Trump’s Fiscal Legacy: A Comprehensive Overview of Spending, Taxes, and Deficits

Photo: trekandshoot/iStock

President Donald Trump’s tax, spending, and deficit legacy is still being defined. Critics point out that Trump’s tax cuts and spending increases led to a $3 trillion budget deficit. They note that Trump’s presidency saw the debt surpass 100% of the economy, even though he came into office with a healthy economy, declining interest rates, and relative peace after 15 years of global military conflict.

On the other hand, the president’s defenders respond that he inherited large budget deficits that were already projected to grow on autopilot due to escalating Social Security and Medicare costs. They argue that the 2017 tax cuts contributed heavily to the growing economy through 2019. Finally, they note that the president repeatedly proposed budgets with significant deficit reduction but was thwarted by a bipartisan congressional majority that aggressively supported expensive new initiatives, as well as by a global pandemic that virtually everyone agreed required a massive federal response.

The end of Trump’s presidency allows for a final assessment of his tax, spending, and deficit record. As the methodology section explains, this analysis begins with the 10-year budget baseline that President Trump inherited in January 2017 and measures all subsequent tax and spending changes through the February 2021 baseline, which was released as the president left office. The analysis is based on more than a dozen Congressional Budget Office (CBO) baseline updates over these four years, supplemented with the line-item scores of all notable bills signed into law by President Trump.[1]

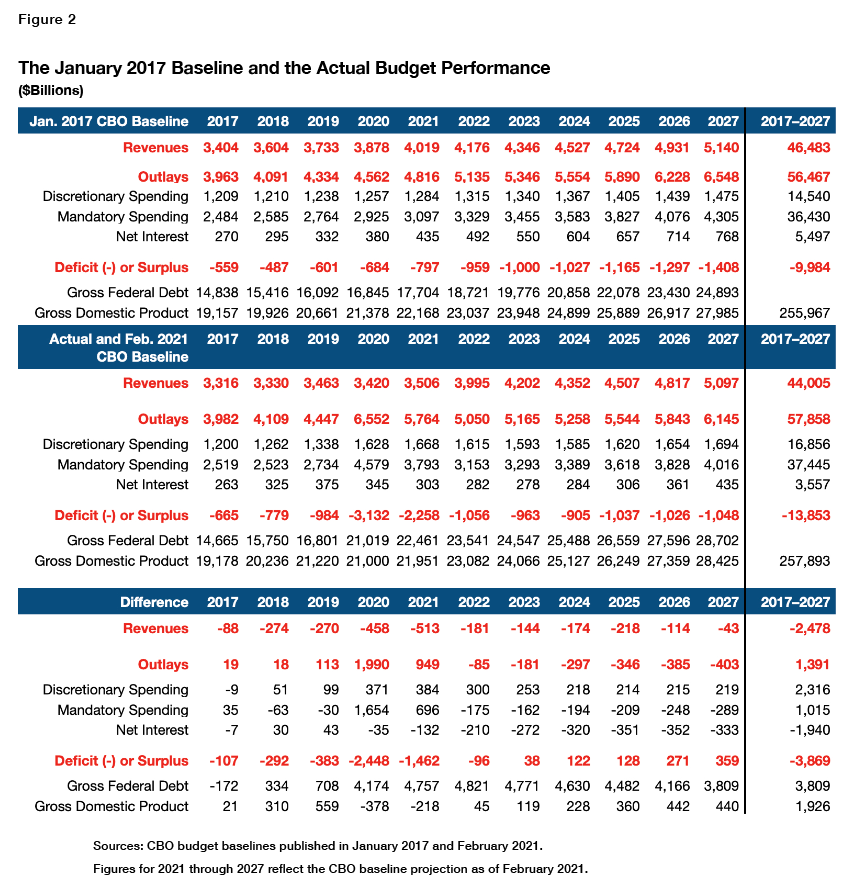

- When President Trump entered the Oval Office, CBO projected the cumulative 2017–2027 budget deficits would be $10.0 trillion. When he left office four years later, CBO’s projected deficits for the same period were $13.9 trillion. The president signed or enacted $7.8 trillion in new initiatives, the costs of which were partially offset by $3.9 trillion saved from economic growth revenues and technical re-estimates of taxes and spending levels.

- Economic and technical factors produced a substantial $3.9 trillion in actual and projected savings over this period. Of this amount, $2.7 trillion comes from falling interest rate projections, which reduced the projected cost of net interest on the national debt. Another $1.3 trillion comes from higher tax revenues produced by faster economic growth projections. Technical re-estimates have reduced mandatory spending projections but also tax revenues. Most of these savings are projected to occur later in the 2017–2027 period and thus may not materialize if economic growth slows or interest rates rise.

- President Trump signed legislation and approved executive actions costing $7.8 trillion over the decade—compared to $5.0 trillion for President Obama and $6.9 trillion for President Bush, and he enacted these costs in just a single four-year presidential term, compared to his predecessors’ eight years in the Oval Office. The largest drivers were pandemic relief legislation ($3.9 trillion), the 2017 tax cuts ($2.0 trillion), and legislation raising the discretionary spending caps ($1.6 trillion).

- President Trump’s four annual budget proposals were scored as reducing budget deficits by $2.4 trillion over the subsequent 10 years. Nearly all proposed savings came from repealing and replacing Obamacare, as well as vague promises to cut domestic discretionary spending nearly in half. Outside of the budget documents, President Trump did not aggressively push either initiative after 2017.

- Trump left the White House with the largest peacetime budget deficit in American history and a national debt exceeding 100% of the economy for the first time since World War II. The failure to address unsustainable Social Security and Medicare costs leaves a projected 30-year baseline deficit of $112 trillion.

