How to Make Student Debt Affordable and Equitable

Photo: William_Potter / iStock / Getty Images Plus

The federal student loan program is needlessly complex, fails to offer an effective safety net for borrowers in financial difficulty, and distributes the largest benefits to borrowers who need them the least. This paper proposes a plan to simplify the system by providing all eligible students with a single $50,000 line of credit, with repayments structured as an income-share agreement (ISA). Borrowers would remit a small fraction of their earnings to the government on their income taxes, capped at 1.75 times the amount borrowed and for a maximum term of 25 years.

For many undergraduates, the repayment terms would be as good as they are today. Students who borrow against their line of credit for graduate and professional degrees, and undergraduates who go on to earn high incomes, will pay more than under the current program because they would lose access to the current system’s overly generous loan-forgiveness terms. The terms of a federal ISA will be easier for student borrowers to understand. Similarly, income-tax-based repayments will make it easier than today’s cumbersome income-based repayment program for borrowers to have their payments set.

Introduction

The system of federal student lending for higher education in the U.S. is falling short. Students face an unnecessarily complex menu of loan types and repayment options, and the lack of appropriate constraints on borrowing for some groups creates perverse incentives that do not serve borrowers well.

Worse, the safety net designed to support borrowers in financial difficulty, income-based repayment (IBR), has failed to meaningfully reduce the delinquencies and defaults that cost taxpayers $4 billion a year.[1] IBR lets borrowers cap their loan payments at an affordable share of their income, which was supposed to make debts affordable for anyone experiencing a hardship.[2] The current system is also failing taxpayers in another way. Excessive subsidies are delivered through IBR mainly to individuals who need them the least: middle- and upper-income individuals who seek graduate degrees—a group that historically has rarely defaulted on federal student loans.[3] With that in mind, it is little surprise that loans repaid through IBR, which were slated at their inception in 2009 to cost $1 billion annually, are now expected to cost over $14 billion annually.[4]

Even with this huge expenditure, it seems that the safety net is failing precisely those whom it was designed to help. Data on enrollment in IBR suggest that low-income borrowers often do not know that IBR exists.[5] And those who do know often fail to enroll because design flaws have made it unnecessarily challenging to do so.[6]

The current federal lending program, including IBR, is the product of countless incremental changes, enacted through a patchwork of legislative changes and executive actions. This approach to reform has led to a policy regime comprising several loan types and a dozen repayment options that fail to meet the needs of students or taxpayers.

Comprehensive reform is overdue. What’s needed is a new system of federal student lending that is simple for students, provides adequate but not excessive resources for borrowers, and has an effective and efficient safety net to ensure that paying for college does not create a lasting and inescapable financial hardship.

In this paper, I’ll describe how these goals can be achieved by establishing a single $50,000 line of credit, with repayment terms structured as an income-share agreement (ISA), such that students remit a small fraction of their earnings for 25 years in exchange for access to funds that will help them pay for their education.

How a Federal ISA Would Work

Students drawing funds from their line of credit would agree to repay at a rate of 1% of their income for every $10,000 they borrow. At this rate, borrowers who decide to use the entire $50,000 available would be on the hook to remit 5% of their earnings for the first 25 years after leaving school.

Crucially, they will also agree to repay this obligation through income-tax withholding. While this is a big departure from the status quo for student lending, it involves only minimal changes to the tax-collection system. And it allows us to largely do away with the costly system of loan servicing and collection agencies.

Linking payments to income and withholding the payments from a borrower’s paychecks also ensure that the borrower’s payments always track their income in real time. Borrowers in financial distress due to low or no income will automatically owe nothing on their debts.

The ISA mechanism eliminates the potential for aid to be delivered in a regressive manner, as is often the case with federal student loans today. Instead, borrowers who see large returns on their education will make larger payments commensurate with their higher income. These larger repayments will help offset the cost that taxpayers bear for those borrowers who face unexpectedly low returns on their education.

This elegant solution to higher-education financing has another advantage: it makes interest rates unnecessary. Charging interest works poorly in the current system because borrowers who do sign up for today’s IBR program often make monthly payments that are less than their accruing interest when their income is low relative to their debts. While the borrowers remain current on their obligations, they may be demoralized as they watch their balances grow month after month.

