overseeing widespread borrower misconceptions about the nature of their debt.

ED has not required colleges to provide a good-faith estimate of total borrowing for the completion of a degree, along with loan terms and estimated payments once the loan becomes due. Banks, of course, are subject to regulatory requirements that mandate disclosure of key loan terms, including the total amount borrowed, interest costs, and monthly payments. Colleges, however, have resisted providing similar disclosures for student loans.

An analysis of 11,000 financial-aid award letters by New America, a think tank, found that many contained “confusing jargon and terminology.” Some loans were even marketed as “awards.”[13] If a private bank used such deceptive marketing to push loans on consumers, regulators would pounce, and for good reason. Lumping loans together with grants and work-study under the “awards” label creates undue confusion among students and their families. Perhaps as a result, 28% of first-year student borrowers don’t even know that they have federal student loans, according to a Brookings Institution report.[14]

Many students are also averse to taking on debt.[15] This is a double-edged sword: loan aversion may reduce overborrowing but may also stop students from borrowing when it could benefit them. Despite the flaws of the federal student loan program, the additional funding that loans provide can help students, when used responsibly. One randomized study found that borrowers earned more college credits and higher GPAs relative to non-borrowers.[16]

The strengths and weaknesses of the existing student loan system point to the need for a model that provides education funding to students who would benefit from it, while avoiding the inherent problems that attend a debt model for education finance.

The Promise of ISAs

For risky, unsecured investments in the private market, debt is not the optimal financial tool. Rather, the first investments in startup businesses and other risky assets occur through equity finance. Unlike debt, equity investments have no balance or interest rate, so the recipient of the investment is not obligated to pay back a set amount. Instead, the investor takes an ownership stake in the asset, and his return rises and falls with the asset’s performance.

Friedman proposed an analogue in the market for education finance. Under the “equity model” in education, an investor pays for a student’s education in exchange for a small percentage of the student’s future earnings over a set period. Rather than repaying a fixed amount, the student’s payments to the investor differ, based on how much the student earns over the course of his career. Though Friedman proposed this model as an abstract concept in 1955, it has gained currency in recent years and today bears the label “income-share agreement.”

The ISA model transfers risk from the student to the investor. Students who earn little after leaving school will repay relatively low amounts toward their obligation, while students with high earnings will pay back the full cost of their education and then some. ISAs therefore provide each student with a safety net against adverse outcomes—payments are never disproportionate to the student’s ability to pay.

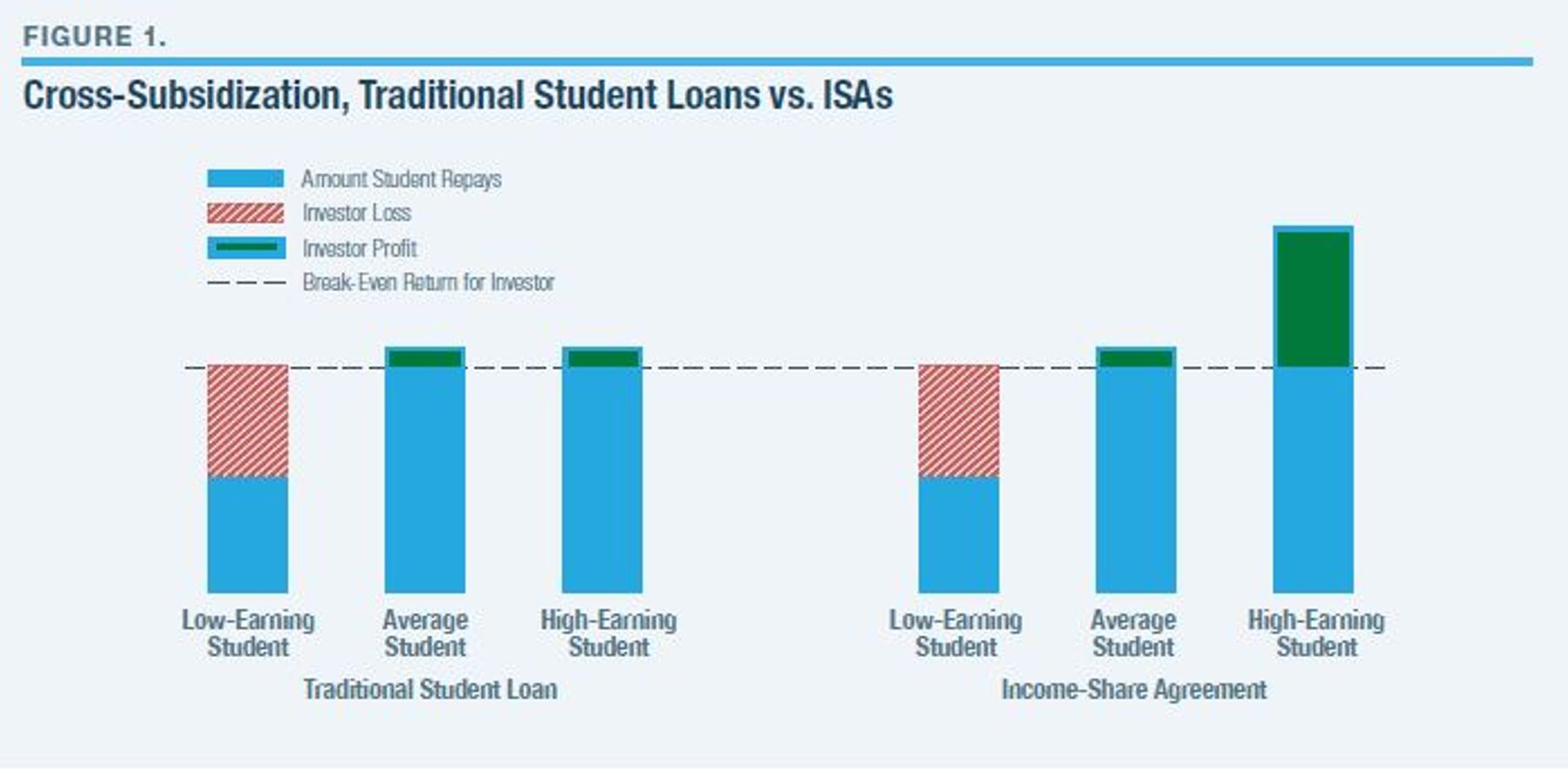

While an investor takes on more risk for each individual student, financing several ISAs can actually reduce investors’ losses relative to traditional student loans. This is because high-earning students cross-subsidize the losses that investors suffer on low-earning students. This level of cross-subsidization is not present in traditional student lending, where borrowers make the same payments on equivalent loan balances, regardless of their income levels. While traditional private student loans require the average student to pay a high interest rate, cross-subsidization under ISAs lowers average students’ expected payments to a reasonable level.[17]

