Powering Forward: Overcoming “Right of First Refusal” Obstacles in America’s Energy Grid

Photo: Anton Petrus / Moment via Getty Images

Executive Summary

The U.S. electrical grid faces unprecedented challenges that threaten its reliability, sustainability, and affordability. A significant portion of the U.S. population could face electricity reliability challenges in the coming years without swift and substantial investments in transmission infrastructure and grid modernization. Exacerbating these challenges are Right of First Refusal (ROFR) laws, which grant incumbent utilities the first right to construct and operate new transmission lines.

These laws, previously enacted by several states and recently reinstated at the federal level by the Federal Energy Regulatory Commission’s Order No. 1920, will entrench bottlenecks in essential transmission infrastructure development.[1]

To address these critical issues, we propose the following key policy recommendations:

- Remove both state and federal ROFR provisions to allow competitive bidding on interstate transmission projects, introducing market forces into the sector.

- Form macro-regional planning entities spanning multiple Regional Transmission Organizations / Independent System Operators to facilitate better interregional transmission planning and operation and create a national planning process for certain transmission lines.

Implementing these reforms requires collaboration among policymakers, utilities, and industry stakeholders. The Federal Energy Regulatory Commission (FERC), North American Electric Reliability Corporation (NERC), Regional Transmission Organizations (RTOs), and Independent System Operators (ISOs) all play crucial roles in ensuring grid stability, reliability, and efficiency.

Introduction

In early 2024, months ahead of the summer peak of high temperatures, the Electric Reliability Council of Texas (ERCOT) requested power generators to delay scheduled maintenance to mitigate potential tight conditions as temperatures climbed into the 80s.[2] This was unusual, as the grid typically has had surplus power-generating capacity in the spring, thanks to mild weather and ample solar and wind power, enabling plants to go offline for repairs before the summer surge in electricity use. Peak electricity demands went on to exceed previous records three times in April and five times in May.[3] The situation in Texas is just one example of the growing challenges that grid operators face in maintaining reliable power supply due to evolving demand patterns. Climate trends have contributed to increased electrical demand, with recent years consistently exceeding average historical summer temperatures.4 Additionally, technological advancements are reshaping electricity consumption. Data centers, which consumed about 2.5% of U.S. electricity in 2022, are projected to account for over 20% by 2030.5 The rise of artificial intelligence is expected to further amplify this demand, presenting new challenges for grid management and capacity planning.

The current economic repercussions of grid instability and power outages are already astounding. A report by the U.S. Department of Energy estimates that power outages cost the U.S. economy approximately $150 billion annually in lost productivity, damaged equipment, and diminished competitiveness. Investing in grid modernization and transmission infrastructure not only improves reliability but also lowers energy costs and enhances economic resilience.[6]

Exacerbating these challenges is the sluggish pace of grid updates, which can be partly attributed to the Right of First Refusal (ROFR) laws present in many states. These laws give incumbent utilities the first right to construct, own, and operate new transmission lines within their service territory, effectively suppressing competition from independent transmission developers who might propose more innovative and cost-effective solutions. ROFR laws have created a bottleneck in the development of essential transmission infrastructure, further heightening the risks to grid reliability and impeding the integration of renewable energy sources.

We highlight the fundamental tension in the management and development of the American energy grid: the balance between comprehensive planning and cost allocation; and the promotion of free-market competition. ROFR laws and regulations play a crucial role in this tension. While ROFRs can facilitate long-term planning and cost allocation by prioritizing incumbent utilities in new transmission projects, they also significantly restrict competition and potentially hinder innovation. As the Federal Energy Regulatory Commission (FERC) and other regulatory bodies lean more toward structured planning and cost allocation, particularly for large-scale projects, they inevitably constrain the degree of open competition possible in grid development and operation. The evolution of ROFR policies at both state and federal levels exemplifies this struggle to balance planning certainty with competitive market forces. This tension is not unique to the energy sector but reflects a broader challenge in economic regulation. We argue that addressing this tension, particularly through reform of ROFR laws, is crucial for modernizing the U.S. electrical grid.

History and Structure of the Electrical Grid

In the 1960s and 1970s, multiple major blackouts exposed vulnerabilities in the nation’s electricity infrastructure. Congress created FERC in response to these failures and tasked the agency with overseeing interstate electricity transmission (the high-voltage lines carrying electricity across long distances) and fostering fair competition in the wholesale electricity market. Over the next few decades, its emphasis shifted toward grid reliability and security. After a major blackout in the Northeast in 2003, the Energy Policy Act of 2005 marked a significant turning point by encouraging energy efficiency and investment in alternative energy sources. This act established the North American Electric Reliability Corporation (NERC) as the national Electric Reliability Organization (ERO) created to “establish and enforce reliability standards for the bulk-power system.”[7] Prior to 2005, NERC existed as an industry-driven organization with a focus on reliability standards but lacked formal enforcement power. The act formalized NERC’s role and empowered it to develop and enforce mandatory reliability standards for the bulk power system across North America. Under the new framework, FERC retained its authority to review and approve these standards, ensuring that they aligned with national energy policy goals. This established the current system where FERC sets the overall rules and NERC translates them into practical, enforceable standards, which FERC then approves.