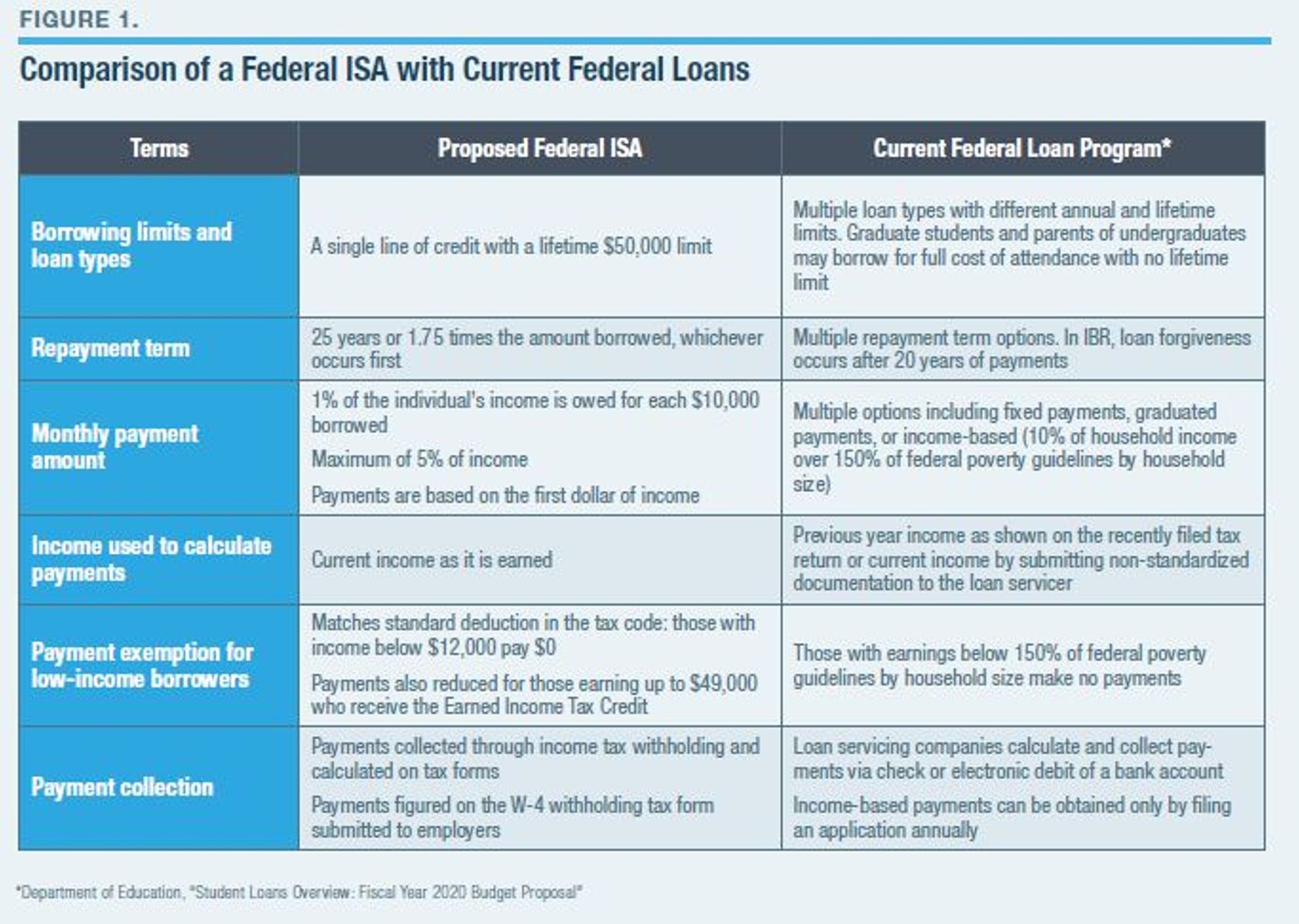

Critics of ISAs (and the existing IBR program) may wish to dismiss this proposal out of hand. But I encourage readers to recognize that the movement to an ISA-inspired system of federal lending is not a departure from the spirit or intentions of the existing regime. It’s simply a more efficient and effective mechanism for satisfying the goals that motivated policymakers to create and expand the federal loan program and the corresponding safety net (Figure 1).

