Correcting the Top 10 Tax Myths

Photo by Spencer Platt/Getty Images

Introduction

As Washington prepares for a 2025 dominated by tax policy—led by the issue of whether to extend the expiring 2017 tax cuts—the debate is likely to bring a fresh recirculation of the most common myths about the federal tax system from both the left and the right.

On the one hand, the false conservative narrative suggests that the middle class is buried in taxes and that tax cuts pay for themselves, or even reduce deficits by “starving the beast” of the ability to expand federal spending. The false liberal narrative, on the other hand, suggests that “tax cuts for the rich” drive the deficit upward and lead to a regressive tax code, in contrast to the strongly progressive tax systems of 1950s America and contemporary Europe.

In reality, the federal tax system is quite progressive—more so than those of Europe and pre-Reagan America. Middle- and low-earners pay very low tax rates. And the vast majority of tax cuts truly reduce federal revenues and increase deficits (albeit less so than rising spending levels). The following report corrects the most common and pernicious federal tax myths.

Myth 1: “Tax Cuts Pay for Themselves”

Perhaps the most common and harmful conservative tax fallacy is that most tax cuts entirely pay for themselves with the revenues from expanded economic activity. Indeed, every major Republican tax cut over the past half-century has been sold as a free lunch that will cost the federal government no revenue.

It is certainly true that well-designed tax cuts can increase incentives to work, save, invest, and be productive, thus creating additional income that is subject to taxation. The problem is asserting that these “economic feedback revenues” will be large enough to pay for 100% of the static revenue loss of the tax cut. The Laffer Curve does show that there is a point at which tax rates rise so high that tax revenues begin to fall (and where reducing the tax rate would therefore increase tax revenues). Yet the peak of the Laffer Curve for the income tax is typically estimated to be between marginal rates of 55% and 73% (well above current rates),[1] while investment-tax revenues likely peak at 30%–45%.[2]

Ultimately, the economic response to tax changes depends on how easily taxpayers can and will alter their tax-producing behaviors to avoid a higher tax rate. Property- and sales-tax increases induce relatively small changes to purchases or home-buying behavior to avoid the tax. By contrast, corporations and investors are extremely tax-sensitive because they are easily able to adjust the timing, location, and size of new investments. Therefore, they can easily reduce their taxable activities in response to higher tax rates, limiting new revenues.

In the current economy, most taxes are not close to their revenue-maximizing rates. At the current average tax rate of 20%, each $1 in tax cuts would need to produce $5 in new economic activity to pay for itself (whereby taxing that $5 at a 20% rate would recover that lost revenue dollar). It is extraordinarily rare to identify tax cuts that can provide such a substantial economic return. It is more common for feedback revenues to offset a modest portion of the static revenue loss.

Critics often point to increased tax revenues after a tax cut as evidence that the cut paid for itself. But such analysis measures the wrong variable. For a tax cut to pay for itself, tax revenues would have to match the level that would have been raised even without the tax cut. After all, even a stable tax code will produce rising revenues due simply to inflation, population growth, rising real wages, and growing business profits (which are needed to keep pace with spending levels that also automatically rise with inflation, population growth, and other factors). If revenues (and spending) are automatically growing 4% annually, due to factors such as inflation and population growth, then a tax cut that yields a 1% increase in revenue would obviously expand the budget deficit. Tax cutters may support reducing this baseline growth of tax revenues, but they should not deny that the vast majority of tax cuts produce lower tax-revenue levels than would be raised under higher tax rates.

The 2017 tax cuts provide a useful example.[3] After adjusting for inflation and netting out revenues from Federal Reserve deposits, 2018–24 federal revenues came in $665 billion below the levels that had been projected by the Congressional Budget Office (CBO) before the 2017 tax cuts. Granted, this decline is far less than the $1,120 billion revenue loss that had been projected by CBO following the tax cuts for the same period. Surely, some of those rebounding revenues resulted from President Trump’s tariffs (raising roughly $80 billion annually), revenue raisers enacted by President Biden, and structural factors such as higher-than-expected immigration levels. And the pandemic and aggressive federal response surely drove tax-revenue trends between 2020 and 2022.

Before all those intervening factors altered later revenues, 2018 and 2019 tax revenues came in a combined $432 billion below CBO’s pre-TCJA (Tax Cuts and Jobs Act) projection, adjusted for inflation. Current tax revenues are also close to pre-TCJA projections, although the interaction of tariffs and new revenue raisers surely influenced these figures. Overall, the data show that TCJA managed to pay for a modest portion of itself—a share that should increase over time because of the cumulative GDP effects of any resulting economic expansion—but it did not fully pay for itself.