Figure 1 compares a portfolio of traditional student loans relative to a portfolio of ISAs. An investor finances the education of several students, who experience divergent outcomes. Under a traditional loan (left panel), low-earning students are unable to fully repay their balances (i.e., the investor must take losses on those students). To compensate for those losses, the investor must demand higher interest rates from all borrowers, which creates undue burdens on the average- and high-earning students who repay their loans in full. Given those high interest rates, some potential borrowers may decide not to bother with college at all.

Now consider using an ISA to fund these students’ educations (right panel). Low-earning students still fail to repay the cost of their education, and the investor just breaks even on average-earning students. But a high-earning student repays far more than he received for his education, which compensates the investor for losses on his less fortunate peers (but with a payment that is affordable to the student).

Because cross-subsidization defrays investor losses on low-earning students, the investor no longer needs to demand high payments from the average student to break even. Therefore, an average student pays less than he would under a traditional student loan. Though high-earning students end up paying more, expected payments for most students should be lower under ISAs relative to loans. Moreover, a high-earning student benefits from the ISA as a form of insurance: if his income suddenly falls, his payments adjust with it.

As investors’ returns rise with students’ income, the ISA structure more closely aligns the incentives of investors with the economic interests of students. This encourages investors to help students seek out institutions and fields of study with the highest expected returns. This incentive still exists in the traditional private student loan market, but it is duller, since investor returns are limited because of the fixed-payment nature of loans.

Aligning the incentives of students and ISA providers is especially important if the provider is the student’s school (the case for most existing ISAs). The ISA model gives the school a direct stake in the student’s future success because the school’s revenue is commensurate with students’ future earnings. Schools therefore have a sharp financial incentive to ensure that their students graduate and that their degrees are valuable in the labor market. The model is also reassuring to students, who know that they will not have to make payments unless their education pays off. This may encourage some prospective students who are on the fence about going to college to pursue higher education.

In some ways, an ISA is easier for students to understand than a loan. The federal student loan program has a wide array of repayment options, each with its pros and cons, and surveys show that most students are not aware of many of the options.[18] Under an ISA, all students use the same repayment structure; this makes it less likely that a lack of knowledge about repayment options will lead students to make an irrational decision.

ISAs could also help solve the loan aversion problem, wherein students who would benefit from additional funds in college nonetheless refuse to take on debt. A survey commissioned by the American Enterprise Institute showed that while students were initially skeptical of ISAs, many changed their minds after learning more about the model.[19]

The ISA is not a perfect model for higher-education finance. A persistent danger is adverse selection, wherein students who expect to have high earnings opt for traditional student loans in order to lower their total payments. This could limit investors’ ability to recoup losses from students who do worse than expected. Servicing costs, a further ISA-related worry, are higher than for traditional loans because students’ incomes must be continually updated and verified.

Furthermore, while ISAs will probably reduce nonpayment rates relative to traditional loans, there is no guarantee that they will solve the repayment crisis entirely. Even though ISA payments are guaranteed to be affordable, students must still be inclined to make them. Surveys show that individuals consider education-finance obligations a low priority relative to other expenses.[20] In addition, some students refuse to pay their loans because they feel cheated by their institutions, not because the debt is unaffordable.[21] In other words, ISAs merely guarantee affordable payments; they cannot compel students to make the payments.

ISAs may fall victim to other problems that bedevil student loans. As with colleges marketing federal student loans as “awards,” ISA providers might fail to accurately convey the character of the financial obligation to students. ISAs will also require basic consumer protections and disclosure rules to guard against abuse by providers. But these dangers are present with any financial product and are no reason to single out ISAs for special scrutiny.

The downsides we identify may be more or less critical, depending on which entity finances and administers an ISA. There are three main options: private financiers, academic institutions, and the federal government.

Who Should Run ISAs?

Private financiers remain a relatively small share of the American ISA market. Some companies, such as Lumni, offer ISAs to students but are unaffiliated with those students’ colleges. Though this type of arrangement remains relatively uncommon, it has made larger inroads in other nations, such as Chile and Colombia.[22]

In the U.S., it is more common for an academic institution to offer students an ISA directly. Several traditional colleges provide ISAs, of which the most prominent is, as noted, Indiana’s Purdue University. New educational models, such as coding academies, also offer students ISAs in lieu of tuition bills. (Usually, a school partners with an independent company, such as Vemo Education, to design and operate the ISA.)

However, most third-party and institution-based ISAs suffer from a scope limitation. Students who use a private ISA are typically expected to take on federal student loans as well (provided they are eligible for federal aid). Most colleges encourage students to use ISAs only after they have exhausted their eligibility for federal (“Stafford”) loans, pushing ISAs as an alternative only to private loans and Parent PLUS loans (federal loans to parents to finance their children’s undergraduate education), which have higher interest rates.

Because Stafford loans are subsidized, it would be irrational for students to use an unsubsidized ISA instead. Generally, the only institutions where ISAs are the primary source of financing for students are those ineligible for student aid, such as coding academies.

The federal government, another potential administrator, has not yet introduced an ISA program. While the federal student loan program’s income-based repayment (IBR) option incorporates some features of an ISA, such as payments that vary with a borrower’s income, it is not a true ISA. Unlike federal loans, ISAs do not have a loan balance or an interest rate. This difference is crucial for two reasons. First, borrowers in IBR may see their loan balances grow even as they make payments if those payments do not exceed interest accrual. This does not happen under an ISA, which has no balance to grow. Second, high-earning IBR borrowers will never owe more than principal plus interest. However, it is a feature of ISAs that high-earning recipients will pay back more than they would under a traditional loan, in order to cross-subsidize their lower-earning peers (though many private ISA programs cap the overall amount that a student will repay at some multiple of the total amount funded).

