How Higher Interest Rates Could Push Washington Toward a Federal Debt Crisis

Photo: f11photo/iStock

Today’s trendy economic argument asserts that the current debt-to-GDP ratio of 100% has not harmed the economy, and therefore Congress can easily afford large new government expansions. But that argument has two fatal flaws. First, it fails to acknowledge that over the next few decades—even without new legislation—the debt is already projected to reach levels that even debt doves would likely consider unsustainable. Second, this argument assumes that interest rates will forever remain near today’s low levels, thus minimizing Washington’s cost of servicing this debt. However, economic trends rarely remain linear indefinitely, and interest-rate movements have rarely followed forecaster projections. Indeed, several realistic economic scenarios could easily push interest rates back up to 4%–5% within a few decades—which would coincide with a projected debt surge to greatly increase federal budget interest costs. Debt doves have no backup plan for this possibility. Policymakers should now enact reforms that scale back the escalating long-term debt projections in order to limit the federal government’s risk exposure to a fiscal crisis.

Introduction

Congress and the White House are engaging in the largest borrow-and-spending spree since World War II. The $3 trillion legislative response to the pandemic was largely justified but nonetheless staggering in its size: at 15% of GDP, it exceeded the 1930s New Deal response to the Great Depression. Yet this deficit spending was just a warm-up to President Biden and Congress’s even more ambitious agenda. They have already enacted a $1.9 trillion stimulus bill and a $550 billion infrastructure bill, and adding proposals like Build Back Better ($3 trillion in deficits assuming Congress repeals the fake expiration dates), [1] and new discretionary spending ($1 trillion over the decade) would add up to $6.5 trillion in additional ten-year debt from one year of legislation. This is quadruple the cost of the 2017 tax cuts, and it exceeds 20 years of domestic and international costs related to the war on terrorism. Nor are Democrats finished yet, as President Biden still has campaign pledges related to health care, Social Security, education, and other areas that would add an additional $3 trillion in debt. [2]

This deficit spending would take place on top of growing baseline deficits and push the national debt—less than $17 trillion before the pandemic—past $44 trillion a decade from now. And the debt would continue growing thereafter as the result of $112 trillion in 30-year baseline deficits, driven largely by deepening Social Security and Medicare shortfalls. [3] In other words, the U.S. government is in the early stages of what is projected to be the largest government debt binge in world history.

Yet there has been no widespread backlash. There is no tea party movement, or Ross Perot– style political candidate warning America about unrestrained red ink. Congressional Republicans have gone largely silent on this historic borrowing spree, and polling by the Pew Research Center shows the public’s budget deficit concerns plummeting over the past decade. [4] Financial markets have shrugged off this surging debt. Most surprisingly, even economists have heralded this new era of red ink. Leading mainstream Democratic economists Jason Furman and Lawrence Summers have written: “Washington should end its debt obsession,” [5] while Trump economic advisor and noted conservative tax cutter Lawrence Kudlow has called the debt “quite manageable” and not “a huge problem right now at all.” [6]

This newfound acceptance of surging government debt is largely based on two highly questionable assumptions.

First, economists have asserted that fiscal consolidation is unnecessary because Washington’s current debt level of 100% of GDP has not proved unaffordable or economically damaging. Leading economists have asserted that expensive new fiscal expansions are justified until the debt reaches 150% of GDP. [7] Yet this framework fails to take into account that Washington is already projected by the Congressional Budget Office (CBO) to run $112 trillion in additional baseline deficits over the next three decades, which will push the debt past 200% of GDP. At that point, annual deficits are projected to top 13% of the economy (the equivalent of nearly $3 trillion today), and interest payments on the debt would be the largest federal expenditure, consuming nearly half of all tax revenues. [8] Adding all of President Biden’s budget proposals would push the debt past 250% of the economy in three decades. And instead of leveling off, the baseline debt would continue expanding by 80% of GDP per decade. In short, the baseline debt is already projected to grow to unsustainable levels even before any new proposals are enacted.

The second questionable assumption that the debt doves make is that today’s low interest rates paid on this debt will continue forever. The average interest rate paid on the national debt has fallen from 8.4% to 1.4% since 1990. [9] This decline was not forecast by economists, and many disagree on its specific cause. Yet many economic commentators have expressed an unshakable confidence that relatively low interest rates will essentially continue forever. If they are wrong, the combustible combination of surging debt and rising interest rates at any point in the future would risk a debt crisis. Even interest rates of 5% could push the national debt toward 300% of GDP within three decades, if paired with modest new fiscal expansions in the meantime. Both the poor historical record of economic forecasters as well as the tendency of economic variables like interest rates to fluctuate over the long term should give pause to policymakers, taxpayers, and economists when examining Washington’s rapidly rising debt projections.

The purpose of this report is to more deeply examine the threat that higher interest rates would pose on Washington’s long-term fiscal sustainability. First, it examines the causes of the post- 1990 decline in interest rates and the factors likely to push interest rates upward over the next few decades. Next, it analyzes Washington’s steeply rising debt levels over the next several decades and how rising interest rates risk pushing government interest costs, annual budget deficits, and total government debt to unsustainable levels. The report concludes by calling on lawmakers to gradually pare back these baseline deficits and thus limit the likelihood of a future debt crisis.

I. The Interest-Rate Outlook

Nominal interest rates are the sum of the demanded real rate of return and a premium to account for inflation risk. After remaining steady during the 1950s through the late 1960s, interest rates accelerated in the 1970s but fell below zero in real terms because the actual inflation rates far exceeded the expected inflation rates that were built in to the nominal rates (see Figure 1). By the early 1980s, investors had learned their lesson and began demanding exorbitant nominal interest rates to compensate for high expected inflation and a premium to account for inflation risk. The Federal Reserve’s subsequent taming of inflation left 1980s real interest rates at historically high levels. A key lesson is that low and stable interest rates require market confidence in low inflation rates.

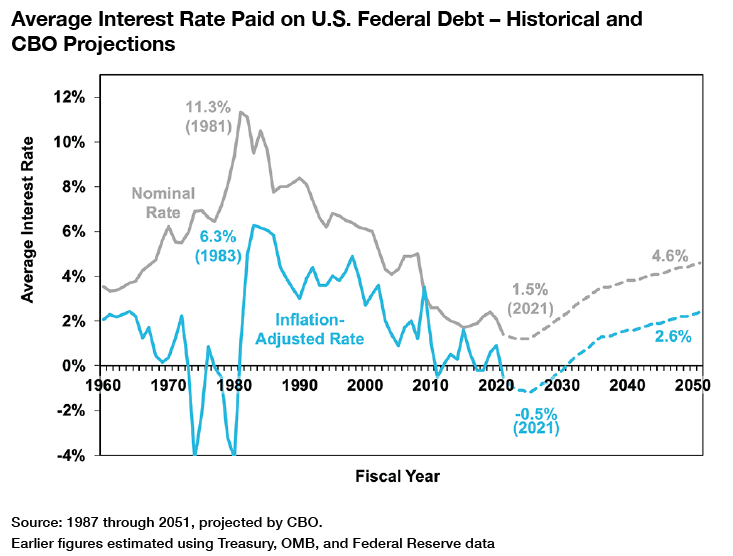

Figure 1

After the higher real and nominal rates of the 1980s, the federal government by 1990 had paid an 8.4% average interest rate on the debt held by the public. The average rate had gradually declined to 4.9% by 2006, before the housing collapse and financial crisis dropped rates further, to approximately 2.0%, where they remained until a recession and a wave of short-term pandemic borrowing decreased average debt maturities and dropped the average federal rate to its current level of 1.4%. [10] Although the Treasury has occasionally altered the average maturity of its debt, the average interest rate has closely tracked the average rate on the 10-year Treasury bond. AAA corporate bonds and mortgage rates have followed a similar path.

A key question is, what caused this steep 30-year decline in interest rates? Private economic forecasters as well as federal government forecasts produced by CBO and the White House Office of Management and Budget (OMB) have consistently failed to predict the interest-rate decline and, in fact, regularly predicted that rates would increase. In hindsight, economists have converged on some combination of several factors to explain the three-decade decline in interest rates: [11]

- Demographics. The 74 million baby boomers began saving more for retirement in their 40s, 50s, and early 60s. At the same time, the population growth of younger adults in their prime borrowing years slowed down. Additionally, the general population growth slowdown in both the U.S. and abroad likely reduced productivity rates, incentives for research and development, and the need for expensive new investments to equip this smaller workforce.

- Declining Productivity. The surprising decline in productivity, particularly since 2006, has reduced interest rates by reducing demand to borrow now against future (assumed) wealth, as well as by reducing the marginal product of capital and demand for new investments in the economy. A related possible factor has been the reduced need for physical capital investments brought on by the technology revolution (i.e., more Facebooks, fewer huge manufacturing factories) and better management techniques, helping companies become more efficient with existing capital.