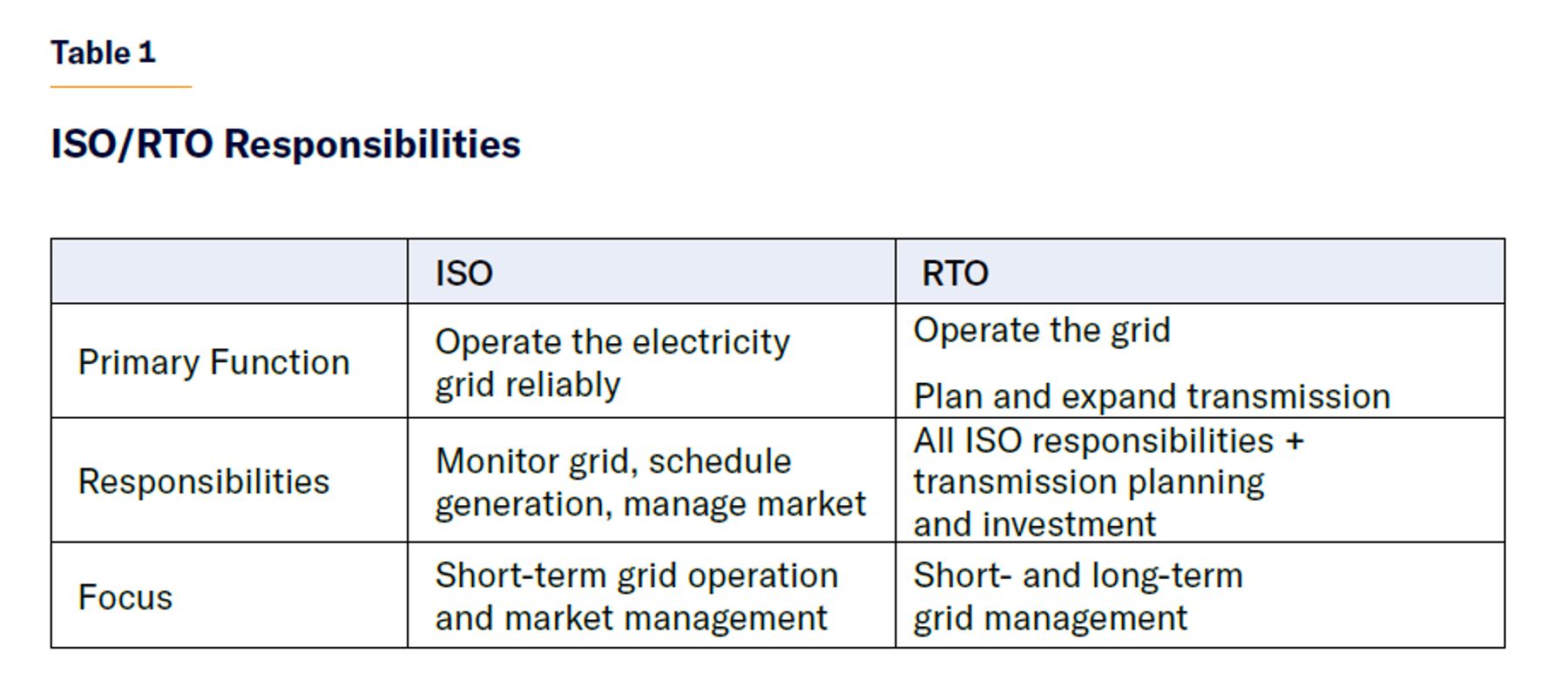

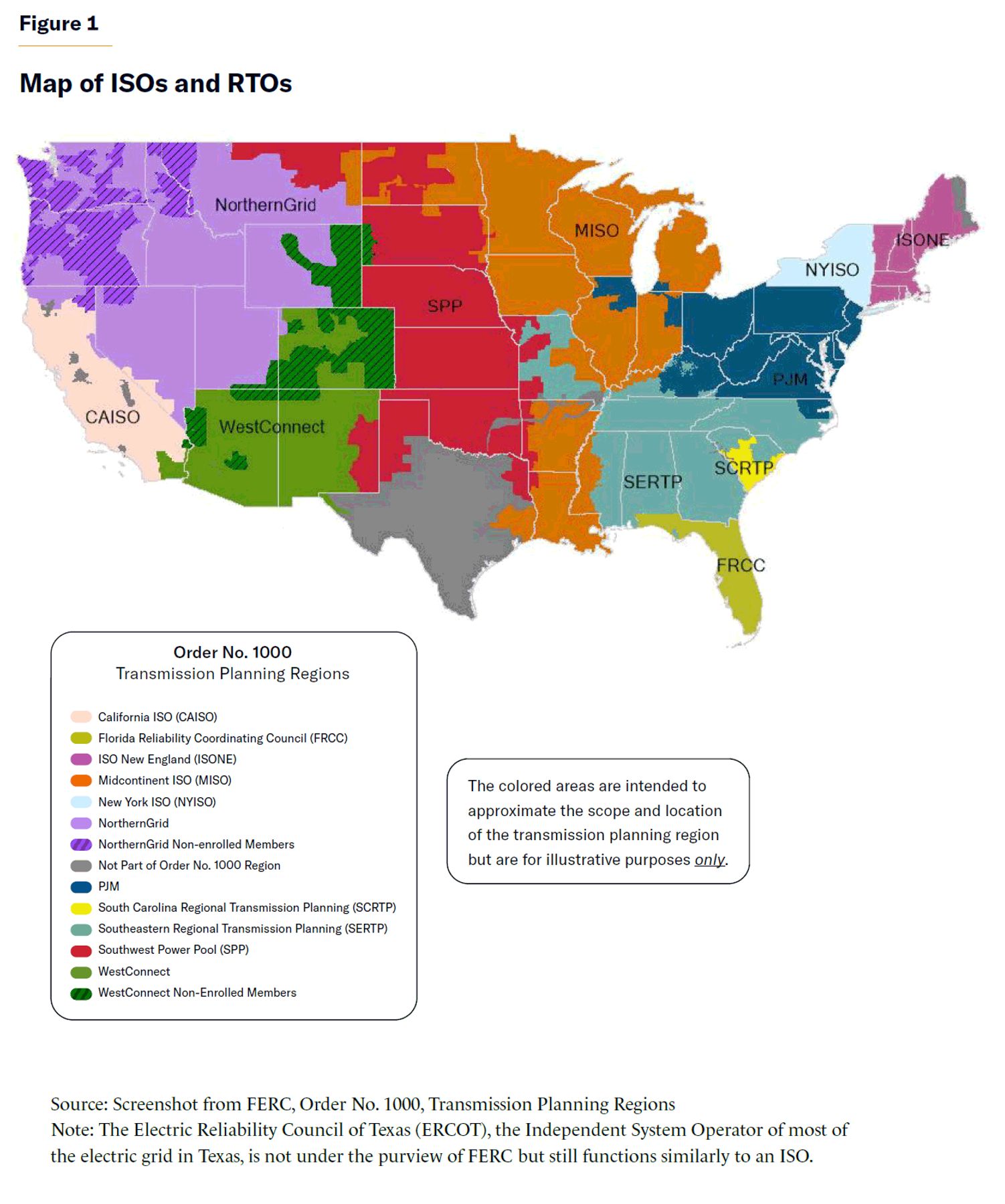

The management of electricity production and transmission is primarily the responsibility of Regional Transmission Organizations (RTOs) and Independent System Operators (ISOs). These organizations play crucial roles in operating the North American bulk power system and managing electricity markets. However, there are key distinctions between ISOs and RTOs (Table 1).

