Whither Fannie and Freddie? A Proposal for Reforming the Housing GSEs

Click here for PDF

SUMMARY

We propose a specific reform of Fannie Mae and Freddie Mac, the two government-sponsored enterprises (GSEs) that securitize and guarantee conforming mortgages. Our plan protects taxpayers and the overall economy from the systemic risk posed by the former GSE model, while ensuring that financing remains available for housing even in periods of credit market strains. Under this proposal the two firms would become private companies that buy conforming mortgages and bundle them into securities that are eligible for government backing. The reformed firms would not have the investment portfolios that were the main source of risk under their previous structure. The federal government would offer a guarantee on mortgage-backed securities composed of conforming loans. This guarantee would be explicit, backed by the full faith and credit of the United States. To compensate taxpayers for taking on housing risk, Fannie and Freddie would pay an actuarially fair fee to the government in return for the guarantee, and the shareholders of the firms would take losses before the government guarantee kicks in. Other private firms such as bank subsidiaries would be allowed to compete by securitizing conforming loans and purchasing the government guarantee. Over time, entry into these activities would help ensure that the benefits of the government support are passed through to homeowners and would reduce the risk that the failure of any one firm would pose a threat to the housing market or the overall economy.

INTRODUCTION

Few issues are as important to financial markets, the U.S. economy, and current and future American homeowners as the fate of Fannie Mae and Freddie Mac, the two government-sponsored enterprises (GSEs) that support the secondary mortgage market. Since the government put Fannie and Freddie into conservatorship in September 2008, the two firms have effectively become federal agencies. Taxpayers have injected more than $100 billion into the two companies – putting them on track to be the most expensive of the financial market bailouts – and may have to add tens of billions more in coming years. At the same time, the Federal Reserve has purchased more than $1 trillion in Fannie and Freddie securities in order to support the mortgage markets and the broader economy.

With help from the government, Fannie and Freddie did succeed in providing affordable mortgage rates to many Americans throughout the recent financial crisis. That is the good news. The bad news is that the public is now on the hook for three kinds of potential losses: those embedded in the $5 trillion of securities and guarantees on the two firms’ balance sheets, those that may come from the firms regular, ongoing operations in the mortgage market, and, perhaps most importantly, further losses that may come now that the firms are being used as de facto government agencies. The two firms remain notionally private companies, despite the government’s almost 80 percent ownership stake. In practice, however, the firms have taken on public policy efforts – including aggressive foreclosure avoidance programs – that will likely increase their losses. In essence, Fannie and Freddie are being used as off-balance sheet conduits for government spending, with losses offset by unlimited injections of taxpayer money.

The firms’ collapse confirmed what many analysts had long warned: the traditional GSE structure is fundamentally flawed. The opportunity to pursue private profit backstopped by an implicit government guarantee was an invitation to excess risk-taking. Light regulation failed to reign in the resulting excesses. As a result, the firms amassed enormous balance sheets – with debts and mortgage guarantees rivaling the size of the market for U.S. Treasury securities – even as political pressures encouraged riskier home lending that put the enterprises – and taxpayers standing behind them – in danger.

In short, the traditional GSE model failed. As the financial sector continues to heal, reform of Fannie and Freddie must be part of a larger vision for the future of mortgage financing. That policy discussion should be informed by the failures of past policy toward the GSEs. But it should also be informed by the successes. Whatever their flaws, Fannie and Freddie did boost liquidity in the secondary mortgage market. That liquidity made it easier for average Americans to get mortgages not only during normal economic times, but also in the depths of the financial crisis. Even as other sources of credit dried up, the agency mortgage market remained robust.

The challenge for reform is to establish an institutional structure for mortgage finance that maintains the best outcomes of the earlier system and corrects its flaws. This paper sets out a framework for evaluating possible future roles for the GSEs and then uses that framework to guide a specific policy recommendation.

The paper begins by identifying seven objectives for GSE reform: ensuring liquidity in the secondary mortgage market; avoiding systemic risk; protecting taxpayers; helping homeowners; encouraging beneficial innovation; promoting transparency; and balancing the roles of government agencies and the private sector.

The paper then examines how these objectives can best be achieved for each of the GSEs’ four main activities: securitizing and guaranteeing mortgage securities; owning portfolios of mortgage securities; supporting affordable housing efforts; and acting as a mortgage lender of last resort.

Based on this evaluation, we believe that the reformed Fannie and Freddie should continue to play a central role in the securitization and guaranteeing of mortgage securities, but as purely private companies with competition from other private companies. Structured correctly – including with fees paid to the government in return for an explicit guarantee – the firms can provide significant benefits to American homeowners with manageable risk to taxpayers and the financial system. Competition from other firms will help ensure that any government subsidy is passed on to homebuyers and people looking to refinance their mortgage. Allowing entry into the market for government-backed mortgage securities will also spur innovation, and make it possible for one or more of the firms to fail without raising the possibility of a substantial adverse impact on the broad economy.

Conversely, we do not believe that the new Fannie and Freddie should have a significant role in the other three activities for the foreseeable future. The multi-trillion dollar investment portfolios amassed by Fannie and Freddie were the primary source of moral hazard in their operations as GSEs. At the same time, the widespread bank ownership of the GSE debt used to fund the portfolio activities posed a systemic risk to the financial sector. In July and September 2008, taxpayers had to stand behind the GSE debt to avoid the possibility that losses in the event of a default would force banks to recapitalize en masse at a time when markets were already under stress. The risks to taxpayers and the economy from large portfolios overwhelm any potential economic benefits from the incremental liquidity they might provide to the mortgage market.

Public policy and taxpayer resources can and should continue to support access to affordable housing by low- and moderate-income families, but this should not be done by imposing affordable housing goals on Fannie and Freddie. Instead, the aims of affordable housing programs should be pursued through activities that receive regular review in the appropriations process and are explicitly recorded in the federal budget. Regulatory efforts to encourage affordable housing through the GSEs, in contrast, receive comparatively little scrutiny and do not effectively focus taxpayer resources on the families that most need help. The lack of transparency and poor targeting convinces us that Fannie and Freddie should not be used as instruments of affordable housing policy.

If Congress decides that resources from the conforming mortgage market should help finance affordable housing programs, this can be accomplished by levying an explicit tax on Fannie and Freddie’s activities rather than by requiring them to undertake the programs themselves.