- Global Savings Glut. Former Federal Reserve Chairman Ben Bernanke has observed that global savings and investment soared in the early 2000s, collapsed after the financial crisis of 2007–09, and then resumed growth. [12] The decline in interest rates suggests that excess savings—rather than growing demand for investments—fueled this growth. However, much of the additional savings came from Asia and oil-exporting countries, and their glut seems to be slowing in recent years. [13]

- Global Flight to Safety. Historic stock- and financial-market crashes in 2000, 2007–09, and again in early 2020 drove savers in the U.S. and abroad to seek out the safety and predictability (albeit with low returns) of U.S. Treasury bonds and related investments, such as AAA corporate bonds. Investment safety has been especially important for baby boomers approaching retirement and international investors worried about global market instability.

- Global Economic Trends. The increasingly interconnected global economy has caused interest rates across countries to converge more than ever before. And the cross-nation replication of factors such as an aging population, global savings, and declining productivity has reinforced these interest-rate declines in most advanced economies.

- Inflation Anchoring and Federal Reserve Policy. As stated above, central banks in the U.S. and abroad have taken a stronger, and more consistent, push for low inflation and monetary stability since the 1980s, which has reduced the inflation-risk premium in interest rates. Over the past 13 years, aggressive low-interest-rate policies and quantitative easing have further pushed short-term interest rates downward.

- Private-Sector Deleveraging. After the 2007–09 financial crisis, many overextended families and businesses took steps to minimize their debt exposure. This has meant households increasing their savings and paying down debt, businesses shoring up their balance sheets, and lenders imposing tighter loan requirements. This deleveraging increased savings and reduced consumption and borrowing. It was also broadly disinflationary, further contributing to lower nominal interest rates.

Government Debt Still Raises Interest Rates

This three-decade reduction in interest rates may create the impression that rising government debt no longer puts upward pressure on interest rates. Standard economic theory has long held that government borrowing reduces the amount of savings available for the private sector to borrow and invest—which, in turn, raises the price of savings, or the interest rate. However, U.S. interest rates fell during a period in which the federal debt held by the public increased from 40% to 100% of GDP. Does that disprove the link between government debt and interest rates?

Extensive economic research maintains that the link still exists. In 2003 and again in 2007, Federal Reserve economist Thomas Laubach determined that, all else equal, a 1-percentage-point increase in the debt-to-GDP ratio increases interest rates by three or four basis points. [14] In 2004, economists Eric Engen and Glenn Hubbard calculated that “an increase in government debt equivalent to 1% of GDP would likely increase the real interest rate by about two to three basis points.” [15] More recently, a 2019 CBO study coauthored by Edward Gamber and John Seliski employed methodologies similar to those of Laubach and Engen/Hubbard to find a persistent two- to three-basis-point effect. [16] A 2019 analysis by current Biden administration economist Ernie Tedeschi found that “each percentage point increase in debt-to-GDP raises the 10-year yield by 4.2 basis points, all else equal.” [17]

This analysis suggests that the post-1990 increase in the federal debt ratio from 40% to 100% of GDP should have raised interest rates by 1.2–2.4 percentage points. Instead, real interest rates fell by 2.5 points. Squaring this circle lies in the final words of the previous paragraph: “all else equal.” The positive link between government debt and interest rates has not been eliminated but rather offset by other economic factors reducing interest rates. Jason Furman and Lawrence Summers concede that interest rates have been pushed upward by factors such as rising government debt and lower tax rates on capital investment. [18] So why have overall interest rates fallen? Because, citing earlier estimates by Summers and Lukasz Rachel, those offsetting factors reducing real interest rates across nations “declined by about 700 basis points.” [19] Tedeschi’s analysis also finds that many of the interest rate–dampening factors detailed above simply overwhelmed the upward pressure on interest rates caused by rising government borrowing.

Will Rising Debt’s Interest-Rate Effects Continue to Be Canceled Out?

It is tempting to conclude that—even if rising debt pushes interest rates upward—those offsetting factors will continue to hold down interest rates, liberating lawmakers to borrow without worry. Instead, these offsetting factors should be a source of caution because there is no guarantee that they will last. The federal government has much more long-term control over rising federal debt—which raises interest rates—than it does over the broader economic and global trends that have recently pushed interest rates downward. [20] These broader interest-rate trends (and resulting lower budget interest costs) have served as a substantial, accidental, and possibly temporary subsidy to heavy-borrowing federal lawmakers. It is dangerous to assume that these offsetting trends will continue forever.

Here’s a key point. Assuming that each percentage-point increase in the debt continues to raise interest rates by 3 basis points, the projected 100% debt-to-GDP increase over the next three decades should, all else equal, push interest rates up by 3 percentage points. [21] To maintain today’s low interest rates, therefore, it would not be enough for those offsetting factors to remain constant; they would have to accelerate even further, in order to drive an additional 3 percentage- point interest-rate decline.

An analogy would be a football team that managed to improve its overall win–loss record over several seasons—despite a rapidly worsening defense—because its offense kept improving enough to barely outscore its opponents. Claiming that the wins prove that defense no longer matters, or should be allowed to continue declining on the assumption that the offense will simply continue to improve even faster, is obviously unwise.

Other Factors May Also Raise Interest Rates

Is it wise to assume that offsetting factors can accelerate enough to overcome the factors that will push interest rates higher in the future? Should we assume, for example, that productivity growth rates will continue to fall closer to zero? Or that the global savings glut accelerates? The Federal Reserve already faces a zero lower bound on short-term interest rates. It is not clear from where such an additional 3-percentage-point decline in the offsetting factors will come.

In fact, it is quite plausible that some of the factors that have reduced interest rates in previous decades could begin to reverse and nudge interest rates even further upward.

- Demographics. The large population of baby boomers who aggressively saved for retirement in their 40s, 50s, and early 60s have begun moving into retirement, where they will be expected to begin drawing down those savings. As will be discussed later, this is already happening in Japan, which has an older population than the U.S. [22]

- Productivity. The rapid rise of computing technology represents the largest technological revolution in a century. Productivity initially soared in the 1990s as the technology became widespread, and has since lagged. This nonlinear productivity growth resulting from new technology should not be surprising, as the world continues to innovate, adapt, and learn new ways to apply these new resources. However, as long as research and development continue, the long-term productivity outlook should be positive. Relatedly, the contention that the world simply needs less capital investment is also questionable. Emerging economies are growing, and their expanded middle classes will require capital investments. Even in the U.S., new technologies will require regular upgrades, and even a gradual shift from fossil fuels to green technology will require significant new capital investments. Nor are traditional physical infrastructure needs going away.

- Other Transitory Savings Factors. The global savings glut seems to have peaked in the mid- 2010s and is slowly receding. [23] The rate of private-sector deleveraging must also eventually slow down and stabilize.

- Flight to Safety Weakens. Low interest rates on Treasury securities could induce borrowers to chase stronger returns elsewhere, such as the stock market or emerging economies.

- Federal Reserve Policy. The Federal Reserve could be expected to raise short-term interest rates over time because of faster economic growth or any uptick in inflation. On the flip side, if central banks weaken their commitment to containing inflation, the resulting price volatility could induce borrowers to demand a higher inflation-risk premium. [24] Rising inflation rates can be difficult to reverse and can raise long-term market expectations of inflation. Such developments would reduce the “flight to safety” appeal of holding Treasury bonds.

- “Unknown Unknowns.” The past two decades have included a major market crash, a housing crash and deep recession, and a global pandemic. Markets have long underestimated the probability of tail risks and “black swan events” that can roil markets. Wars, financial crises, pandemics, environmental catastrophes, cyberterrorism, or any number of unanticipated events can drive the economy in unanticipated directions, including raising or lowering interest rates.

Any of the variables above could conceivably push interest rates in either direction. However, it is worth reiterating that, as long as the projected doubling of the national debt (as a share of the economy) is likely to push interest rates upward by approximately 3 percentage points, the offsetting factors above would need to continue pushing interest rates downward by an additional 3 percentage points to maintain current interest rates.

Some of the factors affecting interest rates—Federal Reserve policy, quantitative easing, private- sector deleveraging, and the dampening effect of the pandemic recession—are likely transitory. Others, such as productivity, demographics, and the demand for capital investment, are longer-term structural factors—but there is no guarantee that they will continue on their current trends indefinitely.

According to the aforementioned economist Thomas Laubach, in an economy operating at its potential and with stable inflation rates, interest rates should revert to a natural equilibrium level (known as the R-star) that is largely related to output growth. Laubach noted that the R-star dropped over the past few decades because of changes in productivity, demographics, and global factors. If those variables reverse, so can the R-star. [25]

Who Will Supply the Lending?