Another key difference is that under IBR, borrowers always pay the same share of income toward their loans, regardless of how much they borrowed initially. But ISAs often charge students a higher share of income if they receive a greater amount of funding, in order to discourage excessive financing.

For now, ISAs remain limited to a small corner of the private market, though, as noted, the model has grown rapidly in recent years. In his essay on the role of government in education, Friedman wondered why equity finance for education was not more popular, despite its theoretical superiority to debt. The difficulty of administering such a scheme was one potential issue, which led Friedman to call for a budget-neutral government program to provide ISAs to students.

Such administrative difficulties are fewer now than they were in 1955, thanks to technology. But there may still be a case for a government-funded ISA to replace the federal student loan program. If political reality dictates that the government must have a major role in higher-education finance, a national ISA would be superior to a national student loan program. There are other arguments in favor of a government program. A purely private ISA market might not provide an acceptable level of access to higher education. And if it became the default option for most students, a government-run ISA would mitigate adverse selection.

However, the federal government running an ISA could make the same errors that it has made administering the federal loan program, such as confusing the borrowers with muddled explanations of program terms. Another danger is that Congress might set the parameters of a public ISA in the wrong places. Make the program too generous, and it could waste taxpayer money; make it too stingy, and students might not participate. Seemingly small changes in ISA terms can make big differences to the overall cost of the program.

Though ISAs are simple in theory, they have several parameters that policymakers must pin down before they can create an effective program. Necessary terms include the income-share rate: the percentage of income that a student must pay toward his obligation. The length of the ISA obligation is another important parameter: How long should a student pay before his obligation is extinguished?

Beyond these parameters, an ISA’s designers must answer other questions, including:

- Should the income-share rate vary with the amount received?

- Should the terms vary with a student’s institution or field of study?

- Should students be excused from making payments if their income falls below a certain level? (Most private ISAs include this feature.)

- If yes, where should that threshold be set?

- Should there be a cap on the amount of funding that a student can receive?

- What about a cap on total payments, to reduce adverse selection? (Again, a feature in most private ISA programs.)

With so many balls in the air, it’s easy for policymakers to get it wrong. Friedman anticipated this problem. “For such reasons as these,” he wrote, “it would be preferable if similar arrangements could be developed on a private basis by financial institutions in search of outlets for investing their funds, non-profit institutions such as private foundations, or individual universities and colleges.”

In other words, before the federal government considers a national ISA, the prudent course is to learn from the experience of private organizations. Further private experimentation with ISAs can give researchers and policymakers a better idea of how the program should be designed and where its parameters should be set. Fortunately, enough institutions now offer ISAs that we can ascertain how the market will take shape.

Academic Institutions Are Leading the Way

The most prominent institution-based ISA program is Purdue’s “Back a Boiler” initiative. Spearheaded by President Mitch Daniels, a former governor of Indiana, the program has served several hundred undergraduate students and disbursed nearly $10 million in funding.[23]

Back a Boiler is meant to supplement low-interest federal loans and only replaces private and Parent PLUS loans. It is available to students in their second year, or later, who have declared a major (the program varies the terms that a student receives, according to his major). Students cannot receive more than $33,000 throughout their college career.

