Moving Left A Study of Ideological and Demographic Change Among Federal Reserve Bank Directors

Photo: Sparky2000 / iStock / Getty Images Plus

Executive Summary

The 12 Federal Reserve Banks are crucial for American monetary policy and financial regulation. Each bank is overseen by a board of directors who also select the President, who manages the bank. The directors are supposed to reflect all sectors of the American economy and be nonpolitical.

In recent years, however, directors have leaned increasingly left ideologically, and they are more likely than in the past to be from consumer & community, and labor groups. While the Federal Reserve Banks have rapidly increased the racial and gender diversity of their directors since 2010, they have become less politically diverse. The directors are also now less likely to have had the crucial banking experience needed for some of their oversight roles. These changes have inhibited the ability of the Federal Reserve Banks to provide strong and dissenting voices on monetary or regulatory policy.

Key findings:

- The share of directors donating only to right-leaning candidates decreased from 2010 to 2023 and has dropped from 24% in 2015 to less than 8% in 2023. There has also been a decline in bipartisan donations and an increase in exclusively left-wing donors, who now make up 34% of all directors.

- Representation from consumer & community groups and labor groups has increased since 2010, collectively constituting about 20% of nonbank directors in 2023, compared with just under 10% in 2010.

- The share of board chairs and deputy chairs with mandated “tested banking experience” decreased overall from 44% in 2010 to 29% in 2023, with sharp decreases commencing in 2021.

- Since 2010, there have been fewer directors with an academic background in economics, finance, and banking, while there has been an increase in directors with a public policy academic background.

- During 2010–23, the share of nonwhite directors increased from 13% to 44%. The share of female directors increased from about 19% to 44% during the same period.

- Increases in nonwhite director numbers were concentrated in nonbank director positions. Nonwhite directors disproportionately represented the consumer & community and labor sectors. This was also true for female directors, but to a lesser extent.

While the current process for selecting Federal Reserve directors has focused on racial and gender diversity, more attention should be given to ensuring that directors are not representing only one side of the nation’s partisan divide. Directors should also be more representative of America’s economic sectors, which would help them speak to the economic conditions of their respective regions. The requirement of “tested banking experience” should be more rigidly defined and adhered to when selecting chairs and deputy chairs.

The Federal Reserve Board of Governors in Washington plays an essential role in Federal Reserve Bank management by, among other powers, selecting Class C, nonbank directors, whose backgrounds have changed more dramatically than other directors in recent years. Rather than trying to overcorrect for a past lack of racial or gender representation, the Board of Governors and other policymakers should cultivate directors who can improve Reserve Banks’ core roles and serve as countervailing voices in the making of monetary and regulatory policy.

Introduction

Most of the attention paid to the Federal Reserve is, understandably, focused on the chairman and the Board of Governors in Washington, DC. These seven officials, along with a rotating group of 12 regional Federal Reserve Bank Presidents, participate in enacting monetary policy in the Federal Open Market Committee (FOMC).

Federal Reserve Bank directors are less well known but play important roles. Each regional bank has nine directors who oversee the operation of the bank and select the bank’s President and Vice President, with the consent of the Board of Governors. According to the Fed, the directors’ jobs include “overseeing the management of the Reserve Banks,” participating in the “formulation of national monetary and credit policies,” and “acting as a ‘link’ between the government and the private sector.”[1] Regional Reserve Banks also monitor the economic and financial conditions of their respective regions. They collect data, conduct regional research, supervise member banks, and share information. Beyond their monetary and regulatory roles, the Reserve Banks distribute currency and process payments.

Fed doctrine stipulates that directors should provide “representation from a wide variety of occupational sectors, demographic groups, and geographic areas.”[2] This is because directors are informational conduits who provide insights about different sectors of the economy, which inform monetary policy recommendations.

The nine Reserve Bank directors are divided evenly into three classes: A, B, and C.[3] Class A directors are nominated by local member banks from the Reserve Bank’s district and represent the interests of these member banks. According to the law, Class B and C directors are elected “to represent the public with due … consideration to the interests of agriculture, commerce, industry, services, labor, and consumers.”[4] Class B directors are elected by member banks but cannot be from member banks themselves. Class C directors are appointed by the Board of Governors.

Class B and C directors perform various functions distinct from Class A directors. Class A directors are excluded from participation in the selection of bank Presidents because of a perceived conflict of interest, so Class B and C directors nominate the President and Vice President for approval by the Board of Governors in Washington. Additionally, two Class C directors serve as the chair and deputy chair of their boards. This grants them, as the Federal Reserve itself notes,“significant management oversight responsibilities.”[5] The chairs and deputy chairs are agenda setters, reviewing the yearly objectives of their Reserve Bank. They review the Reserve Bank’s budget and performance. They also assess the performance of the Reserve Bank’s President and Vice President. Chairs are required by law to possess “tested banking experience,” which, the Fed notes,“has been interpreted as requiring familiarity with banking or financial services.”[6] Deputy chairs, by logical extension, should also possess “tested banking experience,” as they historically tend to succeed chairs and can serve in the chair’s absence.

According to the Fed, directors “should not consider themselves to be champions of any special interest or constituency.”[7] Rather, they should “act objectively and in the public’s best interest.”[8] Thus, directors are cautioned to “not engage in any political activity or serve in any public office that might associate the Federal Reserve with any political party and partisan political activity.”[9]

Although there is no legal mandate to hire sexually or racially diverse directors, the Federal Reserve has made demographic diversity among directors a goal. The Fed’s website tracks the gender and racial diversity of Reserve Bank and branch directors, and it shows a rapid increase in such demographic diversity over the past 15 years.[10]

Methodology

This report presents the results of a comprehensive investigation of directors from all classes and all Federal Reserve Banks from 2010 to 2023. An accompanying database details the political donations, professional positions, industry sectors, educational backgrounds, and demographic details of various directors.

This database includes additional elements and extends earlier databases of Federal Reserve directors, including one created by Peter Conti-Brown and Kaleb Nygaard in “The Federal Reserve System: Diversity and Governance” and one created by Gabrielle Elul that measures political leaning.[11] This database adds data on director political donations, as well as on tested banking experience, and it extends earlier analyses up to 2023.

To estimate director ideology, we use two methods. One is relatively simple, while the other is more complex and mirrors methodologies employed in the existing literature.

First, we look at political donations for all directors. Using Federal Election Commission (FEC) filings, the authors determined whether donations were made (with no donations categorized as “none”). If they were made, they determined whether these donations were “left,” “right,” or “unclear.” Donations are considered partisan if they went to a Republican or a Democratic candidate or party-tied organization or Political Action Committee (PAC).[12] “Unclear” was primarily used for donations to company and industry PACs that appeared to have no specific partisan agendas. From this, we can determine how many directors were right-only, left-only, or bipartisan in their donations. The threshold for a bipartisan donation was low, requiring only that a director made at least one donation to each party or a bipartisan PAC. Donations were considered for the five years prior to when a director started his or her term through the end date of his or her term.