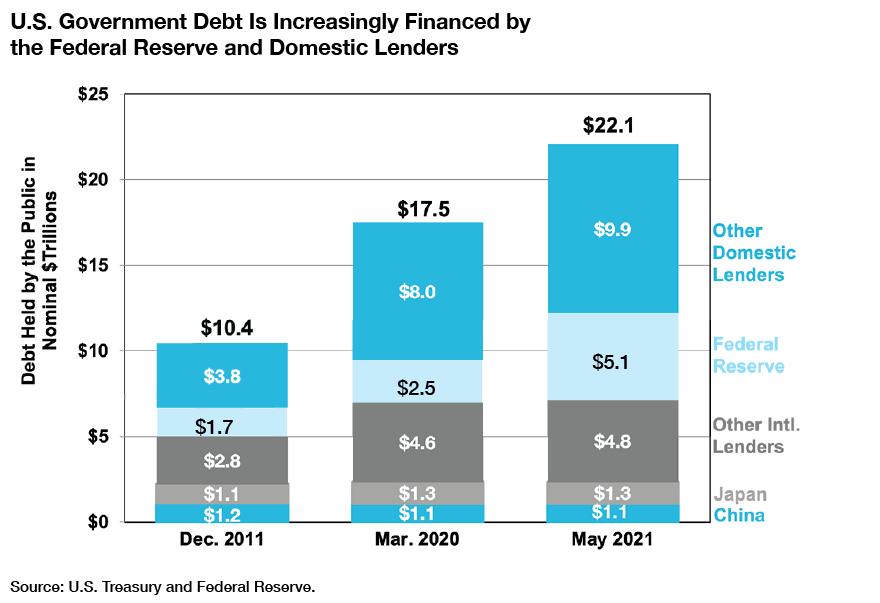

The national debt held by the public—currently $23 trillion—is projected to grow by an additional $112 trillion over the next 30 years, even if no additional spending programs or tax cuts are enacted. Who will supply this large amount of lending? China and Japan have financed just 1% of all federal borrowing over the past decade. Specifically, Figure 2 shows that, during a period in which the debt held by the public soared from $10.4 trillion to $22.1 trillion, the amount of combined debt held by China and Japan merely inched up from $2.2 trillion to $2.3 trillion. [26] It is highly unlikely that either nation has the capacity or willingness to take on a significant portion of the coming $112 trillion debt deluge. Other nations (led by the United Kingdom, Ireland, Luxembourg, and Switzerland) have collectively increased their U.S. Treasury holdings during this time, from $2.8 trillion to $4.8 trillion. Even quadrupling those holdings would still leave nearly $100 trillion in leftover debt to be financed elsewhere.

Figure 2

In short, the U.S. will be forced to fund the overwhelming majority of this debt domestically. Advocates of Modern Monetary Theory suggest that the Federal Reserve can essentially monetize a large portion of this debt (as well as the cost of unprecedented additional spending increases). Indeed, the Fed has indirectly financed much of the recent pandemic budget deficits, pushing its total Treasury holdings past $5 trillion. However, many analysts expect the Fed to eventually reduce its Treasury holdings and end its quantitative easing policies. [27] Even if the Federal Reserve remains somewhat dovish, there are no indications that it would consider financing any significant portion of the $112 trillion borrowing spree, as doing so would almost certainly trigger rapid inflation (as discussed later in this report). [28]

That leaves other domestic lenders, such as retirement funds, mutual funds, other federal agencies, state and local governments, and savings bonds. Can American savers and investors finance $100 trillion in federal borrowing over 30 years? Possibly, but it will be a heavy lift, given that they currently hold just $10 trillion in Treasury assets. It is entirely plausible that the Treasury will need to offer higher interest rates to induce this level of lending.

Future Uncertainty Requires Humility

Much of the current economic research, news coverage, and national debate on fiscal policy simply takes as a given that interest rates will remain low forever, regardless of federal policy and economic events. The only remaining question is how much new debt Washington should add in order to take advantage of these low rates. However, there is never any guarantee that current economic trends will forever move in the present direction. Virtually all economic variables fluctuate over time; yet most shifts are missed by lazy forecasts that simply extrapolate current trends forward.

More specifically, the classic phrase “often wrong, never in doubt” is only a slight exaggeration to describe the fields of economic forecasting and, more broadly, economic commentary. Macroeconomic variables such as economic growth, productivity, inflation, and interest rates have proved difficult to predict, even in the short term. Unpredictability is to be expected in a country of 330 million people with a $22 trillion economy, which is also influenced by an interconnected global economy consisting of nearly 8 billion people. Throughout 2021, members of the Federal Reserve’s Federal Open Market Committee (FOMC) repeatedly missed the mark on inflation projections for the rest of the year by a full 3 percentage points. [29] Most economic forecasters have consistently failed to predict interest-rate movements for the past 30 years. Yet rather than humbly accept economic uncertainty, many forecasters now insist that this time, they have improved their models—and this time, they can predict macroeconomic variables even decades in advance. David Card, a corecipient of the 2021 Nobel Prize in economics, has criticized economists for the “unbelievable certainty that they know what they are talking about, when the actual reality is they do not really know.” [30]

History is filled with examples of confident, consensus economic predictions that were shredded by subsequent events. In 1929, legendary Yale economist Irving Fisher was quoted in the New York Times that “stock prices have reached what looks like a permanently high plateau”— right before the crash that precipitated the Great Depression. Even after the crash, the president of the Equitable Trust Company declared: “I have no fear of another comparable decline.” [31] Many economists predicted that the end of the World War II buildup would sink the economy back into another depression. Then, in the 1960s, a new Keynesian economic consensus confidently declared victory over the business cycle, leaving only a Phillips-curve menu of inflation versus unemployment—which was then followed by a decade of painful recessions and (supposedly impossible) periods of simultaneous high inflation and unemployment. [32] In the late 1990s, economists and market experts predicted that the tech-driven economic boom would bring a new era of economic growth and soaring stock markets—until the dotcom bubble burst and the tech-heavy Nasdaq market index fell by 78%, initiating a new era of sluggish economic growth. Economic forecasters and an entire industry of Wall Street investment experts completely failed to foresee the impending collapse of the housing bubble and its ripple effects on mortgage-backed securities and broader markets, resulting in a historic recession and collapse of Wall Street investment-bank balance sheets. In early 2000, Lehman Brothers chief investment strategist Jeffrey Applegate was reportedly telling clients to “throw out everything they had learned in the last 20 to 30 years about how markets and business cycles operate,” and invest on the expectation “that the unprecedented continues to happen.” [33] Before the decade had ended, Applegate’s own 161-year-old investment bank—the fourth largest in the country—filed for the largest bankruptcy in U.S. history, due to its overextended investments.

Economic forecasters have been consistently wrong about interest rates, in particular, for the past 50 years. The steep rise in nominal interest rates during the 1970s was largely unanticipated, and yet still often failed to keep pace with inflation. The disinflation of the 1980s and subsequent softening of nominal interest rates were also unanticipated. For the past three decades, economic forecasters, including CBO, have repeatedly overestimated future interest rates. Jason Furman and Lawrence Summers write that, over this period, “long-term forecasts . . . entirely missed the large decline in real interest rates.” [34] A 2015 report produced by the White House Council of Economic Advisers adds: “Between 1984 and 2012, CBO, private-sector forecasters, and the Administration all systematically overestimated the path of nominal interest rates just two years into the future.” [35] A 2019 report shows that these interest-rate-forecasting errors have continued. [36] Hoover Institution economist John Cochrane stated:

Debt crises are like the Spanish Inquisition; no one expects them to come. If you knew they were coming, they would have already happened. Interest rates, in fact, have never [been accurately] forecast. [Economic forecasters] didn’t forecast inflation in the 1970s, and they didn’t forecast the disinflation in the 1980s. So interest rates didn’t forecast the Greek debt crisis. Interest rates didn’t forecast that Lehman was going to go under. [37]

But the current leaders of the same economics profession and Wall Street firms that have consistently failed to predict even short-term economic variables for the past half-century now express supreme, airtight confidence that they can predict the yield on the 10-year Treasury bond in the year 2050 (specifically, that it will be much lower than the rates that prevailed as recently as 2008). Economists claim that they have learned from past forecasting errors, built new and updated economic models, and now can finally predict inflation and interest-rate trends decades in advance.

Such continued overconfidence in the face of repeated failures is both arrogant and foolish. Economics is not a hard science. Even the most sophisticated economic models are only as good as the assumptions built in by imperfect economists (which are often just extrapolating the recent past forward). And no set of mathematical equations and causal relationships can accurately predict future innovations, government policies, external economic shocks, or the daily economic behavior of 330 million Americans and 8 billion people on earth. In reality, no one has any idea which interest rates will prevail in 5, 10, 30, or 50 years.