Figure 1 displays RTO and ISO within the contiguous United States.[8]

An ISO is an independent, nonprofit organization responsible for ensuring the reliable operation of the electricity grid within its designated region. ISOs act as the neutral traffic cop for the grid, overseeing the flow of electricity across high-voltage transmission lines. ISOs monitor real-time electricity supply and demand in their region to maintain grid stability and prevent blackouts. Additionally, they schedule power plants to ensure that enough electricity is generated to meet demand while considering factors like cost and efficiency. ISOs operate wholesale electricity markets where generators sell electricity and utilities buy it to meet consumer demand. They ensure fair competition and market transparency.

An RTO performs all the functions of an ISO plus additional responsibilities related to transmission planning and expansion. RTOs operate more as a comprehensive traffic-management system for the grid, not just managing traffic flow but also planning for future needs. RTOs conduct long-term studies to assess future electricity needs and develop plans for expanding the transmission system to accommodate projected growth and integrate new resources like renewable energy. They coordinate the planning and investment in new transmission lines among various stakeholders in the region.

While connections between RTOs and ISOs exist as part of the national electrical grid (except Texas’s ERCOT, which remains outside the rest of the system), each operates independently within its geographic area. As a result, reliability and capacity issues are primarily addressed on a regional basis.

Problems with the Existing Grid

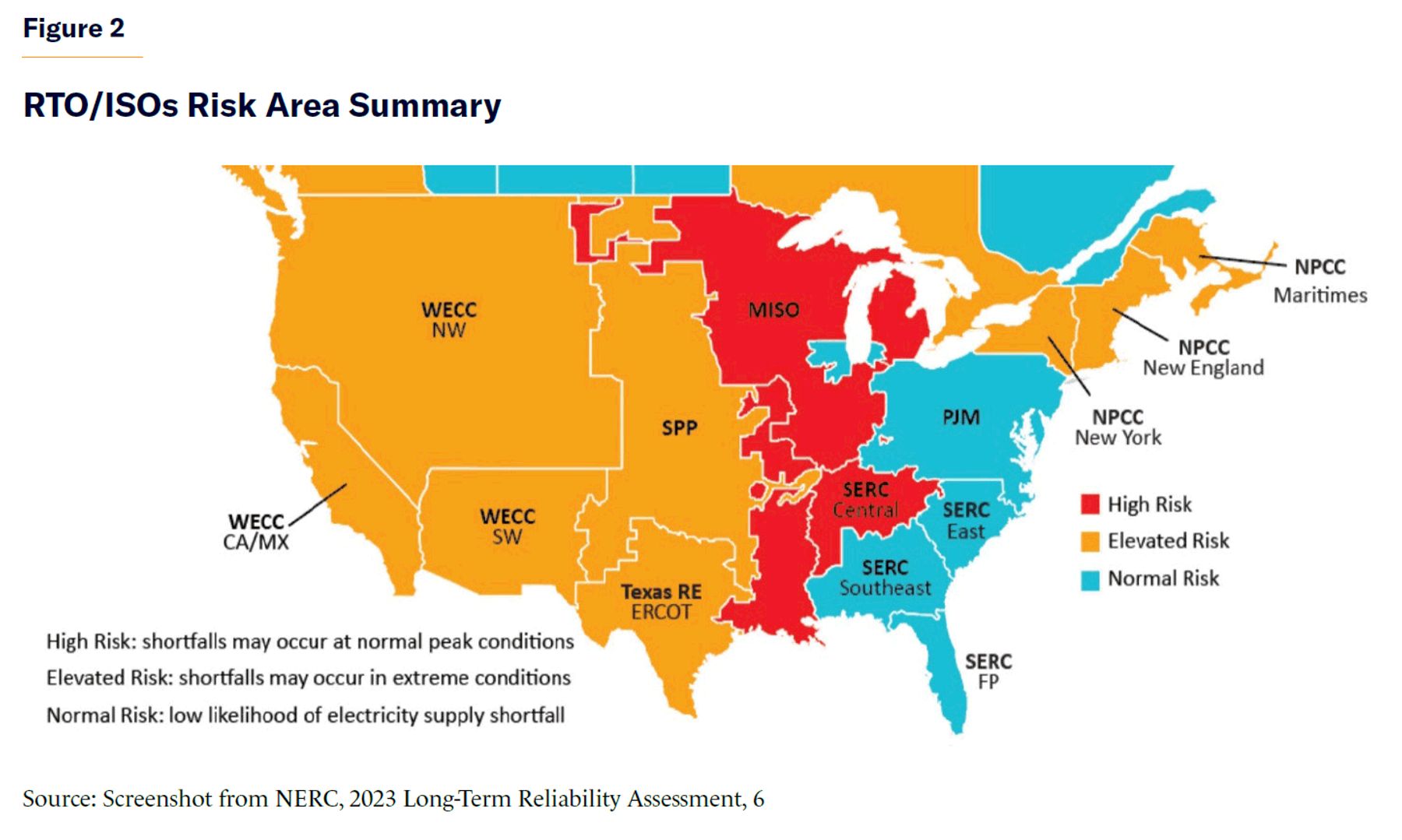

In December 2023, NERC released its Long-Term Reliability Assessment (LTRA).[9] Figure 2 displays risk levels for geographic areas within NERC.LTRA classifies RTOs and ISOs as “high risk” when they fail to meet established resource-adequacy targets or requirements. While NERC does not set these resource-reserve requirements, they are generally based on a “1-day/event load-loss in a 10-year planning” period standard.[10] This indicates that although these regions typically have sufficient capacity under normal conditions, they may lack adequate resources during extreme events or unexpected spikes in demand.