$3.9 Trillion in Additional Deficits

When President Trump took office in January 2017, he inherited a growing economy and budget deficits that had gradually fallen to 3% of GDP in the years since the Great Recession. At this time, the Congressional Budget Office (CBO) projected that the $585 billion budget deficit from 2016 would dip to $487 billion by 2018, before the baby boomer–driven rise in Social Security and Medicare costs would gradually push deficits up to $1.4 trillion by 2027. Overall, CBO projected that $10.0 trillion in deficits over the 2017–2027 period would drive the debt held by the public to $24.9 trillion (see Figures 1 and 2).[2]

Yet while running for president, Trump pledged to balance the budget and then pay off the entire national debt. He boasted to the Washington Post’s Bob Woodward, “we’ve got to get rid of the $19 trillion in debt … I think I could do it fairly quickly … I would say over a period of eight years.”[3] Of course, doing so would be virtually impossible—politically, economically, and mathematically—especially given his promise not to cut Social Security and Medicare, which drove virtually the entire projected rise in debt. Trump’s plan to achieve nearly $25 trillion in 10-year savings consisted of renegotiating trade deals, bringing overseas companies (and their taxes) back to America, repealing Obamacare, and growing the economy. While paying off the debt within a decade was an absurd promise, serious deficit reduction was possible given the growing economy, falling defense costs, and a unified Republican Congress that had long promoted significant entitlement reform.

Instead, as Trump left office, the 2017–2027 budget deficits were estimated at $13.9 trillion—$3.9 trillion higher than the inherited projection. During each of Trump’s four years in the White House, the actual deficit exceeded the original CBO’s projections by at least $100 billion. For the first time in American history, the deficit in fiscal year 2020—amid a massive bipartisan fiscal response to the pandemic—reached $3 trillion (accounting for 14.9% of GDP, a level that has been exceeded only during the height of World War II).

The president left office with a $2.3 trillion deficit projected for 2021. Potential budget savings forecast for the 2022 through 2027 period are driven by the expiration of expensive legislation as well as economic and technical re-estimates, not by any deficit-reduction legislation signed by President Trump.

Economic and Technical Factors Produced Substantial Savings

CBO classifies three factors that drive all movements in budget deficits: new legislation, changes in economic growth rates, and technical changes brought on by noneconomic factors (such as new technologies altering health care costs). Under President Trump, faster economic growth and technical revisions saved an estimated $3.9 trillion over the 2017–2027 decade relative to the initial CBO projections. However, new legislation and presidential initiatives cost $7.8 trillion over the same period (see Figures 3 and 4). Most of these costs will be borne between 2017 and 2021, while the economic and technical savings are projected to accrue towards the end of the 10-year window.

(As the methodology section explains, most changes in this report are scored over the full 2017–2027 period because most policy, economic, and technical changes have long-term budget effects that can be measured against the original January 2017 CBO baseline covering the 2017–2027 period).

The $3.9 trillion in economic and technical budget savings can be broken down as follows:

- Economic Growth Revenues ($1.3 trillion saved). During the Trump presidency, the total economic output projected for the 2017–2027 period increased by $1.9 trillion, which is expected to bring in $1.3 trillion in additional tax revenues. Even though the beginning of this period, from 2017 to 2020, included a deep recession, an extra $511 billion in total economic output produced $68 billion in tax revenues.

- Technical Re-estimates of Revenues ($1.7 trillion cost). On the flip side, technical revisions reduced projected tax revenues by $1.7 trillion over the same decade—more than offsetting the economic gains. Much of these losses resulted from downward revisions of corporate profits and taxable income, as well as lower-than-expected individual taxable income.

- Economic and Technical Re-estimates of Mandatory Spending ($1.6 trillion saved). Economic and technical factors trimmed the mandatory spending baseline by an estimated $1.6 trillion over the 2017–2027 period, but these savings will mostly come during the latter years. Leading drivers included slightly smaller-than-expected Social Security old-age and disability caseloads, as well as Medicare savings from lower utilization and higher premium payments.

- Technical Re-estimate of Net Interest Costs ($2.7 trillion saved). However, the largest automatic savings came from net interest payments due to projected lower interest rates. During the Trump presidency, the average interest rate paid on the federal debt remained near the 2.1% rate that was projected when he entered office. However, the average interest rate projected across the 2021–2027 period fell from 3.0% to 1.3%—reducing projected net interest costs by a staggering $2.7 trillion.[4] In 2027 alone, lower interest rates are projected to reduce net interest costs by $491 billion.

Falling interest rates on the (growing) national debt are by far the largest reason that CBO’s projected baseline deficits for the 2023–2027 out-years actually fell during the Trump presidency despite the costs of new legislation. Even with trillions in new debt signed into law by President Trump, the projected 2027 interest amount fell from $768 billion to $435 billion. For comparison, between 1997 and 2027, the debt held by the public will have skyrocketed from $3.8 trillion to $28.7 trillion (655%), yet annual interest costs will have grown only from $244 billion to $435 billion (78%).[5] Had interest rates remained at 1990s levels, annual budget interest costs would approach $2 trillion by 2027.

How much credit does President Trump deserve for the $3.9 trillion in projected economic and technical budget savings over the decade? Probably not much. More than two-thirds of the savings reflect a decline in interest rates that has been gradually occurring for three decades, driven by global economic factors, demographics, productivity trends, and Federal Reserve policy.[6] (President Obama also saved $2.3 trillion over the decade from lower-than-projected interest rates.) Technical savings in mandatory programs were also driven by broader health and economic trends and were offset by projected lower tax revenues from technical re-estimates. The 2017 tax cuts likely contributed to the $1.3 trillion in higher projected economic growth tax revenues, although those numbers also partially reflect higher inflation and other economic factors.

It is also important to note that most of these economic and technical savings are projected to occur toward the end of the 2017–2027 period. They do not reflect significant savings that have occurred already, which means they are not guaranteed to occur. If interest rates continue rising—or if the post-pandemic economic recovery is slower than expected—those trillions of dollars in projected savings could vanish.

Yet overall, the economy and technical revisions remain a major—and often forgotten—driver of deficit trends. During the Bush presidency, economic and technical revisions worsened deficits by an estimated $3.3 trillion over the decade. Those factors saved $400 billion over the decade under President Obama and $3.9 trillion over the decade for President Trump. This $3.9 trillion head start should have made it easy for President Trump to substantially reduce budget deficits during his presidency. Instead, new legislation—driven in part by the Covid-19 pandemic response—pushed deficits substantially higher.