Of course, some features of our economic future can be predicted relatively safely—such as that 74 million baby boomers are now retiring into Social Security and Medicare programs with preset benefit formulas that, unlike interest rates, are directly controlled by Congress. Over the next three decades, the costs of these programs will exceed their dedicated revenues (such as payroll taxes and senior premiums) by approximately $20 trillion for Social Security and $47 trillion for Medicare. [38]

Given the comparative certainty of these large federal budget deficits—which will make budget interest costs extraordinarily sensitive to even small interest-rate changes—it would be reckless to commit to decades of permanent new debt in the hope that the interest rate paid on this debt never again reaches 4% or 5%. Such levels would not even represent historical outliers; they are well within the normal range of fluctuations over the past half-century. Furthermore, the economists who remain married to their forecasting models have offered no fiscal backup plan if they happen to be wrong about interest rates. Prudence demands economic humility, as well as setting Washington’s finances on a course that can survive normally fluctuating economic variables.

II. The Fiscal Consequences of Rising Interest Rates

We have already seen that there is no guarantee that interest rates will remain low forever. The next question is, how much would higher interest rates cost the federal government? Before examining this issue, two caveats are in order.

First, in contrast to a family buying a home, the Treasury does not lock in 30-year interest rates when borrowing. Instead, Washington overwhelmingly relies on short-term borrowing, with an average maturity of 69 months. Consequently, if interest rates rise at any point in the future, nearly the entire national debt will roll over into those higher rates within a decade.

Second, different economic developments that raise interest rates (and federal budget interest costs) can also produce second-order effects on the federal budget—both positive and negative. For example, higher inflation rates can affect spending and revenue policies differently, leading to larger or smaller budget deficits. A reduction in savings rates or tighter monetary policy can reduce investment spending, capital formation, and, ultimately, economic growth, thereby worsening budget deficits. Most important, higher productivity rates, which raise interest rates, would also bring in significantly higher tax revenues and curtail the usage of antipoverty programs, ultimately counteracting the added budget interest costs. Of course, increased productivity is just one among many ways in which interest rates could rise—rising debt, demographics, Federal Reserve policy, a slowdown in private deleveraging, and a slowdown of the global savings glut are also likely candidates—so there is no guarantee that the costs of higher interest rates will coincide with the budgetary benefits of productivity increases.

Because these second-order budgetary effects can be positive or negative, depending on the specific set of economic developments that also affect interest rates, the analysis below makes no assumptions of those effects.

Soaring Debt Projections [39]

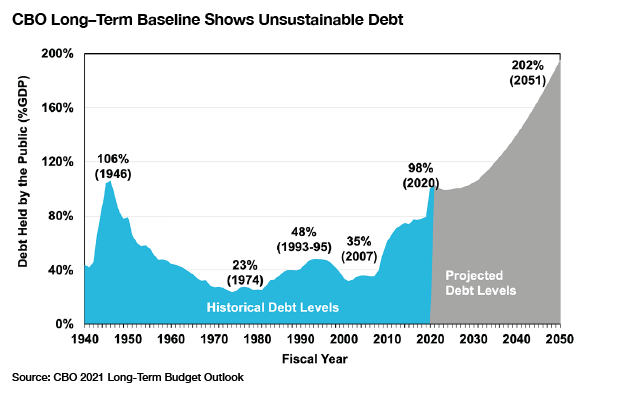

CBO projected in March 2021 that the national debt held by the public will rise from 100% to 202% of GDP over the next three decades (see Figure 3). This “current law baseline” represents only the cost of continuing current programs and policies. Thus, the baseline assumes the scheduled expiration of all pandemic relief spending and the temporary provisions of the 2017 tax cuts. It also assumes that Congress enacts no additional tax cuts or spending expansions.

In short, a 202% debt-to-GDP ratio is the rosy scenario—but even that is unsustainable. Annual budget deficits would gradually rise to 13.3% of GDP over three decades (the current equivalent of $3 trillion per year) even with (assumed) peace and prosperity. These rising annual deficits would mean that, beyond the next three decades, the debt would only continue growing, by an additional 80% of GDP in the fourth decade and more thereafter (with annual interest costs surging beyond 5.8% of GDP per decade at that point). This is fundamentally different from Japan’s large debt, which was built more gradually, with smaller annual deficits, and then began to level off before the pandemic.

Figure 3

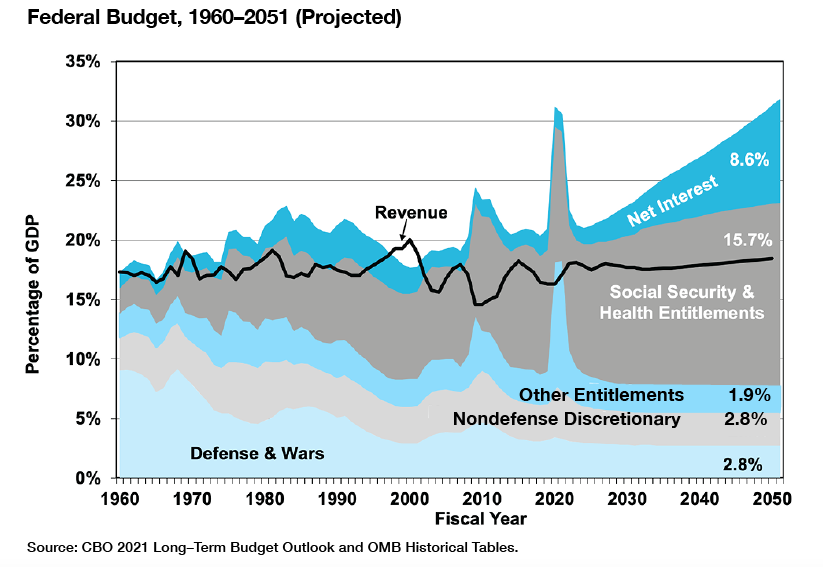

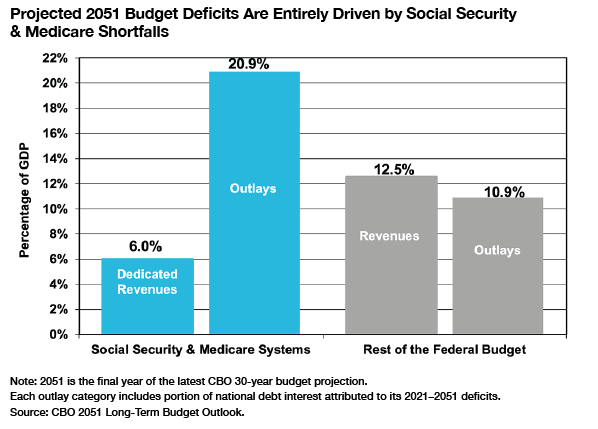

The driver of this debt is no mystery. The Social Security and Medicare systems—which will continue to collect 6% of GDP in payroll taxes and other dedicated revenues—will see their spending levels rise from 7.9% to 12.6% of GDP between 2019 and 2051. These rising costs will, in turn, deepen budget deficits that push net interest costs on the debt from 1.6% to 8.6% of the economy. The rest of the budget is entirely balanced over the long term (see Figures 4 and 5).

Specifically, CBO projects that tax revenues—historically 17.3% of GDP—will gradually rise to 18.5% over the next three decades. And federal spending outside of Social Security, Medicare, and net interest is projected to fall from 11.3% to 10.5% of GDP over this period. Thus, virtually the entire fiscal deterioration comes from Social Security and Medicare costs.

Figure 4

Figure 5

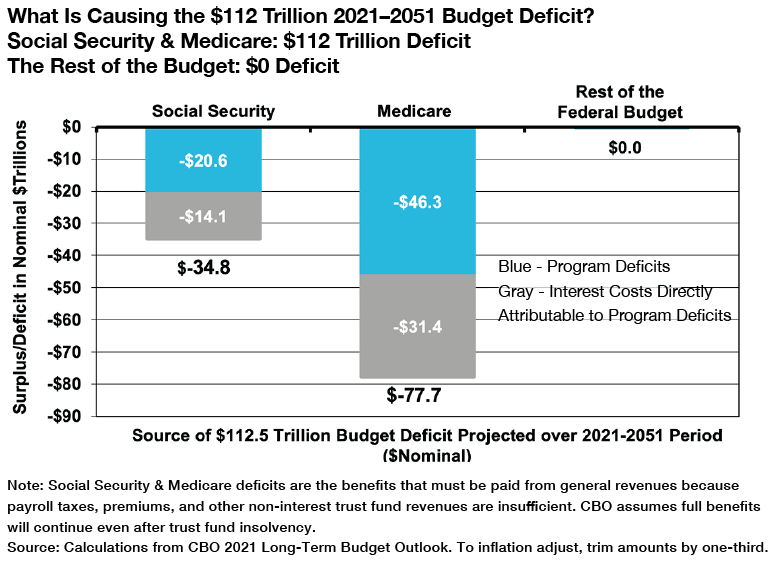

This can also be expressed in nominal dollars. Figure 6 shows that, over the next 30 years, Washington is projected to run $112 trillion in budget deficits. Because Social Security and Medicare’s payroll taxes and premiums are insufficient to finance all promised benefits, these systems will require steeply escalating general revenue transfers that total $67 trillion over 30 years. And because nearly that entire amount will have to be borrowed, it will bring $45 trillion in new interest costs on the national debt. The combined $112 trillion shortfall of the Social Security and Medicare systems (including interest costs) covers the entire 30-year projected budget deficit. The rest of the projected budget is balanced over 30 years, with initial deficits eventually transforming into surpluses.

