Medicare for All? Lessons from Abroad for Comprehensive Health-Care Reform

Photo: monkeybusinessimages / iStock / Getty Images Plus

The “Medicare for All” proposals espoused by various Democratic presidential candidates vary greatly in terms of benefits, provider payment arrangements, and the role of private insurance. In some versions, the government is the sole purchaser of medical services; in others, a publicly financed system would allow individuals to choose between a government plan and competing private insurers; in still others, a publicly managed option would be added to the wide variety of insurance and entitlement programs that already exist. There has also been a lively disagreement about whether individuals should be allowed to purchase private insurance to obtain better care than is available under a publicly financed plan.

In their variety, the various Medicare for All proposals reflect the diversity of arrangements by which medical care is financed in the Western world. In order to better evaluate U.S. Medicare for All proposals, this paper examines the varied roles that eight developed countries (including the U.S.) have afforded to private resources and insurance competition within their health-care systems.

There are four broad models:

- Single payer (Canada and U.K.): the government is the predominant purchaser of medical services.

- Dual payer (Australia and France): the government is the primary purchaser of medical services, with widespread private supplemental health insurance.

- Competing payer (Germany, the Netherlands, and Switzerland): the government publicly subsidizes individually purchased health insurance.

- Segmented payer (U.S.): a patchwork of employer-sponsored insurance, public entitlements, and individually purchased health insurance.

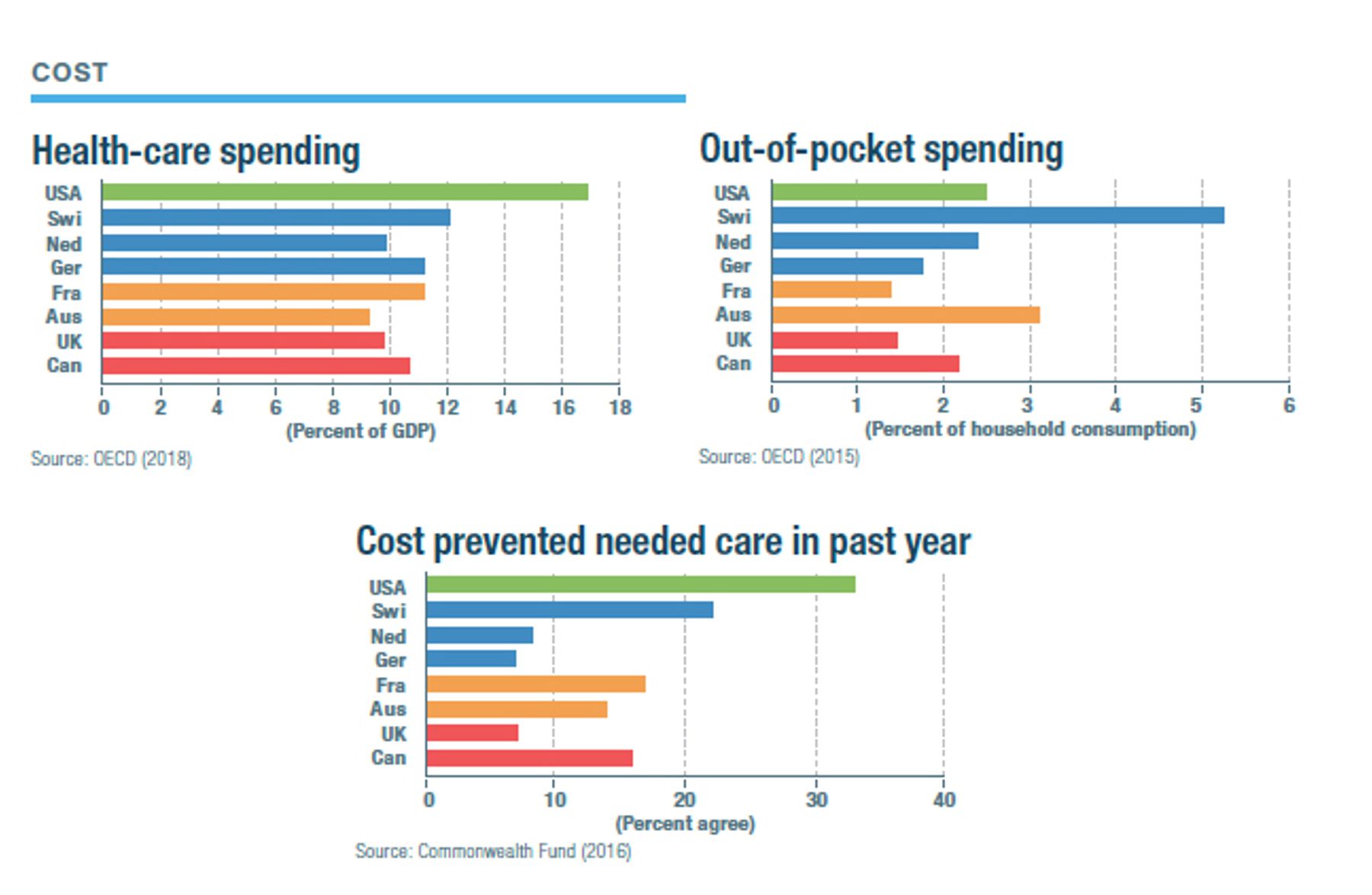

This report concludes that, across these eight countries, the ability of citizens to obtain expensive medical procedures tends to increase in proportion to their ability to purchase insurance for medical care beyond what public entitlements cover. Single-payer systems, which restrict the ability of individuals to purchase private insurance, deliver consistently worse access to specialty care or surgical procedures—without reducing individuals’ overall out-of-pocket health-care costs. Relative to countries that restrict private insurance, the U.S. provides good access to high-quality care, but individuals who fall in the gaps between employer-sponsored insurance and public entitlements are at risk of high costs. Systems that seamlessly integrate competitive private insurance with well-targeted public subsidies prove best able to make use of private resources with minimal gaps in coverage.

The Interaction of Health-Care Entitlements and Private Insurance

As Democratic presidential hopefuls debate “Medicare for All” proposals, the key division among them involves private insurance. Should it compete alongside a public option? Should it be allowed to pay for access to medical care over and above the public plan? Should it be prohibited altogether?[1]

Health care everywhere in the Western world is paid for by a mix of public and private funds, with governments in North America and Western Europe spending 6%–10% of GDP on medical entitlements (the U.S. spends 8.5%). On top of this, private health-care spending in these countries varies from 1% to 9% of GDP (the U.S. spends 8.8%).[2]

In the mid-20th century, given the limits of medical technology, governments in the developed world could realistically purchase all effective medical care for all citizens within reasonable fiscal constraints. Today, in the world of heart transplants, knee replacements, and new immunotherapies becoming available every year, this is no longer the case. That is a consequence of medical progress and is fundamentally a good thing—but as citizens live longer into old age and disease, and more can be done for them when they need treatment, it does mean that every country faces difficult trade-offs and limits in allocating scarce public funds. There are economic, cultural, and political limits to how much the government can raise in taxes—and public funds that are spent on health care reduce the amount that is available to defense, infrastructure, education, and the relief of poverty.

Private health insurance tends to be defined by the shape and limits of public spending. Where the coverage under public entitlements falls short, private insurance will tend to grow to fill the gap. This is true for benefits excluded in public entitlements (prescription drugs in Canada), cost-sharing (coinsurance in France), waiting times (elective surgery in the U.K.), and eligibility restrictions (able-bodied working-age adults in the U.S.).

The debate over the value of private insurance is partly a question of efficiency.[3] But it is, above all, a question of whether private access to medical care beyond that funded by public entitlements is to remain a viable and meaningful option—for those other than the very few who are able to spend tens or hundreds of thousands of dollars out-of-pocket for care.

Some argue that private demand risks taking physicians away from public entitlements or driving up the costs of employing them, thus diverting care from those who most need it to those who can most afford to pay for it.[4] Physicians and hospitals who can bill privately may choose to see only patients who are easier to treat.[5] However, in the long run, preventing doctors from treating privately insured patients may not be the best way to increase their willingness to treat individuals covered by public entitlements and might divert skilled workers from the medical profession altogether.

For capital-intensive medical goods, such as hospital capacity or new drugs, increased private spending may likely help reduce average costs for public payers, as overheads can be spread over a larger level of output—with the cost borne by public entitlements and low-income patients able to be further reduced by price discrimination. However, if most hospital revenue comes from well-insured patients, attempts to attract them may increase the technological intensity and quality of care, which drives up the cost of treatment for all. But differences in the level of intensity of care from hospital to hospital and neighborhood to neighborhood may mitigate this externality.