Myth 2: “Tax Cuts Will Starve the Beast”

In the late 1970s and early 1980s, conservative tax cutters began to assert that aggressive tax cuts induce lawmakers to cut spending by an equal amount, thus offsetting their deficit impact. If tax cuts “starve the beast” of revenue, then a deficit-conscious electorate and Congress will have no choice but to demand offsetting spending cuts. The flip side of this theory is that any tax increase revenues will be plowed into new spending rather than left for deficit reduction. Thus, the most effective way to slash government spending is by first aggressively cutting taxes.

This theory contradicts both price theory and public choice theory. Tax cuts lower the price of spending, making voters want more of this free lunch. Persuading voters to oppose spending hikes would require making them pay for that spending with accompanying taxes.

More broadly, it is ahistorical to believe that abandoning all fiscal responsibility on one side of the federal budget will induce Congress and voters to demand even tighter fiscal responsibility on the other side of the ledger. Lawmakers who cut taxes—often while claiming that “deficits don’t matter”—cannot credibly turn around and make a deficit-focused argument to slash popular Medicare benefits or education spending. They have already surrendered any deficit credibility—which is why GOP lawmakers who had focused obsessively on deficits during the early 2010s suddenly stopped talking about them following the 2017 tax cuts.

Instead of starving the beast, tax cuts have been followed by aggressive spending sprees, while tax increases have been followed by spending restraint. This is because tax cuts signal to voters and lawmakers that deficits are no longer a concern, while tax increases reflect an era of deficit-panic and austerity. In other words, fiscal responsibility is either practiced on both sides of the tax and spending ledger, or on neither side. This historical record is clear:

- The 1981 Reagan tax cuts were followed by a defense-driven spending spree and no significant spending cuts in other areas.

- The 1990 Bush tax hikes contained significant spending reforms and, after the 1993 Clinton tax hikes, were followed by the largest spending decline since the 1950s, culminating in the 1998–2001 budget surpluses.

- The 2001 Bush tax cuts, which put an end to surpluses, were followed by a historical spending surge for wars, “compassionate conservative” domestic spending, and new entitlement programs.

- The 2017 Trump tax cuts came with a GOP-led 13% discretionary spending hike in one year, and the past seven years have seen the largest spending spree since World War II.

These trends are not an accident. I served as an economic advisor in the Senate until 2017, and since then have informally advised several senators and U.S. representatives. Republicans who voted for the 2017 tax cuts quickly learned that any public discussion of the need to rein in growing budget deficits would be quickly and forcefully met with demands to start by canceling their own large tax cuts. Eventually, these lawmakers just gave up and stopped mentioning budget deficits in public. Having lost the ability to cite deficit concerns, these lawmakers concluded that they now had little choice but to vote for popular, deficit-expanding spending bills.

Theory, practice, and lawmaker testimonials all agree that “starve the beast” does not work, as even President Reagan’s own top economist eventually conceded.[4] In the imperfect world of social science research, that evidence is as solid as possible.[5]

Myth 3: “The Middle Class Pays Higher Tax Rates than the Rich”

The conspiratorial populism that characterizes modern politics often suggests that virtually all government policies are designed to benefit the wealthy at the expense of everyone else. The tax policy version of this view is that wealthy families pay less in taxes than the middle class. This narrative is very common but spectacularly false.

