Photo by Witthaya Prasongsin/Getty Images

As interest rates recede, mortgage rates might not be poised to follow.

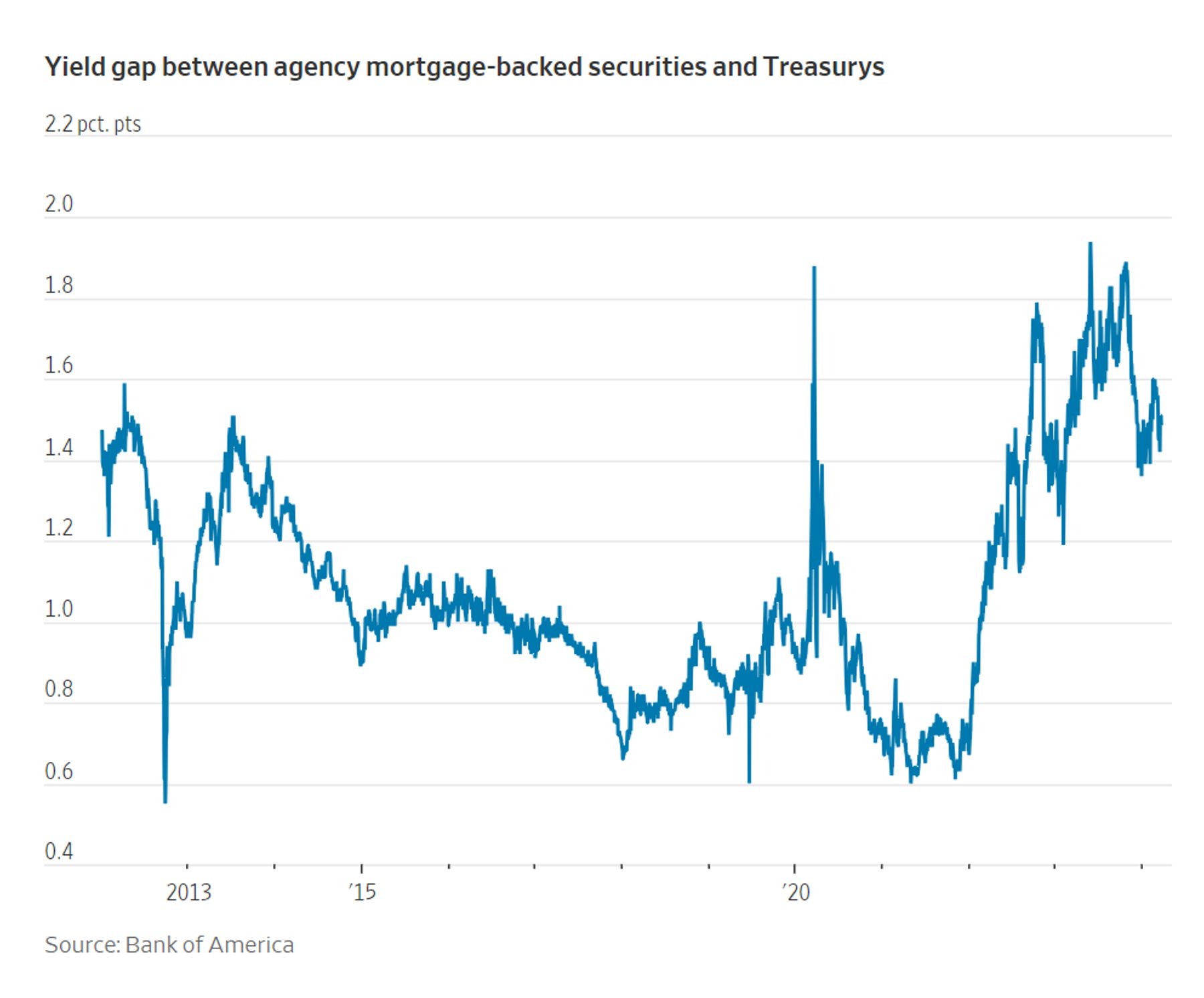

As reflected in the chart below, the difference in yield between Treasuries and mortgage-backed securities (MSBs) has narrowed. However, it has not returned to its historic level. It probably will not. Homebuyers should expect a “new normal” of higher rates. Fannie Mae economists, for example, reassessed their projection of 2024 Q4 rates to 6.4%, an increase from a previously estimated 5.9%.

Higher projected rates are a product of shrinking demand for mortgages and MSBs. As the Fed continues to wind-down its balance sheet, it is not seeking to purchase MSBs as it did during previous rounds of quantitative easing. In fact, Fed governor Christopher Waller expressed a desire to reduce MBS holdings “to zero.” Banks are also weary and wary of MSBs in the wake of last year’s bond crisis (the one that torpedoed Silicon Valley Bank). Finally, investors are more eager to place their capital elsewhere, specifically cash funds.

From a supply side, the pool of mortgage originators is shrinking. Many are closing shop as demand (and profitability) plunges. Loan volumes are likely to remain low as current homeowners with locked-in lower rates are unlikely to sell or refinance.

For new homebuyers, subsequently, the future of mortgages remains higher for longer.

Source: Telis Demos, WSJ; Allison Schrager, Bloomberg Opinion; Stacey Vanek Smith, NPR

Reade Ben is a policy analyst at the Manhattan Institute.

Interested in real economic insights? Want to stay ahead of the competition? Sign up for our weekly newsletter here.

Photo by Witthaya Prasongsin/Getty Images