$8 Trillion in New Legislation and White House Policies

During President Trump’s four years in office, he signed legislation (and issued executive orders) that cumulatively added $7,787 billion to 10-year deficits. His policies reduced tax revenues by $2,098 billion, increased spending by $4,912 billion, and added $777 billion in interest costs.[7]

The main components are listed in Figure 4, and summarized below:

- Pandemic-Relief Legislation ($3,940 billion). The pandemic drove more than half of all new legislative costs during the Trump presidency. Direct health spending such as pandemic testing, vaccine development and distribution, and payments to health providers accounted for just $390 billion, or approximately 10% of all pandemic spending. Mitigation activities meant to slow the spread of Covid, such as funding for disaster relief, maintaining key federal operations, and upgrading school facilities, totaled $139 billion. The remaining $2,999 billion in assistance consisted of economic aid, primarily to families and businesses affected by the pandemic. This included Paycheck Protection Program loans for small businesses ($1 trillion), multiple rounds of relief payments for families ($457 billion), enhanced unemployment benefits ($392 billion), other general business aid ($313 billion), expansion of traditional safety net programs ($143 billion), and paid-leave programs ($105 billion). These deficit-financed costs added $412 billion in projected interest costs through 2027.

The coronavirus pandemic spurred one of the largest federal mobilizations in American history. In 2020 and 2021, federal Covid-relief spending amounted to 8.7% of GDP. By comparison, between 1933 and 1939, federal spending expanded by an average of 5% of GDP to combat the Great Depression. The $2.2 trillion legislative response to the “Great Recession” between 2008 and 2012 equaled 3% of that period’s GDP.[8] Nor has any military action since World War II exceeded the federal response to the pandemic (although the Korean War mobilization was comparable). The pandemic response produced America’s first $3 trillion budget deficit in 2020, which, at 14.9% of GDP, represented the largest-ever peacetime deficit as a share of the economy.

The pandemic response was expensive—and likely excessive in aid to state governments as well as individuals who suffered no income losses, while shortchanging direct Covid testing and mitigation. But there is little doubt that failing to respond to the pandemic, or to compensate businesses and families for their lost income, would have produced catastrophic economic damage and suffering that would have also cost the federal government trillions in lost tax revenues and higher automatic income-support payments. In other words, much of these budgetary costs were inescapable. Additionally, despite its stratospheric immediate cost, nearly all pandemic aid enacted in 2020 was scheduled to be temporary and therefore should have a smaller permanent budgetary cost than some items detailed below that are likely to continue adding debt each year indefinitely.

- The 2017 Tax Cuts ($1,969 billion). The most controversial budget battle of the Trump presidency focused on his tax reform proposal. Congressional Republicans had spent years drafting revenue-neutral tax reform frameworks that were intended to simplify the tax code by combining a broader tax base with lower tax rates. Earlier GOP tax reform models focused primarily on reducing America’s 39% (federal and state combined) corporate tax rate, reducing corporate tax loopholes, and moving toward a territorial international tax system.

Tax reform was the first major legislative priority for the Trump administration and the Republican Congress, but the plan that emerged diverged from this model in two significant respects. First, revenue-neutral tax reform became more of a traditional tax cut, as interest groups swarmed to protect their tax preferences. Second, family tax cuts took budgetary precedence over corporate tax cuts. The result was the Tax Cuts and Jobs Act (TCJA), which is estimated to add $1,969 billion in 10-year deficits. The tax cuts for individuals—which were distributed in roughly equal proportion to the previous tax burden[9]—totaled $1,438 billion (plus $20 billion added later to permanently expand the medical-expense deduction). The corporate and international reforms cost $329 billion over the decade. This law also added $182 billion in interest costs over the 2017–2027 period.[10]

Because the TCJA was passed using budget reconciliation procedures that disallow new long-term deficits, many of its most popular family tax cut provisions are set to expire by the end of 2025, at which point the law would become deficit-neutral moving forward. However, there is little reason to believe that Congress or a future president would allow the family tax cuts to expire. When the similar 2001 and 2003 tax cuts were set to expire in 2014, a bipartisan congressional majority made them permanent for all families except the highest-earning 2%. If Congress makes these latest tax changes permanent, the long-term cost will be approximately 0.7% of GDP, plus an additional 0.6% of GDP (and rising) in interest costs over the next 30 years.

- Higher Discretionary Spending Caps ($1,568 billion). The 2011 Budget Control Act imposed tight caps on annual discretionary spending through 2021. Within a few years, Congress began enacting legislation to gradually increase current cap levels by roughly $30 billion annually. Because returning to the original cap levels would mean ratcheting annual appropriations back down by $30 billion—which Congress is loath to allow for regular government operations—most observers expected the Republican Congress and new administration to renew the discretionary spending levels at $30 billion above the original cap levels.

Instead, Presidential Trump signed the Bipartisan Budget Act of 2018, which raised the spending caps by $143 billion—a 13% hike over the previous year’s level. That inflated spending level became a starting point to expand the cap levels by an additional average of 2.4% annually for the next three years. The 2021 expiration of the spending caps then ensured that these higher spending levels would become the new permanent discretionary spending baseline. The result was an additional $1,448 billion in higher “regular” discretionary spending (and baseline levels) during the 2017–2027 period, plus $120 billion in resulting interest costs. These budget deals raised the long-term discretionary spending baseline by 0.7% of GDP.

Essentially, these budget deals reflected a bipartisan compromise. Republicans won $761 billion in higher defense spending, and Democrats secured $687 billion in nondefense discretionary spending. The largest increases in nondefense discretionary spending included veterans’ benefits (up 22%), natural resources and environment (20%), income security (20%), health research and regulation (18%), justice administration (18%), and housing aid (14%).[11]

- Disaster Aid and Additional Discretionary Spending ($493 billion). Not all discretionary spending was governed by statutory spending caps. Spending on overseas contingency operations (OCO) began as a separate fund for military operations in Afghanistan and Iraq and did not count against traditional spending caps. Also exempt from Congressional spending limits are emergency spending in response to natural disasters, program integrity funding to root out waste, wildfire suppression, and even some funding to combat the opioid epidemic.[12] Some of this spending appeared in the original January 2017 CBO budget baseline, but additional spending increased the baseline cost of these spending categories by an estimated $419 billion over the 2017–2027 decade. The disaster aid classified as mandatory spending added $32 billion, and the resulting interest costs total $42 billion. Disaster aid is the most unpredictable category of spending, so the 2021—2027 baseline amounts reveal little about actual spending levels. Events will determine whether the baseline figure is optimistic or pessimistic.