Based on NERC’s current LTRA, only four of the 18 RTO/ISOs have “normal risk.” Most of the remaining 14 operate at “elevated risk,” but the two remaining organizations (MISO and Southeastern Electric Reliability Council [SERC], which cover much of the Midwest and Southeast U.S.) face “high risk.” High-risk areas may face challenges in maintaining electric service reliability, especially under extreme conditions. For example, the Midcontinent Independent System Operator (MISO) is projected to experience a 4.7-gigawatt shortfall by 2027, while SERC-Central is anticipated to have a shortfall between 2025 and 2027 due to the retirement of utility assets before the planned addition of new sources.[11] These areas often meet the expected resource requirements but struggle to satisfy the demands of “probabilistic or deterministic scenarios.”[12] Among other recommendations, the LTRA says that ISOs and RTOs must expand transmission capacity to meet new sources.

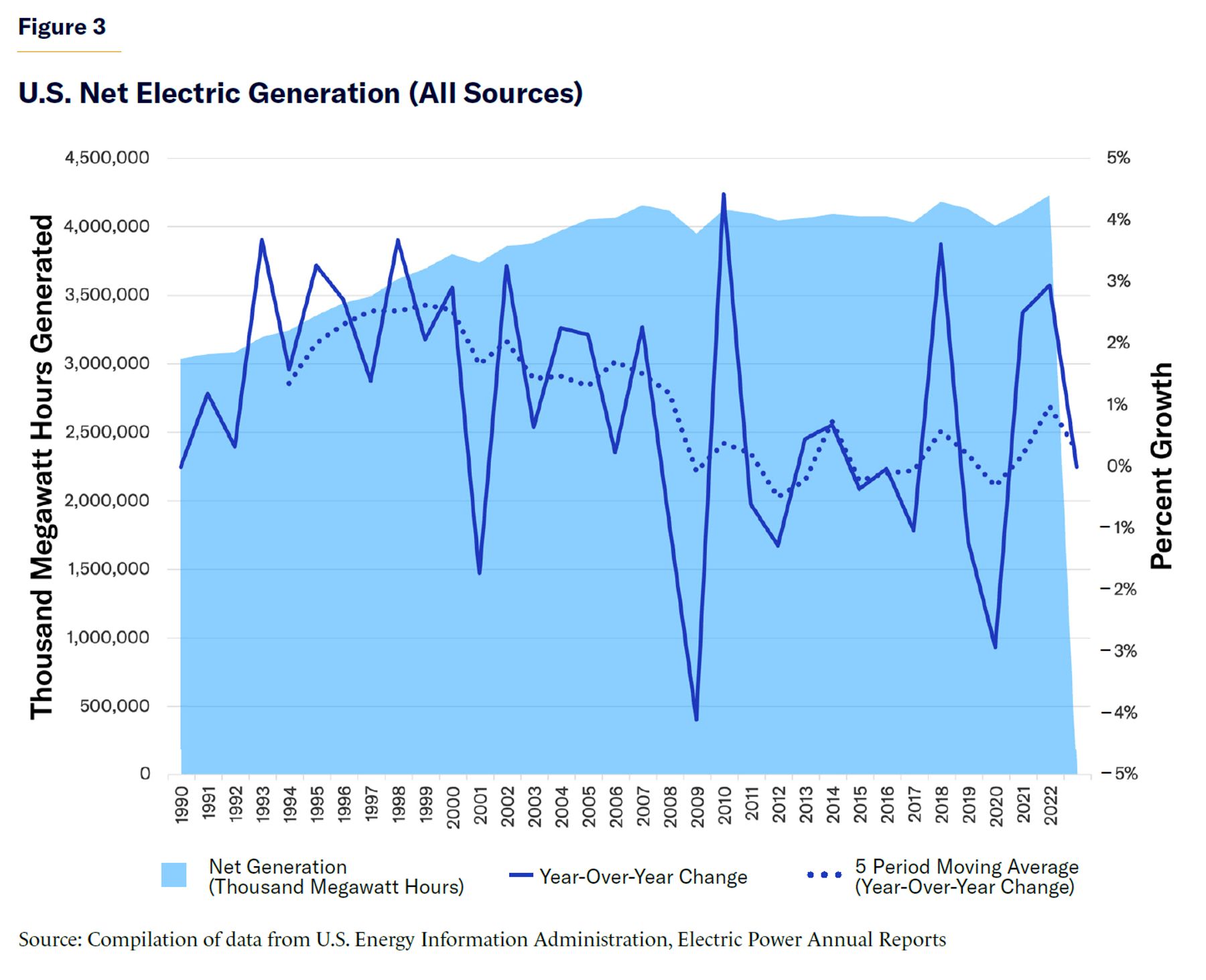

FERC’s mission is to help consumers get reliable, efficient, and sustainable energy services at a reasonable cost. Interstate transmission is vital for expanding and integrating new energy sources, especially as the supply of renewables increases the diversity of energy resources. Therefore, having FERC oversee interstate transmission effectively is vital for balancing supply and demand and ensuring grid reliability. The U.S. Energy Information Administration reports that annual U.S. electrical generation stands at just over 4 trillion kWh, with demand expected to grow by 1% a year.[13] While this projected growth rate may appear modest, U.S. electrical generation has averaged annual growth of only 0.5% over the last 20 years (Figure 3). The disparity between electrical demand and supply in the U.S. may create rationing problems that threaten 300 million people, or nearly 90% of the current U.S. population, with electrical shortages.[14] Currently, residential electrical consumption accounts for the largest share (38.4%) of U.S. retail electricity, with “space” heating and cooling making up nearly one-third of residential use.[15] Consequently, extreme weather events, as well as increased demand due to data centers and artificial intelligence, will likely put substantial strain on the grid, heightening reliability concerns.