To the extent that people are able to pay for services privately that would otherwise be provided publicly, a public entitlement program may have more funds to treat those remaining. Universal public entitlements, by contrast, may crowd out private spending, in which case higher taxes are incurred, without greatly expanding the provision of medical care.[6] Health-care entitlements that incorporate an element of means-testing may be more distributionally progressive, as benefits are concentrated on low-income enrollees, and the same value of public spending can be funded without taxes on low- to middle-income citizens. This dynamic may also hold, to some extent, for universal publicly financed benefits, which provide inferior access to medical care, from which more affluent citizens may opt out.[7]

The interaction of public and private payers may create an incentive for them to shift costs to each other, confusing responsibility and impeding accountability. Mixing public funds and private administration creates a risk that firms will try to privatize profits while socializing losses. Providing subsidies for individuals to purchase private insurance may not save public programs much money if these individuals would purchase insurance anyway and if they had previously used little care from the public system.[8] It may be easier to ensure that public subsidies are focused on advancing public priorities if the government entirely controls their disposal through public facilities.[9]

The incentives created by the interaction of public programs and private insurance are undoubtedly highly sensitive to small details of private market regulations and conditions attached to public payments. It is therefore essential to structure public programs and private insurance markets so that each is coordinated to complement the other, and so that organizations are accountable for efficiently delivering care, rather than encouraged to shift costs to each other.

|

GLOSSARY • Balance billing: an amount charged to patients by health-care providers above the government fee schedule • Capitation: payment per patient treated, rather than according to services provided • Coinsurance: a proportion of the bill that individuals must pay out-of-pocket • Copay: a fixed per-service amount that individuals must pay out-of-pocket • Deductible: an amount of medical costs the individual pays before insurance pays for services • Dual practice: the right of physicians to work for both public and private payers • Community rating: the requirement that premiums do not vary with enrollees’ medical risks • Fee schedule: the government’s list of prices it will pay for medical services • Global budget: the government’s limit on a hospital’s aggregate annual spending • Preexisting condition: a medical problem or need that an individual has prior to the purchase of insurance • Reference price: fixed reimbursement above which patients must pay costs out-of-pocket • Risk adjustment: redistribution between insurers according to medical needs of enrollees • Selective contracting: agreements between insurers and providers to join a network of preferred providers • Underwriting: varying insurance premiums according to enrollees’ medical risks |

Models of Public- Private Interaction

Health-care systems may be understood as operating along a spectrum that ranges from a pure single-payer model, where the government directly purchases all medical services, to a pure competing-payer model, where competing private organizations purchase all medical services. The dual-payer model exists as a hybrid, while the segmented-payer model refers to a patchwork of single, dual, and competitive payer models, each applying to different segments of the population. In this paper, the health-care systems of eight developed countries—for which standardized data are available and collected by the Organisation for Economic Co-operation and Development (OECD)—are analyzed and compared:

- Single payer (Canada and U.K.): the government is the predominant purchaser of medical services, with restrictions on private insurance.

- Dual payer (Australia and France): the government is the primary purchaser of medical services, supplemented by private insurance whose premiums are publicly subsidized.

- Competing payer (Germany, the Netherlands, Switzerland): the government subsidizes the purchase of private insurance.

- Segmented payer (U.S.): a patchwork of employer-sponsored insurance, public entitlements, and individually purchased insurance.

Canada (single payer)

Canada provides a universal entitlement to hospital and physician services funded through general taxation, with no associated out-of-pocket costs. It effectively prohibits the purchase of private health insurance that would improve individuals’ access to medically necessary services.

The public entitlement. The Canada Health Act of 1984 requires provinces to administer comprehensive coverage of all hospital and physician services through a uniform and universal entitlement that is portable across provinces and has no out-of-pocket costs for patients.[14] Provinces that comply with the Canada Health Act are eligible for block grants worth 23% of their health-care spending.[15] Dollar-for-dollar deductions are made from these federal grants to the extent that patients must incur out-of-pocket costs (such as copays or deductibles) to obtain covered services.[16] Almost all revenue for hospital and physician services comes from general taxes, mostly imposed at the provincial level.[17] Prescription drugs are not covered, but each province has separate targeted programs to provide drugs to the poor, the elderly, and other needy groups.[18]

Payments to providers. Provinces each have a single medical plan, with provider payment arrangements and waiting lists varying slightly among them. Canadians cannot seek care from other provinces in order to benefit from shorter waiting lists, but doctors are able to move to provinces where the government fee schedule (see the glossary) is set higher. Hospitals are usually public or nonprofit, and provincial governments establish global budget limits on what they may spend on patient care. Physicians are paid on a fee-forservice basis. Primary-care physicians generally play a gatekeeping role, with specialists paid less for services to patients if there is no referral.[19]

The Canada Health Act does not prohibit private care delivery, and physicians can opt out of the public system. However, the ability of the national government to withhold funds from provinces that allow private care that is inconsistent with a comprehensive, universal, and uniform entitlement leads them to find a variety of ways to constrain access to privately financed health care in practice.[20] Some provinces ban physicians who have opted out of the public program from billing more than their fee schedule, while others prohibit patients who see physicians who have opted out of Medicare from receiving publicly funded services.[21]

Health care delivered beyond hospital settings, such as prescription drugs, medical devices, and home health, lies beyond the scope of the Canada Health Act, and so its delivery through the private sector is less constrained.[22] This has allowed for the gradual growth in the outpatient provision of publicly covered services by the private sector, such as ambulatory surgery, diagnostic services, or rehabilitation care—whose availability through the public system is limited.[23] Almost all dental care is privately funded, as is most drug spending.[24]

Private insurance. The Canada Health Act does not explicitly prohibit private insurance for hospital and physician services. But provinces have been deterred from allowing it because of the risk that the federal government could determine that it threatens comprehensive, uniform, and universal public access to care—and could withhold their federal subsidy.[25] Private insurance for medically necessary services is officially prohibited by the majority of provinces, and only Newfoundland lacks any significant constraint on the ability of supplemental insurance to make available access to services nominally covered by Medicare.[26]

As a result, private insurance is mostly employer-sponsored coverage of non-Medicare services such as dentistry or prescription drugs.[27] Prescription drug spending is a third publicly funded, a third funded by private insurance, and a third out-of-pocket—roughly the same split as in the United States.[28] Some concierge-style clinics offer membership fees that provide immediate access to doctors, MRI scans, and other diagnostics without restriction, but these services are priced at levels that would appeal only to those who are very wealthy.[29]

A 2005 court declared Quebec’s ban on private insurance at odds with the province’s charter of rights, ruling: “Access to a waiting list is not access to health care.” Although Quebec subsequently legalized private insurance for outpatient surgery, no market has since emerged, thanks to limitations on covered benefits and the provincial government’s restriction on dual practice.[30]

United Kingdom (single payer)

The United Kingdom (U.K.) provides a universal entitlement to hospital and physician services funded through general taxation, with no associated out-of-pocket costs. It allows individuals to purchase better access to scheduled medical procedures through unsubsidized private supplemental insurance.

The public entitlement. U.K. residents receive a broad range of hospital and physician services, fully covered by public funds through the National Health Service (NHS), with no associated out-of-pocket costs. There are target limits on waiting times for individuals to obtain different types of care, though these are routinely violated in practice. There is no legally enforceable right for patients to receive any particular treatment.[35] Access to care varies greatly by specialty and geographic region.[36] Surgical procedures and drugs may also be excluded from coverage if they fail to gain approval for cost-effectiveness.[37]

Getting an appointment with a specialist requires a referral from a general practitioner. In theory, patients have a free choice of general practitioners; in practice, few accept new patients.[38] Prescription drugs determined to be cost-effective are also covered, and in 90% of cases are exempt from copays.[39] A range of supportive services, including post-acute care, home visits by nurses, and some eye and dental care, may also be provided without charge.[40]

Payments to providers. Public hospitals provide care exclusively for the NHS and are paid according to the diagnoses of patients admitted.[41] In recent years, the NHS has paid for some care at privately owned facilities—though 94% of spending remains at publicly owned hospitals.[42] Private hospitals don’t have emergency departments, and clinics tend to concentrate on the areas where gaps in public coverage are the greatest, such as imaging, joint replacements, and cataract surgery.[43] There are high barriers to entry for private hospitals, which has caused higher prices that are little constrained by competition from public hospitals.[44]

Most general practitioners work as NHS contractors and are paid according to a standard contract, negotiated collectively with the government, that blends capitation and fee-for-service compensation. Specialists usually work within hospitals as salaried employees with some private work externally on the side. Dual practice is allowed, but the income earned by NHS-employed specialists from private practice is restricted.[45] The share of the specialist workforce seeing some privately funded patients was 55% in 2006 but has declined over recent years.[46]