The Benefits (and Challenges) of Repayment Through Tax Collection

Collecting loan payments through the tax system has major advantages over borrowers repaying loans through IBR. The main one: payments track income as it is earned, so there is no annual certification process that borrowers must complete.

Under the current system, borrowers submit documentation of their income to their loan servicer, usually the previous year’s tax return; based on the return, the servicer sets the monthly payment for the current year. Thus, the payment calculation is backward-looking and static for 12 months, no matter how much the borrower’s current income fluctuates, unless the borrower requests a recalculation mid-year due to a change in income and then submits additional paperwork and supporting documentation. If a borrower fails to resubmit this income information on time and correctly each year, monthly payments automatically jump to the original fixed 10-year term, which can be many times the income-based repayment.

Another advantage is that the proposed ISA would not require the government to contract with student loan servicing companies to send borrowers statements, process IBR applications, collect payments, and inform borrowers of their repayment options. Those administrative activities cost taxpayers approximately $3 billion a year.[7] Of course, some administrative burden would remain for Department of Education, and some new burden would be imposed on the Internal Revenue Service and borrowers. But the net effect could reduce total costs.

The new challenge in a tax-collection system is that amounts collected may not exactly match what the borrower owes. This is because not all sources of income require withholding, such as income that someone earns as a nonemployee (e.g., an Uber driver) or from an investment.[8] Our tax system addresses this issue with an annual reconciliation process where the filer calculates the exact amounts owed and sends in any underpayments. A loan system run through tax withholding will also minimize the likelihood that borrowers will underpay throughout the year. It will also reduce the likelihood of delinquencies and defaults. The low delinquency rate on income taxes suggests that payroll withholding could reduce unpaid loans. Specifically, the delinquency rate for unpaid individual taxes is less than 6%, while about 20% of borrowers whose loans have come due are in default on their federal student loans.[9]

Eliminating Interest and Rising Balances

Repaying through IBR can cause a borrower’s debt to increase even while he makes on-time monthly payments. This can occur if a borrower’s monthly income-based payments are less than the interest accruing on the debt. The borrower may eventually repay this interest when his income increases, or he may have it forgiven after 20 years if his income remains low relative to his debt. But in the meantime, borrowers must watch their outstanding balance rise each month, creating anxiety and a sense that they are not making progress on their obligations.

For example, a borrower whose loans accrue $200 in interest each month but whose income-based payments are only $100 sees his unpaid interest balance grow by $100 every month while his principal balance remains unchanged. It would appear to this borrower that he is going backward on his debt despite making the required payments. Of course, this borrower might have those unpaid amounts forgiven if there were a balance remaining after 20 years of payments. In present-value terms, he may not owe all of his rising balance. By design, the sum total of his expected future payments after inflation will not cover all of the principal and interest on the loan. But few people see their financial situation in present-value terms. To the borrower, it is unnerving to watch a debt grow for many years despite making payments.

Compare that with the ISA proposed here. Rather than track and display accrued interest that a borrower might have to pay or might have forgiven, the ISA does away with an explicit interest rate. Balances would never grow if payments are too low. Instead, borrowers always make progress toward their obligation because it is time-based. Each year that passes counts toward the 25-year term, regardless of how much they pay each month or year.

Simple and Targeted Benefits

While the ISA proposed here would not charge interest, most borrowers would end up paying more during the repayment term than they draw down from their line of credit. In other words, the ISA would effectively impose interest on the loan—but instead of a standard interest rate charged to all borrowers, the amount of effective interest (i.e., each dollar in excess of the amount borrowed) that any individual borrower ultimately pays varies with how much he earns during repayment. By design, borrowers with low earnings pay the lowest effective interest rates and those with higher earnings pay higher effective interest rates. Under the current IBR design, this is true only some of the time. Moreover, the IBR program allows some higher earners to pay, in effect, lower effective interest rates than borrowers with low earnings by providing generous loan-forgiveness terms to borrowers with large debts.