Despite the potential benefits that new clean power capacity offers, efforts to integrate these sources into the existing transmission grid are encountering significant hurdles. Lengthy wait times and high costs for grid connection have hindered progress. Over the past decade, the construction of new high-voltage transmission lines has declined, exacerbating the bottleneck. Reforming transmission planning and interconnection processes is essential to overcoming these challenges. Currently, over 930 gigawatts (GW) of clean energy capacity (solar, wind, hydropower, geothermal, and nuclear) and 420 GW of energy storage are in interconnection queues seeking transmission access. This capacity is nearly sufficient to achieve an 80% clean electricity share by 2030.[16]

Grid operators require new projects to undergo a series of impact studies to ensure grid stability and safety. This process determines necessary transmission upgrades and their associated costs, but the extensive nature of the process often leads to delays and financial uncertainty. Less than 25% of projects that sought connection to the grid from 2000 to 2016 have been completed. Recent years have seen even lower completion rates for new wind and solar projects, compared with natural gas projects. Many of these proposed sources are waiting for connections, and the time between these connection requests and operation has nearly doubled, increasing by over 1.5 years (to 3.7 years), relative to the previous decade, resulting in many proposed sources never being built.[17] Despite recent significant investments, the construction of new high-voltage transmission lines has declined, from an annual average of 2,000 miles (2012–16) to 700 miles (2017–21).[18]

FERC plays a vital role in setting and reviewing the rules for interconnection, transmission planning, and cost allocation. Its ongoing rulemaking efforts are crucial for addressing the challenges in the current system. Active participation by regional planning organizations, grid operators, utilities, states, nongovernmental organizations, and the private sector is essential in implementing these rules and advancing transmission infrastructure. Government bodies at all levels will influence the structure and pace of the permitting process, while community engagement is critical for successful implementation.

Right of First Refusal (ROFR) Laws

The process of connecting new electricity generation and storage projects to the power grid involves joining interconnection queues, which are essentially waiting lists. These queues have become increasingly lengthy due to the current infrastructure’s limitations, as it was originally designed for centralized fossil fuel plants and struggles to accommodate the geographically dispersed nature of renewable energy. The prolonged wait times in these interconnection queues pose several challenges, including delayed clean energy adoption, increased uncertainty for developers, higher project costs, and potential risks to future grid reliability.

Until the 1990s, the Public Utility Holding Company Act of 1935 (PUHCA) reinforced a system of geographic monopolies for utilities. This meant that a single company held exclusive rights to provide electricity within a designated region. In essence, one company was responsible for producing, transmitting, and distributing electricity within its assigned territory. PUHCA also restricted the investments in and structures of utility holding companies. In 1996, FERC issued Order No. 888,[19] which mandated open-access transmission service, requiring electricity transmission providers to allow third-party generators to access their lines. This rule, along with other mid-1990s regulations, aimed to promote competition and reduce electricity prices. These reforms significantly reshaped the U.S. electricity industry, leading to a more deregulated market.

The Energy Policy Act of 2005 focused on increasing energy efficiency and investment but also repealed PUHCA and expanded FERC’s oversight in the electrical industry.[20] In 2007, exercising its new authority, FERC issued Order No. 890. This order required transmission providers to implement open, transparent, and coordinated transmission planning processes.[21] While it was intended to promote competition and fairness, Order 890 inadvertently set the stage for practices that often favored incumbent utilities.

The formalized transmission planning processes established under Order 890 frequently resulted in de facto (federal) ROFRs for incumbent utilities. A federal ROFR in the context of electrical transmission refers to provisions in FERC-jurisdictional tariffs and agreements that grant incumbent utilities the first opportunity to construct new transmission projects identified in regional transmission plans. Unlike state ROFRs, which are enacted through state legislation, a federal ROFR is implemented through FERC regulations and applies to projects under federal jurisdiction, typically those involving interstate commerce or wholesale electricity markets.

Under Order 890, transmission providers were required to identify needed transmission projects. Due to the planning required for such a task, this requirement created an incumbent advantage. Since existing utilities were also often transmission providers, the utilities were given the first opportunity to build new transmission projects within their service territories. This outcome essentially granted utilities significant control over the development of the transmission grid. It ensured that they had a strong incentive to invest in and maintain the infrastructure within their domain but also potentially limited opportunities for new entrants and alternative developers in the transmission sector.

A shift toward increased competition emerged in 2011 with FERC’s landmark Order No. 1000,[22] which attempted to increase competition across electrical sources and transmission. These changes (1) required regional transmission planning, (2) required public utility transmission providers to prepare an open-access transmission tariff to address local and regional planning processes, (3) removed de facto federal ROFRs for certain transmissions due to a change in incumbent planning requirements, and (4) improved coordination between neighboring transmission regions.[23]