Figure 6

It is tempting to dismiss these long-term debt projections as vague theoretical guesses. And certainly, a lot can happen in the meantime. However, the rising Social Security and Medicare costs reflect specific, preset spending commitments enacted into law. The existence of 74 million retiring baby boomers is not a theoretical projection like future interest rates. And these individuals’ Social Security and Medicare benefits and payments are already set in law. Nor do these projections significantly depend on future economic variables such as growth, inflation, or poverty rates. Changes in health-care cost trends or demographic mortality may slightly alter Social Security and Medicare costs but not enough to fundamentally cancel out the resulting debt trajectory. These escalating Social Security and Medicare costs—and the resulting debt projections—cannot simply be wished away.

Nor are there easy economic solutions to long-term deficits. While rapid inflation may reduce the real cost of the current $23 trillion national debt, investors would, in turn, require higher nominal interest rates that significantly raise the cost of the next $112 trillion in projected borrowing over three decades. As for economic growth, even replacing CBO’s 1.1% projected annual growth in total factor productivity (TFP) with the 1.7% rate that prevailed between 1992 and 2007 would show a first-order effect of $30 trillion in added revenues and $10 trillion in interest savings over three decades. [40] However, some of those savings would be pared back by the budgetary costs of (likely) higher interest rates on the national debt, increased inflation, and more generous Social Security benefits from faster wage growth. Similarly, alternative CBO estimates that aggressively (and indefinitely) raise annual productivity growth rates by 0.5 percentage points above the baseline would still leave a debt of 156% of GDP by 2051. [41] Faster economic growth would obviously be helpful, but it cannot fully outpace the growth of Social Security and Medicare costs or avert the need for reform.

Rising Interest Rates Drastically Worsen the Debt

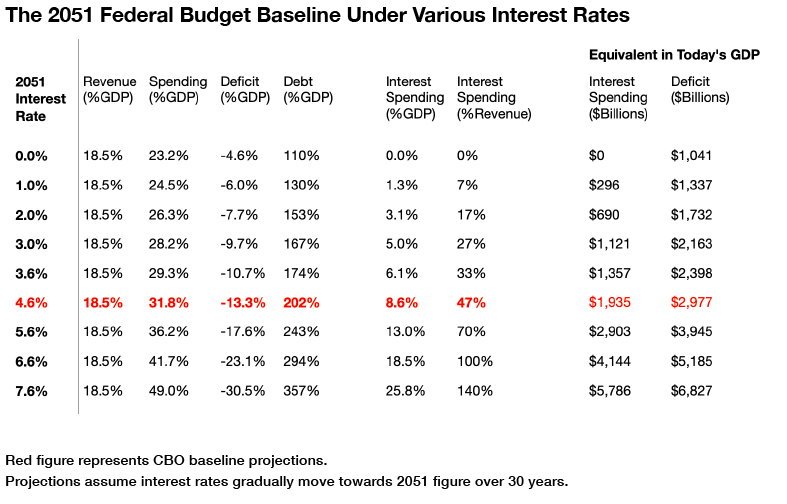

The CBO baseline above assumes that the average interest rate paid on the federal debt gradually rises from 2.4% to 4.6% between 2019 and 2051.42 CBO begins by using the decade from 1995 to 2004 as a neutral baseline period of economic stability, with low inflation, no major recessions, and neutral monetary policy. During that time, the average interest rate paid on the federal debt was 5.8%. From there, CBO weighs the impact of subsequent interest-rate-dampening effects that may be sustained long-term (such as lower productivity growth compared with that period, an investor flight to safety, and slower labor-force growth) with interest-rate-rising effects that are likely to be sustained (such as rising government debt, aging of the population, and investment shifts to emerging markets) to arrive at rates reaching 4.6% in three decades. [43]

That figure would still be lower than the 5.0% average interest rate that Washington was paying as recently as 2008. [44] If one assumes—as shown in the studies described above—that the coming 100%-of-GDP rise in the national debt would push interest rates up by approximately 3 percentage points over 2019 levels (from 2.4% to 5.4%), then CBO’s 4.6% assumption reflects additional offsets from factors such as continued low productivity, demographics, and rising savings. However, if those offsetting factors merely remain at current levels, it could mean interest rates above 5%. And if those dampening factors in any way begin to reverse, they could drive rates even higher. This suggests that CBO’s 4.6% assumption is reasonable and could possibly turn out to be an underestimate.

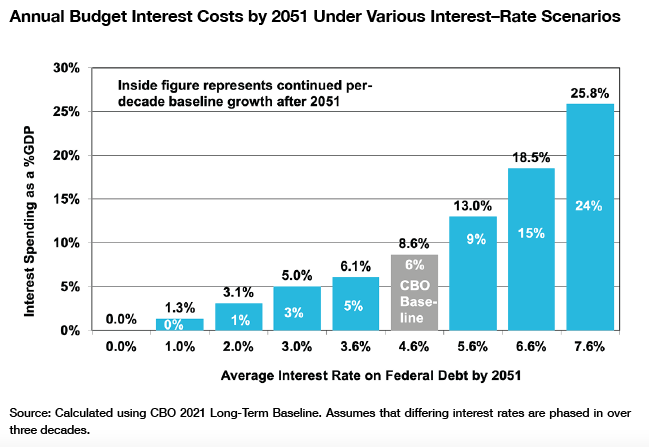

Given the surging baseline debt, even CBO’s interest-rate projections would push federal budget interest costs to historic levels. The CBO baseline assumes that, by 2051, interest on the national debt will cost 8.6% of GDP (the current equivalent of $1.9 trillion annually). This would become the largest expenditure in the federal budget and consume nearly half of all federal tax revenues. And as the debt continues to rise in subsequent decades, interest costs would continue growing rapidly as a share of the economy.

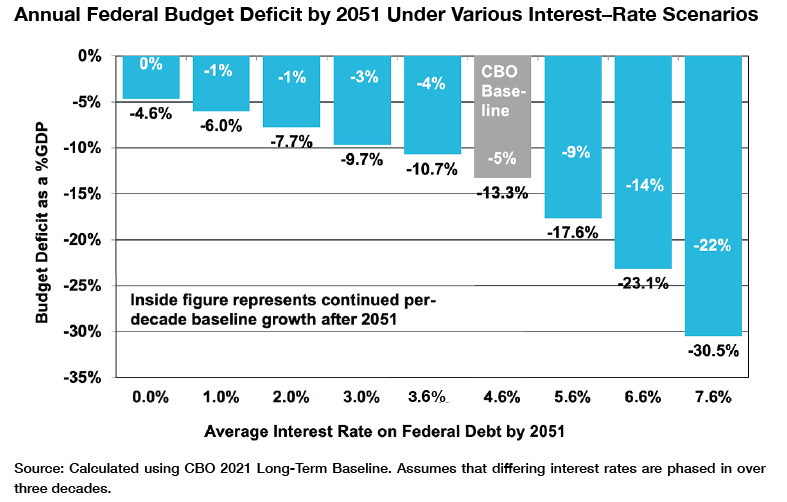

What if interest rates exceed CBO’s projection? An analysis of CBO data reveals that every percentage point by which interest rates exceed the CBO projected rates would increase government interest costs by $30 trillion over 30 years. That is 1.5 times the size of the entire Social Security shortfall and roughly matches total projected defense spending over that period. Moreover, even this 1-percentage-point additional rise in interest rates would push the projected debt to 243% of GDP in 30 years. By that point, annual deficits would jump to 17.6% of GDP, with interest costs consuming 13.0% of GDP, or 70% of all tax revenues. Again, that is merely from an additional 1-percentage-point rise in interest rates above the CBO baseline. A 2-percentage- point overage would push the debt to nearly 300% of GDP within three decades, with interest consuming 100% of all tax revenues. In short, once the debt surges, even modest interest- rate movements can impose stratospheric costs.

Contrary to Popular Belief, the Debt Is Not Sustainable

The CBO long-term budget baseline clarifies that—even under modest long-term interest assumptions—the federal debt is projected to expand at an unsustainable rate. This requires a deeper explanation of what “unsustainability” means, in a federal budget sense, as well as the consequences of “unsustainable” trends.

A sustainable economy requires (among other necessities) manageable taxes, adequate federal investments and benefits, and modest levels of inflation and interest rates. Unsustainable debt can threaten each of these factors. If the federal government’s borrowing needs grow significantly faster than the private sector’s capacity to produce savings, the result can be higher interest rates and fewer pro-growth investments. If exorbitant spending is financed through the central bank, it can produce excessive and unstable inflation (more on this below). If surging borrowing risks bring much higher inflation and interest rates, the only option is to limit federal borrowing and instead finance the interest costs with damaging new taxes or drastic reductions in federal program spending.