While total payments will vary more with income under the ISA, the income-based payments under ISA are still typically lower than what borrowers pay today on their federal student loans, including those using IBR. Several studies have shown that median annual student-loan payments over the past 15 years have ranged from 5% to 7% of annual income.[10] The proposed ISA results in payments equal to a maximum of 5% of income but only for students who borrow the maximum $50,000. (Payments are also based on a borrower’s individual income, not household income, which reduces the amount owed relative to the status quo, a topic discussed later in this paper.) Many students will borrow less than the maximum amount and therefore repay a smaller share of their income.

To balance out the effect of borrowers making lower payments than they do under the current system, the ISA requires that borrowers make payments for 25 years, versus the 20-year repayment period for a loan repaid through IBR. The ISA proposal stretches out the loan term to keep payments at a very low share of income, which helps minimize the amount by which a borrower could underpay each year through tax withholding. But even with longer payment terms, many borrowers will still receive a better deal than they do on average today. The final section of this paper discusses how policymakers could sunset tuition tax benefits as a logical offset to make ISA budget-neutral.

The repayment terms of the ISA create a transparent link between how much borrowers must pay monthly and how much they borrowed, and it does so while maintaining relatively low payments. Those who borrowed more simply pay a higher percentage of their income. There is no similar feature under the current IBR program; payments are always the same share of income, regardless of how much a student borrowed. That feature of the IBR program creates perverse incentives for students to borrow more, and it provides the largest benefits to those who borrow the most. Linking monthly payments to the amount that a student borrows, as the ISA design does, helps mitigate those perverse incentives.

Another feature of the ISA also helps target benefits better than the current IBR program. For some borrowers, the new ISA would result in higher total payments than what they pay under today’s student loan program. These would primarily be borrowers who end up earning higher incomes in repayment, particularly if they earn high incomes early in their repayment terms. These borrowers would pay more than what the current IBR program requires—or even what they pay on a fixed payment loan—because there would be no loan balance for a borrower to repay under this design other than the 1.75 cap (1.75 times the amount borrowed) on total payments.[11] Higher earners are likely to reach the cap well before the 25-year term is up, which means that their combined principal and interest payments will exceed those under any terms currently available in the federal loan program. In effect, they pay higher interest rates because their incomes are higher. The sidebar Loan Repayments: ISA Versus IBR illustrates how much two different borrowers would pay under the existing IBR program and the new ISA.

| Loan Repayments: ISA Versus IBR |

| A student repaying through IBR who borrowed $15,000 at 5% interest who has an initial adjusted gross income of $35,000 makes monthly payments of $140. If her income grows at 4% annually, the present value of her payments is $19,093 over the life of the loan (2.0% discount rate; includes $1,200 in-school interest accrual). Under the proposed ISA, she would make initial monthly payments of $44 and the present value of her payments is $16,404. The ISA is a better deal. Now consider a student with more debt and a higher income. This borrower has a $50,000 loan balance (at 5% interest) from attending graduate school. His income when he begins repaying is $60,000, with an 8% annual raise. Under IBR, his initial monthly payment is $348, and, in total, he will repay $68,238 on the loan, discounted to present value (includes $6,000 in-school interest accrual). With ISA, his initial monthly payment is lower, at $250, but his income grows rapidly and so does his monthly payment. He reaches the payment cap (1.75 times the amount borrowed) in his 16th year of repayment, well before the 25-year maximum repayment term, meaning that he does not need to make further payments. Even though he ended his repayment obligation before the 25-year term, he pays more overall on the ISA ($72,251, at present value) than if he had a loan under the current system and repaid in IBR ($68,238) because his income starts high and grows rapidly. |

That a borrower could pay more in total on an ISA than a loan is intentional. It helps offset the cost of providing reduced payments to borrowers with lower incomes. It also helps prevent middle- and upper-income borrowers from receiving large government subsidies in the form of loan forgiveness or low effective interest rates—benefits that they can receive now in the existing student loan program.