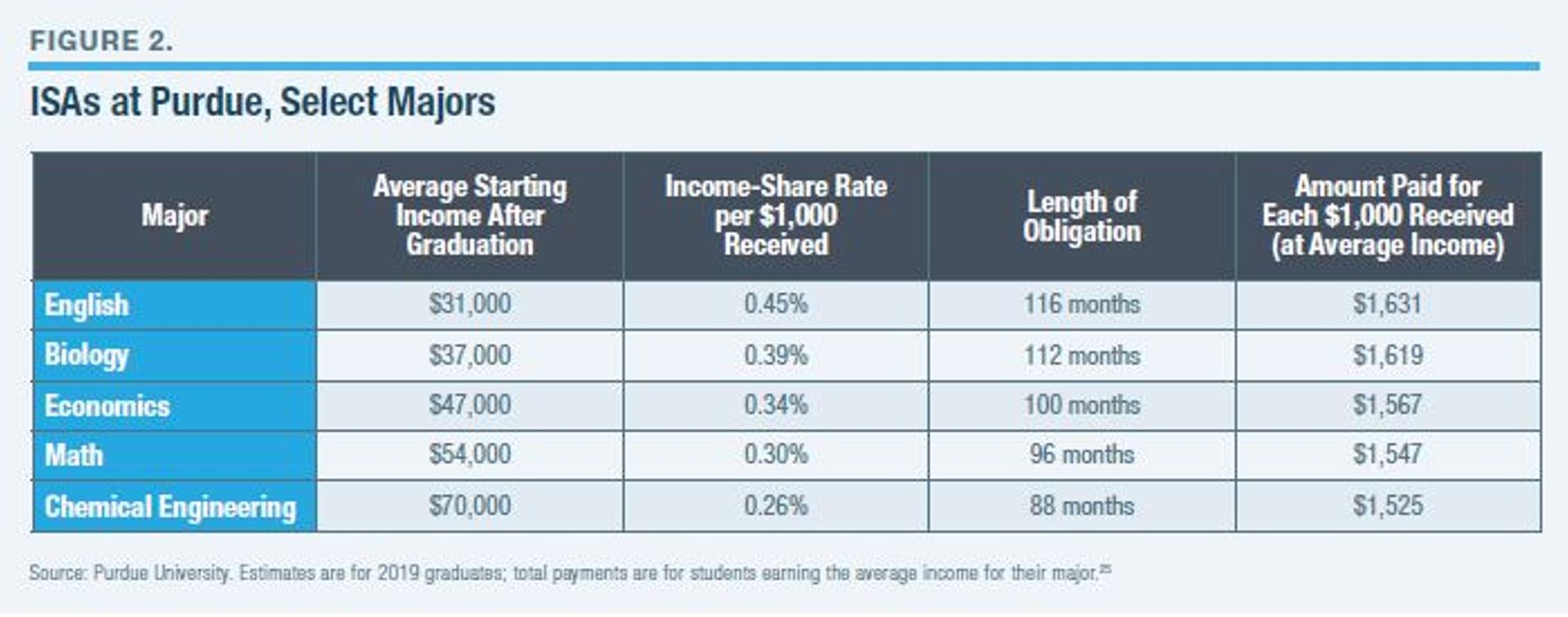

Figure 2 displays ISA terms for several majors at Purdue, along with total payments as estimated by the university. More remunerative majors carry a lighter burden. A chemical engineering major in the class of 2019 pays 0.26% of his income for every $1,000 received, and his obligation lasts for 7 years and 4 months after graduation. An English major with a lower expected income receives less generous terms: he must pay 0.45% of income for every $1,000 received, and his obligation lasts for 9 years and 8 months.[24]

Despite the stricter terms, Purdue estimates that the average English major will pay only slightly more in total than the average chemical engineering major, due to the English major’s lower income. Students who earn the average income for their major will end up paying back $1,500–$1,600 for every $1,000 received, even though average incomes vary widely across majors.

More favorable terms for higher-earning majors might encourage students who expect high salaries after graduation to use an ISA rather than a traditional student loan. Keeping high earners in the program could make an ISA program more sustainable in the long term, though it is up for debate whether Purdue’s strategy is the best way to fight the adverse selection problem.

Daniels has argued that varying ISA terms by major will help students choose the right fields of study. “As an ISA market develops, students will benefit further from the market signaling that tells them which fields are most likely to be rewarded economically,” he wrote in a 2015 Washington Post op-ed. “A chemical engineer, for instance, is likely to negotiate a much lower repayment rate or shorter repayment term than her art history roommate.”[26]

While Purdue has achieved the highest-profile ISA program in the U.S., this feature of the program (varying terms by major) is unique. The University of Utah’s recently introduced ISA program, for example, varies the length of the obligation based on major but not the income-share rate.[27] Indeed, most ISA programs at traditional four-year colleges that we reviewed do not change ISA terms for students depending on major or even the amount received.

Not all college leaders share Daniels’s perspective that ISA designs should nudge students toward more lucrative majors. Some argue that ISAs provide important protections for those who pursue lower-earning fields of study. Mark Volk, president of Lackawanna College, which launched an ISA in 2017, writes that ISAs “level the playing field” across majors, since “the less a student earns, the less he or she must pay—easing the burden of payment for those in lower-paying fields.”[28]

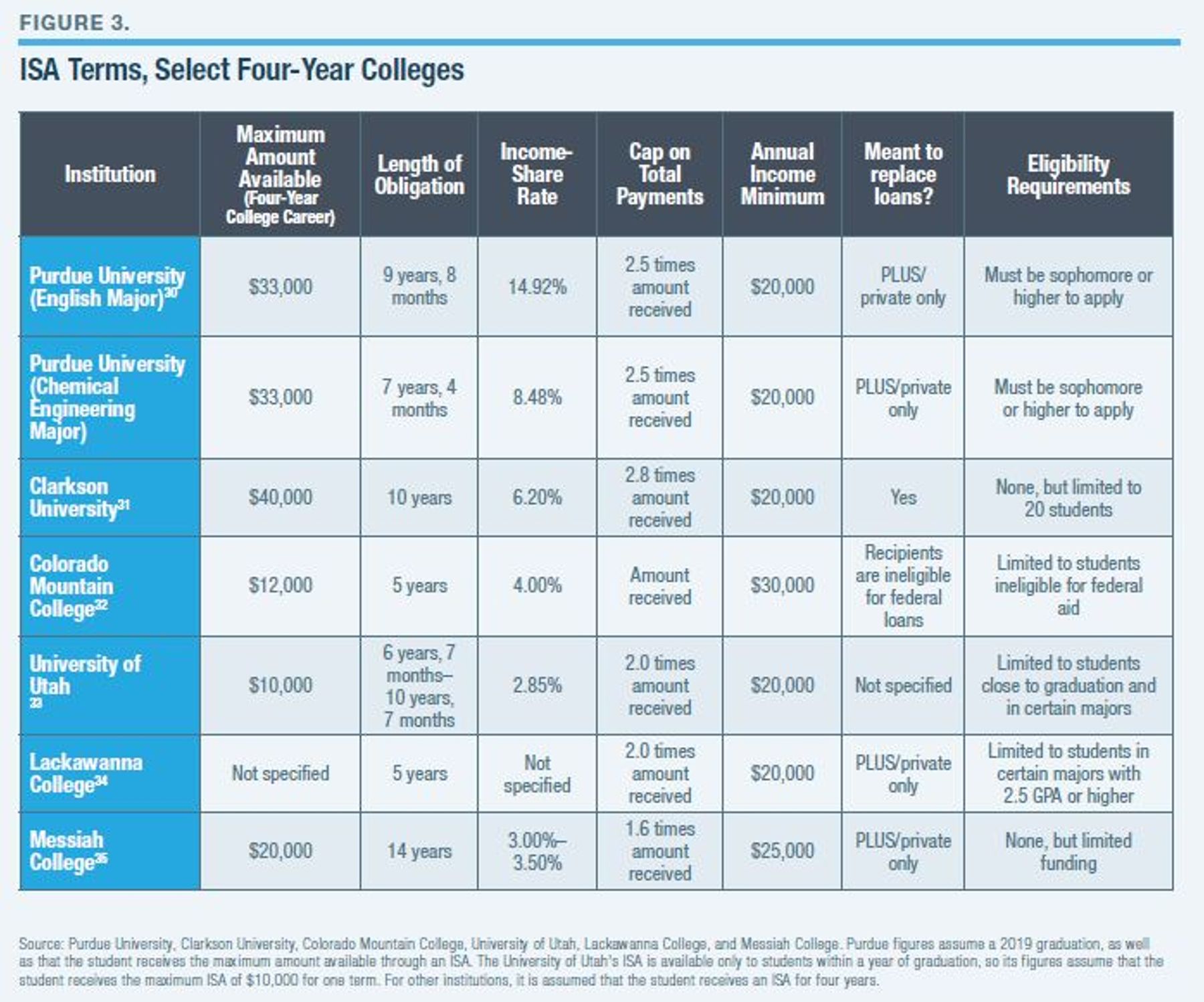

Figure 3 displays the terms of ISA programs at several traditional four-year colleges. For the most part, ISAs at these schools are meant to supplement, not replace, subsidized federal student loans. The exceptions are the ISA programs at Clarkson University in New York and Colorado Mountain College. Clarkson explicitly markets its ISA as “an option [for students] to pay for their education without incurring debt.”[29]