- Presidential Imposition of Tariffs ($367 billion in savings). Tariffs, taxes imposed on imported goods, are the only policy change in this section that was imposed by President Trump without legislation. This is possible because Congress has increasingly delegated tariff authority to the executive branch.[13] President Trump campaigned in 2016 on renegotiating trade deals and blocking low-cost imports from competing with American firms. Beginning in 2018, the president imposed a series of tariffs that —gradually expanded to include aluminum, steel, solar panels, washing machines, and approximately $200 billion of Chinese goods.

As a result, annual federal customs revenue quickly doubled from $35 billion to $70 billion between 2017 and 2019.[14] This amounted to one of the largest tax hikes in decades, and for many families, offset a large portion of the TCJA tax cuts.[15] The Penn-Wharton Budget Model calculated that President Trump’s tariffs will “cost the median U.S. household with earnings of $61,000 about $500 to $550 a year. That figure is the equivalent of raising Social Security taxes by 1 percentage point.” Targeted nations also responded with retaliatory tariffs on American exports, costing American jobs in affected industries.[16] The CBO assumes tariff policies will remain in place and generate $400 billion in revenues through 2027. However, $33 billion of this revenue has been redirected to farmers as compensation for lost exports, leading to net savings of $367 billion.

- Repeal of Obamacare Individual Mandate and IPAB ($317 billion in savings). The Affordable Care Act (“Obamacare”) mandated that most Americans carry a minimum level of health insurance or pay a penalty that reached $695 per uninsured adult and $347.50 per child, up to a family maximum of $2,085 or 2.5% of their income. After President Trump and Congressional Republicans failed to repeal the ACA, they settled for a provision in the 2017 TCJA reducing the individual mandate penalty to zero. This policy saved the federal government a projected $314 billion through 2027, as the lost revenue from the penalties was substantially outweighed by the reduction in Medicaid and ACA exchange subsidies for families who quickly took advantage of the new freedom to drop their health coverage.

The individual mandate was not the only part of Obamacare to get repealed. The Bipartisan Budget Act of 2018 eliminated the Independent Payment Advisory Board (IPAB), which was intended to consist of 15 presidentially appointed (and Senate-confirmed) health experts who were charged with recommending Medicare savings proposals that Congress would have to either accept or replace with equivalent policies. Because it was so controversial and unpopular, the board was never actually created. Still, CBO estimated that repealing IPAB would cost $17 billion through 2027 by eliminating a mechanism for Medicare savings. Interest savings from the two policies in this section would total $20 billion through 2027.

- Repeal of Obamacare Taxes ($299 billion). During President Trump’s term, there was also a bipartisan agreement to repeal three of the ACA’s most unpopular taxes, the “Cadillac tax,” the health insurer tax, and the medical device tax. The “Cadillac tax” was a 40% excise tax on high-end employer-issued health plans that was so unpopular with labor unions, large employers, and families that it had never been implemented. Even so, its permanent repeal was scored as costing $133 billion through 2027. The health insurer tax was applied to health insurance providers based on their market share, which, according to critics, was passed on to families in higher premiums. Congress rotated between applying and suspending the tax until finally repealing it at a cost of $125 billion through 2027. The medical device tax—a 2.3% excise tax on medical devices sold—was blamed for job losses in the industry. It was suspended beginning in 2016, and the eventual repeal cost $23 billion through 2027. The final $18 billion tab came from additional net interest costs resulting from this lost tax revenue.

- All Else ($201 billion). The remaining $201 billion in costs comes from hundreds of smaller policies. President Trump and Congress spent $131 billion renewing expiring policies, mainly covering taxes, health care, customs fees, and the mandatory sequester that was created in the 2011 Budget Control Act. Other costs included $37 billion in various tax changes, $23 billion in expanded veterans’ income assistance, and $10 billion for 9/11 victims and first responders. On the flip side, $31 billion was saved from various health programs, mostly provider savings to offset the extensions of expiring health programs. Various mandatory and tax changes cumulatively cost the remaining $31 billion.

Are These Purely “Republican Deficits?”

Partisans often rate each party’s commitment to fiscal responsibility by the budget surplus and deficit changes during their respective presidencies. This approach is flawed for several reasons. First, each president inherits a vastly different federal budget baseline, consisting of budget surpluses or deficits that are rising or falling almost entirely on autopilot. (For example, these inherited 10-year baseline projections have ranged from a $6 trillion surplus for President George W. Bush to an incoming $10 trillion deficit for President Trump.) Second, as this report shows, much of the movement in the surplus or deficit is driven by economic and technical factors that are mostly outside of White House influence. Consequently, assessing a president’s deficit performance should be based largely on the legislation enacted rather than the inherited baseline or the economic and technical movements of that baseline.

Even when it comes to enacted legislation, however, presidents are also limited to signing what Congress will pass. And during the Trump presidency, much of the $8 trillion in enacted legislation was passed by overwhelmingly bipartisan Congressional majorities.