States’ Regulatory Responses

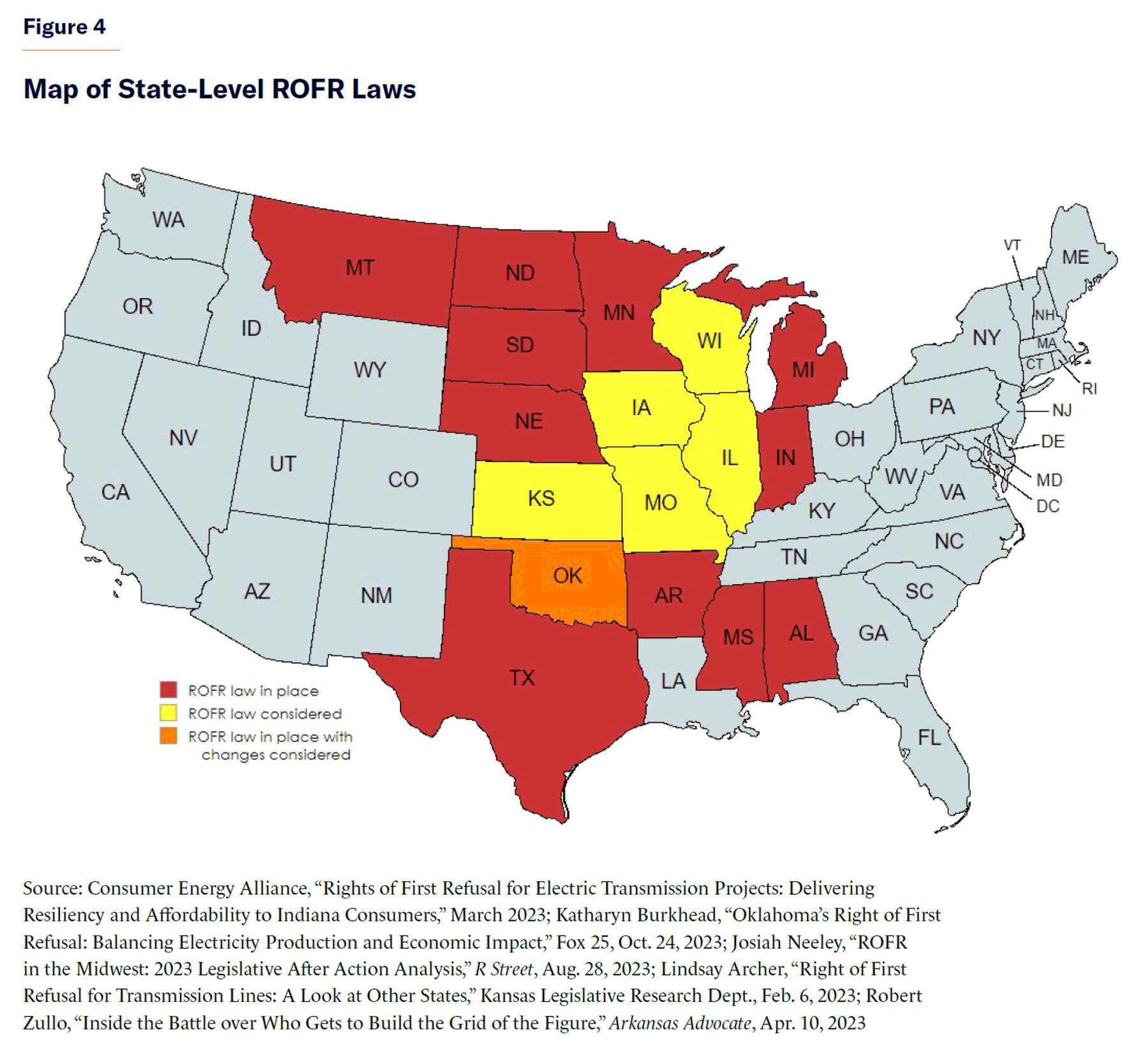

Since FERC’s Order 1000 removed federal ROFRs in 2011, several states have passed their own ROFR laws, especially in the Midwest and Great Plains regions. As shown in Figure 4, most of the states in MISO have enacted ROFRs, including Indiana, Michigan, Minnesota, Mississippi, North Dakota, South Dakota, and Texas. Similarly, Nebraska, Iowa,[24] Oklahoma (below 300 kilovolts), and the Southwest Power Pool RTO have all enacted ROFR.[25] Proposals to introduce new state-level ROFR rights or expand existing ones have been advanced in Missouri, Montana, Wisconsin, Kansas, and Illinois. With the exception of Kansas, the central portion of the U.S. has established a network of ROFR regulations, effectively dividing the country into eastern and western regions. These regulations have made the development of long-distance high-voltage transmission lines harder and more expensive to develop, making intercontinental connection tougher.[26]

Defenders of state ROFR laws have cited a desire to limit federal oversight or a lack of necessary state oversight of transmission lines as justifications.[27] State ROFR laws give state or electrical commissions more authority over the development of transmission lines. While construction and reliability of transmission lines remain under FERC and NERC purview, state ROFR laws can limit competition, especially from out-of-state companies. These laws significantly affect the development of multistate transmission lines by increasing the costs associated with such projects.

As more states adopt ROFR laws, the complexity and cost of developing interstate transmission infrastructure continue to increase. It is increasingly difficult to implement large-scale, multistate transmission projects, which are crucial for enhancing grid reliability and facilitating the integration of renewable energy sources. In addition, reduced competition among the states with—or considering—ROFR laws will only exacerbate problems identified by NERC’s current LTRA showing forthcoming energy shortages.

There has been pushback against these laws. When Iowa’s ROFR was examined by the state supreme court in 2023, the justices unanimously concluded:

We are not surprised the ROFR lacked enough votes to pass without logrolling. The provision is quintessentially crony capitalism. This rent-seeking, protectionist legislation is anticompetitive. Common sense tells us that competitive bidding will lower the cost of upgrading Iowa’s electric grid and that eliminating competition will enable the incumbent to command higher prices for both construction and maintenance. Ultimately, the ROFR will impose higher costs on Iowans. The data back this up: amicus Coalition of MISO Transmission Customers offers data collected from two recent bid-based projects that indicate competition reduces costs by fifteen percent, compared to MISO’s estimates.[28]

The Iowa Supreme Court remanded the case, challenging Iowa’s ROFR laws back to a district court. The district court ruled the ROFR law unconstitutional.[29] Less than two months later, a new version of a ROFR bill was advanced out of a House subcommittee.[30]

Studies on electrical transmission indicate that transmission upgrades cost 20%–30% less if ROFR laws are eliminated and replaced with a competitive bidding process.[31] Soliciting bids has also resulted in additional innovation through the proposed engineering solutions. One analysis of competitive bidding on projects showed “the winning bids of these 15 competitive transmission projects have been priced 40% below the ISO/RTOs’ or incumbent TO’s initial project cost estimates.”[32] The delays have resulted in higher transmission costs, and although the number of requests for projects (usually requested by utilities) has increased, the number of operational projects has declined since 2013.[33] In some regions, the cost of electrical transmission has more than doubled over the past decade.[34] For consumers in the PJM Interconnection, the cost of electrical transmission now exceeds the cost of generation capacity. While regulatory hurdles likely increase delays, the lack of competition and firm deadlines stemming from ROFRs further exacerbate these problems.