Colorado Mountain College’s program, Fund Sueños, is available only to students who are ineligible for federal financial assistance. Specifically, the ISA targets noncitizen “DREAMers” authorized to remain in the U.S. under the Deferred Action for Childhood Arrivals (DACA) program.[36] Colorado had 16,000 DACA recipients as of August 2018, all of whom are ineligible for federal loans, making this population a prime target for nongovernment college-finance programs such as ISAs.[37]

Purdue’s Back a Boiler program is the most variable of the programs we analyzed. Most programs have the same income-share rate regardless of a student’s major or how much ISA funding he receives. For instance, an English major at Purdue pays an income-share rate of 4.52% if he receives $10,000 in ISA funding, but pays 14.92% if he receives the maximum of $33,000. By contrast, an ISA-participating student at Clarkson University pays a flat income-share rate of 6.2%, assuming that he receives ISA funding for all four years of college.

Most ISA programs also incorporate a cap on total payments in order to mitigate adverse selection. Under a payment cap, the student stops making ISA payments once his total payments reach a certain proportion of the ISA’s initial funding. Messiah College caps payments at 1.6 times the amount received; so if a student received $5,000 in funding, he would stop paying after his total payments reached $8,000. This “cap ratio” ranges from 1.0 at Colorado Mountain College to 2.8 at Clarkson. If a student does not reach the cap, he simply continues making payments until his ISA term expires.

Another common feature of ISAs is a minimum-income threshold for repayment. Students are not obligated to make payments if their incomes fall below a certain threshold (generally $20,000 but sometimes higher). Some programs also allow students to postpone payments in special circumstances, such as medical leave. Zero-payment periods are generally incorporated as “deferments” that do not count toward a student’s ISA term; if the ISA term is five years, the student must make five years of positive payments. The deferment feature helps limit schools’ losses on students who meet temporary financial distress while not placing an undue burden on students.

Details on the financial performance of institutional ISAs are not public, but variations in program design suggest that institutions create ISAs with different financial goals. At Purdue, students of average incomes are estimated to pay back 1.5–1.6 times the amount received. Back a Boiler may thus be budget-neutral or even turn a profit for Purdue. By contrast, at Colorado Mountain College, ISA recipients never pay back more than the amount received. This means that the program, which is philanthropically funded, is a money-loser for the institution.

Even money-losing ISAs may be attractive prospects for institutions that receive philanthropic funding. Relative to scholarships, a dollar of philanthropic funding has a much broader impact if channeled into an ISA. Once an institution spends a dollar on a scholarship, the dollar is gone. But ISA funding is continually replenished as students pay back into the program. Institutions must renew scholarship funding every year; but with an ISA, they need raise only enough money to cover whatever subsidy they wish to offer students.

Consider a hypothetical institution that wants to offer a $10,000 line of funding to a student. At an endowment draw rate of 5%, that institution would need $200,000 in the bank to offer that $10,000 as a scholarship. If instead it offered the funding as an ISA, former students’ ISA payments could defray some of the cost of new ISAs. Even if payments from old ISAs covered only 80% of the cost of new ISAs, the institution would need just $40,000 in the bank for every $10,000 ISA that it offers. Philanthropists’ money would go much further.

A certain class of academic institutions, however, often runs ISAs with the intention of turning a profit. At these institutions, ISAs have become the norm rather than the exception.

ISAs at Coding Academies

In recent years, accelerated training providers have grown in popularity as an alternative to traditional higher education, usually at the graduate level. The most common type of institution in this category is the coding academy, or “coding boot camp,” which teaches students computer programming skills and then places them in lucrative software engineering and web development jobs. Programs have short durations, sometimes measured in weeks.

The coding academy market has tripled in size since 2014, with the annual number of graduates rising from 6,700 to 20,300 in the last four years.[38] Most academies boast high job-placement rates, and many provide extensive assistance in helping graduates find work. Some even help students write cover letters and stage mock job interviews. The close link between education and work at coding academies makes them uniquely suited for the ISA model.

Moreover, most coding academies are unaccredited and thus ineligible for federal student aid. Students must therefore turn to alternative sources of funding. It has become common—even standard—for academies to offer their students ISAs with little to no tuition paid up-front as an option to finance their education.

Coding academies have found that the ISA model is a critical tool to build trust among their students. Since ISA payments are commensurate with a student’s income after graduation, a coding academy’s revenue depends on how much its graduates make. This aligns the incentives of school and student, and it signals to prospective entrants that the school has a stake in their future success. As Lambda School CEO Austen Allred writes: “The economic incentives must be structured so that a student can enter [a coding academy] without worrying if their lives will be over should it not work out.”[39]