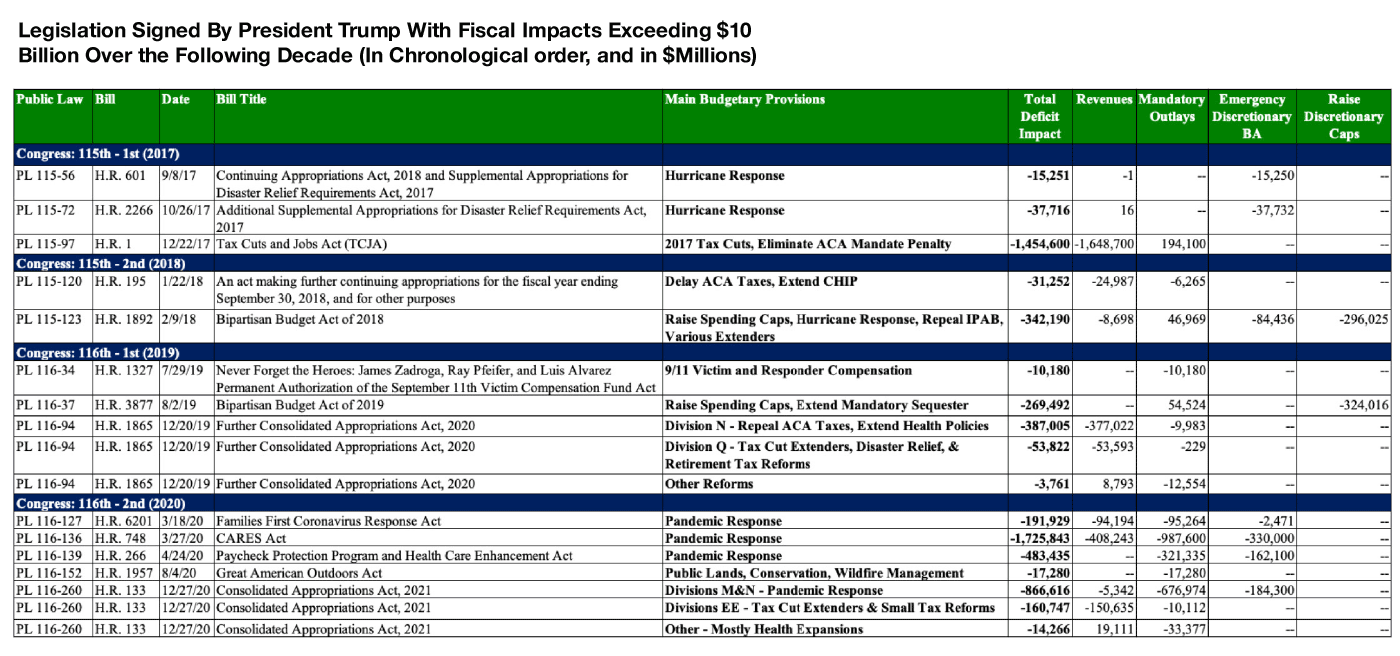

Consider the eight bills that Congress passed and President Trump signed costing at least $100 billion over the baseline, plus a separate pandemic relief bill (P.L. 166-159) that accelerated nearly $100 billion in previously enacted expenses.[17] The most partisan of these nine bills was obviously the 2017 tax cuts (which also repealed the Obamacare individual mandate penalty). That law was passed exclusively by Republicans without a single Democratic vote. (See Figure 7 in the appendix for the largest bills signed during the Trump presidency.)

The other eight bills—which consisted of five pandemic-relief laws, the 2018 and 2019 Bipartisan Budget Acts that raised the discretionary spending caps, and the 2019 law repealing key Obamacare taxes—were generally bipartisan. In fact, each of the eight bills passed the Senate with the majority support of both Republicans and Democrats. Senate Democrats cumulatively voted 94% in favor of these bills, and Senate Republicans cumulatively voted 76% in favor—not counting the CARES Act that passed the Senate by voice vote.

In the House, the five pandemic-relief bills each passed with overwhelming bipartisan majorities, with House Democrats cumulatively voting 99.7% in favor and House Republicans voting 79% in support (not counting one bill that passed by voice vote). The remaining three bills had House votes that were somewhat more partisan. In 2018, three-fifths of House Democrats voted against legislation raising the budget caps, due mostly to nonbudgetary disagreements over immigration policy (their leaders endorsed the higher spending levels, voted for the appropriations later funding the spending targets, and then voted to raise the caps again the following year).[18] On the flip side, three-fifths of House Republicans voted against the 2019 legislation repealing the Obamacare taxes (even as they supported the policy), mostly due to disagreements with appropriations policies included in the same bill. The only post-TCJA concerns over fiscal issues arose when two-thirds of House Republicans voted against the 2019 legislation again raising the discretionary spending caps, mostly due to deficit concerns.

Cumulatively, following the partisan 2017 tax cuts, the remaining tax reductions and spending expansions were generally bipartisan. The only exceptions were three House votes in which the minority party often supported the deficit-increasing provisions but voted no because of other issues in the bills. With neither party enjoying a filibuster-proof Senate majority and control of the House flipping from Republican to Democrat following the 2018 elections, all of these major bills except the 2017 tax cuts were crafted by the two parties together to balance their interests, such as combining a defense spending expansion with a similar hike in domestic spending.

Incorporating the president’s tariffs—which can be classified as partisan because they did not go through Congress at all—means that roughly $1.3 trillion of the new deficits reflect purely Republican policies, and $6.5 trillion resulted from (often overwhelmingly) bipartisan legislation.

A similar phenomenon occurred during the Obama presidency, when $5.0 trillion in enacted legislation was dominated by $4.1 trillion in bipartisan extensions of various current tax policies such as the 2001 and 2003 tax cuts. In fact, the $1 trillion stimulus legislation in 2009 was the only major deficit-hiking bill passed by an almost-exclusively Democratic majority during those eight years.[19] Over the previous two presidencies, the vast majority of new deficit-expanding bills has been enthusiastically bipartisan.

The Trump Budget Proposals

The previous section explains how presidents lack the authority to unilaterally determine spending, taxes, and deficits. They cannot control the inherited budget baseline, have little control over economic and technical movements, and must persuade Congress to pass any major reforms. However, presidents are free to lay out their vision for Congress in their annual budget request.

President Trump’s budget requests appear bold at first glance. A deeper analysis shows them to be vague, gimmicky, unrealistic, and even contradicted by the president’s own actions. Figure 5 shows that President Trump’s four annual budget proposals were scored by the Congressional Budget Office as reducing deficits by an average of $2.4 trillion over the subsequent 10 years. On the tax side, he proposed an average of $828 billion in 10-year tax cuts, which generally consisted of policies to repeal and replace Obamacare and later to extend the 2017 tax cuts.[20]

On the spending side, nearly all the $3.0 trillion in typical 10-year program savings came from two budget areas:

- Health Care. The Trump budgets proposed an average of $1.3 trillion in 10-year savings from repealing and replacing Obamacare and reducing payments to Medicare providers. Most of the Obamacare replacement savings proposals were vague and considered politically unrealistic.[21] After health reform failed in 2017, the president stopped pushing the issue but continued to assume the significant savings in his budget proposals.

- Nondefense Discretionary Spending. The budgets proposed an average of $1.6 trillion in 10-year savings from nondefense discretionary spending. Meeting these targets would have required nearly cutting in half this portion of federal spending, which includes health research, K–12 education, highways, and veterans’ health care. The president’s budgets refused to specify which programs would be cut, instead using a “magic asterisk” placeholder asserting that cuts would be defined later.[22] Moreover, while proposing these massive unspecified cuts, President Trump repeatedly signed legislation expanding this portion of the budget by 21% over four years (as well as enacting additional pandemic, disaster, and emergency spending).