A Repayment Exemption for Low-Income Borrowers

Borrowers who use IBR with incomes at or below 150% of the federal poverty line (the poverty line is $12,490 for an individual) are exempt from making loan repayments. That exemption is also part of the payment calculation for all borrowers—in other words, payments are calculated on income above 150% of the federal poverty level. ISA payments would be calculated on a recipient’s first dollar of income. However, low-income borrowers would be exempt from making payments under two provisions. Tax filers who qualify for the Earned Income Tax Credit (EITC) would have their obligations reduced or canceled that year, and anyone who earns too little to file a federal return would also owe nothing that year.

These two provisions align the terms of the ISA with federal tax rates. Under the standard deduction in the tax code, individuals earning $12,000 or less are generally not required to file a tax return. (Even if they do file, they owe no federal income tax.) The ISA would exempt those borrowers from payments each year but would still give them credit for one year toward their 25 years of payments.

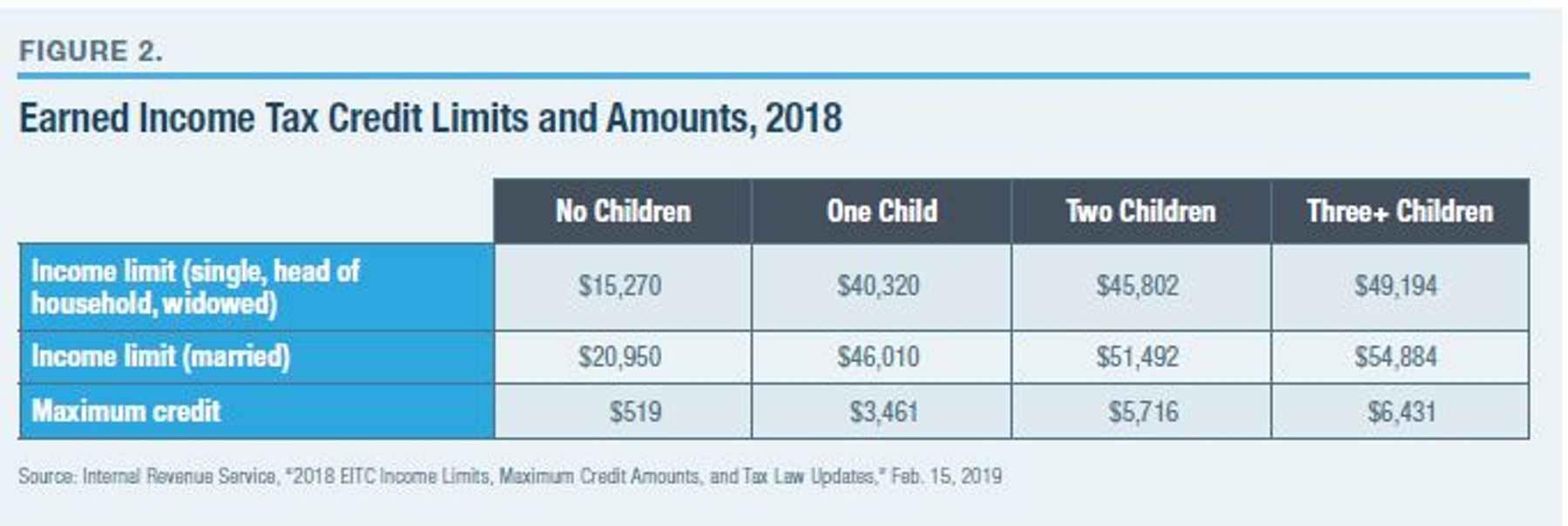

Another provision would provide even larger exemptions to those who receive EITC. This creates a means-tested, household-size-adjusted exemption that closely tracks the current exemption structure of IBR in the current loan program, which is 150% of federal poverty guidelines. EITC provides refundable credits based on a tax filer’s earned income and number of children, and it phases out as income increases. Figure 2 shows EITC income limits and maximum credit for 2018.