Private insurance. Individuals buy private insurance generally to circumvent waiting lists, gain broader access to specialists, or be treated in private rooms at hospitals. Insurance plans are mostly employer-sponsored and designed for acute care rather than ongoing chronic conditions. Private insurance is not available to cover high-cost cancer drugs that may be unavailable through the NHS.[47]

The premiums for private insurance are underwritten on initial enrollment and exclude preexisting conditions, but the plans can guarantee renewability without later underwriting. Insurers negotiate rates with providers, have their own fee schedules and preferred providers, and may use managed-care techniques; out-of-network providers may balance bill. Employer-sponsored supplemental plans were exempt from income taxation for those over age 60 from 1990 on, but this exemption was repealed in 1997.[48]

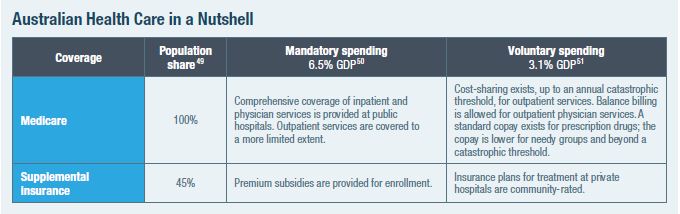

Australia (dual payer)

Australia provides a universal entitlement to medical services at public hospitals funded through general taxation, but independent providers of outpatient services may balance bill. Supplemental insurance to fund broader access to providers is tax-advantaged and publicly subsidized for lower-income groups.

The public entitlement. Australia’s Medicare program covers hospital, physician, and prescription drug services for all permanent residents.[52] It provides inpatient care at public hospitals with no associated out-of-pocket costs. The entitlement is more limited for outpatient care.[53] Specialty care and high-tech services are restricted in public hospitals. A referral from a general practitioner is needed for specialists to get the standard public reimbursement.[54]

The public drug benefit was initially limited to “life-saving and disease-preventing drugs,” but the list of covered prescription drugs has been expanded over time—with copays varying by income and consumption levels. The addition of drugs to the covered list is ad hoc but takes into account the cost-effectiveness of therapies.[55]

Payments to providers. Australia’s states administer and regulate public hospitals, which are paid according to the diagnoses of patients admitted, with disincentives (reduced reimbursement rates) for increased volumes.[56] The national government funds and administers a fee schedule and provides grants to states covering 40% of the costs of public hospitals.[57] Public hospitals may not balance bill for inpatient or outpatient services.[58]

There is little constraint on the private purchase of medical services.[59] Private doctors may claim reimbursement from the government fee schedule or bill private insurers without restriction.[60] Doctors who balance bill are not required to opt out of public funding.[61] Complex rules govern dual practice, which varies from state to state.[62]

Private hospitals, a mix of for-profit and nonprofit facilities, may balance bill.[63] About a third of hospital beds are in private facilities, which focus on elective surgeries and patients with less acute medical needs.[64] Some 60% of elective admissions are to private hospitals, but only 8% are emergency admissions.[65] Public and private hospitals are often located close together to facilitate dual practice.[66] Public hospitals may profit by supplementing their allowed public income with private patient revenues.[67] This gives states an incentive to steer costly outpatient cases from public hospitals to private doctors who bill Medicare, as it allows them to stretch their grant allocations further.[68]

Private insurance. The government pays 75% of official hospital fees for all, including those enrolled in private insurance—with private coverage merely paying additional charges. Private insurance allows patients to avoid waiting lists to see physicians or receive care in public hospitals by getting care at private facilities.[69] Private insurance premiums vary greatly, according to the extent of benefits and degree of cost-sharing.[70]

Private insurance premiums had been allowed to vary only according to age (a modified form of community rating), but this policy encouraged people to wait until after getting sick to sign up.[71] In 1999, a refundable tax credit was introduced for the purchase of private insurance, worth 25%–35% of premiums, depending on age.[72] Starting in 2000, private insurance plans may charge higher premiums to enrollees who have failed to maintain continuous coverage since the age of 30.[73] A tax penalty of up to 1.5% of income was also established on those who failed to purchase private insurance.[74]

France (dual payer)

The national government pays for hospital and physician services, funded through payroll taxes, but patients are often subject to substantial coinsurance and balance billing. Supplemental private insurance to cover these out-of-pocket costs is tax-advantaged and subsidized.

The public entitlement. France funds its public entitlement to medical care mostly through a payroll tax, but it also covers those who have never worked, financed by general taxation.[78] Coinsurance is 20% for inpatient hospital care, 30% for outpatient and dental care, 40% for diagnostics, and 70% for specialty care without a referral from a general practitioner.[79] Coinsurance for prescription drugs is 0%–85%, depending on assessments of the cost-effectiveness of drugs.[80] Covered services are often subject to small copays.[81]

Those with major chronic conditions, individuals with low incomes, pregnant women, handicapped children, and military veterans may receive medical care without having to pay coinsurance out-of-pocket.[82] Referral from a general practitioner reduces coinsurance for subsequent specialist consultations.[83] Public funds cover an average of 89% of inpatient spending and 57% of outpatient spending for those who do not have low incomes or major chronic conditions.[84]

Payment to providers. A third of French hospitals are publicly owned, a third are privately owned nonprofits, and a third are privately owned for-profit institutions. While public hospitals treat most inpatient cases, about half of outpatient procedures are performed at private hospitals.[85] Public hospital capacity, service volumes, available resources, and investments in new equipment must secure approval from regional planning groups.[86] Public hospitals within a region are required to share resources and infrastructure, and they may be subject to closure if they fail to meet minimum volume requirements.[87] Since 2004, hospitals have been paid according to the diagnoses of patients admitted, rather than by global budgets—though lump-sum payments remain for emergency care and transplant operations.[88] Private hospitals are not subject to global budgets but do receive lower reimbursement rates from the government.[89] This site-of-service price disparity is being challenged under European Union competition law.[90]

Payments for physicians performing procedures are bundled with facility fees for hospitals, except at for-profit facilities, where physician reimbursements are carved out.[91] Physicians based in public hospitals are salaried, but independent specialists are paid fee-for-service.[92] In France, 40% of physicians are salaried employees of hospitals; the rest work in private practice.[93] Dual practice is allowed, but income from private payers is restricted.[94] About 25% of doctors balance bill, but only a limited subset of doctors may do so.[95] The share of specialists balance billing is higher (42%), with the proportion doing so varying by region and by specialty (19% of cardiologists; 73% of surgeons).[96] Balance billing adds an average of 34% to physician incomes.[97]

Private insurance. Private insurance plans cover coinsurance and pay for access to private providers who balance bill. Coverage for balance billing is often written as paying a percentage of the public fee schedule (usually 200%–300%).[98] While all private plans cover coinsurance, only 48% of plans include coverage of balance billing—which is most common among dental providers.[99] Copays are not covered by supplemental insurance, but copays amount to no more than €50 per year.[100] Private insurance is designed to complement the incentives of the public system—with 0% coinsurance for care approved by gatekeepers.[101]

As the government held back the rate of growth of payments to public hospitals and more than doubled cost-sharing for outpatient services, private insurance enrollment increased from 30% in the 1960s to 95% in the 2010s. Tax incentives including an employer mandate penalty were also established to encourage firms to purchase supplemental plans for staff, and 44% of insurance is employer-sponsored.[102] While the poorest households are exempt from coinsurance, the near-poor receive income-based subsidies to help them purchase supplemental insurance.[103]

Nonprofit insurers (mutuelles) may vary premiums only by age. For-profit insurers may charge premiums based on underwriting and exclude preexisting conditions on enrollment but are subject to a 7% tax on premiums. However, this tax was recently extended to nonprofit plans.[104]

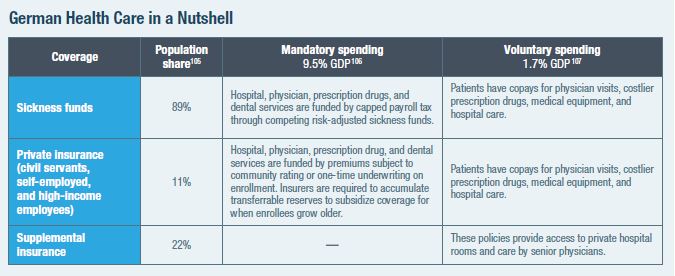

Germany (competing payer)

Germany provides a standard package of medical benefits, available through competing “sickness funds” (Krankenkassen), financed largely by a payroll tax. Higher-income individuals may instead purchase private insurance to get better benefits and access to care.