The second methodology uses campaign finance scores obtained from the Database on Ideology, Money in Politics, and Elections (DIME), which is also based on political donations.[13] A campaign finance score is a standardized measurement of ideology, wherein a score above zero is more conservative and a score below is less conservative.[14]

To understand the representation of various sectors and interests, this report assessed the companies and organizations at which directors held leadership positions. Sectors were based on those listed in the Conti-Brown and Nygaard report. Broad sectoral analysis was performed for “nonbank” directors (Class B and C) because the structure of the director system makes the proportion of directors from the banking sector (Class A) largely fixed over time, accounting for about a third of all directors. However, our analysis of sectoral distribution parsed by race and gender includes Class A directors.

Again following Conti-Brown and Nygaard’s framework, we determined directors’ education level and background, including the various degrees a director held, what area of study that degree concentrated in, and the institution from which the degree was awarded. The highest level of education that a director received, or “terminal degree,” was used to determine the director’s broader academic “area of focus.” This report’s accompanying database contains three columns for various degrees.[15]

We assessed whether Class C directors had “tested banking experience,” with each director classified as “yes,” “no,” or “adjacent.” Industry experience and education were considered when making determinations. A “yes” categorization, for example, might include an individual with a strong educational background in finance or experience in the banking industry, or a high-level academic with expertise in economics and business. An “adjacent” score might denote a successful business magnate or entrepreneur with perhaps an informal understanding of the financial system. A “no” would denote an individual with an evident lack of experience in banking or financial services. Such an individual might have a career in social services or government administration.

This investigation categorized Fed directors based on race and gender. To corroborate its methodology, this report cross-referenced its determinations with Gender and Racial/Ethnic Diversity Statistics published by the Federal Reserve.[16]

Rapid Change in Directors

Fed directors have become increasingly left-leaning, activist, and demographically diverse since 2010. These changes are connected to increased representation from sectors such as community, consumer & community, nonprofit, and labor, from which nonwhite directors are more likely to hail. Nonbank directors are much less likely to represent “traditional” industries and are more likely to be from politically active backgrounds than in the past. In addition, an increasing proportion of nonbank directors come from public policy and business backgrounds.

Leaning Left

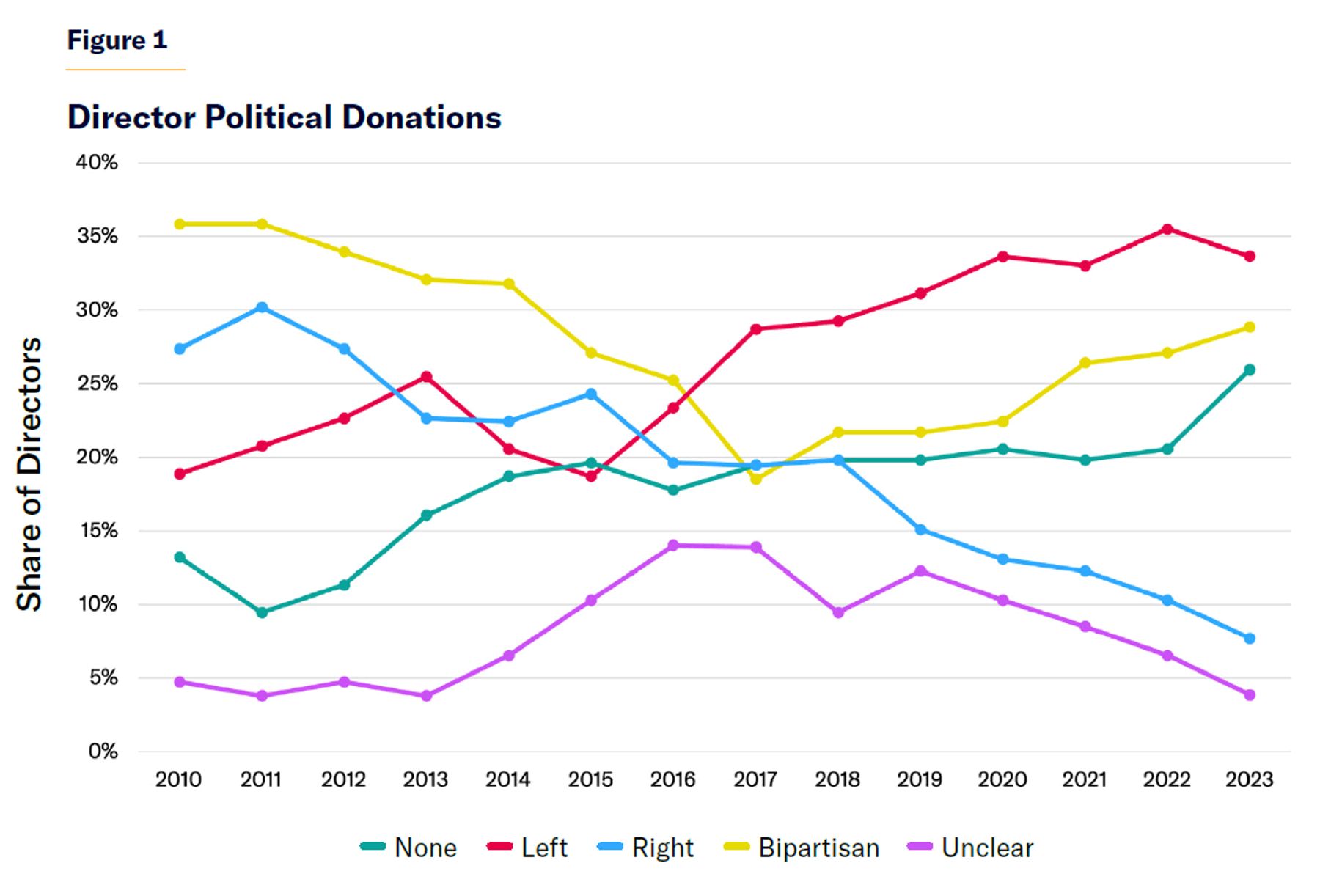

Directors have become increasingly left-leaning since 2010 and especially since 2018 (Figure 1 and Table 1). Donations to right-leaning candidates have plummeted, while donations to left-leaning candidates have increased. In 2023, roughly 26% of Fed directors had no political donations registered with the FEC or OpenSecrets. Just under 35% of Fed directors had donated only to left-leaning candidates or PACs. A little over 28% of directors made bipartisan donations. Less than 8% of directors donated only to right-leaning candidates or PACs. The rarity of donations to right-leaning candidates is surprising, given that directors are supposed to be broadly representative of a country where left and right political preferences are evenly split.[17]

Until very recently, there was not a sharp divergence among donations of directors. During 2010–12, right donations surpassed left donations. This trend repeated in 2014–16, after which they dropped rapidly. There has also been a sharp decline, nearly 20%, in bipartisan donors since 2010—which is especially striking, given our low threshold for a bipartisan classification, which requires making just one donation to another party.