As the Supreme Court of Iowa example shows, the legality of state ROFR laws has also come into question.[35] ROFR laws give preferential treatment to incumbents, thereby discriminating against other firms. For interstate transmission lines, this potentially violates the Dormant Commerce Clause,[36] which is based on two important ideas. First, state regulations may not discriminate against interstate commerce; and second, states may not impose undue burdens on interstate commerce.[37] ROFRs may violate the Dormant Commerce Clause by empowering firms with a local presence (incumbents) and preventing out-of-state companies from entering.

Federal Regulatory Response

In April 2022, FERC proposed rules (RM21-17-000)[38] to improve electrical transmission and limit state ROFRs.[39] Their Notice of Proposed Rulemaking (NOPR) stated that, traditionally, transmission planning processes that focus on electrical generation have been produced by large facilities. However, contemporary electrical generation has evolved to include a mix of electrical sources and sizes. As a result, the processes have led to a growing backlog of interconnection requests and study delays for many transmission providers. Backlog-related interconnection requests from solar, storage, and wind projects were already on the rise, but the passage of the Inflation Reduction Act in August 2022 exacerbated this backlog because it incentivized renewables projects. As of the end of 2023, almost half the active capacity in the interconnection queues had entered the queues after the passage of the IRA in August 2022.[40]

FERC’s proposed rules aim at improving the approaches that led to electrical insecurity and prevented the connection of other electrical generation sources. As recommended by NERC, this includes longer-term planning/forecasting, improved transmission approvals and cost allocation, and greater stakeholder involvement.

The NOPR makes several changes to regional transmission planning. Besides extending the mandated planning horizon to 20 years, RTOs need to examine multiple scenarios to anticipate a future with a variety of electrical sources as well as varying demand. These changes are needed to better prepare for an uncertain future due to new technology, retirement of older utilities, extreme weather, and, one hopes, greater interconnection. The current web of state regulations also makes planning more challenging; therefore, the NOPR incorporates the approval of state entities for cost allocation in long-term planning. The RTO must also provide transparent criteria for transmission planning to avoid “unduly discriminatory criteria to select transmission facilities.”[41]

Several of these proposed changes are clearly aimed at reducing monopoly power currently occurring with both generation and transmission. Despite these efforts, the NOPR also amends the federal ROFR rule from Order 1000, effectively reinstating ROFRs for transmission. This new approach proposed giving incumbent utilities ROFR if they establish joint ownership of the lines with other companies and meet certain conditions, such as using “right-size” facilities based on long-term regional transmission planning. This shift reflects FERC’s attempt to balance competing priorities: promoting competition, ensuring efficient planning and development, encouraging cooperation, and maintaining regulatory oversight. By conditioning ROFR on joint ownership and alignment with regional planning goals, FERC aimed to harness the benefits of competition while still facilitating coordinated, efficient transmission development. Notably, this approach does not directly delegate ROFR authority to states or RTOs but rather creates a federal framework that influences industry behavior while maintaining FERC’s oversight on interstate transmission projects.

As discussed in the NOPR, these proposals are designed to improve planning and cost allocation, which is certainly needed. According to FERC:

Taken together, these proposed reforms would work together to remedy deficiencies in the Commission’s existing regional transmission planning and cost allocation requirements. This, in turn, would fulfill our statutory obligation to ensure that Commission-jurisdictional rates remain just and reasonable and not unduly discriminatory or preferential.[42]

While transparency in planning and costs would be an improvement, the NOPR did not directly address the ability of new sources to connect to regional transmission, or to enable competition in the regional transmission. Instead, the proposed rules significantly expand regional transmission planning but do so by expanding the role of incumbent providers in future planning and expansion. In addition, existing transmission providers can determine “opportunities” to replace existing transmission to meet capacity needs, which was referred to as “right-size” replacement.

New Federal Regulations May Impede Competition

In May 2024, FERC issued Order No. 1920,[43] adopting many of the provisions outlined in its 2022 NOPR. As expected, Order 1920 introduced several significant reforms. This new rule built on previous efforts (such as Orders 888 and 890 and the above-mentioned 1000) to address deficiencies in existing regulations to ensure that transmission rates are just and reasonable, and not unduly discriminatory or preferential against certain generators or customers. Like Order 1000, Order 1920 mandates that transmission providers engage in comprehensive and forward-looking regional transmission planning to identify and address long-term transmission needs. These provisions include:

- The inclusion of alternative transmission technologies, requiring transmission providers to incorporate a regional cost-allocation method for long-term regional transmission facilities into their tariffs, ensuring that the costs of new transmission projects are distributed fairly among stakeholders.

- “State Agreement Processes,” enabling relevant state entities to voluntarily agree on cost-allocation methods for specific projects, promoting cooperation and equitable cost distribution.

- Identification of interconnection-related transmission needs, requiring transmission providers to evaluate regional transmission facilities. This requirement aims to streamline the integration of new generation sources into the grid, ensuring that interconnection issues do not hinder the development of new energy projects.

- Enhanced transparency in local transmission planning processes, ensuring that all stakeholders have access to the information they need to make informed decisions, increasing transparency and coordination.

These reforms aim to ensure that future demands and potential scenarios are considered in transmission planning, potentially leading to more robust and resilient grid infrastructure. However, they also potentially impede competition by reinforcing the position of incumbent transmission providers. Under these reforms, incumbents are granted the first opportunity to plan, build, and own transmission expansions and replacements within their service territories.

FERC Order 1920 adopted the federal ROFR provisions from the previous NOPR.[44] One potential benefit of ROFR is that it incentivizes incumbent transmission providers to offer more accurate and competitive estimates for in-kind replacements of transmission facilities. By guaranteeing incumbents the right to build the facilities that they estimate, the ROFR encourages them to carefully consider right-sizing opportunities (i.e., downsizing the facility where necessary) and to identify needed expansion. This means that incumbents may be more likely to propose solutions that are appropriately scaled to meet the specific needs of the project, rather than overbuilding or underbuilding. In theory, this could lead to more efficient and cost-effective transmission solutions, as the facilities would be optimally sized to balance costs and benefits.