The public entitlement. Most Germans are enrolled in one of about 100 quasi-public, nonprofit “sickness funds,” financed through a 15.5% payroll tax on income up to about $50,000.[108] Revenues are collected by the central government and distributed to funds according to enrollees’ expected relative medical needs.[109]

Participation was gradually made mandatory for employees in different sectors of the economy, and individuals have been allowed to choose from competing funds since 1993.[110] Individuals can switch funds with two months’ notice, after being enrolled for 18 months.[111] Funds may charge small additional income-based premiums to enrollees, or use gatekeeping and networks of preferred providers to generate savings that can be returned to enrollees as supplemental benefits.[112] The distinction between “public” sickness funds and “private” insurance was once significant, but sickness funds are now almost as much subject to market forces as private insurance.

Private insurance. Civil servants, the self-employed, and those earning above $55,000 may opt for private insurance instead of coverage through sickness funds.[113] About half of private insurers are for-profit.[114] Private insurance enrollees are exempt from payroll tax contributions to support sickness funds but are still subject to other taxes used to support these funds.[115] Plans compete against one another and against sickness funds and may use deductibles to reduce premiums.[116]

Private insurance is financed by premiums that may be underwritten only at initial enrollment.[117] Premiums increase with the age of entry into private insurance, so there is an incentive for individuals to buy in when they are young.[118] Unlike sickness funds, private insurance requires additional premiums to cover other family members.[119] Plans must set aside 10% of premiums until age 60, as “aging reserves” that subsidize the purchase of plans when individuals grow older.[120] Private insurance premiums are supposed to be constant over enrollees’ lifetimes—though growing life expectancy and health costs make this fall short, in practice.[121] A Basistarif private plan option was established in 2009 to cover individuals with preexisting conditions. Basistarif plans may adjust premiums only by age, may not have premiums higher than the maximum sickness fund payroll tax, are limited in what they can pay providers, and are eligible for risk-adjustment subsidies financed by a tax on all private plan enrollees.[122]

An individual mandate penalty was imposed in 2009 on those failing to purchase public or private plans, with payment retrospectively required for premiums that had been missed.[123] Insurers may not cancel contracts and must pay for many services even if enrollees default on their premium payments. Enrollees may return to the public option only if they are under 55 and their earnings fall below a threshold, or if they are civil servants or self-employed.[124]

Payments to providers. A third of German hospitals are publicly owned, a third are nonprofit, and a third are for-profit—though about half of beds are in public hospitals and only a sixth in for-profit facilities. Over recent decades, the number of private hospitals has increased, while many public facilities have closed.[125] Hospitals were once used exclusively for inpatient care but now offer some outpatient procedures.[126] Charges for accommodation and meals may be carved out of hospital bills and agreed to by contract with patients before treatment is carried out.[127]

State governments determine the capacity of hospitals, which must meet minimum volume thresholds to gain reimbursement for complex procedures.[128] Hospitals were allocated global budgets but are increasingly reimbursed according to the diagnoses of patients admitted, subject to spending limits agreed to with sickness funds. Hospitals receive separate subsidies for capital investments if they accept patients from sickness funds, though these subsidies have declined significantly in recent years.[129] Physician fees are bundled into payments for inpatient hospital care, and hospital-practicing physicians work as salaried employees. But physicians delivering ambulatory care are paid fee-for-service, with some element of capitation increasingly common.[130]

Sickness funds pay providers according to a standard fee schedule, with regional spending limits agreed to by physician associations and fund associations.[131] Physicians receive lower fees if aggregate spending on their services exceeds a budget target.[132] Some 90% of physicians and 91% of hospitals see patients from the public health system.[133] Sickness funds may selectively contract with providers or require a referral by general practitioners before individuals can see specialists, but they have only recently begun to do so significantly.[134] Physician associations restrict the right of doctors to practice in other regions or in the private sector.[135]

Private insurers pay at a higher fee schedule, determined by the national government, and physicians may charge private insurers a multiple between 1 and 3.5 times the national fee schedule.[136] Physicians treating privately insured patients are not subject to volume restrictions, allowing enrollees access to superior-quality physicians or hospitals.[137]

Medical procedures are reviewed by the government for cost-effectiveness before they can be subject to reimbursement. Prescription drugs are classified into existing therapeutic groups, which may include generics, with reimbursement up to a reference price by sickness funds.[138] If drugs offer additional therapeutic benefits, the government sets reimbursement levels according to cost-effectiveness analysis.[139] Private insurers may also claim rebates from drug manufacturers.[140]

The Netherlands (competing payer)

The Netherlands allows individuals to choose coverage from competing insurance plans, largely funded by payroll taxes, with additional mandatory community-rated premiums that are subsidized for those outside upper-income groups.

The public entitlement. In the Netherlands, 40 private insurers provide competing comprehensive coverage. The plans are funded half through public subsidies and half through community-rated premiums, with funds redistributed between plans, according to the relative medical needs of their enrollees.[145]

Residents who fail to purchase a plan are assessed a penalty of about 130% of the premium (there are many plans, but most premiums are about the same).[146] Insurers may not withhold coverage from individuals who fail to pay premiums, but unpaid premiums are automatically deducted from their incomes.[147] Two-thirds of households receive additional subsidies, which are provided in advance of their purchase of a plan. These subsidies are based on income levels from the previous year, and then reconciled in tax assessments.[148] Premiums for those under age 18 are publicly financed.[149] Premium discounts of up to 10% may be obtained in return for the purchase of plans offered by employers, unions, or any other organized group.[150]

A referral from a general practitioner is required to see a specialist or to obtain an elective hospital procedure.[151] Insurance coverage is subject to a mandatory deductible, but there are exemptions for primary care and family medicine.[152] Plans may offer managed-care or high-deductible options in return for lower premiums, but premium reductions are capped.[153] Insurers may waive deductibles to encourage patients to go to in-network providers.[154]

Payments to providers. Most hospitals and clinics are private nonprofits. Prices for elective care (70% of hospital spending) have gradually been deregulated.[155] Maximum prices set by the government remain in effect for hospital services that have not been deregulated and for specific services performed by general practitioners.[156] Prices for hospital procedures still subject to regulation, along with overall target spending levels, are negotiated between associations of hospitals and insurers, brokered by the government.[157] The government has the right to recoup hospital revenues if aggregate hospital spending across the country overruns the permitted rate of growth, but this policy may provide an incentive for each hospital to boost prices in order to better bear the collective punishment.[158] A safety-net fund for hospitals was established to facilitate the transition to competitive pricing.[159]

Selective contracting is permitted for hospitals, so long as insurers include sufficient providers to satisfy demand without waiting lists.[160] However, the effectiveness of selective contracting has been hobbled by a court ruling that insurers reimburse 75%–80% of the costs of out-of-network care.[161] Nor is selective contracting permitted for general practitioners, where prices generally reflect maximum amounts permitted by the state.[162]

Certificate-of-need laws restricting hospital capital investments, which were used to plan and allocate funds for expanded capacity, were abolished to allow facilities to make investments according to market-based calculations.[163] For-profit hospitals are currently prohibited, but the parliament has attempted to repeal this ban to encourage investment.[164] However, private investors can be paid “a result-related compensation for risk capital,” so long as they are not owners of the hospital.[165] For prescription drugs, insurers will often reimburse only the amount needed to cover the lowest-price generics, which reduces patient access to branded drugs.[166]

Supplemental insurance. Major legislation in 2006 integrated public subsidies and private insurance—replacing the two-tier system of private insurance for the wealthy and a government program that purchased services for the majority of the population.[167] The goal was to reduce segmentation, improve equity, and replace government regulation of the provision of medical services with oversight by private managed-care organizations.[168]

Today, supplemental private insurance covers dental, physical therapy, and other services that are not part of the standard benefit. Yet the appeal of such insurance is declining, as individuals are less willing to pay for insurance to protect themselves from stable routine expenses.[169]

Switzerland (competing payer)

Switzerland requires its residents to purchase private insurance, largely funded by premiums, with cantons providing additional subsidies to hospitals and low-income individuals.

The public entitlement. Residents of Switzerland for more than three months must purchase insurance that covers essential health benefits from private nonprofit organizations.[173] The standard benefits package is very broad and even includes alternative medicine, as the result of a series of national referendums. Insurers must be nonprofit, are nationally regulated, are required to set community-rated premiums, and are subject to some redistribution between plans, according to the relative medical needs of enrollees.