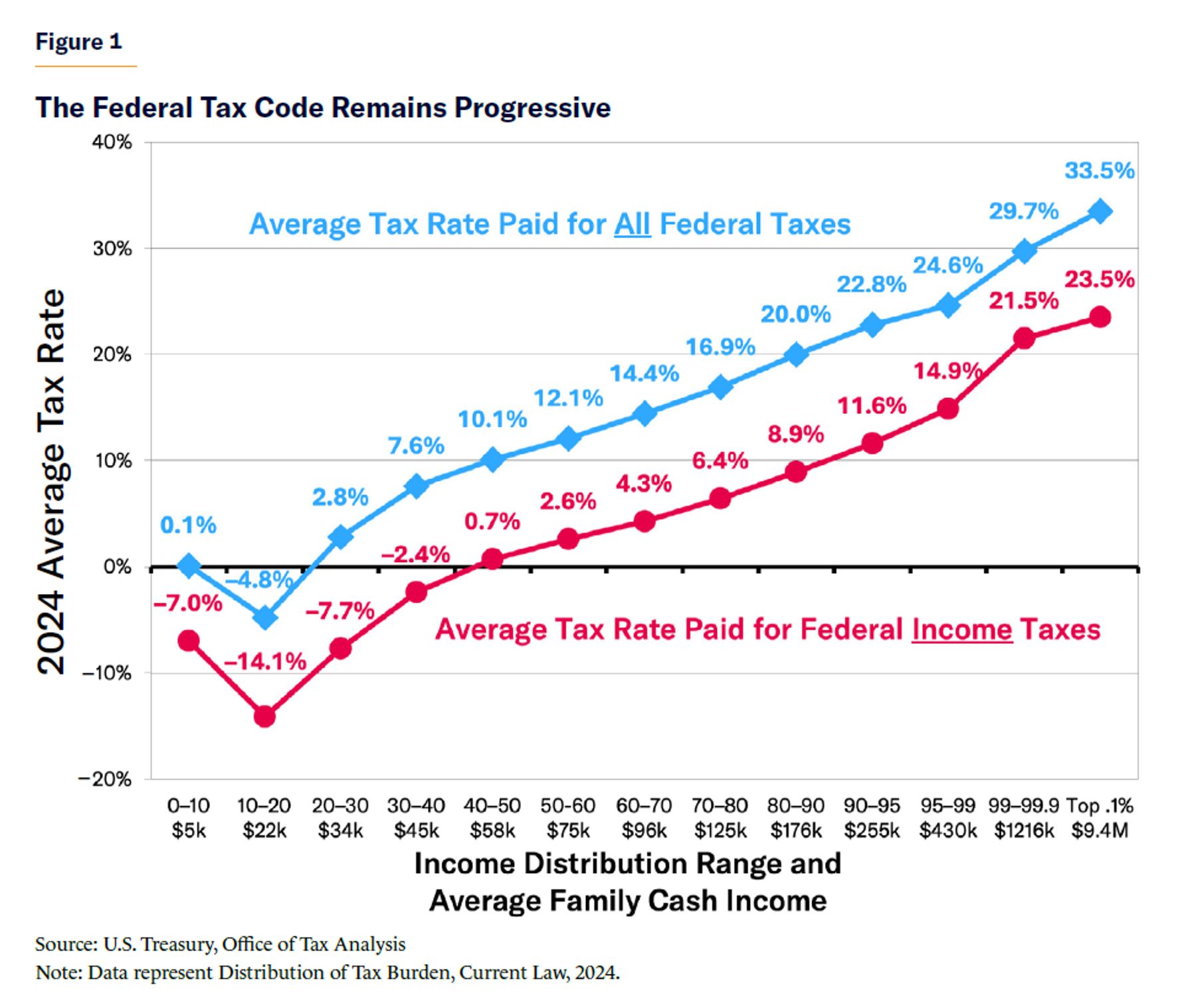

As Figure 1 shows, the federal tax system is remarkably progressive. Within income taxes, the lowest-earning 40% pay a negative rate, and the median-earning family pays an effective rate of just 2%. Meanwhile, the top 1% of earners pay an average income-tax rate of 21.5% or higher.[6]

The same chart includes IRS data on the average of all federal taxes paid—income, payroll (including the employer side), corporate, estate, and excise taxes. With these included, the tax code remains progressive, with the bottom-earning 20% paying negative federal taxes, middle-earners paying about 11% of their income in federal taxes, and the top-earning 1% paying a nearly 30% tax rate.[7]

Indeed, the federal tax code has grown more progressive over time, mainly due to refundable tax credits and tax relief that removed 10 million low-earners from the income-tax rolls. Since 1979, the share of income taxes paid by the top-earning 20% has jumped from 65% to 90%, while their share of all combined federal taxes has increased from 55% to 69%. These increases in the share of federal taxes paid by high-earners well exceed the increase in their share of the total income earned during this period.[8] In fact, OECD data reveal that the U.S. has the most progressive income and payroll taxes of any OECD nation—even after adjusting for income distribution across countries.[9] America taxes the wealthy within international norms but taxes lower- and middle-earners far less than other nations (not to mention not imposing, unlike many of those countries, more regressive value-added taxes).