Table 1

Political Donations

| Year | Bipartisan | Left | None | Right | Unclear | Grand Total |

| 2010 | 35.85% | 18.87% | 13.21% | 27.36% | 4.72% | 100% |

| 2011 | 35.85% | 20.75% | 9.43% | 30.19% | 3.77% | 100% |

| 2012 | 33.96% | 22.64% | 11.32% | 27.36% | 4.72% | 100% |

| 2013 | 32.08% | 25.47% | 16.04% | 22.64% | 3.77% | 100% |

| 2014 | 31.78% | 20.56% | 18.69% | 22.43% | 6.54% | 100% |

| 2015 | 27.10% | 18.69% | 19.63% | 24.30% | 10.28% | 100% |

| 2016 | 25.23% | 23.36% | 17.76% | 19.63% | 14.02% | 100% |

| 2017 | 18.52% | 28.70% | 19.44% | 19.44% | 13.89% | 100% |

| 2018 | 21.70% | 29.25% | 19.81% | 19.81% | 9.43% | 100% |

| 2019 | 21.70% | 31.13% | 19.81% | 15.09% | 12.26% | 100% |

| 2020 | 22.43% | 33.64% | 20.56% | 13.08% | 10.28% | 100% |

| 2021 | 26.42% | 33.02% | 19.81% | 12.26% | 8.49% | 100% |

| 2022 | 27.10% | 35.51% | 20.56% | 10.28% | 6.54% | 100% |

| 2023 | 28.85% | 33.65% | 25.96% | 7.69% | 3.85% | 100% |

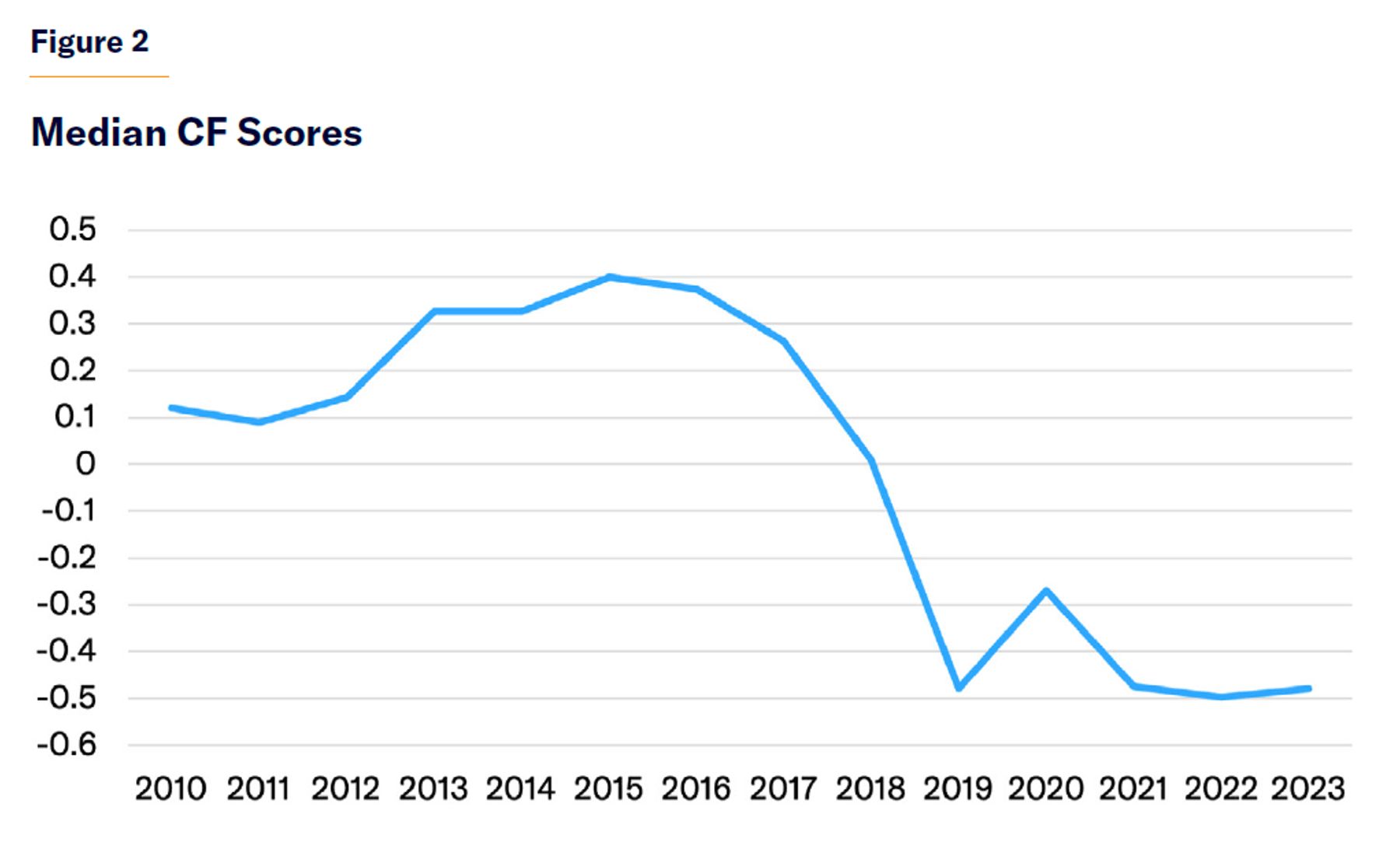

Our second method for measuring director ideology involves campaign finance (CF) scores found in DIME. Scores below zero are more liberal, and scores above zero are more conservative. The change in CF scores over time denotes that director ideology has become sharply more liberal since 2015. This trend aligns with the ideological shifts suggested by the simpler donation methodology.