Plans may reduce premiums by requiring a referral to see specialists, establishing networks of providers, or increasing deductibles up to a maximum limit—though deductibles must also exceed a set minimum. Coinsurance is 10% above the deductible, up to a catastrophic cap. The coinsurance for branded drugs is 20% where there are generic substitutes.[174]

Health insurance is mostly funded through mandatory and uniform premiums, rather than income-based taxes. However, the government provides additional subsidies to limit premiums as a share of household income.[175] Premiums and subsidies may vary greatly among cantons.[176]

Payments to providers. Most hospitals are publicly subsidized by cantons, and inpatient care is financed half by insurance, half by direct subsidies.[177] Before 2012, cantons paid hospitals to treat their residents. Since then, hospitals have been paid patient-by-patient, according to a national fee schedule, allowing individuals to seek treatment beyond their home cantons.[178] A third of hospitals are private and ineligible for subsidies from cantons, but they are paid higher rates (by insurers and by individuals with cost-sharing) and may provide better-quality amenities.[179]

Dual practice is allowed in Switzerland—specialists who are salaried employees of public hospitals may also maintain a private practice.[180] Ambulatory-care physicians are paid by a national fee schedule, which is generally the product of negotiations between groups of insurers and groups of physicians. Physicians may not balance bill.[181] A “necessity clause” seeks to restrict the establishment and proliferation of new specialists and providers of outpatient care. Drugs are included on formularies according to cost-effectiveness determinations, with tiered coinsurance where generics are available.[182]

Supplemental insurance. Premiums to purchase supplemental insurance can be underwritten and may be managed by for-profit insurers. Such plans have long been available to cover services that are exempt from Switzerland’s mandatory benefit package but are prohibited from reducing cost-sharing associated with covered services.[183] Supplemental plans are neither subsidized nor eligible for purchase with pretax funds.[184]

As mandatory coverage has gradually been expanded, the demand for supplemental insurance has greatly diminished. There was strong political pressure to add drugs to mandatory coverage after they become widespread under voluntary insurance coverage. The reform requiring mandatory plans to cover access to hospitals beyond individuals’ home cantons eliminated the main motivation for them to purchase supplemental insurance. The absence of significant waiting times in Switzerland means that few people purchase supplemental insurance to get preferential treatment.[185]

United States (segmented payers)

The U.S. provides entitlements to medical care through programs for the elderly and low- to middle-income residents, which may be used to purchase privately managed plans. Employer-sponsored insurance is exempt from income taxes, and subsidies are provided for hospitals to deliver care to the uninsured.

The public entitlement. Government health-care entitlements target discrete sections of the population. The diversity of U.S. publicly financed health-care programs and the aggregate amount spent on them are both as great as those for all the other countries in this paper combined.

Medicare covers hospital and post-acute care for all elderly and disabled Americans who have made sufficient payroll tax contributions. Heavily subsidized coverage of physician services and prescription drugs is available with the payment of additional premiums. Medicare covers three-fourths of medical expenses, and enrollees often purchase supplemental private insurance to further reduce deductibles and coinsurance, though balance billing is prohibited. Originally, the federal government purchased medical services directly for all beneficiaries, but a third of enrollees now opt to receive coverage through private insurers (in Medicare Advantage plans) that may contract independently with providers and compete by reducing out-of-pocket costs and providing additional benefits such as dental care.

Medicaid and the Children’s Health Insurance Program (CHIP) cover low-income Americans. They are funded mostly by the federal government but are managed by states. As a condition of receiving funds, states must provide comprehensive coverage of hospital and physician services without significant out-of-pocket costs to defined categories of low-income Americans. States may claim additional federal funds to expand eligibility and provide benefits (such as long-term care, prescription drugs, or dental coverage) above Medicaid’s mandatory floor.

While states may make separate health-care expenditures, their spending tends to be focused on Medicaid activities, for which they may claim matching funds from the federal government. States may, however, apply for waivers to use Medicare and Medicaid funds to provide coverage in forms that are not specifically prescribed under those programs’ statutes. Recent years have seen an increase in the share of health-care spending that is publicly financed, along with a rise in the proportion of publicly financed health care that is administered by private insurers.[190]

Payments to providers. Most community hospitals in the U.S. are privately owned nonprofit organizations, but a quarter are for-profit firms, and a sixth are owned by state and local governments.[191] Physicians may choose whether to operate in private practice, as employees of hospitals, or in integrated managed-care organizations. The hospital market structure varies significantly from state to state, with the majority regulating capital investments and the expansion of specialty hospitals.[192] Similarly, states have much influence over physician certification and the permitted scope of medical practices.

Hospitals must accept patients funded by Medicare or Medicaid and provide uncompensated care to uninsured individuals in order to qualify for broad exemptions from state and federal taxes. Access to hospitals is broad under both Medicare and Medicaid, but access to physicians under Medicaid may be limited in some states—particularly for specialists. Reimbursement for medical care provided to those who are privately insured may depend on plans’ networks of preferred providers.

Private insurance. Most Americans ineligible for public entitlements receive health insurance purchased by their employers. Employers can provide insurance as compensation to their staff without incurring income or payroll taxes, and larger employers (50 or more employees) incur a penalty if they fail to do so.

Individuals who do not receive health-care coverage through entitlements or employment may purchase coverage directly from private insurers in state-regulated markets. They may sign up at any point of the year to purchase underwritten insurance through the Short-Term Limited Duration market. They may also, during limited enrollment periods, purchase community-rated plans through the Affordable Care Act. Low- to middle-income households may also be eligible for subsidies to assist with the purchase of ACA plans.

The Health-Care Models Assessed: Access, Volume, Quality, and Cost

Great caution must be exercised in drawing inferences from a comparison of health-care statistics across countries. This is because countries differ in many ways—including national income, medical needs, political systems, wage rates, and other government

policies—beyond the influence of differences in their health-care systems.

It is best to focus specifically on factors such as the access, quality, cost, and quantity of medical services available, rather than broad differences in medical outcomes, as medical outcomes may differ for a variety of other reasons. It is also possible to learn from how these factors have changed, as individual countries have altered their policies over time.

How the Models Compare*

/*Sources for the charts: IPSOS (2018): “Global Views on Healthcare—2018,” IPSOS Global Advisor, 2018; Commonwealth Fund (2016): “2016 International Survey of Adults,” Commonwealth Fund, 2016; OECD (2015): Health at a Glance 2017, OECD Indicators, 2017; (data is for 2015); OPTN/SRTR (2010): Bertram L. Kasiske et al., “OPTN/SRTR 2011 Annual Data Report: International Data,” American Journal of Transplantation 13, no. 1 (January 2013): 199–225; AHRQ (2014): AHRQ (Agency for Health Care and Quality) (2014): (appendectomy chart) Claudia A. Steiner et al., “Surgeries in Hospital-Based Ambulatory Surgery and Hospital Inpatient Settings, 2014,” AHRQ Statistical Brief no. 223, February 2018; AHRQ (2014): (heart bypass chart) Kimberly W. McDermott et al., “Overview of Operating Room Procedures During Inpatient Stays in U.S. Hospitals, 2014,” AHRQ Statistical Brief no. 233, December 2017; Ianchulev et al. (2016): Tsontcho Ianchulev et al., “Office-Based Cataract Surgery,” Opthalmalogy 123, no. 4 (April 2016): 723–728; OECD (2018): Health Spending, OECD.data/

Canada (single payer)