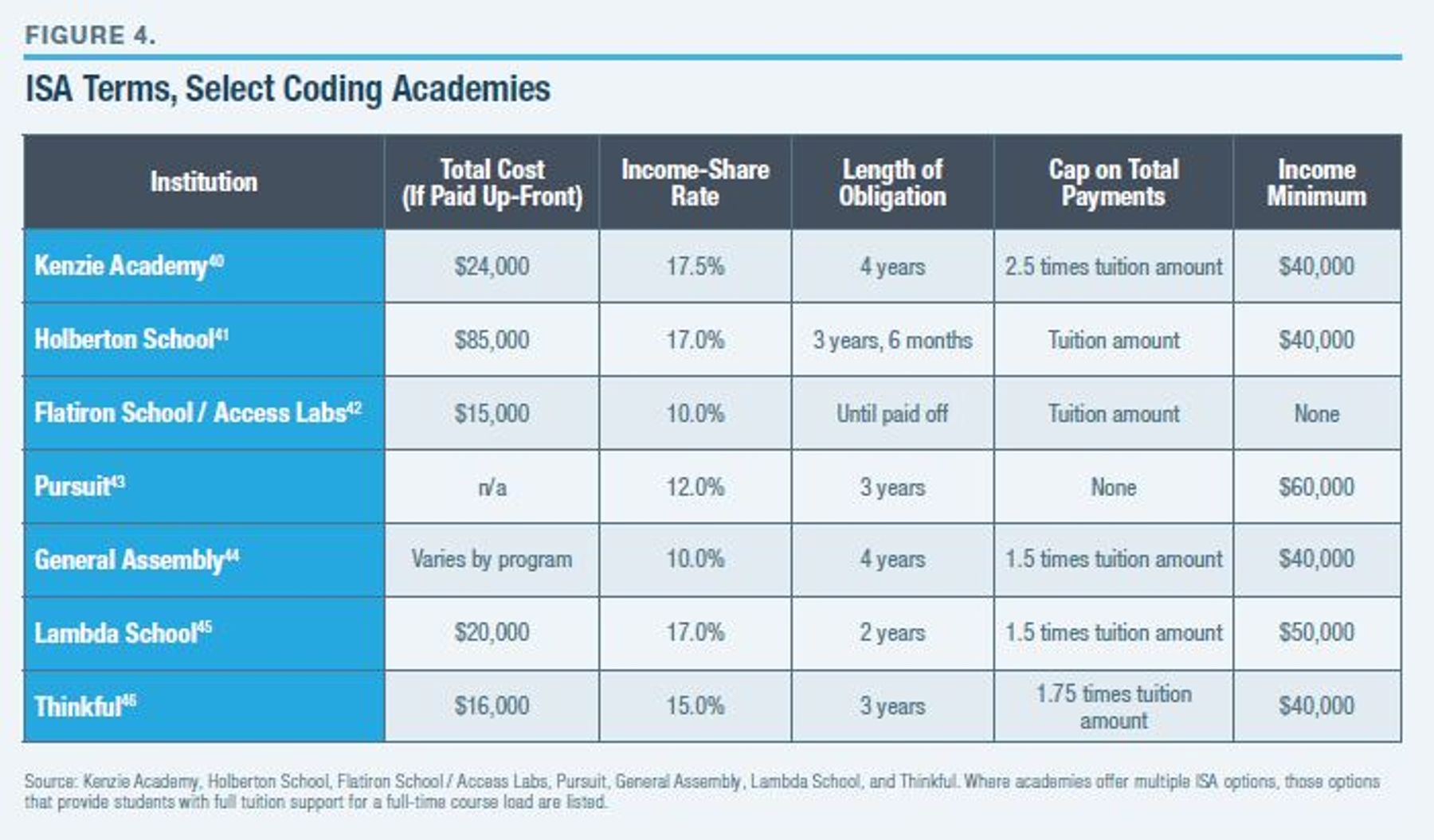

ISAs at coding academies differ markedly from those at traditional four-year colleges (Figure 4). Students are obligated to pay their ISAs for a much shorter period—at Lambda School, the term is just two years. Yet the income-share rates are much higher, usually in the double digits. This model is consistent with an emphasis on quickly placing students in high-paying jobs.

Another key difference is the minimum-income threshold below which students are not required to make payments. These thresholds are generally much higher than they are in the traditional college sector; at Pursuit, students pay nothing until they reach $60,000 in annual earnings. These high minimum-income thresholds make the high income-share rates more tenable. (Years of zero payments do not count toward the student’s ISA term.)

On the other hand, this arrangement sometimes creates “income cliffs” for students. At Lambda School, a student pays nothing if he earns $49,000 per year—but as soon as his income rises to $50,000, his annual payment is $8,500, since the 17% income-share rate applies to his entire income.[47] This creates a disincentive for students to increase their earnings. While this may not be a concern at coding academies, which tend to attract students determined to hold high-paying jobs, this model could create problems if it were expanded to other sectors of higher education.

A similarity between ISAs in traditional higher education and those at coding academies is the existence of total payment caps. These caps range from 1.0 to 2.5 times the up-front tuition at the academies that we analyzed. (A few academies do not have caps.)

A coding academy student who uses an ISA and earns a typical salary postgraduation will generally pay back more than the academy’s cost of tuition. For instance, a Lambda School graduate earning $70,000 per year pays about $24,000, 1.2 times Lambda School’s tuition of $20,000. (According to Course Report, an industry research group, the average salary for a new coding academy graduate is approximately $71,000.)[48]

Many students, even average earners, hit the cap on total payments—suggesting an important role for this feature of the program in mitigating adverse selection. However, the ISA also provides important downside protection: if a student earns less than $40,000 for several years after graduation, he will almost certainly not pay back the full cost of tuition.

While ISAs have made their mark on the world of coding academies, they still face significant barriers should they expand beyond their current niche. Some of those barriers are structural—a budget-neutral private ISA simply can’t compete with a subsidized federal student loan program—but smart policy can remedy others.