The threshold for sustainable debt is not clearly defined—and largely depends on whether a country can borrow in its own currency and thus monetize even a portion of its debt. That said, debt levels exceeding 150% of GDP have proved rare in developed economies. Market psychology plays a role as well. If financial markets determine that a nation’s debt and deficits are expanding at a pace that cannot likely be financed without inflation or significantly squeezing investment, they may demand higher interest rates from the Treasury to compensate for these new risks. These higher interest rates, in turn, will raise federal borrowing costs, which, in turn, raises annual deficits and total government debt, in a vicious circle. Once a debt-and-interest-rate spiral begins, it is nearly impossible to escape without drastic inflation or fiscal consolidation.

Several prominent theories have emerged to determine the threshold of fiscal sustainability. The leading theories focus on stabilizing the national debt, or annual government interest spending, as a share of the GDP. The ability for a government to achieve such stabilizations often depends on the interest rate.

- The Blanchard Standard (r < g). Former IMF chief economist Olivier Blanchard famously pointed out that a nation can reduce its debt ratio and essentially grow its way out of debt by meeting two specific conditions. First, tax revenues must be sufficient to cover nearly all primary (i.e., noninterest) spending. Second, the economy’s growth rate (g) must exceed its interest rate (r). If both conditions are met, the economy will grow faster than the national debt. [45]

This is mathematically correct but largely irrelevant to America’s fiscal outlook because neither condition will likely be met. First, CBO projects that long-term economic growth will eventually stabilize at 3.5%, while the government’s interest rate rises to 4.6% (the inflation- adjusted figures would be 1.5% and 2.6%, respectively). Second, Washington’s primary deficits are projected by CBO to rise from 2.9% to 4.6% of GDP between 2019 and 2051.

Even stabilizing the debt ratio—which can be done with modest budget deficits—does not make government borrowing “free,” as some suggest. Unless the government borrowing is entirely responsible for the nation’s economic growth, the interest expense still represents a burden on taxpayers. A one-time debt-financed $1 trillion transfer program that does not add additional growth will still require taxpayers to make a $30 billion interest payment (assuming a 3% interest rate) every year, forever, regardless of whether the overall economic growth rate exceeds that interest rate. [46]

- The Furman/Summers Standard. Jason Furman and Lawrence Summers have written that a manageable national debt would limit the (inflation-adjusted) federal budget interest cost to 2% of GDP. [47] Assuming 2% inflation, that would mean limiting nominal interest spending to 4% of the economy. Interest costs above that threshold would need to be offset with economically damaging tax increases or spending cuts, or, if not offset, would simply push up deficits and debt in a spiral that continues to hike interest costs until financial markets respond negatively. They note that “if real interest rates stay below 1.33%—which is currently well above what is expected—then a debt level of 150% of GDP would be comfortably sustainable according to our criteria.” Furman and Summers add some fiscal space by defining their 2% of GDP target as real interest payments net of the annual profits that Washington earns on other financial assets, such as the Federal Reserve remitting the interest it collects each year.

Given rising primary deficits, the Furman/Summers standard requires that interest rates permanently remain well below CBO-projected levels (a point that the economists acknowledge and ably defend by assuming a continuation of many of the rate-reducing factors described above). If the CBO baseline assumptions prove accurate, interest spending will leap to 8.6% of GDP (or 6.6% after inflation) within three decades, driving the debt past 200% of GDP.

Even if interest rates do remain relatively low, as Furman and Summers suggest they will, there is no guarantee that the U.S. will be able to keep its debt at 150% of GDP, the level they deem sustainable. The rapidly rising structural deficits caused by Social Security and Medicare alone make this a challenge over the long term. The economists concede this point by assuming Social Security reform in their budget proposals. But Medicare and other health spending would still require reform to prevent them from driving structural budget deficits upward indefinitely. In other words, low interest rates can slow the climb, but the primary deficits driven by unreformed Social Security and Medicare costs would still keep the debt ratio rising indefinitely, eventually reaching levels that even low interest rates cannot fully absorb.

The Furman/Summers standard relaxes on the variables that policymakers can control (taxing and spending) by assuming that the costs of these primary deficits will be bailed out by a variable that policymakers cannot easily control (interest rates). And if any factors push the debt above the targeted thresholds—such as a war, deep recession, or aggressive new entitlement expansions—the interest rates needed to keep (inflation-adjusted) interest costs at the 2%-of-GDP target will need to be even lower. In fact, at a projected 200%-of-GDP debt level, limiting inflation-adjusted interest costs to 2% of GDP would require real interest rates to remain close to 1% (assuming some offsetting savings from the interest received from federal financial assets).

Which Interest Rates Would Be Sustainable?

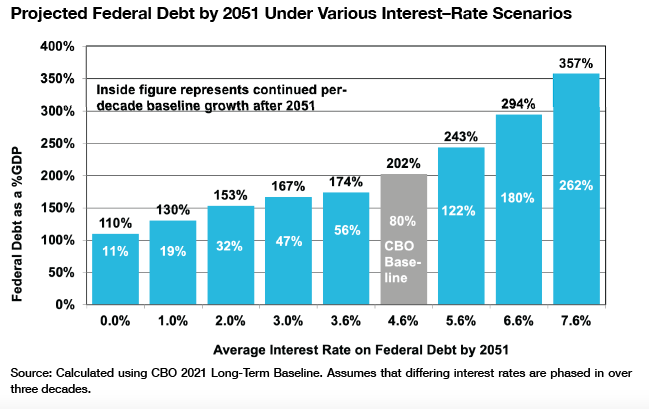

The large primary deficits driven by escalating Social Security and Medicare shortfalls are projected to push the national debt’s share of the economy far beyond anything seen before in U.S. history. The interest rate paid on this burgeoning debt will largely determine the sustainability of Washington’s fiscal and economic policy. At the projected interest rates of 4.6% (or 2.6% after inflation), the debt would soar past 200% of GDP in three decades, and continue rapidly rising thereafter.

If Washington’s average interest rate was 1 percentage point lower—gradually growing to 3.6% over 30 years (or just 1.6% after inflation), the debt would grow more slowly, reaching 174% of GDP within three decades. Even at that level, annual interest costs of 6.1% of GDP (the equivalent of $1.35 trillion in today’s economy) would nearly match the individual spending levels of Social Security and Medicare, consume one-third of all federal revenues, and divert significant spending resources from other priorities. The debt would continue rising thereafter, at a rate of 56% of GDP (and rising) per decade, which would, in turn, raise annual interest costs by an additional 4.5% of GDP (and rising) every decade (see Figures 7–10).

Figure 7

Figure 8

Figure 9

Figure 10

Even a nominal interest rate as low as 2%—which corresponds to a real interest rate approximating zero under CBO inflation projections—would allow the 30-year debt to rise to approximately 153% of GDP. In that scenario, the federal budget interest cost of approximately 3% of GDP would likely be sustainable, although that annual interest cost would continue by 0.8% of GDP in subsequent decades as unrestrained Social Security and Medicare costs continue to push up the debt ratio.

These scenarios show that—as long as primary deficits continue to grow unreformed—the debt ratio and annual interest costs as a share of GDP will continue rising indefinitely. Interest rates merely determine the pace at which these figures rise as a share of GDP, as well as the amount of time lawmakers have to stabilize the primary deficits before they become economically dangerous. However, a reasonable time window is 30–40 years, given that Social Security and Medicare costs are more predictable within that time frame, and today’s workers are paying payroll taxes that correspond to a promised level of benefits that far down the road. Over three decades, the threshold for sustainability would likely be interest rates at or below 3%, which would lead to the debt reaching 167% of GDP (with annual deficits approaching 10% of GDP) and producing annual interest costs of 5% of GDP. These figures would continue worsening thereafter, meaning that even this sustainability is by no means permanent.

Ultimately, debt doves are gambling Washington’s fiscal sustainability on the hope that interest rates never again exceed 3% or 4%, even though the Treasury was paying a 5.0% average interest rate as recently as 2008 and CBO projects a 4.6% interest rate in three decades. And given that the CBO baseline (unrealistically) assumes no additional spending expansions, tax relief, or expensive crises, the more likely scenario is that new deficit-financed legislation further lowers the interest rate required for long-term fiscal sustainability.

The Japan Case Study in Debt

Advocates of substantial additional federal borrowing often point out that Japan’s central government has gradually pushed its gross debt past 200% of GDP, the highest level in the developed world, without its economy imploding. [48] Yet a closer examination shows Japan to be more of a cautionary tale than an example for the U.S. to emulate. It is important to note that Japan’s central government also holds significant financial assets, which (depending on their potential ability to pay down debt) [49] reduce its net debt closer to 150% of GDP. [50] Much of Japan’s debt has come from a Keynesian response to stratospheric savings rates—such as corporate retained earnings equaling 89% of GDP [51]—that otherwise threaten to starve the economy of spending. Financing much of its debt from a large pool of domestic savings is a key reason that Japan has avoided galloping inflation (although the Japanese central bank holds roughly half the central government debt). U.S. savings rates have long been lower than those of Japan, and there is little indication that this will change in the future.