The president’s budget proposals also tried to claim as much as $3.4 trillion in additional 10-year tax revenues based on flatly unrealistic economic growth assumptions.[23] This growth was supposed to result from the $5.5 trillion tax reform proposal the president unveiled in early 2017, but that mammoth cost was simply left out of the budget proposal.[24] In other words, the White House budget assumed a $3.4 trillion burst of economic growth revenues from a $5.5 trillion tax proposal that did not actually exist in the budget. Overall, President Trump’s budget proposals were too vague, gimmicky, and contradicted by his spending increases to serve as a legitimate blueprint of his fiscal vision.

Comparing Trump to Obama and Bush

President Trump’s record on fiscal responsibility does not compare favorably to his immediate predecessors (see Figure 6). Surely, it would not be fair to judge President Trump simply by the total budget deficits under his watch, however, as the $10 trillion 10-year baseline deficit that he inherited dwarfed the $4 trillion projected baseline deficit inherited by President Obama and the $6 trillion projected baseline surplus inherited by President Bush. That is far from a level playing field.[25]

On the other hand, President Trump also received the largest automatic deficit reductions from his inherited baseline. During his presidency, economic and technical factors that fall mostly outside of political control produced $3.9 trillion in 10-year deficit reduction, mainly through falling interest rates on the federal debt. By contrast, President Obama saved only $378 billion from these factors (as savings from falling interest rates were offset by the lost tax revenues of the slower-than-expected recovery from the recession), and President Bush lost $3.3 trillion to these factors, mainly due to lost tax revenue from the 1997–2000 economic bubble bursting, followed by the 2008 recession.

Instead of accepting this easy, automatic deficit reduction, President Trump signed legislation and approved executive actions costing $7.8 trillion over the decade—compared to $5.0 trillion for President Obama and $6.9 trillion for President Bush. In addition, President Trump enacted these costs in just a single four-year presidential term compared to his predecessors’ eight years in the Oval Office.

Surely, President Trump was a victim of circumstances to some extent, with a global pandemic that was met with a bipartisan $3.9 trillion response (which likely shortened the recession and thus contributed to some of the economic budgetary benefits described above), but most presidents face expensive circumstances beyond their control. President Bush faced the costs of responding to the 9/11 attacks, as well as substantial tax revenues lost to two economic crises. President Obama inherited a deep recession and was also saddled with a $4 trillion “cost” simply for renewing the tax policies he inherited. As stated above, presidents are also limited by the legislation Congress is willing to pass. President Obama’s more expensive initiatives were often thwarted by a Republican Congress, and President Trump was not able to persuade Congress to replace Obamacare with a less-expensive policy.

The Failure to Address Soaring Entitlements

For those concerned with fiscal responsibility, the Trump presidency represented a colossal missed opportunity. Presidential fiscal records should mainly be judged by the legislation they enact because that is a variable over which they have a reasonable degree of control. However, the escalating baseline deficits represent an economic danger that cannot be ignored. Presidents do not control the fiscal situation they inherit, but that does not absolve them of the responsibility to address worsening deficits.

President Trump inherited 74 million retiring baby boomers whose escalating Social Security and Medicare costs accounted for nearly all of the $10 trillion in projected 10-year deficits. Despite having a Republican Congress that had long promised to ensure the long-term fiscal sustainability of these programs—and House Speaker Paul Ryan, who had dedicated his career to promoting such reforms—Trump opposed all structural Social Security and Medicare reforms. Instead, the president cut taxes, increased discretionary spending, saw the loss of the Republican House majority, and then was pressured by the pandemic to sign $4 trillion in additional debt.

At first glance, the long-term budget situation may have appeared better in 2021 than in 2017. Examining the 2017 to 2027 baseline budget window, projected 2027 deficits actually dipped during the Trump presidency. However, legislated spending and tax cuts clearly worsened longterm deficits. The smaller projected deficits in those later years are based largely on assumed lower interest rates on the debt—which can change at any time, and indeed rates are already rising. The smaller future deficits also reflect the dubious assumption that Congress will allow taxes to rise substantially for lower- and middle-class families when much of the 2017 tax cuts are set to expire at the end of 2025. The slight decrease in the projected growth rate of Social Security and Medicare costs also reflect minor technical revisions that can easily be reversed.

Yet even with those assumed budget savings, the long-term budget outlook remains bleak. The CBO estimates that the next three decades will bring a staggering $112 trillion in baseline budget deficits, even under the rosy scenario of low interest rates, expiring tax cuts, and no additional spending. CBO projects that within 30 years, annual deficits will exceed 13% of the economy and push the federal debt past 200% of the economy. Even with modest interest rates, interest is projected to become the largest expenditure in the federal budget and consume half of all tax revenues within three decades.[26]

Social Security and Medicare shortfalls drive virtually the entire $112 trillion projected deficit over the next three decades. Medicare is projected to spend $78 trillion more than it collects in payroll taxes and premiums, while Social Security is expected to run a $34 trillion shortfall (both figures incorporate the resulting interest on the national debt). By 2051, these two programs will run an annual shortfall of nearly 15% of the economy.[27] That is not sustainable.

Refusing to reform Social Security and Medicare over these four years will eventually make the inevitable reforms more expensive and painful. During the Trump presidency, approximately 14 million more baby boomers retired. The current retirees grew four years older and less able to accommodate any benefit changes, while near-retirees missed out on four years to prepare for a reformed system. Delaying Social Security and Medicare reforms merely locks in higher benefits and raises the federal debt—forcing the eventual budget reforms to be larger and more drastic. Realistically, as baby boomers grow older and less able to accommodate benefit changes, the eventual fiscal reforms will more likely rely on historic middle-class tax increases. Stabilizing the national debt as a share of the economy without reforming Social Security and Medicare would eventually require choosing between options such as a 33% payroll tax rate or a 34% value-added tax.[28] Merely taxing the wealthy or cutting defense is far from sufficient.

Faced with a potentially calamitous long-term fiscal outlook, President Trump and Congress joined a long line of politicians who kicked the can down the road.

Conclusion: The Trump Budget Legacy

While President Trump inherited a daunting $10 trillion in projected baseline budget deficits over the decade, he also was granted positive conditions to significantly rein in the debt. These included $3.9 trillion in economic and technical budget savings over the decade, declining defense costs, a soaring economy, and a Republican Congress that had long promoted deficit reduction. Yet Trump instead enacted $7.8 trillion in new initiatives, pushing the debt steeply upward. While the $4 trillion pandemic response was largely unavoidable (if excessive in some areas), it would have proven more easily affordable without nearly $4 trillion in earlier tax cuts and spending expansions. Both parties of Congress bear responsibility for approving the vast majority of this new debt with broad bipartisan support.