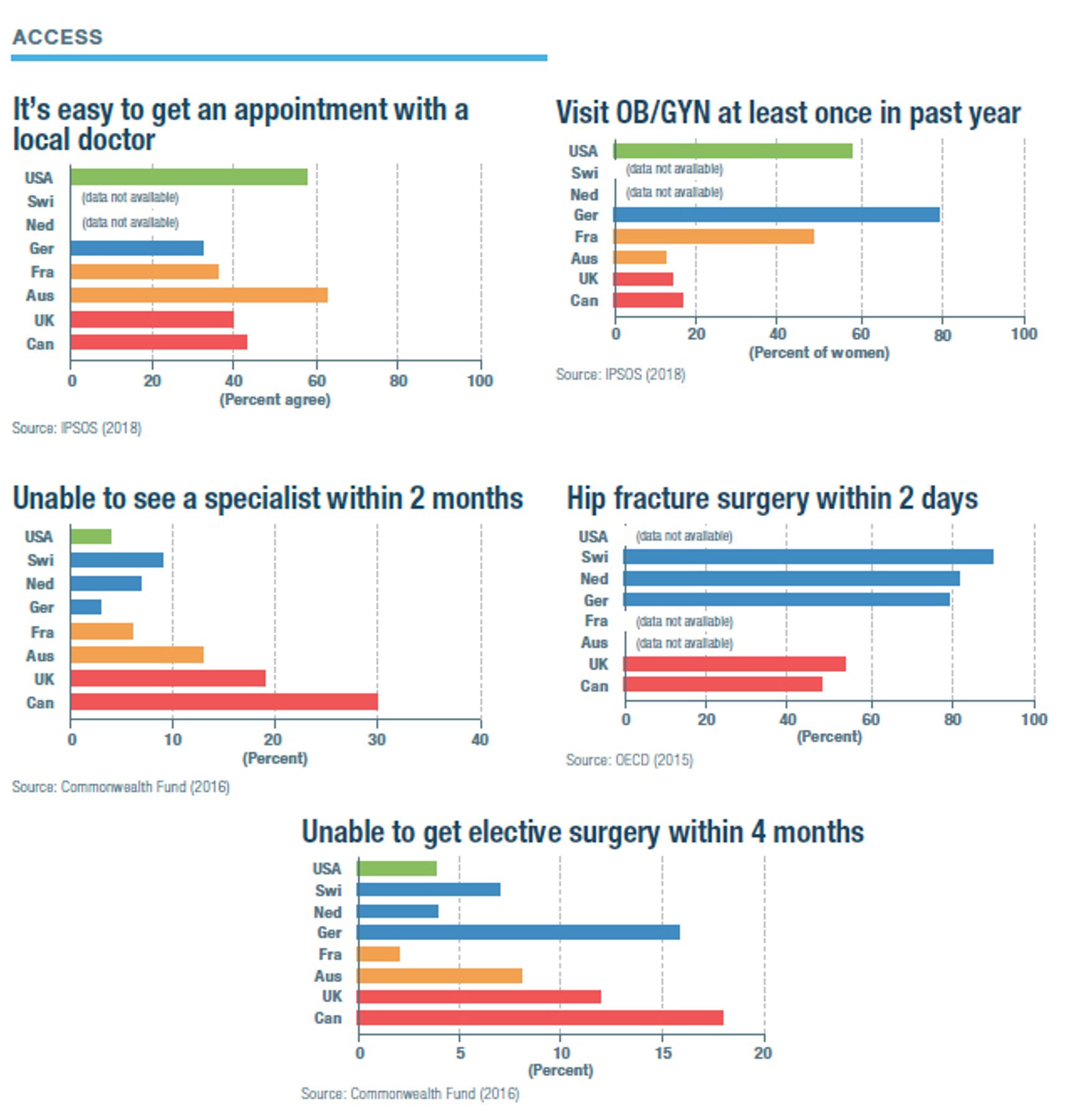

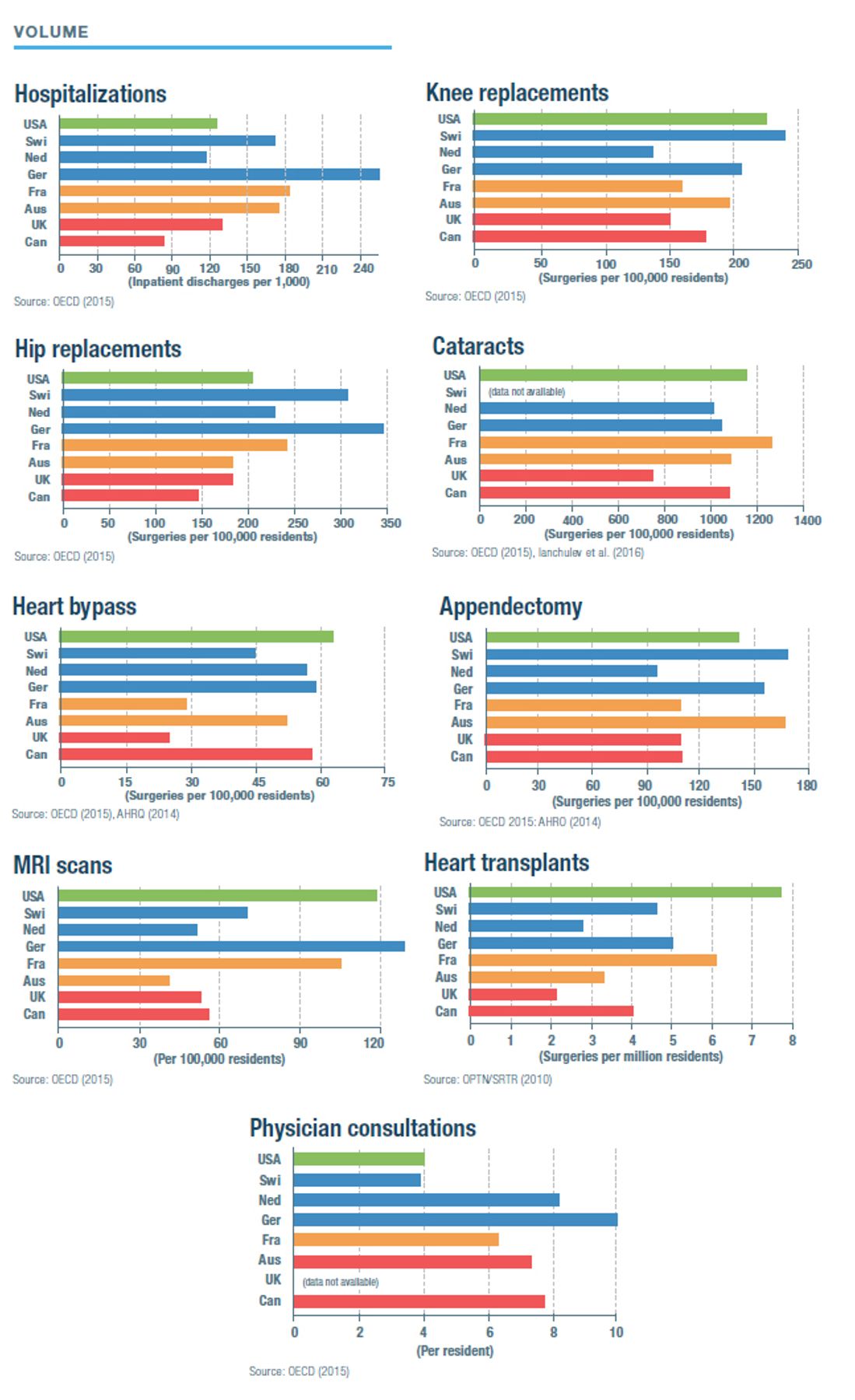

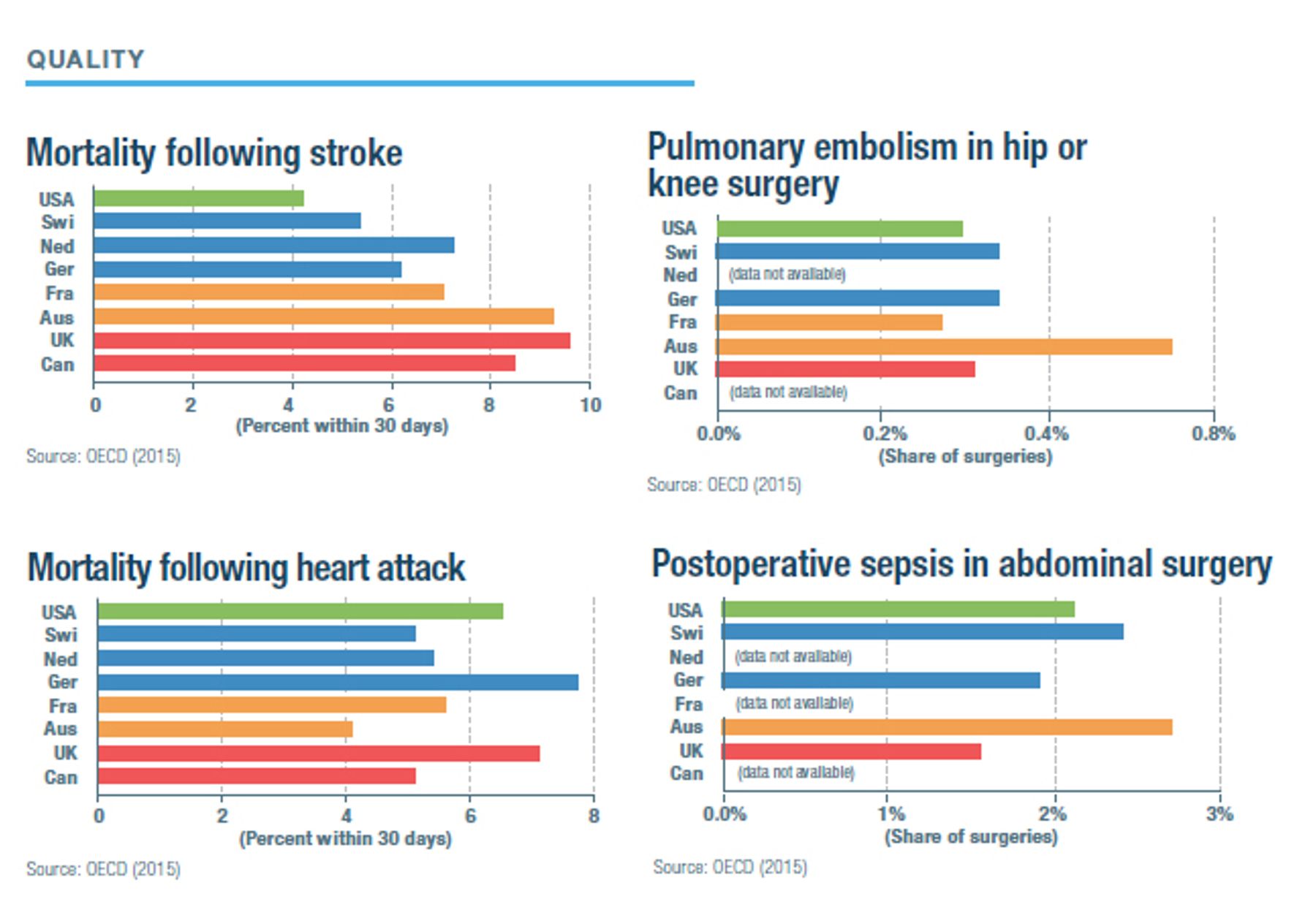

Canadians have easy access to general practitioners, but getting an appointment to see a specialist is more difficult than in all the other nations studied in this report. The Canadian medical system provides the least hospital care, delivers consistently fewer outpatient procedures, and provides much less access to modern diagnostic technology.