Barriers to ISAs

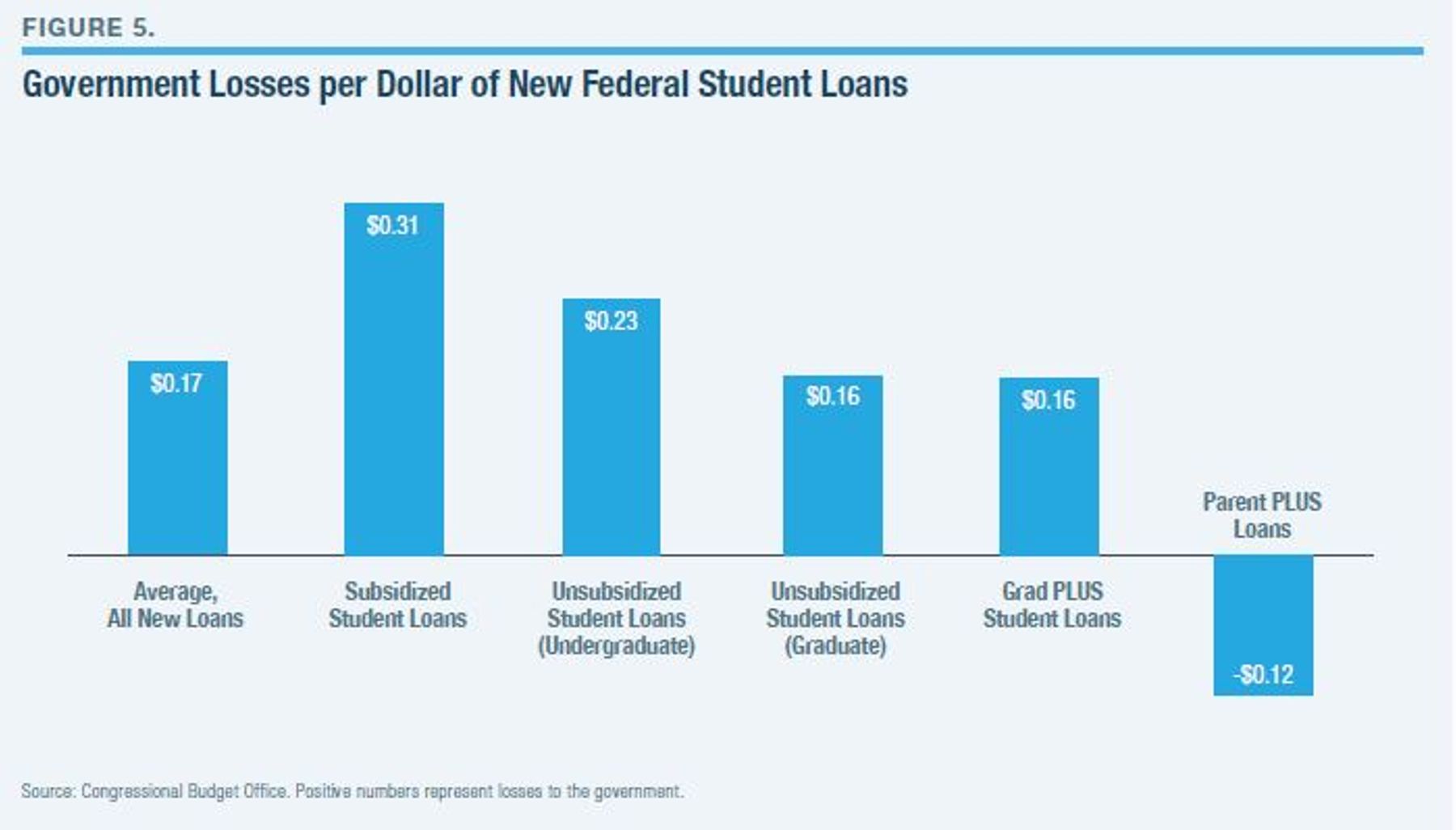

A private ISA market will never be competitive with subsidized federal student lending. The federal government offers student loans at a subsidy, taking a loss of 17 cents for every dollar in new loans issued (Figure 5).[49] The government takes even bigger losses on loans made to undergraduates. Only on loans made to parents of undergraduates, which, as noted, carry a higher interest rate and lack many repayment benefits, does the government turn a profit.[50]

While the federal government can continue to take losses on its loan program, private ISA investors must turn a profit eventually. To do so, they must offer worse terms to students than the federal government—i.e., it would be irrational for students to use private ISAs while leaving federal student loan money on the table. Philanthropically funded ISAs might be able to offer competitive terms, but institutions might not be able to keep up with the burden of constantly raising money to maintain ISA subsidies. Clarkson’s ISA, which is intended to replace all traditional student loans, will be a key test for this model.

For these reasons, many institution-based ISA programs do not aim to replace student loans to undergraduates. Purdue and several other traditional colleges intend for their ISA programs only to replace Parent PLUS loans and traditional private student loans. Other schools, such as Colorado Mountain College and most coding academies, target ISAs at students or programs that are not eligible for federal aid.

In addition, students who exhaust federal undergraduate student loans may be wary of taking on a second financial obligation in the form of a private ISA. While ISAs have become commonplace where federal student loans do not exist, those markets are limited.

Even setting aside the federal loan program, ISAs face other artificial barriers. ISAs lack an explicit legal framework under which to operate. Investors are rightly hesitant to enter a market where consumer protections and enforcement have not been clearly established and the right to collect ISA payments may be challenged. Investors may be exposed to adverse enforcement actions or lawsuits stemming from the misapplication of laws and regulations tailored to loan products but ill-suited to ISAs. The last thing an investor wants to do is sink millions into an ISA fund, only to be put out of business by an overzealous state attorney general.

As with any financial innovation, regulators can be hostile to ISAs. New York State’s Education Department issued a highly prescriptive “policy guideline” on ISAs.[51] Among others, it declared that certain ISA funders could not collect more in payments than the price of tuition. (This is a curious standard; students who fund their tuition with traditional loans pay back the price of tuition plus interest.) As noted, an essential feature of ISAs is that high-earning students pay back more than they receive in funding, in order to cross-subsidize lower-earning students. If the ability of ISA administrators to collect those excess payments is removed, the whole model falls apart.

An American Enterprise Institute report identified three areas where policymakers need to create legal clarity for ISAs.[52] First, Congress must assign ISAs to an appropriate regulator to protect students from abuses while providing a consistent, holistic approach to oversight that would allow the ISA market to develop. Second, because disclosure rules and usury laws are designed for traditional loan products, the law must specify how those protections should apply to ISAs. Third, lawmakers must decide how ISAs will be treated in bankruptcy and under the tax code.