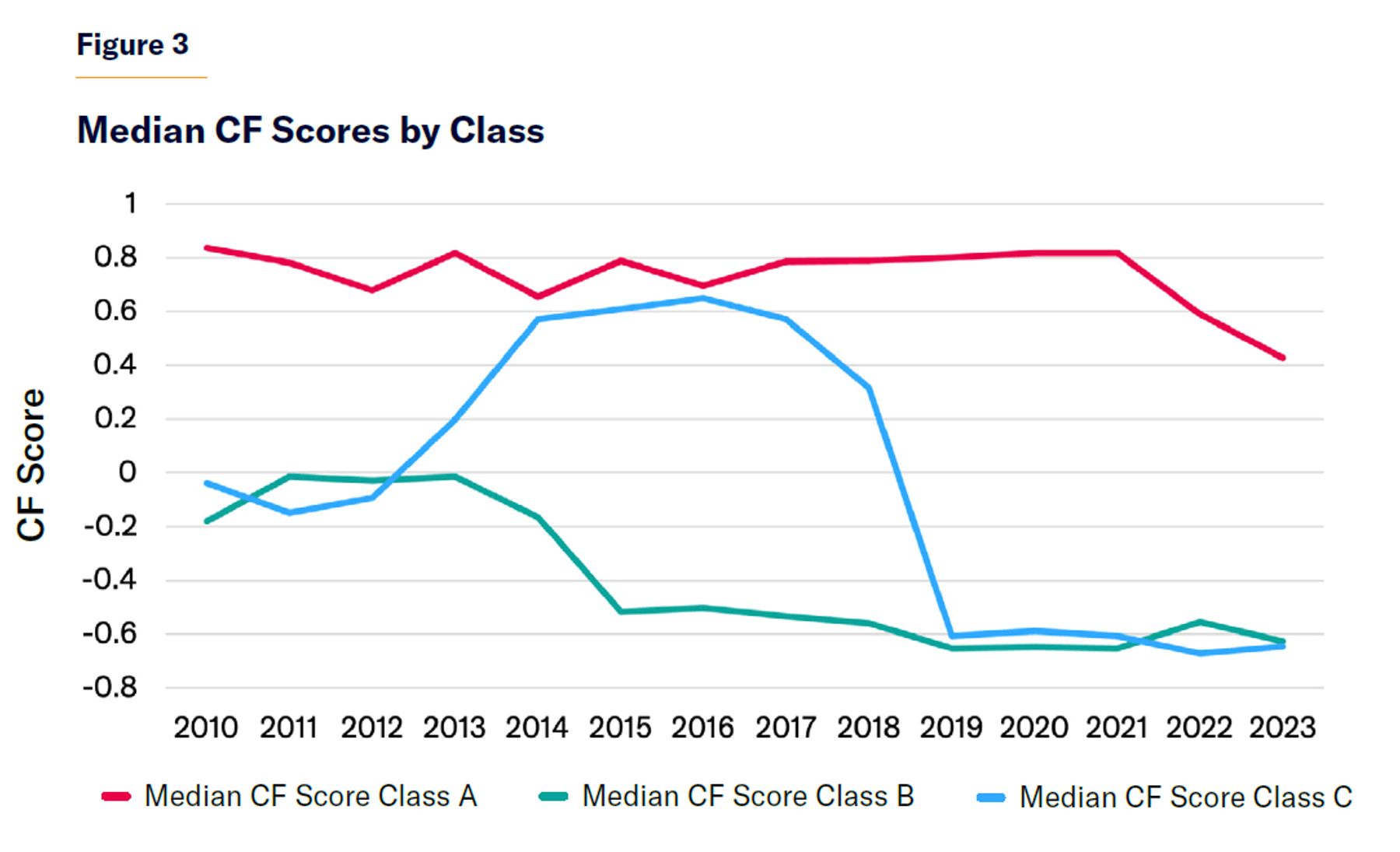

Of the 379 directors studied, CF scores were matched to 315 directors, or about 83% of those who served in this period.[18] During 2010–15, mean and median CF scores of directors start off positive and increase slightly, meaning that they start off more conservative than average and become more conservative over time (Figure 2). This is in line with findings from Elul, which looked at Federal Reserve directors from 1975 to 2015 and found them to be consistently more conservative than the average campaign donor for the entire period studied.[19] But mean and median CF scores start to decline sharply in the years after Elul’s database ends. Median CF scores in our database decrease from about 0.39 to –0.48, which is a sharp change from a historically conservative-leaning director group. The current median CF score of Fed directors is further to the left than the median CF score was to the right during the recent conservative peak. CF scores for Class A directors, however, have remained extremely stable over time, and they remain the most conservative director class. The largest changes have occurred among Class C directors, who are now the most liberal of all classes (Figure 3). This gap between Class A and Class C directors is intriguing and most likely is attributable to the manner in which directors are selected.

Sector Representation

In the past, the Fed has faced criticism because a disproportionate number of nonbank directors have come from the nonbank finance sector. While this has been true historically, finance has become slightly less dominant in recent years. In 2013, for example, about 14.29% of all directors belonged to the nonbank finance sector. This figure slumped to about 7.14% in 2018, before rebounding somewhat to 11.43% in 2023.

Since the mid-2010s, the largest share of nonbank directors has come from one of two sectors: labor; or consumer & community (Table 2). The consumer & community sector is defined by affiliation with nonprofit organizations with a variety of missions, including affordable housing, community development, and naturalization. The labor sector contains representatives of labor unions. Both tend to be focused on policy change, as opposed to economic production, and tend to be more left-leaning.

Despite a slight decrease in 2023, the consumer & community sector remains dominant among nonbank directors. Moreover, the combined share of consumer & community and labor has far surpassed any other sector listed since 2016. In 2023, these sectors accounted for slightly under 20% of all nonbank directors.

By contrast, the agriculture sector and the energy, mining, and extraction sector have seen significant drop-offs in representation in the same period. Each of these sectors possessed under 2% representation in 2023, falling from 10% and 8.57%, respectively, in 2010.

Table 2

Director Sectoral Distribution

| Year | Agriculture | Consumer & Community | Energy, Mining, and Extraction | Finance (Nonbank) | Labor | Other |

| 2010 | 10.00% | 5.71% | 8.57% | 10.00% | 2.86% | 62.86% |

| 2011 | 8.70% | 8.70% | 7.25% | 14.49% | 1.45% | 59.42% |

| 2012 | 5.80% | 8.70% | 7.25% | 14.49% | 1.45% | 62.32% |

| 2013 | 5.71% | 11.43% | 4.29% | 14.29% | 2.86% | 61.43% |

| 2014 | 7.14% | 10.00% | 4.29% | 11.43% | 2.86% | 64.29% |

| 2015 | 5.71% | 10.00% | 2.86% | 10.00% | 2.86% | 68.57% |

| 2016 | 4.23% | 14.08% | 2.82% | 9.86% | 4.23% | 64.79% |

| 2017 | 4.17% | 13.89% | 2.78% | 8.33% | 5.56% | 65.28% |

| 2018 | 4.29% | 12.86% | 2.86% | 7.14% | 5.71% | 67.14% |

| 2019 | 1.45% | 11.59% | 2.90% | 8.70% | 7.25% | 68.12% |

| 2020 | 0.00% | 10.14% | 2.90% | 11.59% | 7.25% | 68.12% |

| 2021 | 0.00% | 12.86% | 2.86% | 10.00% | 7.14% | 67.14% |

| 2022 | 0.00% | 14.29% | 1.43% | 8.57% | 7.14% | 68.57% |

| 2023 | 1.43% | 12.86% | 1.43% | 11.43% | 5.71% | 67.14% |

The increase in directors from the consumer & community sector—who often come from activist organizations—helps explain the increase in left-leaning donations and general leftward tendencies in recent years. For instance, recent San Francisco director Karen Lee worked for Plymouth Housing, whose nominal purpose is to address homelessness in downtown Seattle.[20] Its mission statement, however, identifies it as part of a “decolonizing effort” to “replace systems that inflict trauma with practices that restore and advance human dignity.”[21] Plymouth, which receives half its revenue from public grants, attributes societal injustices to land stolen from the indigenous and labor stolen from West Africans.[22] Similarly, Federal Reserve Bank of Philadelphia deputy chair Sharmain Matlock-Turner leads the Urban Affairs Coalition, a group that lobbies private firms in Philadelphia to achieve minority contracting goals.[23]

Not only are there a greater number of directors from the consumer & community sector, but the organizations from which they are drawn has become increasingly ideological. Although the sector has always leaned somewhat to the left, the saliency of left political messaging within the sector has become more acute, even with organizations that were neutral in the past. For example, Lisa Hamilton of the Richmond Fed is president and CEO of the Annie E. Casey Foundation. This organization previously focused on foster care but now funds strategies promoting “equity and inclusion” and has published extensive research on “inclusive and equitable” theories of change.[24] A focus on diversity, equity, and inclusion (DEI) is a consistent theme among more activist directors.[25]

This ideological shift seems to be reflected in increasingly activist efforts by the Reserve Banks. For instance, the banks recently partnered to present a webinar series,“Racism and the Economy,” where the keynote speaker argued: “Racism really has been about the economy, and the economy has fueled racism.”[26] The accompanying “discussion guide” informed participants that “there is a zero-sum mindset that’s predominant among White Americans, more than among Americans of color.”[27] The Minneapolis Fed has highlighted policies to create racial justice, such as “offer restorative housing reparations” and “eliminate systemic racism in the appraisal industry” as part of a campaign of “Promoting Inclusivity and Effecting Change.”[28]

Education

Overall, a business education remains the most common academic background for bank directors. But since 2010, more directors have a public policy background, while far fewer have a legal background.[29] In 2010, slightly under 4% of directors possessed a public policy focus, compared with 12.5% in 2023. The share with a legal background dropped from 15.09% in 2010 to 6.73% in 2023. Public policy has now replaced law as the second most common background of directors (Table 3).