ISA recipients who qualify for EITC would have their annual ISA payments reduced by 15% of the value of EITC that they receive. This exemption would be halved for married households in which only one individual owes on the ISA to align with the rule that married tax filers make payments on half of household income (discussed later in this paper). Thus, an ISA recipient who earns more than the standard deduction for federal income taxes and therefore owes payments on the ISA that year could still end up having payments waived or reduced if he receives EITC (see sidebar Married Borrowers Receiving a Federal EITC). Borrowers would have this exemption figured on their tax returns during the annual filing process.

| Married Borrowers Receiving a Federal EITC |

| A couple with two children earns a combined income of $30,000. Only one member of the household has an ISA, which he used to finance $20,000 of his higher education. His payments on the ISA are therefore 2% of his income. But because he is married and files a joint tax return, the 2% is calculated on half of his household income. Therefore, he owes $300 for the year. This couple also qualifies for a federal EITC of $4,332, based on their income and number of children.* That means that the household member with the ISA qualifies for a reduction on the ISA—in this case, of $325 (which is 15% of the $4,332 EITC divided in half, to reflect the joint tax return). The resulting $325 exemption is more than the $300 that he would otherwise owe on the ISA for the year; therefore, he owes nothing on the obligation that year. He does, however, earn credit toward the 25 years that he must make payments. |

*Internal Revenue Service, “Earned Income Tax Credit (EITC) Assistant”

Borrowing Limits Reduce Risks for Students and Taxpayers

The proposed ISA would limit how much students can borrow. Without a loan limit, colleges and universities might charge prices that are out of line with the value that their credentials provide in the labor market. Loan limits also help reduce costs for taxpayers—costs that increase when loan forgiveness or an ISA is available.

Loan limits also help reduce the risk that borrowers might take on unaffordable levels of debt. With a $50,000 lifetime line-of-credit limit, a borrower’s payments can never exceed 5% of income (1% for each $10,000 borrowed). Lifting the cap to $100,000 would mean that borrowers who used the maximum would pay 10% of their income, even if they earned a low income that exceeded the exemption levels. In any case, the ISA limit is similar to current limits in the federal loan program for undergraduates.[12] Few undergraduates would see a reduction in their federal borrowing limits, including those enrolled in high-cost colleges.

The ISA would mean a more substantial change for graduate students, who can borrow up to the full cost of attendance through the federal loan program. Under the ISA proposal, they would be limited to any amount left in the $50,000 account that they did not use to finance their undergraduate education. Graduate borrowers are, however, good candidates for private financing as an alternative to federal funds. They have had the chance to establish earning and credit histories and hold four-year college degrees. About half of all students who earned a graduate or professional degree in the 2015–16 academic year borrowed more than $50,000 in federal loans for their undergraduate and graduate degrees combined.[13]

Additional Features of a Federal ISA

How to Treat Married Versus Single Borrowers

The federal income-tax system generally treats married borrowers as one unit, which complicates repayment using an ISA. Consider a married couple, both of whom work; but only one borrowed to finance an undergraduate degree. If the couple filed a joint return, the repayment would be based on their combined income. This is inconsistent with a key principle of an ISA, which is supposed to be linked to the return on the investment that it financed. Logically, only the borrower’s income should be used to repay it.

One solution would be to require tax filers to separate their incomes to figure the ISA obligation each year.[14] That approach is workable but adds complexity and paperwork to the repayment process and reduces the appeal of ISA relative to the current student loan program. The simplest solution for a married couple filing a joint return is to base the recipient’s ISA payments on half of the household’s adjusted gross income.

While this solution will create marriage bonuses and penalties, it is still preferable to a complicated process that assigns income to each tax filer on a joint return.[15] This solution is also easier than having ISA recipients file separate federal tax returns. Moreover, the marriage bonus that a 50-50 income split creates is not that much different from the income exemption in the existing IBR program, which is linked to federal poverty guidelines and increases with household size.[16] Any marriage penalty that the income split creates is unlikely to cost them more than the existing IBR program, where couples always repay on 100% of their combined income.