The median waiting time for treatment by a specialist following referral by a general practitioner was 20 weeks in 2018 (4 weeks for oncology, 10 weeks for elective cardiovascular procedures, 21 weeks for gynecology, 26 weeks for neurosurgery, and 39 weeks for orthopedic surgery). There were also substantial waiting times for diagnostic tests: 4 weeks for an ultrasound and 11 weeks for an MRI.[193] Seven percent report that they were unable to find a regular doctor.[194]

Canada spends a similar amount on health care as do most other developed nations, though significantly less than the U.S., with which it shares a high-cost labor market. But the average out-of-pocket costs faced by Canadians are similar to those faced by Americans, as many in Canada lack prescription drug coverage—which covers the most common out-of-pocket expense. Access to drugs is often limited: provincial drug plans for low-income Canadians cover an average of 23% of drugs, by comparison with 83% for private drug plans.[195]

United Kingdom (single payer)

Britain’s health-care system requires the fewest out-of-pocket payments from patients but lags behind other nations in funding access to quality medical care. The country faces a constant struggle to reconcile a rapidly growing demand for medical care with government budget constraints. Private funding has been increasingly squeezed out by unsupportive government policy (including restrictions on dual practice).

U.K. hospitals often lack cutting-edge technology, and mortality after major emergency hospitalizations compares poorly with that of other nations in this report. Access to specialists is very limited, and the system falls well short of most other nations in the delivery of outpatient surgery.

Annual pay increases for medical staff were capped at 1% during 2015–18.[196] Fifty percent of senior physicians are considering reducing their working hours, and 60% of specialists intend to retire at or before age 60.[197] There are 100,000 unfilled staffing vacancies, straining the workforce of 1.2 million.[198]

By November 2018, 4.2 million of the 55 million people in England were on waiting lists for elective care—up from 2.7 million in March 2013, with only 1.3 million receiving treatment each month.[199] Median waiting times to receive treatment from specialists range from 5.4 weeks to see a geriatrician to 8.2 weeks for neurosurgeons.[200] Of the patients requiring urgent cancer care, 18% do not receive treatment within two months of referral—a proportion that rises to as much as 41% in some parts of the country.[201] Of the patients needing emergency care, 15% must wait over four hours to be seen—up from 4% in 2013.[202]

Australia (dual payer)

Australia holds an intermediary position between single-payer and multi-payer health-care systems, as just under half the population has private insurance for hospital and physician services. Its system offers good access to general practitioners but restricted access to care and often high out-of-pocket costs for those who lack private insurance.

Private hospitals enable Australians to obtain surgeries from modern facilities without waiting lists, but there is a growing segmentation of publicly funded patients into public hospitals and privately insured patients into private hospitals.[203] For those reliant on the public system, waiting times for inpatient procedures were similar to those in single-payer countries such as Canada and the U.K.[204] Waiting times for many kinds of outpatient surgery increased by 50% from 2002 to 2012.[205]

The establishment of guaranteed renewability without underwriting for individuals who maintained continuous insurance coverage caused enrollment in private insurance to suddenly increase from 32% to 45% of the population.[206] The establishment of subsidies and a tax penalty on those who failed to purchase private insurance had a much smaller impact on enrollment.[207] Only 11% of enrollees have first-dollar insurance coverage, suggesting that mandates and incentives may have encouraged them to purchase thin coverage.[208] Out-of-pocket costs are particularly high for prescription drugs, for which public reimbursement levels are low.

The complexity of financial interactions between public and private payers, and between state and federal governments, has created a myriad of opportunities for cost-shifting between them.[209] This has led to frequent political battles passing blame, confusing accountability, and inducing gaps in service.[210]

France (dual payer)

France provides a modest government-funded benefit, but almost everyone has supplemental private insurance. Access to specialists and surgery overall is very good.

The policy accommodating balance billing appears to have encouraged vigorous price competition, as consumers are highly price-sensitive at the margin.[211] In regions where physicians are scarce, most physicians balance bill, and the growth of private insurance to cover balance billing is associated with significant price increases.[212]

There is an eightfold difference in the number of specialists between the highest and lowest regions. In regions with few physicians, most balance bill. Overall, 40% of physicians balance bill and refuse to see patients without private insurance, as these patients cannot be charged more than the government fee schedule.[213]

The dual-payer system adds some administrative rigidity and waste. Separate insurance to cover cost-sharing means that each medical claim involves two payers, almost doubling overall administrative costs.[214] As they do not bear responsibility for the bulk of medical costs and are unable to selectively contract, insurers have little incentive or ability to make the delivery of care more efficient.[215]

Germany (competing payer)

Germany’s system of competing insurance plans provides excellent access to specialty care and surgical services, with out-of-pocket costs rarely impeding access to care. The amount of care provided on an inpatient basis is unusually high, compared with the other countries in this report, although this is gradually changing. Public hospitals have lower costs, but private hospitals have more investment and shorter waiting lists.[216]

Among community-rated sickness funds, there is some evidence of plans selecting against elderly and chronically ill enrollees.[217] Healthier individuals tend to opt for “private” plans, where they can qualify for lower premiums as a result of underwriting, and 80% of private insurance enrollees opt for plans with higher cost-sharing than is standard through sickness funds.[218]

Privately insured patients face significantly shorter waiting lists for specialty care than enrollees of sickness funds, are more likely to receive innovative drugs, tend to be kept in the hospital longer, and are 50% more likely to receive organ transplants, despite being healthier on average.[219] Waiting times for a sample of six outpatient treatments increased from an average of 27.5 days in 2014 to 30.7 days in 2016 for patients covered by sickness funds, whereas they fell from 13.5 days to 7.8 days for those covered by private insurance.[220] Waiting times for primary care were slightly shorter for those covered by private insurance, though residents of the former East Germany faced waits twice as long.[221]

The Netherlands (competing payer)

The Netherlands sought to move away from a segmented two-tier health-care system to help improve access to care for those unable to afford private insurance.[222] Market-based mechanisms for insurers and providers have replaced rationing and waiting lists as methods of cost control. This has also increased the autonomy of providers and facilitated the portability of insurance coverage between jobs and across the country.[223]

As prices for elective care have been deregulated and made subject to competition, they have increased more slowly than prices that remain subject to regulation and set by collective negotiation.[224] The number of outpatient specialty facilities has soared from 30 in 2000 to 280 in 2010, and prices in these facilities are 15%–20% lower than in hospitals.[225] Following the transition to a competitive system, waiting times for joint replacements, cataracts, and heart surgeries fell to levels much lower than in single-payer countries.[226] As the cost of care has fallen, demand has increased, so total spending has not fallen along with costs.[227] Spending on specialists increased from €17 billion in 2006 to €27 billion in 2016.[228] Single hospital rooms, which had largely disappeared, are reemerging.[229]

The breadth of eligibility for publicly subsidized premiums makes the Dutch health-care system less progressive.[230] Tight regulations on insurance premiums have also caused out-of-pocket costs to increase.[231] They have also limited resources available to the system, and waiting times for outpatient care are beginning to increase again.[232]

Community rating has encouraged insurance plans to appeal to healthier enrollees, and this incentive has not been entirely mitigated by risk adjustment.[233] There is a constant battle to avoid insurers cherry-picking healthier enrollees, with “selective marketing” to them by plans recently being prohibited.[234] Discounts to groups, such as employers, under community rating, have served only to increase premiums for those left out.[235]

Switzerland (competing payer)

Switzerland does not limit the amount of health-insurance coverage that individuals may purchase, which allows good access to specialists, high volumes of surgeries, and innovative high-quality care. But public hospitals remain highly sheltered from price competition, and insurance-market rules inadvertently impose high out-of-pocket costs on patients.