However, as transmission costs increase, incumbent firms obtain greater revenue, which disincentivizes grid expansion. ROFRs provide stability for incumbents but reduce the competitive pressures that could drive down costs. Without the threat of competition, incumbents may not feel compelled to minimize expenses, potentially leading to higher costs for transmission projects. This lack of competition can result in complacency, where incumbents might not pursue cost-saving innovations or efficiency improvements. Over time, the absence of competitive bidding will lead to higher prices for consumers and less incentive for incumbents to adopt new technologies or best practices that could enhance grid performance and reduce costs. Therefore, any potential efficiency gains seem to be more than offset by the reduced competition and potential for higher overall costs associated with the ROFR.

For states that already have ROFR laws in place, the reintroduction of a federal ROFR by FERC Order 1920 adds a new layer of complexity to the existing regulatory framework for transmission planning and development. Meanwhile, states considering a ROFR provision may no longer see a need to enact their own version. States with existing ROFR laws will need to align their regulations with the new federal requirements to prevent overlapping bureaucratic hurdles. This alignment process may involve reviewing and amending state laws to ensure that they are consistent with federal provisions. The costs associated with this regulatory harmonization can include legal and administrative expenses, as state regulatory agencies work to interpret and integrate the new federal guidelines into their existing frameworks. For states with well-established ROFR laws, these alignment efforts may be less burdensome if their regulations already closely mirror the federal rules. However, states with unique or more divergent ROFR provisions may face higher costs as they undertake more substantial revisions and compliance efforts.

Policy Recommendations

ROFR laws, which primarily apply to local transmission projects within a utility’s service territory, can hinder the development of interstate transmission infrastructure. Interstate transmission projects require navigating transmission by incumbent firms across different states, further complicating and delaying development. This fragmented regulatory landscape can significantly impede the progress of clean energy integration efforts.

To address the regulatory and permitting complexities that hinder the development of crucial infrastructure projects, we recommend the following:

Remove ROFR Provisions: Removing FERC’s federal ROFR provision would enable competitive bidding on interstate transmission projects. Introducing market forces will drive down costs. Additionally, the federal government could pass legislation that preempts state ROFR laws for certain critical transmission projects, particularly those related to interstate energy integration. Absent the passage of federal legislation, another approach could be to utilize the commerce clause to challenge state ROFRs in court. Even if this approach is not utilized, FERC should encourage alignment and incentive changes in state ROFR laws that impede the timely addition of critical new grid capacity.

Ultimately, establishing a uniform regulatory framework at the federal level will streamline and expedite the development of essential interstate transmission lines.

Create More Regional Transmission Planning: Develop a standardized, national approach to transmission planning that prioritizes interregional projects. This should include revisiting and strengthening FERC’s Order 1000 to enhance interregional planning and cost-allocation requirements. RTOs and ISOs should explore regional cooperation frameworks, including the formation of macro-regional planning entities spanning multiple RTOs/ISOs, to facilitate the development of interstate transmission lines and potentially harmonize approval rules across jurisdictions. FERC should promote a more transparent approach to transmission planning and development.

Our recommendations require a more standardized regulatory structure. At the local level, states can foster joint ownership and cost-sharing agreements among utilities and transmission providers in adjoining states, ensuring equitable distribution of benefits and responsibilities while aligning local needs with broader regulatory requirements. Regionally, the formation or enhancement of multistate transmission planning groups, including representatives from ISOs/RTOs and other stakeholders, can facilitate coordinated planning for cross-state projects. Interstate Compacts, akin to “customs unions,” offer another model for establishing common policies and procedures, which would remove incumbent-firm control over planning and expansion.

At the federal level, FERC must assume a pivotal role in developing a comprehensive national plan for transmission integration and reinforcement. FERC should abolish all ROFRs, expand regional ISO/RTO planning requirements, and ensure a competitive process for upgrading and expansion projects. This is crucial for optimizing efficiency, reducing costs, and facilitating more effective regional and state planning efforts.

Conclusion

The U.S. electrical grid is at a critical juncture, facing unprecedented challenges and opportunities. Severe weather events, the rapid growth of renewable energy sources, and the rising demand for electricity driven by factors such as data centers and artificial intelligence have exposed vulnerabilities in the existing grid infrastructure. To ensure a reliable, resilient, and efficient electrical system, we must make significant investments in grid modernization and transmission infrastructure.

The Inflation Reduction Act of 2022 contains substantial financial incentives to accelerate the development and deployment of clean energy technologies. Transforming the U.S. energy grid requires a delicate balance between comprehensive planning and market competition, a balance that has been significantly undermined by both state and federal ROFR laws and regulations. The tension between these two approaches is at the heart of many regulatory challenges facing the sector. These laws hinder competition, increase costs, and delay the construction of essential transmission lines, particularly those most needed: the ones crossing state boundaries.

Furthermore, the evolving relationship between FERC and NERC and the critical roles played by RTOs and ISOs highlight the necessity for a coordinated and cohesive approach to grid modernization and reliability. Such an approach should prioritize competition and innovation to implement the most efficient and cost-effective solutions.

By fostering greater competition, streamlining processes, and promoting regional cooperation, policymakers and stakeholders can create a more conducive environment for developing a robust and efficient transmission grid. This, in turn, will enable the seamless integration of clean energy resources, unlocking their full potential and accelerating the transition toward a sustainable and secure energy future. As the U.S. navigates this transformative period in its energy history, policymakers must recognize that the path forward requires not only financial investments but also regulatory reforms, technological innovation, and collaboration among all stakeholders.

About the Authors

Jason M. Walter is an associate professor of economics and energy fellow at the Center for Energy Studies at the University of Tulsa. His research focuses on industrial organization, environmental economics, and regulation.

Meagan McCollum is an associate professor of finance at the University of Tulsa and director of the University of Tulsa Center for Real Estate Studies. She is also a fellow at the University of Tulsa Center for Energy Studies. Her research focuses on real estate finance, public policy, and energy issues.

Eric Olson is the Mervin Bovaird Foundation Endowed Professorship in Business and an associate professor of finance in the Collins College of Business at the University of Tulsa. His research focuses on energy policy, monetary policy, and open-economy macroeconomics.

Endnotes

Photo: Anton Petrus / Moment via Getty Images

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).