Finally, we also conclude that lender of last resort functions are best carried out by other parts of the government, specifically the Treasury Department and the Federal Reserve. The Treasury is the appropriate agency to support financial markets when there is significant risk that government investments may incur losses. Indeed, that was the rationale for placing Treasury in charge of the Troubled Asset Relief Program. The Federal Reserve is the appropriate agency to support financial markets with investments that provide liquidity but pose little or no risk of losses such as well-secured loans. The Federal Reserve has embraced that role aggressively in combating the current crisis, becoming the largest single buyer of guaranteed mortgage securities. The Fed acquired $1.25 trillion of mortgage-backed securities backed by Fannie and Freddie as well as $175 billion of their debt. Treasury and the Fed can play these roles again in the future if financial stresses threaten liquidity in the mortgage market.

The following sections develop the seven objectives in greater detail and apply them to the GSEs’ four activities. We then make a detailed policy recommendation for reforming the firms and conclude by discussing alternative reform proposals.

SEVEN OBJECTIVES FOR GSE REFORM

Ensuring liquidity in the secondary mortgage market

Policymakers have long recognized that active secondary mortgage markets increase the availability of primary mortgage credit. That insight led to the creation of Fannie Mae in 1938 during the Great Depression. Fannie initially focused on the secondary market for whole mortgage loans. With the advent of mortgage-backed securities in the 1970s, both Fannie and its younger sibling Freddie moved into securitization.

Despite the well-documented failures in some segments of the mortgage market (most notably subprime), it remains the case, as Jaffee et al. (2009) recently put it, that “the securitization of the mortgage market is one of the great stories of financial innovation.” Securitization bridges the gap between global capital markets and local mortgage markets. Before widespread securitization, mortgage pricing and availability were often limited by the capital held by the local banks that made mortgage loans and by the limited size of the secondary market in whole mortgages. Since the 1970s, securitization has become a crucial part of the mortgage market, allowing local lenders to make mortgages that were bundled together and sold to investors across the United States and around the world. Local banks could then recycle the proceeds into additional mortgage loans. Borrowers benefitted from lower interest rates and more favorable terms made possible by the influx of capital into housing, while investors benefitted from the opportunity to finance American mortgages and take on a diversified exposure to housing-related returns.

That process has had its excesses. For example, the availability of easy liquidity was associated with broad slippage of lending standards in the run-up to the financial crisis. And some securitization practices may have been fraudulent. But the basic insight remains robust: liquid secondary mortgage markets support primary mortgage lending. For that reason, policymakers’ first objective in remaking the GSEs should be to ensure continued liquidity in the secondary mortgage market. As discussed later, this objective need not imply the same mechanism as the existing GSEs; in principle, other approaches – e.g., widespread adoption of covered bonds – might also suffice. Our policy recommendation is compatible with continuing evolution for the sources of housing finance.

Avoiding systemic risks

Any reform should also satisfy a second objective: avoiding systemic risks to the broader financial system.

In their earlier form, Fannie and Freddie added to systemic risk in at least two ways. First, the companies’ vast, highly levered investment portfolios threatened their viability and, thereby, the functioning of much of the mortgage market. Second, the implicit guarantee inspired investor confidence in GSE securities. As a result, many financial institutions owned large portfolios of GSE debt and MBS. That fact, in turn, made the implicit guarantee into a self-fulfilling prophecy, as the government had to step in to prevent sudden losses on GSE securities from compromising the solvency of the financial system. In a sense, the portfolios allowed the GSEs to hold the financial system hostage and require a government intervention to prop up the firms once they got into trouble.

To limit such systemic dangers in the future, policymakers should both reduce the risk that the successors to the GSEs might collapse and soften the impact if one or more does. An important way in which our policy recommendation accomplishes this latter goal is by allowing other firms to carry out functions now done only by Fannie and Freddie. Once new entry takes place over time and other firms such as established commercial banks securitize conforming mortgages with a government backstop, the failure of a single guarantor would no longer threaten the financial system, the housing market, or the broader economy.

Protecting taxpayers

The previous GSE system exposed taxpayers to enormous downside risks – which may ultimately be measured in the hundreds of billions of dollars – and gave them nothing in return. As discussed below, some of the subsidy implicit in the unspoken government guarantee was passed on to borrowers in the form of lower interest rates, though much of it was captured by GSE shareholders and management. But taxpayers in general (as opposed to families buying homes) were on the hook for the implicit guarantee, which has now been exercised, but received no premiums to compensate for taking on this risk.

Any new structure for Fannie and Freddie should protect taxpayers from such a one-sided arrangement. In principle, such protection can take a variety of forms including limiting the scope of the firms’ activities, ensuring that they hold adequate amounts of private capital, and collecting insurance premiums that are commensurate with the remaining risks that taxpayers bear.

Helping homeowners

The GSEs provided significant benefits to homeowners during the financial crisis. The markets for jumbo, subprime, and alt-A mortgages all froze up during the financial crisis, restricting the availability of credit to families looking to use a non-conforming mortgage to purchase a home or refinance their mortgage. Meanwhile, the conforming market stayed open throughout the crisis.

Before the crisis, however, one of the primary criticisms of the GSEs was that consumers received only limited benefits of the implicit government support that allowed the GSEs to borrow at lower rates than other financial institutions. For example, Passmore, Sherlun, and Burgess (2005) estimated that less than 25 percent of the implicit subsidy made its way to borrowers in the form of lower interest rates. The bulk of the benefit was captured by the two GSEs and, to a lesser extent, the primary mortgage lenders.

In short, many of the benefits created by government policy – enhanced secondary market liquidity and a backstop from the American taxpayer – accrued to Fannie and Freddie shareholders and management rather than to borrowers. Reform efforts should focus on market structures that pass much more of the benefits through to borrowers.

Encouraging beneficial innovation

Careless use of financial innovations, most notably subprime mortgages and tranched MBS, played a key role in the financial crisis. But that does not mean that further financial innovation is undesirable. Instead, it means that policymakers should create an environment that encourages beneficial innovations while ensuring that the supervisory frameworks overseeing the financial sector have the potential to avoid the adverse effects of harmful innovation.

GSE reform should ensure that the new system for housing finance does not stifle innovation in other forms of mortgage finance. Our recommended policy outcome moves toward a level playing field for other sources of mortgage finance by levying an explicit charge for the government backing of mortgage-backed securities with conforming loans and then allowing firms other than Fannie and Freddie to purchase the government backing. This will first add competition with the framework of conforming mortgages in which the two firms now have a duopoly, and then reduce the disadvantage faced by alternative models such as covered bonds.

Promoting transparency

Transparency was sorely lacking in the traditional GSE structure. Everyone believed that the government would step in to rescue the firms if they depleted their capital, but that guarantee was never made explicit. As a result, the firms could portray themselves as fully private firms when it suited their interests, while hinting at the implied government guarantee whenever it was useful, e.g., in raising new capital from investors. The implied guarantee was a subsidy to the GSEs – but it did not appear as a government obligation until it was actually called upon.