Under President Trump’s watch, budget deficits reached a peacetime-record 15% of the economy and pushed the debt held by the public past 100% of the economy for the first time since World War II. In nominal dollars, the debt jumped from $14 trillion to $21 trillion and was projected to reach nearly $29 trillion by 2027.

The CBO-projected budget deficits for the final half of the 2017–2027 period did improve under President Trump’s watch, but these savings may prove illusory because they are based on economic and technical re-estimates rather than legislation. Projected long-term mandatory spending dropped by 1.3% of GDP due mostly to technical re-estimates that can easily change. Similarly, projected net interest costs fell by 1.2% of GDP by 2027 (despite the added debt) because CBO significantly reduced its projection of the interest rates that Washington will pay. Interest rates are already rising, however, and the 2022 10-year Treasury rate is already more than double the 1.3% rate that CBO had forecast when President Trump left office.[29] Even the higher projected levels of economic growth (and accompanying tax revenues) assume a healthy economic recovery that is not guaranteed.

On the negative side, these four years saw projected long-term discretionary spending levels rise by 0.7% of GDP and long-term revenue projections fall by 0.5% of GDP (which will expand to 1.1% of GDP if the 2017 tax cuts are renewed). Spending will continue to exceed the typical levels of the past few decades, and revenues—while growing—will not be able to keep pace.

All in all, President Trump signed expensive legislation and left even modest future budget savings increasingly dependent on assumptions of faster economic growth, declining interest rates, and technical savings such as slower growth of health care costs. Those latter factors are largely out of the control of politicians and cannot be confidently assumed to occur. Perhaps most importantly, four more years were lost by failing to enact Social Security and Medicare solvency reforms just as more of the 74 million baby boomers retired into those systems. President Trump leaves a federal budget with surging debt, unprecedented peacetime deficits, and a daunting $112 trillion baseline shortfall over the next three decades.

President Bush’s Fiscal Record: A Look Back

In January 2001, President Bush inherited a projected $5.9 trillion budget surplus over the 2001–2011 period. Instead, he oversaw a $4.4 trillion budget deficit. This $10.3 trillion fiscal decline far exceeds the $4.6 trillion decline under President Obama and $3.9 trillion decline under President Trump.[30] Additionally, President Bush’s legislative debt overwhelmingly consisted of new initiatives (some of which were thrust upon him, like 9/11), while much of President Obama’s debt resulted from extending tax policies inherited from President Bush.

Overall, the $10,286 billion fiscal decline under President Bush consisted of $5,148 billion in lower-than-projected revenues and $5,138 billion in higher-than-projected spending. Legislation cost $6,908 billion, while economic and technical changes cost the remaining $3,378 billion:[31]

- Economic and Technical Changes ($3,378 billion cost). CBO’s early 2001 projections were developed near the end of a historic stock market and economic bubble that had created surging and ultimately unsustainable tax revenues. CBO had projected a continuation of these economic trends. Instead, the bubble burst and created a brief 2001 recession, which was followed by a modest recovery before the Great Recession collapsed tax revenues.

- The 2001/2003 Tax Cuts ($2,328 billion cost). Back when the most pressing budget concern was that massive budget surpluses would pay off the entire national debt too quickly, President Bush signed large tax cuts into law. Setting aside the $503 billion in net interest costs, approximately 75% of the tax cuts went to families earning under $250,000 annually. Preventing their full expiration became a major bipartisan focus during the Obama administration.

- Defense Spending Increases ($2,169 billion cost). The 9/11 attacks and subsequent wars in Afghanistan and Iraq reversed the steep defense cuts of the 1990s. Nearly $400 billion of this cost is interest.

- Nondefense Discretionary Spending Increases ($802 billion cost). “Compassionate conservatism” had a hefty price tag. The largest budget hikes between 2001 and 2008 went to veterans’ health benefits (95%), international aid (79%), education (42%), and health research and regulation (37%).

- Other Tax Changes ($492 billion cost). The annual Alternative Minimum Tax (AMT) patch and other current-policy tax extenders dominated this category.

- Other Mandatory Spending Changes ($396 billion cost). This consists of dozens of smaller mandatory program expansions, in areas such as farm subsidies and Hurricane Katrina flood relief.

- Medicare Prescription Drugs ($320 billion cost). The 2003 Medicare law has cost less than anticipated and played a lead role in the subsequent slowdown of Medicare cost growth. Still, it is contributing to Medicare’s long-term unsustainability.

- TARP ($220 billion cost). Most of the 2008 Troubled Asset Relief Program costs were later recovered during the Obama Administration.

- Economic Stimulus Act of 2008 ($181 billion cost). President Bush’s anti-recession bill relied chiefly on tax rebates for families. The economy did not respond.

Despite these costs, President Bush oversaw much lower budget deficits than Presidents Obama and Trump because he had inherited a budget surplus. During the Bush presidency, federal spending rose from 17.7% to 20.2% of GDP, while revenues fell from 20.0% to 17.1% (although this compares the earlier revenue bubble with a later deep recession). The national debt held by the public increased from $3.4 trillion to $5.8 trillion (or from 34% to 39% of GDP) through 2008. And like other recent presidents, President Bush (despite prioritizing Social Security reform) was not able to put entitlements on a sustainable long-term path.

President Obama’s Fiscal Record: A Look Back

In January 2009, President Obama inherited a projected $4.3 trillion budget deficit over the 2009–2019 period (a projection which incorporated the effects of the year-old deep recession.) Instead, he oversaw $8.9 trillion in 10-year deficits. This represents a fiscal decline of $4.6 trillion.[32] Much of this debt consisted of extending the policies inherited from President Bush.

Overall, the $4,610 billion fiscal decline under President Obama consisted of $6,273 billion in lower-than-projected revenues and $1,663 billion in lower-than-projected spending. Legislation cumulatively cost $4,988 billion, while economic and technical changes saved $378 billion:[33]

- Renewing the AMT Patch and Tax Extenders ($2,108 billion cost). President Obama inherited a number of tax policies that were set to expire. Renewing the small policies as well as keeping the Alternative Minimum Tax from significantly raising taxes on millions of households cost $2 trillion. Because this legislation merely continued current tax policies, some argue that their costs should have already been assumed in the CBO baseline.