Outside of Class A directors, who must be bankers, the rarity of economics and finance backgrounds is noticeable. From 2010 to 2023, only four directors possessed PhDs in economics, and there were no such directors in in 2023.

Table 3

Academic Focus

| Year | Accounting | Banking | Business | Economics | Finance | Law | Public Policy | Other |

| 2010 | 0.94% | 0.94% | 41.51% | 4.72% | 0.94% | 15.09% | 3.77% | 21.74% |

| 2011 | 0.00% | 0.94% | 37.74% | 5.66% | 0.94% | 17.92% | 4.72% | 22.58% |

| 2012 | 1.89% | 0.00% | 37.74% | 3.77% | 0.00% | 15.09% | 4.72% | 26.37% |

| 2013 | 4.72% | 0.00% | 33.96% | 4.72% | 0.00% | 16.98% | 3.77% | 26.88% |

| 2014 | 4.63% | 0.00% | 34.26% | 3.70% | 0.93% | 15.74% | 5.56% | 25.53% |

| 2015 | 4.67% | 0.00% | 34.58% | 3.74% | 2.80% | 14.95% | 5.61% | 24.47% |

| 2016 | 4.67% | 0.00% | 34.58% | 4.67% | 2.80% | 13.08% | 7.48% | 21.74% |

| 2017 | 5.56% | 0.93% | 34.26% | 6.48% | 3.70% | 12.04% | 4.63% | 22.34% |

| 2018 | 5.66% | 0.94% | 34.91% | 6.60% | 5.66% | 14.15% | 5.66% | 18.75% |

| 2019 | 6.60% | 0.94% | 39.62% | 6.60% | 6.60% | 9.43% | 8.49% | 16.16% |

| 2020 | 7.48% | 2.80% | 42.06% | 6.54% | 6.54% | 5.61% | 8.41% | 15.84% |

| 2021 | 8.49% | 2.83% | 44.34% | 6.60% | 4.72% | 6.60% | 7.55% | 14.85% |

| 2022 | 7.48% | 3.74% | 44.86% | 5.61% | 2.80% | 8.41% | 12.15% | 13.33% |

| 2023 | 7.69% | 2.88% | 49.04% | 6.73% | 1.92% | 6.73% | 12.50% | 11.65% |

Underqualified Directors?

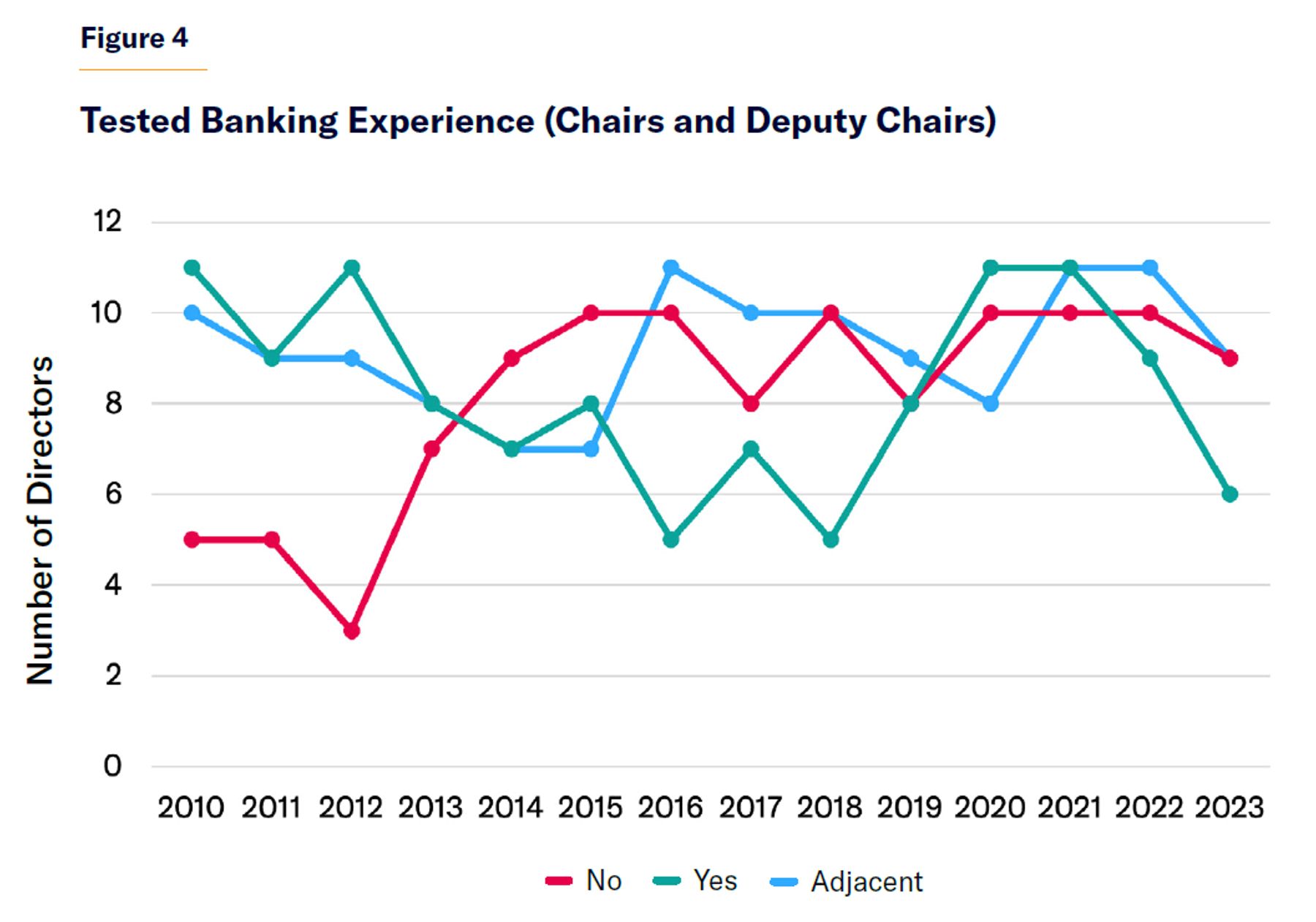

The Federal Reserve Act requires that board chairs have “tested banking experience” (TBE)—and because the deputy chair is supposed to substitute for the chair when necessary, they also should have such experience. But in recent years, an increasing proportion of chairs and deputy chairs seem to lack such experience. In 2010, 44% of those in these positions had identifiable TBE, while 16% did not, and 40% had only adjacent experience. In 2023, only 29% had identifiable TBE, while 38% did not, and 33% had only adjacent experience (Figure 4).