Policymakers, meanwhile, used their leverage over the firms to influence their investment and lending decisions – for example encouraging investments in the subprime securities that ultimately generated the most losses. In practice, that political leverage was often exercised behind the scenes, not through an open regulatory or legislative process.

The net result was that the GSEs were an opaque mix of public and private financing and hidden agendas. There is no reason for such ambiguity to exist with the newly reformed Fannie and Freddie. Whatever policy objectives Congress and the President decide to pursue can be achieved in the sunshine, with clear lines of accountability and authority. If a government guarantee remains on Fannie and Freddie MBS (as would happen under our recommended policy) it should be made explicit, backed by the full faith and credit of the United States government. If resources from these firms are used to support affordable housing, that too should be explicit, with a clear tax structure on the firms, well-specified goals, and an open process to monitor compliance and outcomes.

Balancing the comparative advantages of government agencies and the private sector

Finally, reform should strike an appropriate balance between government and the private sector and, for actions taken by the government, among the relevant agencies.

As recent events have demonstrated, private capital markets may not work smoothly during periods of extreme financial stress. At the same time, asset values can fall sharply, eliminating the capital buffers of even the most conservative financial firms. For those reasons, it is not reasonable to expect that a purely private firm could offer insurance against large-scale mortgage defaults without access to some backstop from the federal government. Given the events of the past several years, investors would rightly worry about a tail risk that would overwhelm any private insurance provider. If policymakers decide that insurance is key to supporting mortgage finance, they must therefore embrace some government role in providing – or, at least, backstopping – that insurance. A purely private solution is untenable.

On the other hand, the private sector is much better equipped to evaluate credit risks, manage interest rate and funding risks, and develop new mortgage products. Society would miss out on important benefits if the future model involved a greatly broadened government role in the mortgage markets. That is one reason that our policy recommendation involves substantially more competition than the previous model, but with a continued government backstop to ensure liquidity in the face of another catastrophic decline in houses that wipes out the capital of the reconstituted Fannie and Freddie and any entrants into the securitization business.

Finally, it is essential for policymakers to take into account the comparative strengths and weakness of different government agencies. In recent years, the existing GSE model has been used to pursue three distinct types of policies: traditional support for the conforming mortgage market, promotion of affordable housing goals, and exceptional support to mortgage markets and the broader economy in a time of financial crisis. These policy goals require different skills and oversight. As a result, reform efforts should consider whether it makes sense for Fannie and Freddie to continue to be involved in these disparate activities. We believe the answer is no, so our proposal limits their role to the first policy goal – support for conforming mortgage markets – while assigning the other goals to other agencies.

RETHINKING THE GSEs’ FOUR MAIN ACTIVITIES

Securitizing and guaranteeing mortgage securities

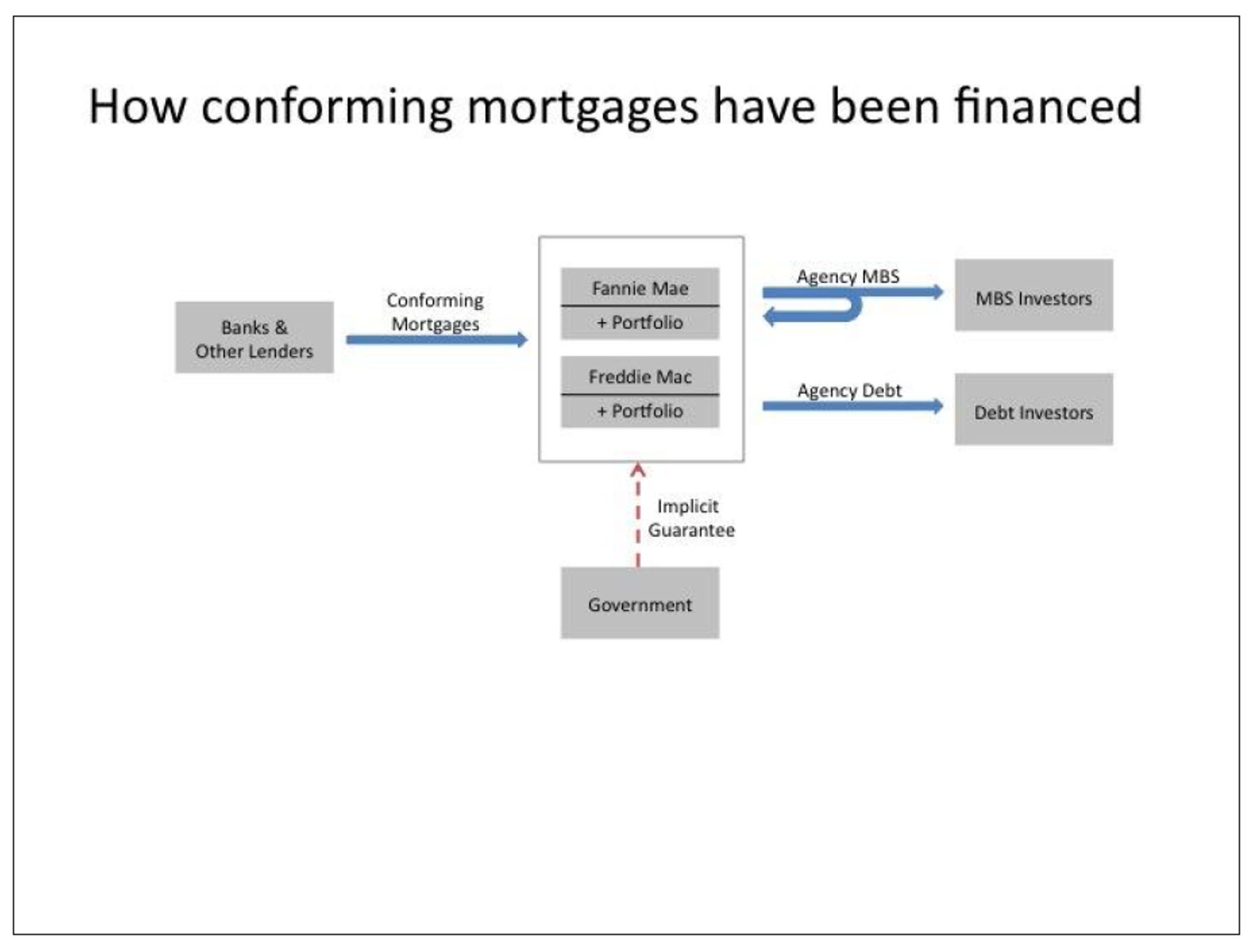

Fannie and Freddie’s primary business has been to purchase relatively safe, standard mortgages, combine them into mortgage-backed securities, and then sell the resulting MBS wrapped with a guarantee that investors will be protected against defaults among the underlying mortgages. In return, the firms receive a guarantee fee that is intended (at least in principle) to cover potential default costs and other operating costs.