Former congressman Luke Messer (R-IN) introduced a bill in the 115th Congress to clarify many of these legal uncertainties.[53] It sets down maximum income-share rates and term lengths and authorizes the Consumer Financial Protection Bureau to set down antidiscrimination and consumer protections in regulation. Importantly, the bill preempts state laws in favor of a single federal standard. The bill attracted 18 cosponsors from both parties.

Besides such artificial barriers, private ISAs face roadblocks inherent in their design. These include adverse selection and servicing costs, problems that were identified earlier. To address the latter, many ISA programs have opted for very short terms, particularly at coding academies. Short terms reduce servicing costs and may even align with students’ preferences—borrowers with traditional student loans have shown an inclination to discharge their obligations as quickly as possible.[54]

Still, economic theory generally holds that the term of a financial obligation should align with the value of the asset being financed. The highest returns to a college education typically occur during mid-career, often decades after a student graduates from college.[55] Though the optimal term length for an ISA could be 20–30 years, administrative costs, student preferences, and impatient investors wanting more immediate returns may conspire to shorten term lengths dramatically. This is unfortunate: longer-term ISAs, with much lower income-share rates, may be better suited for majors such as liberal arts, where graduates take longer to reach peak earnings.

Conclusion

In the short term, Congress should lower existing barriers to ISAs by providing them with legal clarity. Basic consumer protections are important, but lawmakers should be careful to provide flexibility for experimentation, lest regulators strangle this infant market in its cradle. Academic institutions should continue to experiment with ISAs as an alternative to Parent PLUS and traditional private loans, following the lead of institutions such as Purdue University and the University of Utah.

In the longer term, Congress should examine the ISA model as a potential replacement for the federal student loan program. Yet more information is needed to ensure that policymakers get the design specifics of such a program right.

The small private ISA market already offers several lessons. Most programs incorporate caps on total payments—suggesting that this is a key component of ISAs to reduce adverse selection, even though it limits the benefits of cross-subsidization. The optimal level at which to set the cap is unclear (Colorado Mountain College sets its cap equal to the amount received, while Purdue University has gone as high as 2.5 times the amount received).

Minimum-income thresholds are also commonplace in the private market, providing protection for students who get into financial trouble. However, private programs usually employ a cliff, wherein students who earn just above the minimum-income threshold must pay the income-share rate based on their entire income, while students who earn just below the threshold pay nothing. This feature improves the financial solvency of ISA programs but creates a strong earnings disincentive. Many private programs have blunted that disincentive by not counting months of zero payments toward the discharge of a student’s ISA obligation. This design is different from the approach taken by the income-based repayment option available on federal student loans, and it may be superior.

Not all features of private ISAs should be incorporated into a national program. For instance, most private ISAs do not vary the income-share rate with the amount received (Purdue is an exception). However, private ISAs are often tied to a particular educational program, where the amount received varies little among recipients. Yet a national ISA would serve many different sorts of programs at the same time—i.e., participants would have varying financial needs. Therefore, a national ISA should vary the income-share rate with the amount received in order to discourage over-financing. This would provide students receiving low amounts of financing with a less burdensome income-share rate than those receiving large amounts, who would tend to be graduate and professional students with stronger earnings capacity. This aspect of a national ISA would be far superior to current IBR programs, which impose the same repayment rate on all borrowers, combined with principal forgiveness after a certain number of years that primarily benefits high-balance borrowers.

Because a national ISA would be different from private ISAs in important ways, policymakers can learn only so much from existing programs. For instance, most private educational providers that use ISAs are selective, while a national program would presumably be open to all students attending accredited institutions and meeting other basic requirements, just as federal student loans operate today.

One benefit of institution-based ISAs is that colleges have a direct financial stake in their students’ success after college, creating a stronger incentive for institutions to provide a worthwhile education. This benefit would disappear under a national program, unless the program incorporated some form of risk-sharing. For instance, colleges could provide some portion of the ISA funding from their own resources, sharing, in proportion, ISA returns after students graduate. Or the government could impose penalties on colleges where students’ ISA payments do not meet an acceptable benchmark. There are many ways to leverage a national ISA to improve incentives for colleges.

To better understand how a national ISA could function, Congress could authorize federal ISA pilot programs at certain institutions. Schools would volunteer to participate, giving up some access to traditional federal student loans in exchange for ISA funding. Multiple pilot programs with varying terms could run simultaneously to gauge how competing ISA designs stack up against one another. Congress could then set about designing a national ISA to fully replace the federal student loan program.

Milton Friedman closed his famous essay on education by noting that, with well-designed policy, “government would serve its proper function of improving the operation of the invisible hand without substituting the dead hand of bureaucracy.” Policymakers should heed Friedman’s advice by not rushing into a radical overhaul of the federal government’s role in higher education. Start instead with a federal ISA pilot program and continue evaluating private ISAs. As Americans increasingly tire of student debt, the appeal—and promise—of income-share agreements will only grow.

Endnotes

About the Authors

Sheila Bair was the 19th chairman of the U.S. Federal Deposit Insurance Corporation, from 2006 to 2011. She has also served as president of Washington College, in Chestertown, Maryland; as a senior advisor to the Pew Charitable Trusts; as the Dean’s Professor of Financial Regulatory Policy at the University of Massachusetts at Amherst; as Assistant Secretary for Financial Institutions at the U.S. Department of the Treasury; as Senior Vice President for Government Relations of the New York Stock Exchange; as a Commissioner and Acting Chairman of the Commodity Futures Trading Commission; and as Counsel to Senate Majority Leader Robert Dole. Bair holds a B.A. and J.D. from the University of Kansas.

Preston Cooper is an education research analyst at the American Enterprise Institute. Previously, he was a fellow at the Manhattan Institute. Cooper is a contributor to Forbes.com, and his writing has also appeared in the Wall Street Journal, Washington Post, Seattle Times, U.S. News & World Report, Washington Examiner, Fortune, RealClearPolicy, and National Review. He holds a B.A. from Swarthmore College.

This report was written as a part of MI's Solutions from Beyond the Beltway series

Photo: BrianAJackson / iStock / Getty Images Plus

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).