As Table 4 shows, generally more than half of those who appear to lack TBE hail from the consumer & community or labor sectors. The increase in these sectors’ share of non-TBE directors aligns both with the rising number of non-TBE directors and the increasing presence of these sectors generally. This suggests that increases in these sectors’ representation have contributed to a rise in directors without TBE.

Table 4

Sectoral Distribution for No Tested Banking Experience Directors

| Year | Consumer & Community | Education | Finance (Nonbank) | Health Care | Labor | Other |

| 2010 | 20.00% | 20.00% | 0.00% | 20.00% | 20.00% | 20.0% |

| 2011 | 20.00% | 20.00% | 0.00% | 20.00% | 0.00% | 40.0% |

| 2012 | 33.33% | 33.33% | 0.00% | 0.00% | 0.00% | 33.3% |

| 2013 | 28.57% | 0.00% | 0.00% | 0.00% | 0.00% | 71.4% |

| 2014 | 22.22% | 0.00% | 0.00% | 0.00% | 11.11% | 66.7% |

| 2015 | 20.00% | 0.00% | 0.00% | 0.00% | 10.00% | 70.0% |

| 2016 | 20.00% | 0.00% | 0.00% | 0.00% | 10.00% | 70.0% |

| 2017 | 25.00% | 12.50% | 12.50% | 0.00% | 12.50% | 37.5% |

| 2018 | 20.00% | 20.00% | 10.00% | 0.00% | 20.00% | 30.0% |

| 2019 | 25.00% | 25.00% | 12.50% | 12.50% | 25.00% | 0.0% |

| 2020 | 20.00% | 10.00% | 10.00% | 30.00% | 30.00% | 0.0% |

| 2021 | 40.00% | 0.00% | 0.00% | 30.00% | 30.00% | 0.0% |

| 2022 | 50.00% | 10.00% | 0.00% | 20.00% | 20.00% | 0.0% |

| 2023 | 44.44% | 22.22% | 0.00% | 11.11% | 22.22% | 0.0% |

Many directors with a more political background do not seem to possess the qualifications required to be a chair or deputy chair. For example, Vincent Alvarez is chair of the New York Fed, and Patrick Dujakovich is chair of the Kansas City Fed. Alvarez and Dujakovich are both presidents of their local AFL-CIO chapters.

Alvarez’s and Dujakovich’s qualifications for these positions are open to question. Dujakovich’s TBE appears to be derived from his role as the treasurer for the Kansas City Fire Department.[30] Alvarez does have a degree in business economics, but he spent his career as a tradesman and an activist on “numerous political campaigns, grassroots initiatives, and negotiating committees.”[31]

The increasing prevalence of more activist directors may conflict with the requirement that directors not “engage in any political activity or serve in any public office that might associate Fed with any political party and partisan political activity.” Yet City & State New York has described how Alvarez has seen his “influence in economic affairs grow” following his Fed appointment, which reportedly includes an effort to lobby New York City mayor Eric Adams to “implement the new city pay law for app-based delivery workers.”[32]

Demographic Dynamics

There has been a large and rapid change in the demographic makeup of Fed directors, mostly driven by increases in the number of nonwhite and (to a lesser extent) female nonbank directors (especially Class C directors), many of whom come from the consumer & community sector.

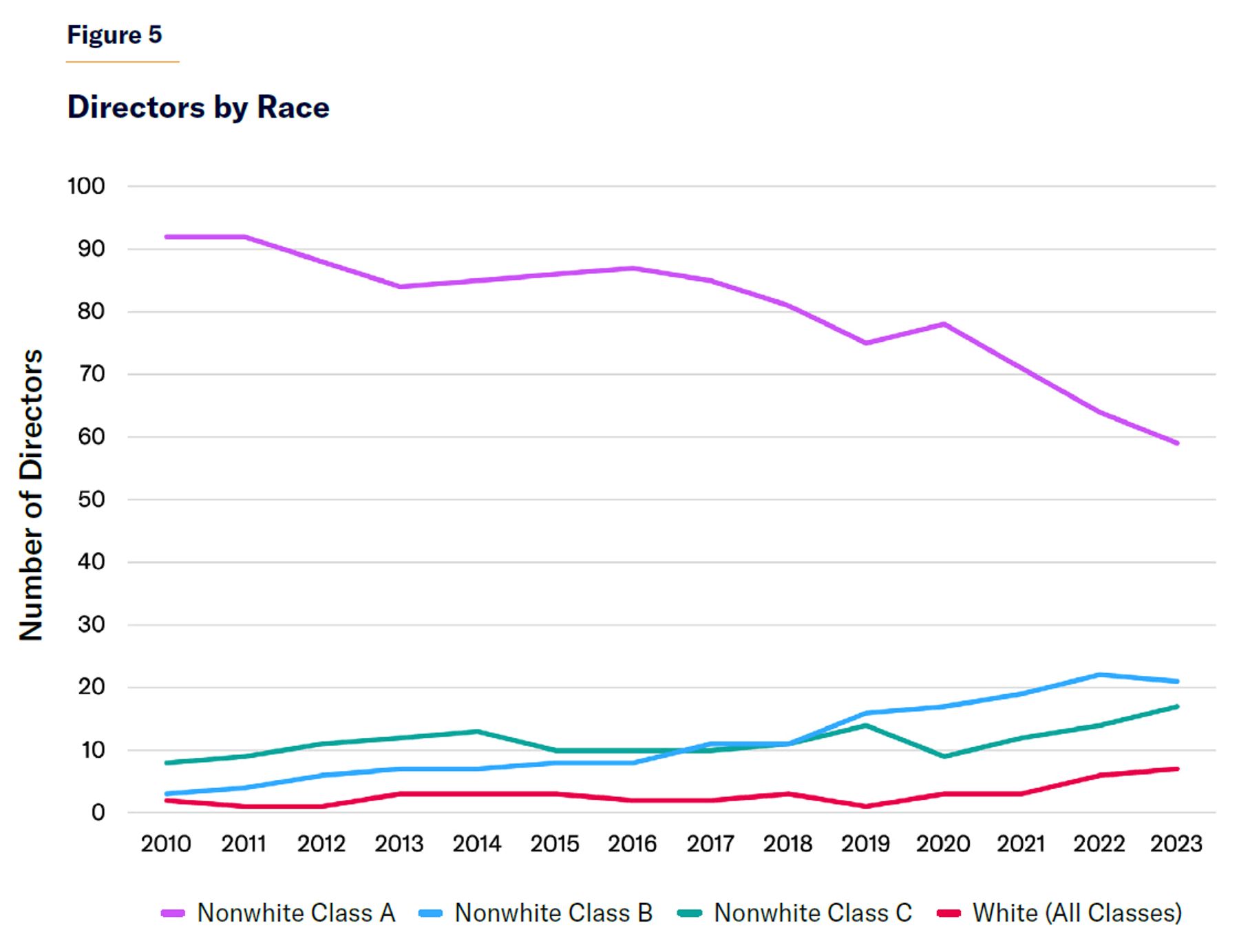

During 2010–23, the share of nonwhite directors more than doubled, from 13.21% to 44.23% (Figure 5). Although they were underrepresented in the past, nonwhite directors are now overrepresented on the Fed Board relative to the nonwhite share of the U.S. population.[33] Nonwhite directors are concentrated in Class C positions, accounting for 62% of all Class C directors in 2023. In 2018, nonwhite directors occupied about 31% of Class C positions. In 2013, this figure was 20%; in 2010, it was 11%. In 2023, nonwhite directors also occupied roughly 58% of all chair and deputy chair positions. In 2018, this figure was about 29%. In 2013 and 2010, it was about 13%. In 2023, white directors were still the majority of Class A and Class B directors. The overrepresentation of nonwhite directors in Class C positions is particularly interesting because these directors are selected by the Federal Reserve Board of Governors. The Board of Governors’ selections, along with the fact that they maintain a database that tracks racial and sexual diversity, would seem to evince an explicit policy of demographic diversity.