In the traditional GSE model, MBS investors could rely on two layers of protection against mortgage defaults. First, each firm held a modest amount of capital as a buffer to make sure it could pay any claims. Second, investors believed – correctly, as it turned out – that the United States government would step up if losses ever threatened to eat through those capital reserves. That implicit guarantee gave the GSEs a strong competitive edge in the mortgage marketplace. Not surprisingly, the two firms played a dominant role, accounting for about half of mortgage originations in the years before the mortgage crisis (Krainer 2009).

The guarantee business played only a secondary role in the failure of the GSEs. Even with the nationwide collapse of housing prices, the considerable protection of 20 percent down payments and credit enhancement through private mortgage insurance (though the PMI firms are having troubles of their own) protected the two firms from much of the financial impact of rising defaults. Instead, as we discuss below, losses on portfolio investments are the primary reason that the companies ran out of capital. By itself, the financial crisis does not, therefore, imply that the securitization and guarantee activities were fundamentally flawed – indeed, the experience suggests that the definition of a conforming mortgage remains a useful concept, with its combination of a sizeable down payment by the homeowner and relatively careful underwriting standards. And, as noted earlier, policymakers should give credit to the GSEs for carrying out these activities throughout the financial crisis.

Our policy recommendation reflects this evaluation of factors that worked and did not work in the previous GSE model. These include:

- Securitization is a valuable mechanism for channeling capital into housing finance.

- It appears inevitable that the government will play some role in backstopping mortgage finance.

- The government role should be explicit.

- Taxpayers should be compensated for taking on risk. In return for providing a backstop guarantee which exposes taxpayers to risk after the capital of Fannie and Freddie’s private shareholders is exhausted, the government should charge fees that are actuarially fair to the extent possible. The purpose of the new Fannie and Freddie (as well as any new entrants) will thus be to promote secondary market liquidity, not to channel a financial subsidy for home ownership.

- Reform should ensure that the benefits of government support flow through to homeowners, rather than being captured by the shareholders and management of firms that engage in securitization.

The portfolio

Fannie and Freddie’s existing investment portfolios should be wound down or sold to other investors. Those portfolios were the main channel through which the firms posed a systemic risk for the financial system. At the time that Fannie and Freddie were put into conservatorship, their combined portfolio of securities and guarantees totaled about $5 trillion. With counterparties widely distributed throughout the financial system, a failure to stand behind the firms would have forced large numbers of U.S. banks to recapitalize at the same time in an already strained market environment (Swagel (2009) provides further context). The firms’ financing needs will be much lower without the obligation to fund portfolio investments and this in turn will greatly reduce the possibility of systemic risk from a failure at either or both of the firms. In our proposed reform below, investors would purchase mortgage-backed securities that have a government backstop rather than routing these investments through Fannie and Freddie and having a guarantee on the firms – under our proposal, the firms will be allowed to fail and shareholders and bondholders take losses, but the MBS will be guaranteed. This ensures that liquidity is available for housing without exposing the financial system and the economy to unnecessary risks.

The ostensible reason for the investment portfolios was to provide liquidity to mortgage markets by having the GSEs themselves act as a source of demand for housing assets such as mortgage-backed securities. Beyond the systemic risk created for the banking system, these investments exposed the firms to four kinds of risk: credit risk, interest rate risk, financing risk, and political risk – a combination of which ultimately sank the two enterprises.

- Credit risk. An investor owning MBS and mortgages faces the risk of credit losses as homeowners default on loans. That is true for Fannie and Freddie as well, with one important caveat: neither of those firms exposes itself to additional credit risk if it invests in its own MBS (since it already bears that credit risk through the guarantees). Nor does it expose itself to credit risk if it invests in MBS that are backed by the full faith and credit of the United States government (as in GNMA securities). Credit risks do exist, however, in all non-agency MBS. Indeed, it was credit losses on private-label mortgage backed securities, including subprime MBS, which played a major role in driving the firms toward insolvency.

- Interest rate risk. Changes in interest rates affect the portfolios in two ways: interest rate moves change the value of assets held on the firms’ portfolios; and lower interest rates lead homeowners to refinance (what is known as “prepayment risk”). These factors led the two firms to undertake highly-sophisticated hedging strategies to manage interest rate risks. While these risks were major concerns in past debates about the GSEs, they turned out not to be key factors in the demise of the GSEs in this crisis. Still, this will remain an issue so long as the firms remain highly levered.

- Financing risk. The massive investment portfolios were funded through equally massive borrowing, exposing the firms to the risk that markets might one day hesitate to roll over their debt. This was the case in 2008, as uncertainties about the financial conditions of the two firms led to gradual increases in their financing costs and brought about the decision to place the firms into conservatorship and to have the Treasury stand behind their obligations.

- Political risk. The hybrid nature of the GSEs as private firms carrying out a public mission to support housing for low- and moderate-income families exposes the firms to pressure to make investments or take other actions on behalf of regulators, members of Congress, or the administration. This can be seen in 2009 and into 2010, as the two firms have taken loss-making actions to stem foreclosures, even at the cost of incurring losses that the Treasury then offsets with additional injections of public capital.

Eliminating the portfolios would remove these risks without undermining the firms’ fundamental liquidity goal, which can be accomplished through securitization backstopped by a government guarantee. For that reason, we recommend that the newly-reformed Fannie and Freddie have no portfolios other than modest warehouses for loans being assembled into MBS, and that their existing portfolios should be separated from the firms and either sold to other investors or allowed to run off as the securities in them mature.

Support for affordable housing

The GSE charters give the two firms the mission of promoting affordable housing and homeownership for low-income families. In the past, Congress has done this by specifying affordable housing goals that require Fannie and Freddie to provide mortgage funding to low- and moderate-income families and underserved locations such as inner cities and rural areas. In practice, meeting these goals drove some of the firms’ riskier portfolio investments.

These goals can be seen as an effort to direct some of the implicit subsidy that the firms receive toward particular policy goals. This raises the question, however, of whether this is the most effective way to target public resources toward those goals. Our answer is a firm no: if society wants to provide subsidies to low- and moderate-income families for housing, it would be more effective to do so directly through traditional spending or tax policies rather than indirectly through private firms such as Fannie and Freddie. Efforts to regulate private firms into supporting low-income housing will at best provide only a rough targeting of the policy goal, while undermining transparency. In practice, much of the implicit subsidy will not reach the intended recipients.