- Renewing the 2001 and 2003 Tax Cuts ($2,028 billion cost). President Obama and GOP lawmakers eventually made the “Bush tax cuts” permanent for all except the highest- earning 2% of earners. Like the tax legislation above, one can argue that the CBO baseline should have been allowed to assume this continuation of existing tax policies.

- 2009 Stimulus Law ($1,010 billion cost). The February 2009 American Recovery and Reinvestment Act included $748 billion in new “stimulus” provisions plus $262 billion in net interest costs over the decade.

- Subsequent Stimulus and Recession Relief ($948 billion cost). Lawmakers followed up ARRA with multiple smaller stimulus laws over several years, including payroll tax holidays and unemployment insurance extensions.

- Discretionary Spending and OCO Reforms ($718 billion saved). The 2011 Budget Control Act and other discretionary savings provided the largest deficit reductions.

- Other Revenue Legislation ($282 billion saved). Dozens of smaller tax reforms.

- The Affordable Care Act ($275 billion saved). The “Obamacare” law balanced benefit extensions with Medicare savings and new taxes.

- Renewing Pre-2009 Health Laws ($154 billion cost). Dozens of small health policies regularly expire unless extended by Congress.

- BCA Mandatory Sequesters ($117 billion saved). The Budget Control Act also required modest automatic savings from some mandatory programs.

- Other Mandatory Spending Legislation ($69 billion cost). This consisted of countless small reforms.

- Hurricane Sandy Relief ($64 billion cost). A major hurricane hit the East Coast in 2012.

- Economic and Technical Changes ($378 billion saved). The sluggish economic recovery cost trillions in forgone tax revenues, yet this was balanced out by lower-than-expected interest rates saving $2.3 trillion over the decade.

Early in 2009, President Obama pledged to “cut the deficit we inherited by half by the end of my first term in office.”[34] He missed those targets and generally ran deficits well above the inherited CBO baseline. To be fair, much of the new legislation was simply extending existing policies that should have been part of the baseline. The weaker-than-expected economic recovery surprisingly did not directly worsen deficits, as lower tax revenues were offset by the net interest savings from lower interest rates. The Obama presidency, like those of Bush and Trump, represented a lost opportunity to avert escalating longterm baseline budget deficits driven by retiring baby boomers and the resulting Social Security and Medicare shortfalls. The national debt held by the public increased from $5.8 trillion to 14.2 trillion (or from 39% to 76% of GDP) through 2016.

Methodology

This analysis of President Trump’s fiscal record begins with the January 2017 Congressional Budget Office (CBO) budget baseline that the president inherited. This provides the 10-year (2017–2027) default projection of spending and revenues against which to measure his record. From there, CBO typically updated these baseline projections three times per year and classified all baseline movements into three causal groups: 1) legislative changes; 2) economic re-estimates that affected spending and revenues; and 3) technical re-estimates of revenues or spending, such as updated projection models (which are often secondary effects of economic changes). CBO further breaks down these three effects by the specific spending or tax category affected (such as the technical changes affecting Medicare). This report aggregates all of these baseline updates across the Trump presidency to provide a total breakdown of all changes to the 2017 through 2027 budget figures and projections.

Digging deeper into the legislative changes required building a database of all spending bills signed into law over these past four years—down to the line-item level of detail—and then classifying them into categories such as education or housing. This involved using CBO’s year-end reports detailing the mandatory and revenue legislation enacted during each Congress, and then using the original bill scores to fill in additional details. One complication is that the mandatory and revenue changes in CBO’s year-end report did not always match the sum totals included in the CBO baseline updates. Additionally, the CBO baseline updates understandably did not always match the actual year-end spending, revenue, and deficit figures. However, 98.3% of the costs are precisely accounted for in this report, and the remaining 1.7% is narrowed into its year and broad category (such as 2019 mandatory spending) and then estimated at the line-item level.

Net interest expenses are incorporated into the cost of individual bills and line-items. Two complications were that: 1) CBO’s baseline updates list only the total interest cost of all recently enacted legislation, rather than a specific breakdown by bill; and 2) these 10-year interest projections were highly dependent on whatever future interest rates CBO assumed at the time of enactment. I addressed both problems by redistributing each year’s total legislative net interest expense based on each tax and spending subcategory’s prorated contribution to the added legislative debt for that year. This method ensured that every bill (and line-item) could have an interest cost assigned to it and that each year would have its own uniform interest rate.

Finally, President Trump’s budget record is measured over a 10-year period (despite a fouryear presidency) because the original January 2017 CBO baseline covered 10 years, which allows us to analyze the effects of the president’s policies over this longer period. Still, the analysis ends with the February 2021 CBO baseline estimating the 2021–2027 budget picture, and any subsequent changes to the 2021–2027 budget will be credited to President Biden. Similarly, the fiscal records of Presidents Bush and Obama are also analyzed over 10-year periods, which incorporates their eight years in the Oval Office plus the updated CBO baseline for the next two years at the time they left office. Any changes that occur in those next two years are then credited to the next president who is in office at that time. Thus, all analyzed presidents are measured under the same 10-year methodology.

Appendix: Major Bills Enacted

About the Author

Brian Riedl is a senior fellow at the Manhattan Institute, focusing on budget, tax, and economic policy. Previously, he worked for six years as chief economist to Senator Rob Portman (R-OH) and as staff director of the Senate Finance Subcommittee on Fiscal Responsibility and Economic Growth. He also served as a director of budget and spending policy for Marco Rubio’s presidential campaign and was the lead architect of the ten-year deficit-reduction plan for Mitt Romney’s presidential campaign.

During 2001–11, Riedl served as the Heritage Foundation’s lead research fellow on federal budget and spending policy. In that position, he helped lay the groundwork for Congress to cap soaring federal spending, rein in farm subsidies, and ban pork-barrel earmarks. Riedl’s writing and research have been featured in, among others, the New York Times, Wall Street Journal, Washington Post, Los Angeles Times, and National Review; he is a frequent guest on NBC, CBS, PBS, CNN, FOX News, MSNBC, and C-SPAN.

Riedl holds a bachelor’s degree in economics and political science from the University of Wisconsin and a master’s degree in public affairs from Princeton University.

Endnotes

Photo: trekandshoot/iStock

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).