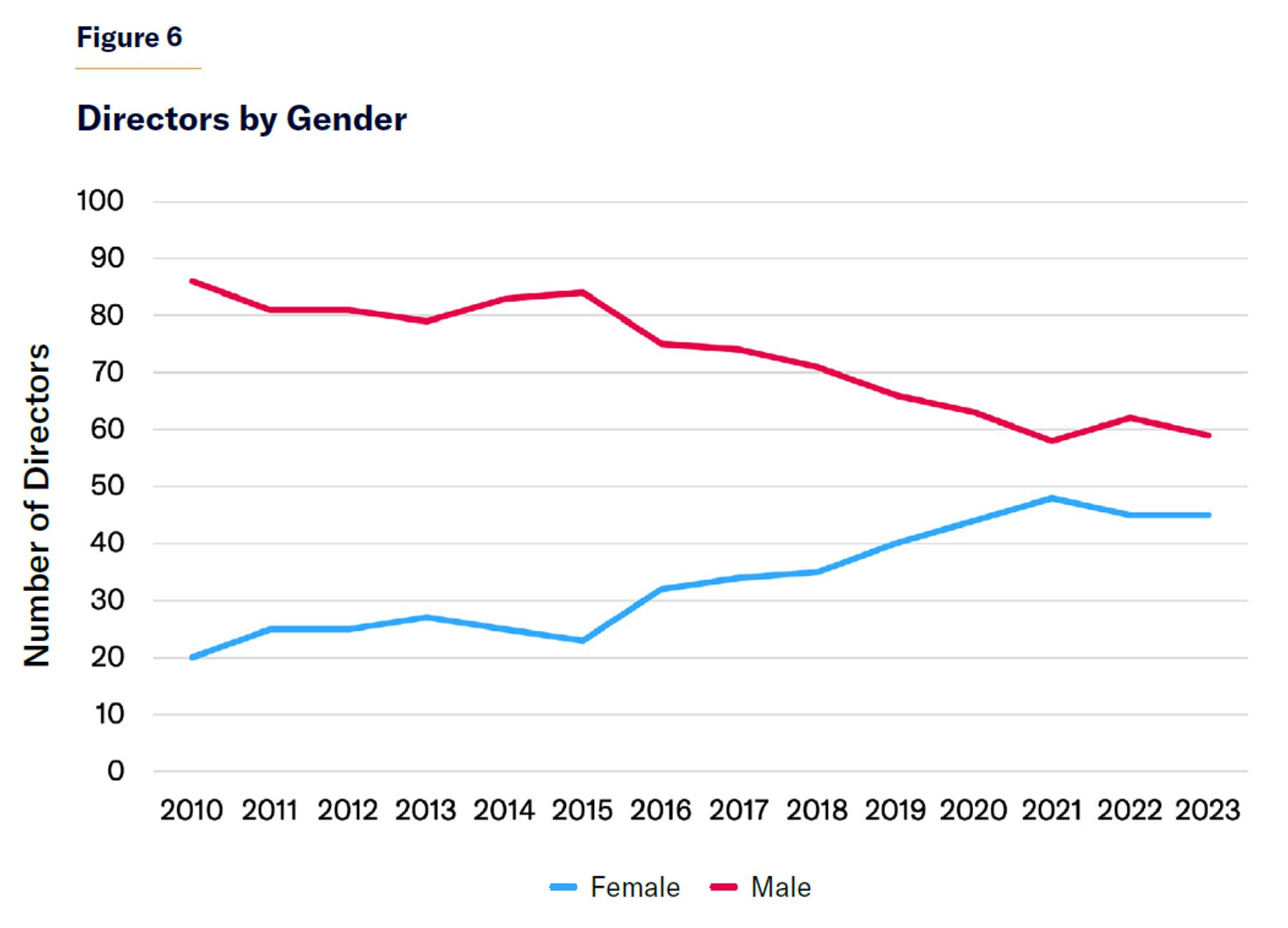

The share of female directors has also increased substantially, by about 25 percentage points since 2010 (Figure 6). The distribution of women across director classes has become more even since 2018, suggesting that change for this group might be more reflective of general changes in society and business rather than a push from the Board of Governors.

As shown in Table 5, nonwhite and female directors disproportionately come from the consumer & community sector. As shown in Table 6, public policy occupies a larger share of nonwhite director academic backgrounds than for directors overall. Female directors disproportionately possess a public policy background, when compared with male counterparts and directors overall.

Table 5

Consumer & Community Distribution for Directors by Race and Gender

| Year | Nonwhite | White | Male | Female |

| 2010 | 7.14% | 3.30% | 1.16% | 15.00% |

| 2011 | 13.33% | 4.40% | 1.23% | 20.00% |

| 2012 | 16.67% | 3.41% | 0.00% | 24.00% |

| 2013 | 18.18% | 4.76% | 0.00% | 29.63% |

| 2014 | 17.39% | 3.53% | 0.00% | 28.00% |

| 2015 | 14.29% | 4.65% | 1.19% | 26.09% |

| 2016 | 25.00% | 5.75% | 4.00% | 21.88% |

| 2017 | 21.74% | 5.88% | 4.05% | 20.59% |

| 2018 | 19.23% | 5.00% | 4.23% | 17.14% |

| 2019 | 19.35% | 2.67% | 3.03% | 15.00% |

| 2020 | 17.24% | 2.56% | 3.17% | 11.36% |

| 2021 | 22.22% | 1.45% | 1.72% | 16.67% |

| 2022 | 22.22% | 0.00% | 3.23% | 17.78% |

| 2023 | 17.39% | 1.72% | 3.45% | 15.22% |

Table 6

Public Policy Distribution for Directors by Race and Gender

| Year | Nonwhite | White | Male | Female |

| 2010 | 7.14% | 3.30% | 3.49% | 5.00% |

| 2011 | 13.33% | 3.30% | 3.70% | 8.00% |

| 2012 | 16.67% | 2.27% | 2.47% | 12.00% |

| 2013 | 9.09% | 2.38% | 2.53% | 7.41% |

| 2014 | 13.04% | 3.53% | 4.82% | 8.00% |

| 2015 | 14.29% | 3.49% | 4.76% | 8.70% |

| 2016 | 30.00% | 2.30% | 6.67% | 9.38% |

| 2017 | 17.39% | 1.18% | 2.70% | 8.82% |

| 2018 | 19.23% | 1.25% | 4.23% | 8.57% |

| 2019 | 19.35% | 4.00% | 4.55% | 15.00% |

| 2020 | 20.69% | 3.85% | 4.76% | 13.64% |

| 2021 | 13.89% | 4.35% | 3.45% | 12.50% |

| 2022 | 22.22% | 4.92% | 6.45% | 20.00% |

| 2023 | 21.74% | 5.17% | 6.90% | 19.57% |

Conclusion and Recommendations

Since the early 2010s, Federal Reserve directors have become much more demographically diverse but also more ideologically homogeneous and politically active.