It would be better to implement affordable housing policies through programs in which subsidies are made explicit, including rental support programs through the Department of Housing and Urban Development (HUD) or subsidies through the Federal Housing Administration (FHA). Indeed, several such programs already exist. That approach allows subsidy programs to be targeted to their intended recipients rather than having part of the value of the subsidy accrue to Fannie and Freddie’s shareholders and management. Explicit subsidies would also be transparent and set by the Congress through normal budgetary channels.

It is important to emphasize that the form of these subsidies is an entirely different matter from their funding. One can certainly make an argument that the homeowners who benefit from the firms’ primary activities – securitizing and guaranteeing conforming mortgages – should help finance other programs that help low-income homeowners or renters. Under our proposal, the federal government could choose to fund subsidies to low-income families through a tax on activities in the conforming mortgage market that benefit from the federal backstop (a tax on Fannie and Freddie and any competitors). This tax would be passed through to homeowners, and would thus ensure that all those benefiting from the federal subsidy contribute to funding subsidies for low-income families.

The discussion above does not touch on the desirability of subsidies for low-income housing but only on how they should be delivered and funded if they exist. Our view is that it is likely that such subsidies will be continued and thus it is best for them to be implemented in a way that ensures transparency, budget accountability, and maximum effectiveness. Continuing to implement the subsidies through Fannie and Freddie would miss out on all three. Even so, an argument could be made that the only way that the subsidies will continue (politically) is if they are implemented in a non-transparent way through the two firms or in a way that comes with a related funding source. We do not believe this to be the case, but if so, we would support tapping the activities of the reformed companies (and any new entrants that securitize conforming mortgages and purchase government guarantee) as a source of funds for low-income housing subsidies since this would pass along the burden of these subsidies to most homeowners.

Mortgage lender of last resort

Some observers believe that Fannie and Freddie should hold portfolios in order to provide additional liquidity to the secondary mortgage market. In ordinary times, we believe that any such benefits are more than offset by the resulting financial and political risks. In times of financial stress, however, there are potential economic benefits from some arm of the government supporting the secondary mortgage market; such support can limit disruption in the availability of housing credit and thus soften downturns in the overall economy. The GSEs played that role, in part, during the current crisis and mortgage finance was available throughout the crisis for conforming loans even while interest rates climbed and availability narrowed for non-conforming mortgages as the secondary market large shut down for jumbo and sub-prime mortgage backed securities.

In the end, however, the activities of the GSEs pale in comparison to the $1.25 trillion in agency MBS purchased by the Federal Reserve. These purchases effectively made the Fed into the provider of liquidity for housing activity, helping to ensure the availability of mortgage financing at quite low rates. The Federal Reserve carried out these purchases to support overall economic activity, but in doing so it has demonstrated that it can readily perform the lender of last resort function for mortgage finance, at least for mortgage securities backed by the federal government. The existence of the GSEs was useful to the Fed, since they provided a ready-made channel through which the Fed could provide liquidity without having to deal directly with individual banks or homeowners.

With the Fed’s apparatus in place to purchase mortgage backed securities again if needed, we believe that the lender of last resort function for housing finance should be exercised in the future by some combination of the Federal Reserve and the Treasury. The Federal Reserve is not – and should not – be an independent agent of large-scale fiscal policy. So its purchases should focus on guaranteed MBS, for which there is no risk of credit losses (such purchases would still involve some fiscal risk, however, since the value of the securities can change from day to day for other reasons such as changes in interest rates). The Treasury, in contrast, is an agent of fiscal policy; with an appropriate authorization from Congress, it could purchase a broad-range of mortgage-related securities (including equity in firms that originate mortgages as was done using the TARP).

If a future credit disruption affects the mortgage market, the first action to be taken would be monetary policy, with the Fed purchasing mortgage-backed securities that have a government guarantee (as is the case in our reform plan). Further action should require a vote of Congress to allow the Treasury to deploy additional public resources. There is no need to rely on Fannie and Freddie on their own to ensure the availability of liquidity to housing markets. The Fed and the Treasury will purchase securities created by Fannie, Freddie, and other companies operating in the secondary market for conforming mortgages, but these will be the channels through which the government acts, not the primary actor.

A PLAN FOR GSE REFORM

Reforming the housing GSEs involves three key decisions.

First, what specific activities should the new Fannie and Freddie undertake? As argued above, we favor a focused role. The reformed firms (and new entrants) should securitize and guarantee mortgage securities, but not own investment portfolios, engage in affordable housing efforts, or act as mortgage lenders of last resort.

Second, who should own and manage the new Fannie and Freddie? Private investors? The government? Or something in between such as a regulated utility? We believe that the firms should be fully private, with no remaining linkage – implicit or explicit – to the federal government. The firms would be subject to rigorous regulatory oversight and eligible to purchase MBS guarantees from the federal government. But the government would neither backstop the firms themselves nor be involved in their management. Furthermore, we believe the government should encourage entry by other firms (also subject to financial oversight) and thus increased competition in securitization of conforming mortgages. This competition will ensure that the benefits of a government backstop that guarantees secondary market liquidity get passed through to borrowers rather than enriching shareholders or management.

Third, what is the appropriate role for government? Clearly the government will need to maintain regulatory oversight over the fully private firms to ensure, for example that they maintain sufficient capital to provide a reasonable buffer against losses on the MBS that they sell before any government backstop would kick in. The broader questions involve the scope and magnitude of the government backing provided to the GSEs as corporations or to individual securities such as MBS. Decisions must be made as well about the details regarding the mortgages that will be eligible for support, and the magnitude of fees charged by the government in return for this support.