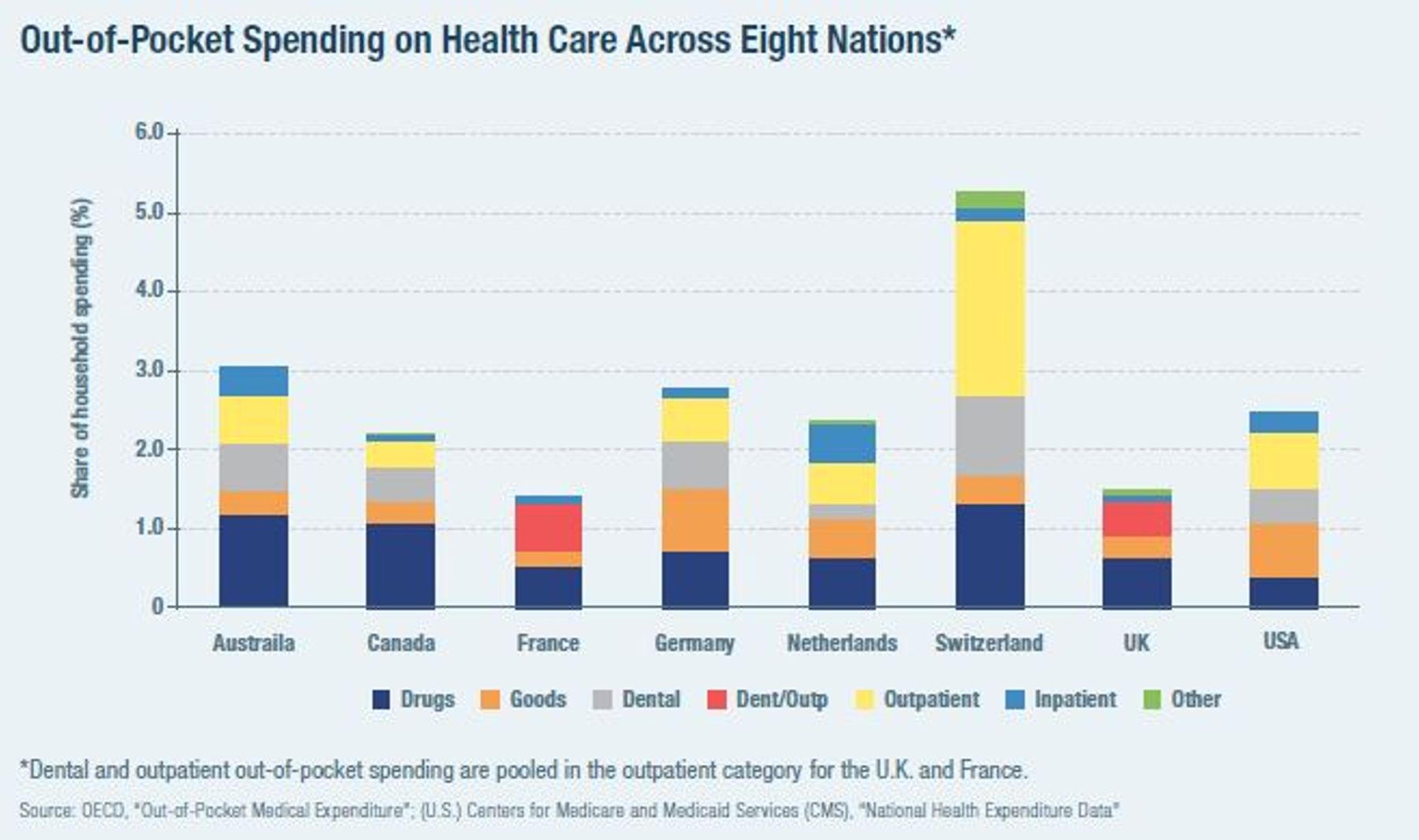

The combination of community rating and inadequate risk adjustment induces healthy individuals to flock to plans offering the maximum permitted deductibles.[236] The share of health-care costs borne out-of-pocket (28%) is the highest in the developed world.[237] This reliance on deductibles as a substitute for premiums may reduce the utilization of low-cost preventive care without doing much to limit wasteful utilization of services or encourage the highest-spending patients to seek hospital care from more cost-effective providers.

The delivery of Swiss medical care remains inefficient, with a large number of hospitals for its size and a high average length of stay.[238] To some extent, this reflects the absence of significant rationing and substantial direct subsidies to hospitals from cantons. Differences in spending levels among cantons tend to reflect variation in the use of medical services.[239]

U.S. (segmented payer)

American health care delivers high volumes of the highest-quality surgical services, though usually at a very high cost. The system is oriented around the preferences of well-insured individuals with a high willingness to pay for convenient, high-intensity care. Access to specialists and surgical services is good for most Americans who are covered by private insurance or Medicare, though it may be less so for those who are on Medicaid or are uninsured.

The tax exemption of employer-sponsored health insurance provides half the population with coverage but insulates the delivery system from direct consumer control and sensitivity to costs. Employer-sponsored health insurance also threatens individuals with the prospect of gaps in coverage if they lose their jobs.

The patchwork of different payment systems inhibits accountability and increases administrative costs, and leaves those in gaps between different sources of coverage facing enormous costs. These gaps are often dealt with in a roundabout way—by subsidies for providers to treat the uninsured. Out-of-pocket costs may be extremely high for out-of-network hospital care, but these costs account for only a small fraction of medical bills, and hospitals rarely collect payment from uninsured low-income patients.

Overall, American health care reflects a system that has been constructed incrementally over 70 years, with problems resulting from inflated costs tending to be addressed by the provision of additional funds rather than through greater accountability and austerity. The gradual privatization of care delivery under Medicare and Medicaid has tended to increase access to care, though it has not reduced public spending.[240]

Conclusion

Single-payer health-care systems, such as those in the U.K. or Canada, are structurally similar, while the interaction of multiple payers tends to differ greatly from country to country. Dual-payer and competitive-payer systems blend into each other, according to the extent of the public entitlement in dual-payer countries and the degree to which all options in competitive-payer countries are constrained by a common delivery system. For instance, provider compensation may be more market-based in dual-payer France than in competing-payer Switzerland.

This means that it is possible to draw general conclusions about single-payer health care to an extent that is not possible for any other particular model. Single-payer systems share the common feature of limiting access to care according to what can be raised in taxes. Government revenues consistently lag the growth in demand for medical services resulting from increased affluence, longevity, and technological capacity. As a result, single-payer systems deliver consistently lower quality and access to high-cost specialty care or surgical procedures without reducing overall out-of-pocket costs. Across the countries in this paper, limitations in access to care are closely tied to the share of the population enrolled in private insurance—with those in Britain and Canada greatly limited, Australians facing moderate restrictions, and those in the other countries studied being more able to get care when they need it.

Waiting lists are inherent to single-payer systems; they are not produced by the very limited role of private insurance that is allowed to operate around them. The concern that private demand for medical services will deprive public programs of staff and facilities, rather than enable scarce public funds to be supplemented by additional private resources, is ultimately a problem only to the extent that the supply of medical resources is fixed.[241] This is most likely to be a problem for skilled labor and is better addressed by expanding its supply, rather than by trying to suppress wages by depriving patients of private access to care.[242] Indeed, restrictions on private health-care spending are likely to exacerbate any physician shortage over the long run.

Nonetheless, in dual-payer and segmented-payer systems, public and private payers constantly endeavor to shift costs to each other—an enterprise for which the complexity of health-care payment affords a near-limitless set of opportunities. There is also a continual confusion of responsibility and an absence of accountability. Under employer-sponsored insurance in the U.S., the separation of responsibility between those in charge of procuring care and those responsible for paying for it has led to the development of increasingly expensive sources of care with little attention to costs.[243] The segmented-payer system generates the most funding for health care overall. However, in fully accommodating individuals’ willingness to pay for care, this approach increases the intensity of care to an extent that is painfully expensive for a minority that falls between gaps in entitlements and employer-sponsored insurance.

The competing-payer model ideally gives insurers the freedom and responsibility to procure health-care services in a way that attracts people to their plans by offering them the best benefits and the lowest medical costs. While all competing-payer systems fall short of this ideal, in practice they consistently offer good access to high-quality medical care with good insurance protection. The competing-payer model is, therefore, best understood as an objective that is sought rather than yet realized—and countries including Germany, the Netherlands, France, and the U.S., which have experienced the most significant health-care reform over recent years, are each moving toward it.

Endnotes

Photo: monkeybusinessimages / iStock / Getty Images Plus

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).