The current ideological leaning of the directors is new in Federal Reserve history. While previous research has shown that directors were generally conservative, directors have taken a recent and abrupt shift to the left since 2015, which has not been documented by previous research, which stopped at around this date. Although there is no mandate to ensure ideological parity among directors, either a consistently conservative stance or a consistently liberal one among directors should be cause for concern, since it would indicate that the leadership of the Federal Reserve has become an entrenched group that is not representative of the nation as a whole.

As previously noted, Class B and C directors are elected to “to represent the public with due … consideration to the interests of agriculture, commerce, industry, services, labor, and consumers.”[34] However, the current makeup of directors, in which agriculture, commerce, and industry have declined in representation,[35] suggests that this is not occurring. Although the precise amount of legally mandated labor and consumer representation on the boards is open to question, the increase in these sectors in recent years has crowded out other mandated representatives. The increase in community and nonprofit group representation not tied to particular economic efforts outside of political activism does not seem necessary to further any part of the Fed’s mandate.

The presence, or lack thereof, of individuals with a strong background in economics or tested banking experience is concerning, given the Fed’s legal requirements. TBE can be difficult to define precisely; but clearly, fewer chairs and deputy chairs possess the kind of experience that would be relevant to performing their core functions, such as accurately assessing the performance of bank Presidents or proposing new ones.

The Fed is not mandated by its charter to achieve a certain level of demographic diversity among its directors. Indeed, attempts to deliberately increase demographic diversity may contradict a 1977 provision that requires that directors be selected without regard “to race, creed, color, sex, or national origin.” Yet three Fed Bank Presidents—Eric Rosengren (Boston), Raphael Bostic (Atlanta), and Loretta Messer (Cleveland)—recently discussed “how to achieve diversity across the Federal Reserve System,” including “leadership on the Banks’ boards of directors.”[36] It appears that this drive for demographic diversity is coming at the expense of things that are mandated in the Fed’s charter, such as sectoral representation, banking experience, and the absence of political activism.

The Board of Governors in Washington appears to be taking a much more active role in the management of the Federal Reserve Banks in general. Not only has the Board of Governors appointed an increasing number of left-leaning Class C directors, but it has also been increasingly involved in influencing the selection of bank Presidents, whom those directors are supposed to nominate themselves. Since 2010, the Board of Governors has not only approved President selections but has actively guided the process. As Jeffrey Lacker (former President of the Federal Reserve Bank of Richmond) has explained, after 2010, the Board of Governors has not just approved President selections but actively guided the process: “The Board’s role appears to have shifted from final-stage review and approval, as suggested by the language of the Federal Reserve Act, to co-management of the Presidential search process.” This has led to bank Presidents who more closely resemble the Class C directors, whom the board also selects. In 2009, more than half of Presidents had published multiple articles in top journals with a monetary or macroeconomics focus. Arguably few, if any, Presidents named since 2011 have such records.[37] The current dominance of the Washington-based board and its selection of regional bank Presidents without macroeconomic backgrounds prevents more informed dissents against the board and ensures more groupthink in monetary policy.[38]

The tendency toward forgoing the written mandates for Federal Reserve governance and toward declining non-demographic diversity is also manifest in the selection of governors for the Board of Governors in Washington. The Fed’s charter requires that no more than one governor must come from each of the 12 Federal Reserve districts. But in recent years, that provision has effectively been ignored, and the large majority of directors now hail from the East Coast. The eastern geographic focus of board members is another example of the decline in nonracial background diversity at the Fed.[39]

The decline in ideological and geographic diversity and the increased power of the Board of Governors has coincided with a decline in monetary policy dissents, both from the Board of Governors and Federal Reserve Bank Presidents. Only one governor has dissented at an FOMC meeting since 2005. Since the outbreak of Covid, and despite the worst inflationary episode in four decades, there have been only three Fed President dissents, only two of which were for tighter policy.[40] Along with the sharp changes in Federal Reserve directors’ backgrounds and the decrease in their donations to bipartisan and right-leaning groups, the Fed might be witnessing a cultural shift to a less open and more political environment.

Director selection needs to be taken more seriously. The economic weight of various sectors in various regions should be assessed when selecting Class B and C directors. The advantages of a regional system are moot if directors do not adequately represent their states and regions. Furthermore, TBE should be more rigidly defined. A robust selection criterion for chairs and deputy chairs requires experience with the Federal Reserve’s main missions of monetary and financial policy. More economically experienced and ideologically diverse Federal Reserve Bank directors and Presidents would help create a more effective counterweight to the Board of Governors in Washington and prevent the groupthink that has become apparent in the making of monetary and regulatory policy in the last few years.

About the Authors

Judge Glock is the director of research and a senior fellow at the Manhattan Institute and a contributing editor at City Journal. He was formerly the senior director of policy and research at the Cicero Institute, a nonpartisan think tank based in Austin, and a visiting professor of economics at West Virginia University. He writes about the intersection of economics, finance, and housing, with a perspective informed by his work in economic history.

Glock’s work has been featured in National Affairs, Tax Notes, the Journal of American History, NPR, The New York Times, and the Wall Street Journal, among other places. He is the author of the book The Dead Pledge: The Origins of the Mortgage Market and Federal Bailouts, 1913-1939, published in 2021 by Columbia University Press. He received his Ph.D. in history with a focus on economic history from Rutgers University.

Reade Ben is a law school associate at the Manhattan Institute, where his work focuses on large-scale data analysis, database creation, central banking policy, trade, and U.S. macroeconomic conditions.

A summa cum laude graduate of Princeton University, Reade studied international trade and finance policy within the Princeton School of Public and International Affairs (formerly the Woodrow Wilson School) and earned a certificate in Russian, Eastern European, and Eurasian Studies. His other areas of academic interest included financial history, political economy, EU integration, and transatlantic relations.

As an undergraduate, Reade interned at the White House, serving on the Domestic Policy Council and the Council of Economic Advisers. He also worked as a Global Markets Summer Analyst at BNP Paribas. He has also served as a research consultant for the U.S. Space Force and a research assistant at Stanford’s Hoover Institution.

In 2023, Reade spent nine months in Belgrade, Serbia, as a Fulbright Scholar. Working with the Belgrade Center for Security Policy and the University of Belgrade’s respective faculties of Political Science and Geography, Reade studied the phenomena of corrosive capital and its political and economic implications for Serbia.

Reade is also a LEAD Fellow at Columbia Law School. He will commence his studies there in September 2024.

Acknowledgments

The authors would like to thank MI data analyst Matias Ahrensdorf and MI collegiate associates Victoria Freeman and Nohl Patterson for their contributions.

Endnotes

Photo: Sparky2000 / iStock / Getty Images Plus

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).