Specifics

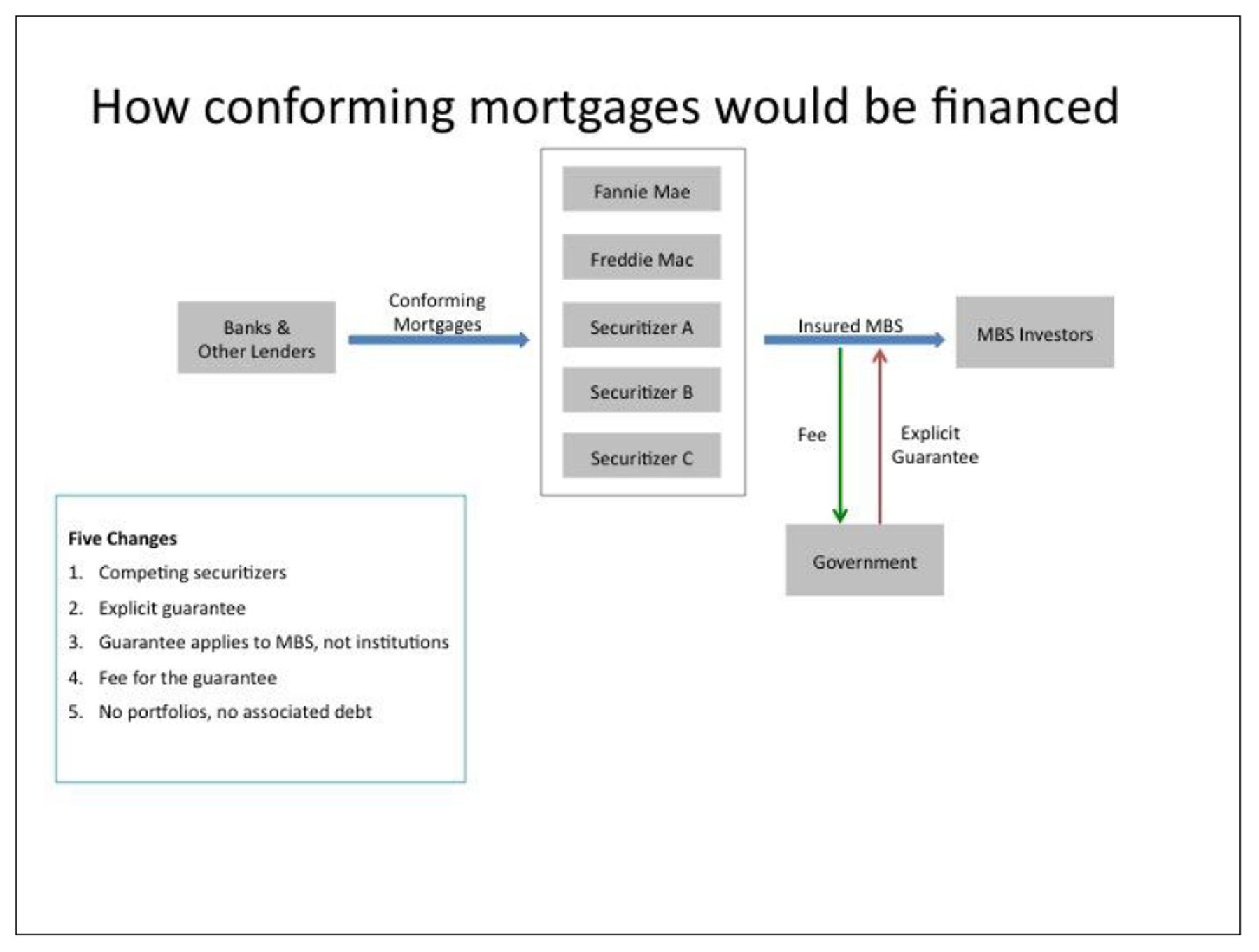

In our proposed reform, Fannie and Freddie once again become private firms, focused on buying conforming mortgages and bundling them into government-backed securities. As illustrated in the Chart, the government backing would be on an MBS-level basis; the guarantee is explicit and comes at a fee – Fannie and Freddie compensate taxpayers for the insurance. Moreover, other private firms such as banks are allowed to securitize conforming loans into mortgage-backed securities and purchase the same MBS-level guarantee from the government. Fannie and Freddie are not allowed to have portfolios for a lengthy transition period until there is sufficient entry into securitization of conforming MBS that the failure of any one firm does not pose a threat to the housing market or the broad economy.

This arrangement involves continued government support to ensure that liquidity remains available for housing finance, but allows entry to boost competition that will ensure that any remaining government subsidy is passed on to homebuyers. The subsidy in this case reflects any difference between the value of the government backing and the fee that securitizers pay for the guarantee.

Key elements of the reform plan are:

- Fannie and Freddie once again become private firms, with the government selling off its ownership stakes.

- Fannie and Freddie focus on bundling conforming loans into mortgage-backed securities. They buy mortgages from originating banks and pay a fee to the government in exchange for the MBS-level guarantee.

- Securitization of conforming loans is opened to competition. Other private firms can also pay the fee and securitize and guarantee conforming MBS with the government backstop. Banks, for example, could securitize conforming MBS from their own originations or could purchase loans, including from Fannie and Freddie. Competition in the securitization industry helps to ensure that the subsidy embedded in the government guarantee is passed through to homeowners and homebuyers.

- Fannie and Freddie have no portfolios – only a warehouse for mortgages that are purchased but not yet bundled into MBS. Strict limits are set on their activities for 5-10 years while competition develops in the securitization industry.

- Fannie and Freddie will evolve over time into either specialized firms focused on securitization or become part of a vertically integrated financial services firm that both originates loans and bundles them into MBS. Over time, the specialized path might have the firms become like Visa and MasterCard and mainly provide network services to banks. In this model, the firms would buy mortgages from originating banks and then sell them to other firms that do the securitization and pay for the government backstop. This potential business model is built on built on the strength of Fannie and Freddie’s network ties into the thousands of originating banks and their ability to impose a screen that ensures the quality of conforming loans.

- A federal guarantee applies on an MBS-level basis. Fannie and Freddie themselves are not guaranteed; the backstop applies to mortgage-backed securities, but only after a firm’s shareholders are wiped out. The entry over time of other firms to securitize conforming loans will make it possible for one of the firms to fail without overly negative consequences for the financial system or the housing market.

- All special government benefits for Fannie and Freddie are repealed. The firms must register with the SEC, the line of credit at the Treasury is ended, and there is no special standing for Fannie and Freddie securities and MBS. All government-guaranteed MBS, whether from Fannie, Freddie, or other private firms, have equal standing.

A key feature of this reform proposal is that it does not prejudge whether Fannie and Freddie are mainly in the service business as securitizers, in the finance business as intermediaries between private capital and the housing market, or even mainly in the technology business as network providers that connect community banks originating mortgages with other firms that securitize them. Competition on all of these dimensions is meant to ensure that the value of the government backstop is passed through to housing market participants.

Restrictions on the firms’ activities would be allowed to fall off over time as other firms begin to compete with them. Fannie and Freddie could eventually be allowed to have portfolios again and enter new businesses, just as their future competitors could. For this to happen, there must first be sufficient entry so that the failure of one of these firms becomes an ordinary event and not one that would impair the housing market. Eventually, the former GSEs could themselves become vertically integrated or be bought by banks. Again, however, the key is to allow a long enough transition period for competition to develop across the different activities.

Advantages

This proposal has several key advantages:

1. It reduces systemic risk by eliminating the investment portfolios and the massive borrowing that was needed to fund the portfolio. There remains a fiscal risk to the U.S. government in the event of another housing collapse, since the government backstop will be explicit. But this fiscal risk is already present and was implicit in the previous system.