How Loan Payments Would Be Withheld

Here is how the withholding process would work. First, the IRS form W-4 that employees file with employers instructing them on how much to withhold for federal income taxes would be modified to incorporate payments on ISA. Currently, the form includes a step-by-step worksheet by which an employee calculates the number of personal allowances that he should claim, thereby determining and instructing how much the employer should withhold.[17] This process places the burden and responsibility of opting to have taxes withheld on the individual. Self-employed individuals would undertake a similar process when they file their estimated quarterly tax payments. Because the ISA is an annual obligation, recipients would begin making payments at the start of the first calendar year that begins after they leave school.[18]

To incorporate ISA payments into tax withholding, the W-4 worksheet would include a question about whether the filer has an ISA. If he does, the form would instruct him to make the necessary adjustment to the number of personal allowances that he claims (i.e., reduce them) or any additional amounts that he has withheld. Those adjustments would be calibrated to the amount of the ISA, and employers have no obligation to determine who has an ISA or how much to withhold. In fact, the employer would not know that an employee has an ISA. The W-4 form submitted to an employer does not indicate why an employee has opted for a particular number of personal allowances. Another advantage of this design is that the withheld funds would be commingled with tax collections and not differentiated until the borrower files his tax return. That creates a simple and streamlined repayment process for ISA holders and does not necessitate that the IRS implement a new and complicated system to collect and track the payments.

Importantly, borrowers with low loan balances may not need to adjust their withholding at all. An individual who used $10,000 of the ISA account, and therefore owes an additional 1% of his income on his withholding, would owe only $400 annually if his income were $40,000. He would simply receive a smaller refund when he files his return. Someone using the full $50,000, however, would owe an additional 5% of his income and would be instructed—through an annual statement from ED—to reduce the number of personal allowances that he claims accordingly or withhold a specified additional sum. Even if he did not, he would be unlikely to significantly under-withhold on his taxes and ISA payments. Payments on ISA are set at a low share of an individual’s income not only to make the annual obligation affordable but also to reduce the chance that an ISA recipient under-withholds by a large amount.[19]

Anyone with an ISA would need to reconcile the amount that he had withheld with the amount he owed. This would be done as part of the annual tax-filing process. The borrower’s payments and obligation (and any exemption tied to EITC) would be figured on a schedule and included as an additional line in the “Other Taxes” section on page 2 of IRS form 1040.[20] Overpayments would be included in any tax refund for the year. Underpayments would be treated as underpaid taxes. Up to a certain amount, filers would pay year-end underpayments without penalty as a lump sum when they file their income taxes. Amounts over the safe-harbor exemption for underpaid taxes would be subject to existing penalties and interest and the IRS collection processes.

A New Accountability Regime for Colleges

Eligibility criteria for students and institutions of higher education to participate in the new program would remain the same as they are under the current federal student loan system. Policymakers could, however, change those criteria, as the design of the ISA is not necessarily contingent on them. But an ISA will necessitate another change to the federal student loan program.

Because the proposed system will make loan defaults rare, even among low-income recipients, policymakers will need to replace the current accountability measure that disallows schools with high default rates (a proxy for low-quality or overpriced institutions) from participating in the student loan program with a new measure.

The best approach is a new quality floor for colleges and universities that would judge institutions (or programs at institutions) on the amount of funds that each cohort of students pays on the ISAs relative to the amount they drew down. If three years after entering repayment, a cohort has repaid less than 5% of the original disbursement (in nominal dollars), penalties would be triggered.[21] These penalties could be a form of risk-sharing payments that the school makes to the federal government, or revocation of a college’s eligibility to participate in the federal program.

Offsetting Higher Taxpayer Costs: Eliminating Duplicative Tax Benefits

ISA terms are likely to increase subsidies (i.e., reduce what students must pay) for many students relative to the current federal loan program. Those increases may not be fully offset by the cuts in benefits for higher earners and those with graduate school debts under ISA. To offset the potential net increase in costs to taxpayers, policymakers could reduce spending on other, related policies. Specifically, they could eliminate three tax benefits that individuals can currently claim for higher-education expenses that now total over $20 billion annually.[22] (See sidebar Tax Benefits for Higher Education: 2018.)

