Photo by PixelsEffect/Getty Images

Over the course of the COVID-19 pandemic, the Small Business Administration extended almost $400 billion in disaster loans to nearly four million businesses and nonprofits. Currently, about 860,000 of these loans are delinquent.

The SBA does not collect delinquent loans: it discharges that responsibility to the Treasury Department. The Treasury Department does not collect for free. In fact, it charges a 30% fee.

For many small businesses, this fee comes as a surprise, hidden in the "fine print" of SBA loan documents. Moreover, the U.S. government can collect outstanding debts at any time, with no court order necessary. The assets of delinquent small businesses can be quickly collateralized, often without warning.

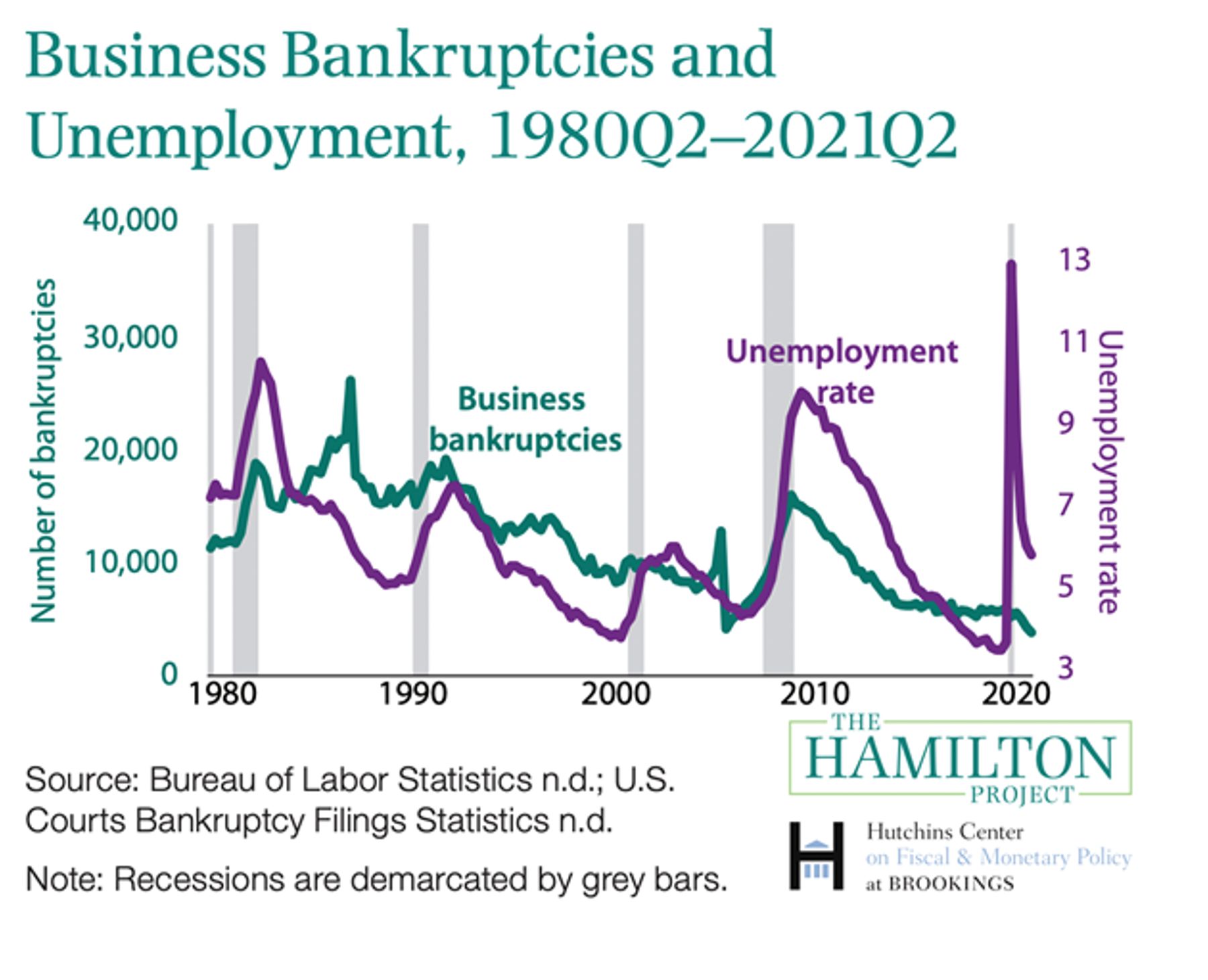

The high "personal cost" of COVID relief for small businesses appears even more excessive considering that the effectiveness of disaster loans is disputable. As the graph below shows, business bankruptcies during the COVID-19 pandemic were actually historically low. However, the role of lending programs in preventing mass bankruptcies was relatively small. A lack of business failures is more likely attributable to "general support for households" and a fast recovery from lockdowns.

Somewhat ironically, disaster relief is becoming a disaster itself.

Sources: Ruth Simon, WSJ; Gabriel Chodorow-Reich, Ben Iverson, and Adi Sunderam, Brookings Institution

Interested in real economic insights? Want to stay ahead of the competition? Sign up for our weekly newsletter here.

Photo by PixelsEffect/Getty Images