Rather than achieve new stimulus, Japan’s deficit spending has accompanied three decades of sluggish economic growth. However, its finances are still on a more sustainable long-term trajectory than those of the U.S. because of how Japan chooses to spend its deficits—namely, on stimulus and infrastructure, rather than entitlements. Economic stimulus and infrastructure projects can be pared back relatively easily over a few years if fiscal consolidation is required. Indeed, Japan’s annual budget deficits have rarely exceeded 8% of GDP, and its (pre-pandemic) debt level began stabilizing in the past decade, with deficits falling to 3% of GDP. By contrast, the U.S. faces escalating entitlement-driven structural yearly deficits that will exceed 13% of GDP within a few decades and continue accelerating thereafter, likely pushing its debt far above Japanese levels. These U.S. entitlement programs cannot be easily pared back if the debt proves unsustainable because much of those costs represent multi-decade commitments to retired senior citizens, many of whom would be unable at that point to replace benefit reductions with other resources.

Greece and Italy are the only other OECD countries with a total government debt exceeding that of the United States. [52] Greece has already suffered a debt crisis (with per-capita GDP still not recovered a decade later), [53] and Italy endured a minor debt crisis a decade ago, and may be heading toward another. [54] Both these European nations have national debts smaller than that of Japan, yet they face the constraint of being eurozone members who do not have full flexibility on monetary policy. Overall, there are not many examples of advanced-economy nations with debt levels matching that of the U.S., much less examples of national debt levels at 200% of GDP—which is where the U.S. is headed. In short, the U.S. debt path is approaching relatively uncharted territory, and the stand-alone “positive” case study of Japan is, upon close inspection, not positive, comparable, or replicable for the United States.

Other Consequences of Rising Debt

The Loss of Policy Flexibility, Especially for the Biden Agenda

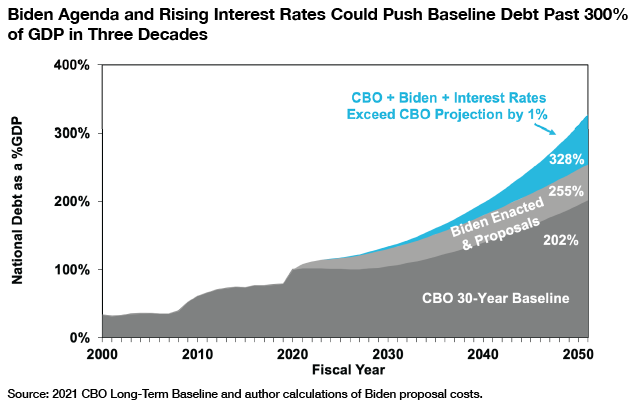

As described earlier, these long-term debt projections are based on a CBO current-law baseline that assumes no new spending expansions, no new tax relief, and the scheduled expiration of all recent stimulus provisions and 2017 tax cuts that require legislative renewal. The baseline also assumes no major wars, no significant natural disasters, and no severe recessions. History suggests that holding to this baseline may prove nearly impossible. Recent events that have added permanent new federal debt include the 2007–09 recession and legislative response (30% of GDP in new debt), 2020–21 pandemic and legislative response (20% of GDP), and the 20-year war on terror (25% of the current GDP). Figure 11 shows that enacting President Biden’s entire agenda of spending and tax proposals would hike the projected national debt by 53% of GDP three decades from now. Extending the expiring portions of the 2017 tax cuts would also push up debt levels by 23% of GDP over three decades. [55]

Figure 11

Altogether, it may be realistic to assume a national debt exceeding 250% of GDP by 2050, even with modest interest rates. In such a scenario, even an interest rate of 3% would produce annual interest costs of approximately 7.5% of GDP (40% of all tax revenues), which would, in turn, induce a spiral of rising debt and interest spending.

Lower Economic Growth and Incomes

Higher interest costs to the federal government are not the only drawbacks of an expanded national debt. Federal borrowing also absorbs savings in the economy that could otherwise have financed business investment and other pro-growth activities. CBO estimates that each dollar borrowed by the federal government reduces investment spending by 33 cents [56]—ultimately reducing economic growth and wage growth. Additionally, because foreign investors hold a healthy share of Treasury securities, the steeply rising interest costs include sending large interest payments abroad rather than keeping the money in the United States. Thus, CBO estimates that the baseline increase in government debt between 2019 and 2050 would shave $6,300 per person (or 6.7%) off the gross national product (GNP) relative to a stabilized debt ratio. [57]

Jack Salmon of the Mercatus Center surveyed 40 leading academic studies published between 2010 and 2020 that analyzed the relationship between public debt and economic growth (with each study examining at least seven countries). Nearly every study concluded that high levels of public debt reduce the economic growth rate. The effect is generally nonlinear (countries beginning with small public debts often see a positive link between debt and economic growth), and the debt level in which the economic growth effect turns negative depends on nation-specific factors such as the overall level of economic development. Nonetheless, according to the 25 studies that offered specific threshold estimates: “For advanced countries, mean and median threshold levels are found at 78 percent and 82 percent of GDP, respectively. For developing countries, mean and median threshold levels are found at 61 percent and 56 percent of GDP, respectively.” [58] The U.S. government debt has already far surpassed these threshold levels, reaching 161% of GDP, including state and local debt (the standard criteria in these studies), [59] and will continue exceeding them by an ever-widening margin.

The Temptation of a Federal Reserve Solution

Consider a scenario in which federal debt is escalating and interest rates are rising—with each percentage-point rate increase adding $30 trillion in government interest costs over three decades. Congress could hypothetically attempt to rein in these added soaring deficits with a drastic and painful program of tax increases and spending cuts. It is more likely that lawmakers will see little point in sacrificing their political careers and their constituents’ financial security for a few trillion dollars in deficit savings when they could instead save a full $30 trillion by simply mandating that Washington’s interest rate be pegged at a rate 1 percentage point lower.

Fiscal dominance occurs when central banks abandon their role in stabilizing the macroeconomy and instead pledge to maintain low interest rates in order to guarantee cheap borrowing for the Treasury. The U.S. practiced this policy during World War II, when the Treasury asked the Federal Reserve to peg interest rates at 0.375% for short-term Treasury securities and to target long-term Treasury bonds at 2.5%. This ensured that the Treasury could borrow cheaply to finance the war but also handcuffed the Fed’s macroeconomic stabilization abilities, and instead led to the Federal Reserve purchasing a significant portion of these securities and thus increasing the money supply. After the war ended, President Truman and the Treasury pushed the Federal Reserve to continue this policy, resulting in high inflation rates, until the Federal Reserve was finally freed in 1951. [60] Later, in the late 1960s and early 1970s, the Federal Reserve held interest rates lower than economic fundamentals dictated, partly because of political pressure from President Johnson and then President Nixon, resulting in inflation. [61]

If Washington finds that mounting debt is putting its fiscal sustainability at the mercy of interest rates, there is little doubt that presidents, Treasury secretaries, and Congress will pressure the Federal Reserve to pledge artificially low interest rates, including monetizing much of the debt, if necessary. Federal Reserve governors are presidentially appointed and Senate-confirmed and not immune to political pressure. As a last resort, Congress and the president could even enact legislation eroding the Fed’s independence. A member of the Federal Reserve’s board of governors recently pledged to resist fiscal dominance pressures, but as the debt rises over the next few decades, that pressure will surely swell. [62]

Fiscal dominance can bring economic chaos. Inflation would rise steeply, and the Federal Reserve would surrender its ability to stabilize the economy. Very low interest rates also harm retirees and others on fixed incomes, encourage speculation seeking higher returns, lead to poor investments, and are bad for business competition. [63] It is true that the Federal Reserve could purchase a substantial amount of Treasury debt and then limit inflation by paying banks whatever interest rate is necessary to keep their new deposits in the banking system and out of broader economic circulation. However, the Federal Reserve interest payments would ultimately come out of its profits that are annually remitted to the Treasury. In that case, the ultimate cost to the federal government would be similar to the Treasury having borrowed the money directly at market interest rates. Federal Reserve solutions will surely tempt elected officials, but they are no free lunch.