| Tax Benefits for Higher Education: 2018 |

| The American Opportunity Tax Credit (AOTC), available to students in their first four years of school, is limited to undergraduates. Students must be enrolled in a degree program at least half-time. Students (or their parents) may receive a tax credit of up to $2,500, or 100% of the first $2,000 in tuition in fees and 25% of the next $2,000. Up to $1,000 of this credit is refundable, meaning that the tax filer can claim it even if he has no tax liability to offset. Eligibility for the full AOTC is capped for single tax filers earning $80,000 ($160,000 for married filers). The Lifetime Learning Tax Credit allows tax filers to reduce their federal taxes up to $2,000. The credit is equal to 20% of the first $10,000 in tuition and fee expenses. Income limits are indexed to inflation and are set at $57,000 ($114,000 for married filers) for the full benefit. Graduate and undergraduate students may claim the benefit. The student loan interest deduction applies to borrowers who earn less than $80,000 ($160,000 if filing a joint tax return) in adjusted gross income. They can deduct up to $2,500 per year in the interest they paid on their student loans from their federal income taxes. This is an above-the-line deduction that can be claimed regardless of whether a tax filer itemizes or claims the standard deduction. Federal and private loans qualify for the benefit, but because most outstanding debt is federal, the benefit largely applies to those loans. |

Source: Internal Revenue Service, “Tax Benefits for Education,” Publication 970, Jan. 17, 2019

Eliminating these three tax benefits is a logical budget expenditure to offset any added cost of the new ISA plan. The ISA and the tax benefits all provide subsidies for college tuition figured on a family’s tax return.[23]

Conclusion

The ISA proposed in this paper is designed to improve on the federal student loan program without abandoning many of its existing features. That makes it less of a radical departure from the existing system than it might first seem and should increase its appeal.

The ISA maintains universal eligibility: all students may access the funds to pay for higher education and repay as a share of their income. It allows borrowers who earn low incomes after leaving school to make very low payments—or none at all, in some circumstances. And students never need to repay beyond a certain time period even if they have not paid back what they borrowed, as in the existing IBR program.

Some observers may criticize the ISA for maintaining these features. But they should consider how ISA does more to mitigate the unintended consequences of these features than does the current loan system and IBR program.

While the ISA maintains universal access to government funds, it breaks from the status quo to impose limits on how much students may borrow. Students who borrow more also must pay a higher share of their income, and higher-earning borrowers are likely to pay the government more than what they would pay on a student loan in today’s system. That is a further improvement over the status quo because these terms restrict generous loan-forgiveness benefits to those borrowers with persistently low income.

Despite these and other potential criticisms, it is hard to argue against some of the other advantages of the ISA. It is radically simpler than the existing system; the borrowing limits are universal and transparent; there are no interest rates or rising balances; payments are set in a straightforward manner and track income in real time without borrowers having to undertake an annual application process; and defaults and delinquencies will be rare, not rampant.

The federal student loan program is in desperate need of reform. In the past, policymakers have tried to improve the program in ways that mostly compounded its problems. They added new features and paperwork, created new eligibility restrictions and rules, and layered on more benefits, only to necessitate further reforms. The ISA proposed here takes a new approach. It strips the existing loan program down to its core components: universal access to capital, income-based payments, and a safety net. Past experience has shown that delivering these benefits through a loan program has failed borrowers and taxpayers. An ISA whose repayments are withheld from a borrower’s income taxes is far more likely to be successful.

Endnotes

About the Author

Jason Delisle is a resident fellow at the American Enterprise Institute, where his research focuses on higher education financing, student loan programs, and the federal budget. He has served as an analyst for the U.S. Senate Committee on the Budget and as director of the Federal Education Budget Project at New America, where he worked to improve the quality of public information on federal funding for education and the support of well-targeted federal education policies. He was also an informal adviser on higher education reform for Jeb Bush’s 2016 presidential campaign. Delisle has written for a variety of publications, including Bloomberg View, Wall Street Journal, and Washington Post. He has also appeared on numerous national television and radio programs, including Fox Business, National Public Radio, and the “PBS NewsHour.” Delisle holds a master’s degree in public policy from George Washington University and a bachelor’s degree in government from Lawrence University.

This report was written as a part of MI's Solutions from Beyond the Beltway series

Photo: William_Potter / iStock / Getty Images Plus

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).