2. It promotes competition in securitization of conforming mortgages, which could lead to beneficial innovation. The proposal would foster competition on several levels, as other firms could bundle MBS out of their own originations, or develop MBS using mortgages purchases through Fannie and Freddie’s networks. In both cases, banks could separately pay for the federal government guarantee.

3. Competition among multiple securitizers leads to greater pass-through of any implicit federal subsidy from the MBS-level guarantee. The federal government will charge an insurance premium for the MBS-level guarantee, but as with many government insurance programs, it is hard to be confident that the government will charge the complete actuarial cost of housing insurance. Competition is thus essential to ensure that any subsidy implicit in underpricing of insurance accrues to homeowners – the ultimate target of the government intervention.

4. The federal role in providing a guarantee for home finance is made transparent, at least to the extent that the premium charged on the MBS backstop is actuarially fair. If Congress decides to subsidize homeownership by directing that the premium be set too low, this will show up as a credit subsidy in the budget.

5. A liquidity backstop is still available in times of credit market stress. The government guarantee on MBS means that investors will continue to provide capital for housing investment to originating banks and thus to homeowners. In addition, in times of particular stress, the Federal Reserve could provide funding as was the case with its 2008-2010 program to buy GSE MBS and debt. In principle the Treasury could provide liquidity with a vote of Congress (meaning that the Fed is likely to be the agency doing this in practice). This provision of liquidity in times of credit market stress is distinct from affordable housing subsidies that would be implemented as normal tax and expenditure policies.

Disadvantages

The proposal would result in Fannie and Freddie being fully private, but there would continue to be a government backstop on the MBS that they create – a hybrid model of sorts. There are inevitably risks with any mixing of public and private purposes and incentives, and these must be weighed against the benefits of the proposed structure. Among the downsides of our proposal are:

1. The ongoing government involvement in housing finance means that there is the possibility of implicit fiscal liabilities and inevitably some distortion of capital in favor of housing (which is already quite favored through the tax code). Our proposal takes as given that government participation in housing will continue – we do not seek to put forward a proposal that ends the backstop but instead look to improve it.

2. Allowing entry into securitization could lead to a fragmented market for MBS that possibly reduces liquidity. This is a concern raised by Woodward and Hall (2009). All conforming MBS will have the same credit guarantee from the federal government, but MBS could differ considerably on other dimensions, notably prepayment risk. This could lead to lower liquidity and higher borrowing costs. If this is the case, however, it would be natural to expect firms to develop mechanisms to offset this, such as by swapping mortgages and thus mixing up the contents of MBS.

3. The proposal puts considerable stress on the definition of a conforming loan, since many more entities are allowed to put together bundles of conforming mortgages. Originators and securitizers will have incentives to put their risky loans into a government-backed MBS, making the definition of conforming loans a key point of stress in the proposal. On the other hand, the federal regulator will be aware of this and devote considerable resources to ensure that the quality of conforming loans remains high. Moreover, originating firms should be required to maintain an economic interest in mortgages to align incentives for high-quality conforming loans. And GSE shareholders and management will have an incentive to monitor mortgage quality, since they will be wiped out before the government backstop applies.

4. Steep administrative costs. With the guarantee on an MBS-level basis, the federal government will need to track each and every MBS issued by a variety of firms, rather than just focusing on the safety and soundness of two firms. It would not be surprising to have the government hire Fannie and Freddie to monitor the loans in conforming MBS, if conflicts of interest can be addressed.

5. Firms that enter the market to securitize conforming MBS will be allowed to hold their own MBS on the balance sheet – that is, new firms will be allowed to have portfolios. (As an example, a bank could pay for the government guarantee on MBS made up of loans it originates and then buy these MBS for its portfolio). This again puts stress on the definition of a conforming mortgage to ensure that originators are not obtaining an underpriced government guarantee, but this stress exists already. This feature also puts stress on the government pricing of the guarantee, but that stress exists already as well. If the new entrants are banks (which seems likely), their supervisor will have to be alert to the danger posed by poor underwriting quality – as every supervisor is in the wake of the crisis.

The biggest downside of this model is that it might just be better to get the government out of the business of providing guarantees for housing. There are other ways to subsidize housing, including direct assistance to people with low-incomes such as through vouchers or other subsidies to buy or rent a home or apartment. Housing-related subsidies for middle class families could be implemented by subsidizing interest rates on conforming mortgages up to a certain amount (e.g., the limit for a conforming loan) or by providing a flat housing credit. Providing such direct subsidies without guarantees would avoid the inevitable moral hazard that comes about with a guarantee. On the other hand, the moral hazard likely exists even without a guarantee in place, because of the belief that a guarantee will be applied in a crisis – this is the legacy of the actions taken over the past three years in response to the financial crisis.

Our feeling is that this bridge has been crossed and it will be impossible in practice to convince the market that a guarantee will not be put in place during a future credit disruption in order to ensure that housing credit remains available even in very bad states of the world with considerable credit stress. Since the Fed (or Treasury) could always apply a guarantee in a crisis, the way to “avoid” the moral hazard of an implicit guarantee is to make it explicit and have it exist at all times, but then charge for it. This might be second best to having no guarantee at all, but we believe that a housing market without a government backstop is not a realistic option (again, because the guarantee will be implicit and expected in times of market stress).

ALTERNATIVES AND EXTENSIONS

Under our proposal, Fannie and Freddie would emerge from conservatorship as fully private companies, with a simpler mandate: to securitize and guarantee conforming mortgages. They would be forbidden from holding mortgage investment portfolios, and would be stripped of their special status. The government would provide an explicit guarantee on conforming MBS and would make it available not only to Fannie and Freddie, but also new entrants. In short, the government would focus on its comparative advantages: insuring against large scale housing shocks and providing financial supervision and regulation, while the private sector would handle everything else.

Over the past few years, analysts have identified several other approaches to reforming the housing GSEs (for good overviews, see Bernanke 2008 and GAO 2009; for specific ideas, see Jakabovics 2009, Jaffee et al. 2009, and Woodward and Hall 2009; MBA August 2009 outlines a proposal similar to ours in certain respects). These include:

1. Restructuring the two firms as regulated public utilities. In this approach, the firms would be subject not only to tight financial regulation, but also tight control over the fees that they charge and products that they offer. Proponents of this approach believe that utility-style rate regulation could help pass through more of the benefits of government support to borrowers, rather than allowing them to be captured by shareholders and management. Our preference, however, is to encourage such pass through via market competition. Under our proposal, competition is enhanced both by allowing additional firms to purchase a government guarantee on their MBS and by charging actuarially fair rates for the insurance, which will make competing mortgage products more attractive. The public utility model would be most attractive if scale economies turn out to limit the degree of competition that emerges in the market. Even in that case, however, policymakers would have to balance the potential pass-through benefits of utility regulation with the potential inefficiencies and discouragement of innovation that may result as well.