The Cost of “Wait and See”

When faced with the prospect of soaring debt and growing interest rates, debt doves often respond that policymakers should just “wait and see.” Essentially, they argue that Washington should continue running up spending and debt and, if interest rates rise steeply in the future, simply reverse the spending increases and reduce the deficit. For example, Jason Furman and Lawrence Summers write that “if the debt becomes a problem, interest rates will rise, putting financial and political pressure on policymakers to accomplish what fiscal fundamentalists have long wanted. But even if that happens, it is not likely to cost so much that it would be worth paying a definite cost today to prevent the small chance of a problem in the future.” [64]

It is not that easy. The policies driving debt upward may prove nearly impossible to reverse later. Specifically, Social Security and Medicare shortfalls overwhelmingly drive long-term deficits. By 2030, nearly all 74 million baby boomers will be retired, and as this generation ages into their 70s and 80s, they will be increasingly unable to absorb any significant reforms to these programs. That means that nearly all annual benefit increases and rising health-care costs will become politically irreversible.

Surging interest costs are mostly irreversible, too, because of the rising debt that will have accumulated (and will continue to accumulate if Social Security and Medicare cannot be reformed) and because the rising interest rates in this situation cannot simply be reversed (unless the Federal Reserve unwisely commits to monetizing much of the debt). In fact, if interest rates are driven upward by financial markets losing faith in the federal government’s long-term ability to manage its debt, the resulting risk premium may remain baked in to interest rates for several years or even decades.

Debt crises typically build slowly over many years, with little response from the financial markets or the broader economy. Then, any economic event—a severe recession, an unexpected emergency expenditure, a breakdown of high-profile congressional budget negotiations, or the debt surpassing a certain round-number threshold—can trigger a financial-market panic out of fear that Washington is on an unsustainable course, which could drive up interest rates and federal debt, in a vicious circle. At that point, the fiscal consolidation required would be brutal, as lawmakers would face a choice between substantial tax increases (4%–7% of GDP), significant reforms to Social Security and Medicare for current seniors, the evisceration of most other federal social programs, or Federal Reserve–driven inflation.

There is a parallel between long-term debt and global warming. Both problems gradually build toward an unsustainable outcome over several decades—often with people not feeling the negative effects. Just as scientists can model greenhouse gas emissions from fossil fuels, economists can model the demographic-driven costs of Social Security and Medicare. Lower temperatures can occasionally lull people into thinking that global warming is not a threat, just as other interest-rate factors may counteract debt interest-rate changes for some period of time. But in both situations, the underlying issue is real and measurable and will keep building long after those counteracting effects have faded away or been overwhelmed. The debt projections show unsustainable interest costs, even with interest rates remaining below long-term averages, and it is highly likely that interest rates at some point will rise above those averages (if, for no other reason than the fact that economic trends tend to fluctuate). In other words, it is difficult to build a long-term model of the climate or the federal budget in which the rising temperatures or unsustainable debt do not eventually overwhelm other factors. In both cases, basic prevention now is far preferable to imposing a painful, drastic cure after the damage is done.

III. A Strategy for Risk Management

The federal government needs to budget sustainably with an eye on basic risk management. This includes analyzing the likelihood of certain risks—such as interest rates someday returning to pre-2008 levels—and assessing the resulting economic damage from such an event. Because such a development is both reasonably likely at some point and potentially calamitous for the federal government and broader economy, lawmakers should begin taking steps to mitigate this risk. After all, any economic policy that begins with the premise “let’s just assume interest rates stay low forever” is extraordinarily hubristic, naïve, and irresponsible, particularly when there is no backup plan if rates do rise.

The first and most obvious recommendation is to stop digging. Lawmakers should hold off on major expensive initiatives, especially new entitlements with rising long-term costs. Even policies “paid for” with large tax increases or spending cuts would consume the limited number of plausible offsets that are needed to address the baseline shortfalls, and thus force those later reforms to cut even deeper.

Second, lawmakers must begin addressing the Social Security and Medicare shortfalls that are projected to cost $67 trillion (plus $45 trillion in resulting interest costs) over three decades. These annual shortfalls and their interest costs would reach 15% of GDP by 2051. There is no plausible combination of other tax increases or spending savings that can plug this gap, and delaying the inevitable reforms of these unsustainable programs would merely enlarge those reforms and impose them on older and more fragile seniors. Reforms gradually phased in over the next few years—such as higher eligibility ages, benefit trims for wealthy seniors, modest payroll tax increases, and health efficiency reforms such as a new Medicare premium support system [65]— can stabilize the long-term federal debt near its current 100% of GDP level while still protecting low-income seniors. At that point, lawmakers could more safely add modest new federal investments or social spending without fear of a debt crisis.

Third, lawmakers can mitigate long-term interest-rate risk by locking as much of its debt as possible into long-term fixed interest rates. The average maturity of the federal debt is just 69 months, which leaves Washington vulnerable to higher interest rates down the road. At this point, Washington could likely lock much of its debt into rates below 2.5%, which may temporarily raise borrowing costs above the current short-term interest rates but, over the long term, could save many trillions of dollars and protect Washington from a fiscal crisis. Yes, there is always a chance that long-term interest rates could remain low indefinitely, in which case locking in a 2.5% rate would ultimately cost more. However, the goal is risk management, and strongly decreasing the likelihood of a long-term fiscal crisis is absolutely worth the cost of (still-cheap) 2.5% interest rates.

Treasury officials and some economists have indicated that weak market demand would likely doom a major shift toward 20-, 30-, or even 50-year Treasury securities. There is reason to believe that these concerns are overstated. The U.S. debt maturities are shorter than those of most OECD countries and, in some cases, far shorter (Great Britain’s average debt maturity is 18 years). [66] Additionally, if the world is awash in savings and desperate for the safety of U.S. government bonds— as debt doves regularly assert—that would suggest that this insatiable demand will not collapse because of extended maturities, particularly if the shorter-maturity options become less available. Longer bonds may prove particularly workable for insurance funds and pension funds. If Washington shifts more toward longer bonds, financial markets are ultimately likely to get on board.

Finally, congressional reformers must keep an eye on long-term economic growth. While economic growth alone cannot solve Washington’s fiscal imbalances, a sluggish economy will deepen the hole by reducing tax revenues and raising unemployment insurance and antipoverty costs. Thus, lawmakers should ensure that long-term fiscal consolidations are enacted gradually and with policies that minimize economic damage.

Conclusion

The U.S. government is projected to run a staggering $112 trillion in budget deficits over the next three decades, driven mostly by Social Security and Medicare commitments that are already set in law. Yet rather than pare back this unprecedented borrowing binge, many debt doves are proposing legislation to drive the borrowing even higher. The plan to handle all this debt is to simply assume that interest rates never exceed 3% or 4% ever again—even though such rates prevailed as recently as 2008. It is easy to specify countless economic factors that can (and likely will) push up interest rates at some point in the future. But debating specific causal factors is not the point. The reality is that no one knows what interest rates will be in 5, 10, 20, or 50 years, and any claim otherwise is hubristic and naïve. Yes, interest rates have been on a downswing in recent decades. Yet the past century has not been kind to confident economists declaring permanent victory over recessions, inflation, falling house prices, or stock-market declines. In particular, economic forecasters and markets have built a terrible track record predicting even medium-term interest-rate movements.

Nevertheless, many of today’s economists, policymakers, and activists assert that this time they can predict interest rates decades in advance—and they are willing to gamble the future of the U.S. economy on that hunch. Interest rates as high as 5% are well within the typical historical range; yet they would likely spark an eventual debt crisis under the projected levels of borrowing. This soaring government debt is particularly dangerous because, by the time the economy feels the negative effects, it is too late to painlessly fix. Within a decade, nearly all 74 million baby boomers will be retired, with benefit levels continuing to rise in the meantime—which will be nearly impossible to pare back. Also, by that point, the substantially larger national debt will require higher interest payments. And once panicking financial markets demand higher interest rates on that government debt (raising federal costs further), it can take years or even decades to calm these markets back down. Drastic, debt-crisis-driven fiscal consolidations can bring substantial pain to a nation. Politicians should not gamble our economic future on the hope that the long-standing laws of economics no longer apply, as America has no backup plan if events prove them wrong.

Endnotes

About the Author

Brian Riedl is a senior fellow at the Manhattan Institute, focusing on budget, tax, and economic policy. Previously, he worked for six years as chief economist to Senator Rob Portman (R-OH) and as staff director of the Senate Finance Subcommittee on Fiscal Responsibility and Economic Growth. He also served as a director of budget and spending policy for Marco Rubio’s presidential campaign and was the lead architect of the 10-year deficit-reduction plan for Mitt Romney’s presidential campaign.

During 2001–11, Riedl served as the Heritage Foundation’s lead research fellow on federal budget and spending policy. In that position, he helped lay the groundwork for Congress to cap soaring federal spending, rein in farm subsidies, and ban pork-barrel earmarks. Riedl’s writing and research have been featured in, among others, the New York Times, Wall Street Journal, Washington Post, Los Angeles Times, and National Review; he is a frequent guest on NBC, CBS, PBS, CNN, FOX News, MSNBC, and C-SPAN.

Riedl holds a bachelor’s degree in economics and political science from the University of Wisconsin and a master’s degree in public affairs from Princeton University.

Photo: f11photo/iStock

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).