2. Restructuring the firms as a government agency along the lines of a combined FHA and GNMA. In this approach, the firms would guarantee conforming mortgages and package them into MBS. This approach would impose greater fiscal risks on the government than the current system or our proposal; the government would be guaranteeing losses on individual mortgages, rather than on firms that have a capital buffer (current system) or on MBS that are backed by firms with a capital buffer (our proposal). In principle, that higher risk could be offset by larger, actuarially fair fees in return for the guarantees. The other downside of this approach is that it may limit future innovation in mortgage finance. To be fair, however, we should note that it was actually GNMA that invented pass-through MBS, one of the most important and beneficial mortgage innovations in recent decades.

3. Eliminating the federal role entirely. Under this approach, the federal government would eliminate the guarantee (either implicit or explicit) and would sell Fannie and Freddie to private investors. In the absence of the federal guarantee, it is unlikely that Fannie or Freddie would be able to offer meaningful guarantees on conforming mortgages. The two firms would likely become consulting firms, like Fair-Isaac. This reform would have wide-ranging effects on the mortgage market. The market for agency MBS would shrink (since only GNMA would continue to issue them), thus limiting one potential tool of monetary policy. Lenders would likely move more toward adjustable rate mortgages and away from 15- and 30-year fixed rate mortgages. Middle-class housing markets would be more exposed to occasional liquidity droughts, although the government could always take steps to counter severe crises. On the positive side, such a step would reduce the degree to which federal policy favors housing over other forms of investment and would maximize innovation as firms would introduce alternative financing means that have worked in other nations (e.g., covered bonds).

4. Gradual elimination of the federal role. This approach would move to the same end state as #3, but over a period of years, perhaps a decade. Administratively, the easiest way to do this would be to cap the conforming loan limit in nominal terms, so that inflation and housing price increases (if and when they restart) would gradually reduce the relevance of the conforming market. In practice, it is difficult to believe that this is politically realistic.

5. Returning to the previous system with better regulation. Under this approach, the GSEs would hold more capital and face tighter limits on their investment portfolios. They might even pay an explicit fee to the federal government for an explicit backstop. In this approach, the firm’s MBS and debt would both be backed by the federal government. Although tighter regulation would help, we believe that this approach would fail to address the fundamental problem of the previous system: the conflict between private profit and socialized risks.

6. Combining reform with expanded, explicit backing for mortgage finance. Some analysts have also proposed that reform be combined with an expanded government role in backstopping mortgage lending. Jaffee et al. (2009) propose reforms similar to ours, but also recommend that the conforming loan limit be eliminated. That would extend the government guarantee to mortgages of any size. Passmore and Hancock (2009) suggest that the government act as a broad mortgage bond insurer, covering not only MBS issued by Fannie and Freddie, but also their debt, that of the Federal Home Loan Banks, any covered bonds issued by authorized depository institutions, and any MBS issued by authorized securitizers. These approaches would make the government guarantee explicit (as we also recommend) and would ensure that mortgage finance is available even in times of financial distress. They raise significant concerns, however, about the impacts of extending the federal role in housing finance even further.

CONCLUSION

Our proposal balances the strengths of the previous system in ensuring liquidity for housing against the critical need to protect taxpayers and the financial system from the systemic risks posed by the previous GSE model. Taxpayers will take on the tail risk of another nationwide decline in housing prices, but will be compensated for this. Meanwhile, competition will help ensure that government subsidies flow through to homeowners rather than being captured by the shareholders and management of private firms. The provision of taxpayer support for low-income housing remains very much possible in our proposal. This support would be funded by a tax on the GSEs and their competitors, but be carried out in a transparent way through regular appropriations channels.

The awkward status of Fannie Mae and Freddie Mac is a lingering reminder of the firms’ problematic business model that greatly contributed to the housing bubble and financial crisis. A new model for the two firms requires an act of Congress. Our proposal provides a specific plan. We welcome comments and criticisms.

Donald B. Marron is director of the Urban-Brookings Tax Policy Center and a visiting professor at the Georgetown Public Policy Institute. Phillip L. Swagel is a visiting professor at the McDonough School of Business at Georgetown University, where he teaches classes on financial markets and directs the Center for Financial Institutions, Policy, and Governance. The findings and conclusions are solely those of the authors and do not represent the views of Georgetown University or the Urban Institute.

References

Bernanke, Ben, “The Future of Mortgage Finance in the United States,” UC Berkeley/UCLA Symposium: The Mortgage Meltdown, the Economy, and Public Policy, Berkeley, CA, October 31, 2008.

Government Accountability Office, “Fannie Mae and Freddie Mac: Analysis of Options for Revising the Housing Enterprises’ Long-term Structures,” September 2009.

Hancock, Diana and Wayne Passmore, “Three Initiatives Enhancing the Mortgage Market and Promoting Financial Stability,” The B.E. Journal of Economic Analysis & Policy 9(3), Fall 2009.

Jakabovics, Andrew, “The Future of the Mortgage Market and the Housing Enterprises,” Testimony before the Senate Committee on Banking, Housing, and Urban Affairs, October 8, 2009.

Jaffee, Dwight, Matthew Richardson, Stijn Van Nieuwerburgh, Lawrence J. White, and Robert E. Wright, “What to Do about the Government-Sponsored Enterprises?,” in Acharya, Viral V. and Matthew Richardson, eds., “Restoring Financial Stability: How to Repair a Failed System,” New York University Stern School of Business, 2009.

Krainer, John, “Recent Developments in Mortgage Finance,” Federal Reserve Bank of San Francisco Economic Letter, October 26, 2009.

Mortgage Bankers Association, “Recommendations for the Future Government Role in the Core Secondary Mortgage Market,” August 2009.

Passmore, Wayne, Shane Sherlun, and Gillian Burgess, “The Effect of Housing Government-Sponsored Enterprises on Mortgage Rates,” Real Estate Economics 33(3), Fall 2005.

Swagel, Phillip, “The Financial Crisis: An Inside View,” Brookings Papers on Economic Activity, Spring 2009.

Wallison, Peter J. and Charles W. Calomiris, “The Last Trillion-Dollar Commitment: The Destruction of Fannie Mae and Freddie Mac,” American Enterprise Institute, September 2008.

Woodward, Susan and Robert Hall, “What to Do about Fannie Mae and Freddie Mac?,” Financial Crisis and Recession Blog, January 28, 2009.