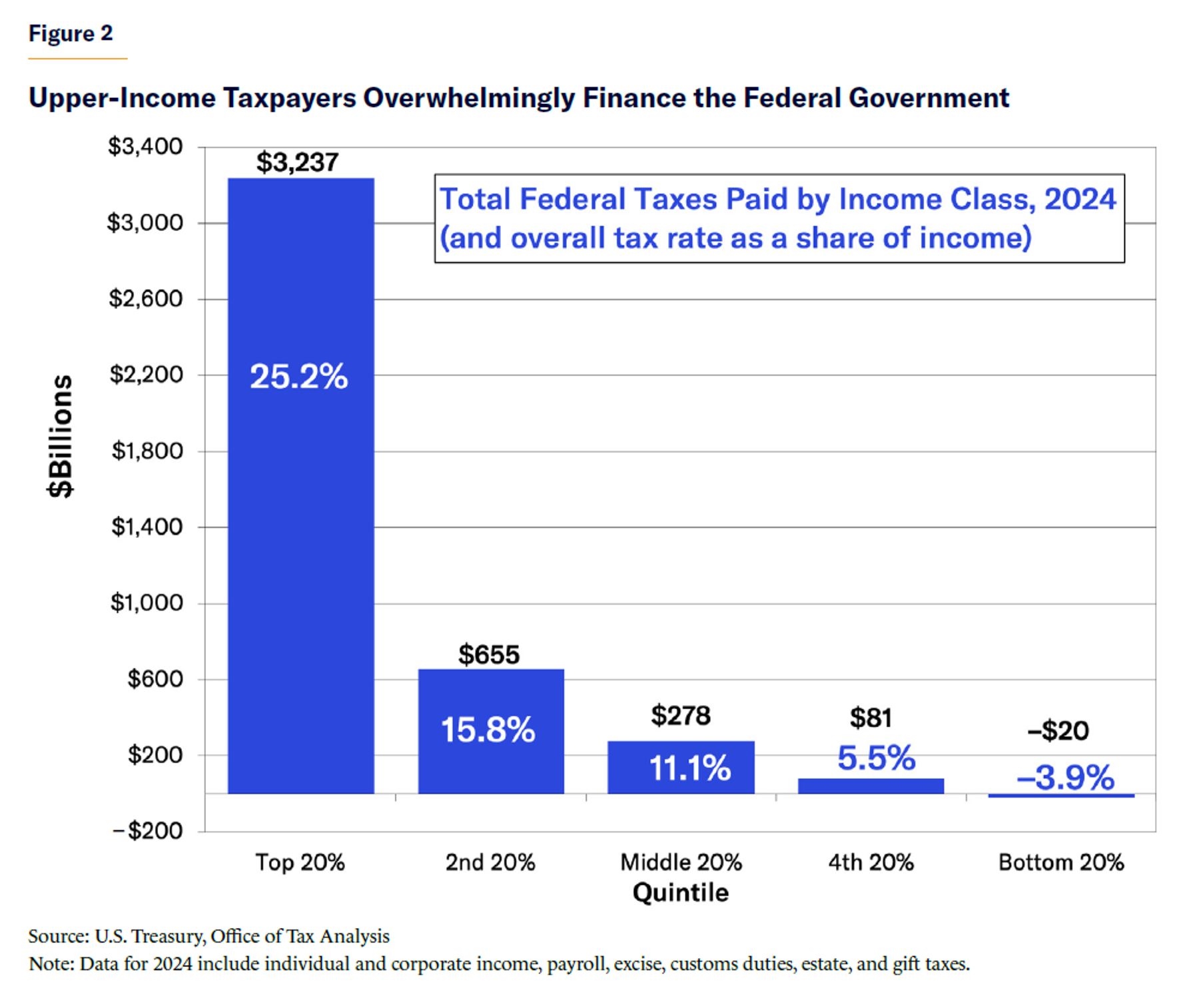

Thus, the wealthy overwhelmingly fund the federal government. In 2024, the top-earning 20% paid just under $2 trillion in income taxes, while the second quintile contributed $228 billion. The remaining 60% of earners, by contrast, paid a collective income tax of negative $92 billion. Across all federal taxes, the top-earning quintile paid $3.2 trillion, while the remaining four quintiles paid $655 billion, $278 billion, $81 billion, and negative $20 billion, respectively (see Figure 2). Put another way, the top-earning quintile funded 201 days of 2024 federal spending, the next quintile funded 41 days, and the bottom-earning 60% of families collectively funded 21 days of spending (the remaining 103 days were financed with budget deficits and borrowing).[10] The notion that middle-earner taxes finance the federal government, while most wealthy families escape taxes, is simply preposterous.

The misperception of a regressive federal tax code has a few sources. Critics aggressively highlight the occasional wealthy corporation or individual who escapes income tax for a single year (often due merely to tax shifting across years). In addition, some ultra-wealthy families rely on investment income rather than wage income, and thus pay a reduced capital-gains tax rate—though one that still exceeds the effective tax rate of a large majority of families.

The Biden White House has contributed to this myth by claiming that billionaires pay an average tax rate of only 8%—but this figure is the result of nonconventional and contradictory calculations. For example, the Biden White House calculations—unlike the U.S. tax code—classifies theoretical income from (unsold) rising capital-gains valuations as “untaxed income” (thus reducing the calculated effective tax rate) while also disregarding the corporate and estate taxes that these families do pay (also thus showing an artificially low tax rate). In fact, the only consistent pattern in the White House’s selection of variables to include in its tax-rate calculations was to choose those that would show the most regressive tax distribution.[11]

Myth 4: “Those Old 91% Tax Rates Raised Large Tax Revenues”

Progressives—and even many nonprogressives—regularly assert that mid-twentieth-century income-tax rates exceeding 90% were able to raise substantial revenues without damaging the broader economy. But reductions to these sky-high tax brackets led to more income-tax revenue because wealthy taxpayers were shielded from those exorbitant marginal tax brackets through concurrent tax expenditures and extremely high tax-bracket thresholds.

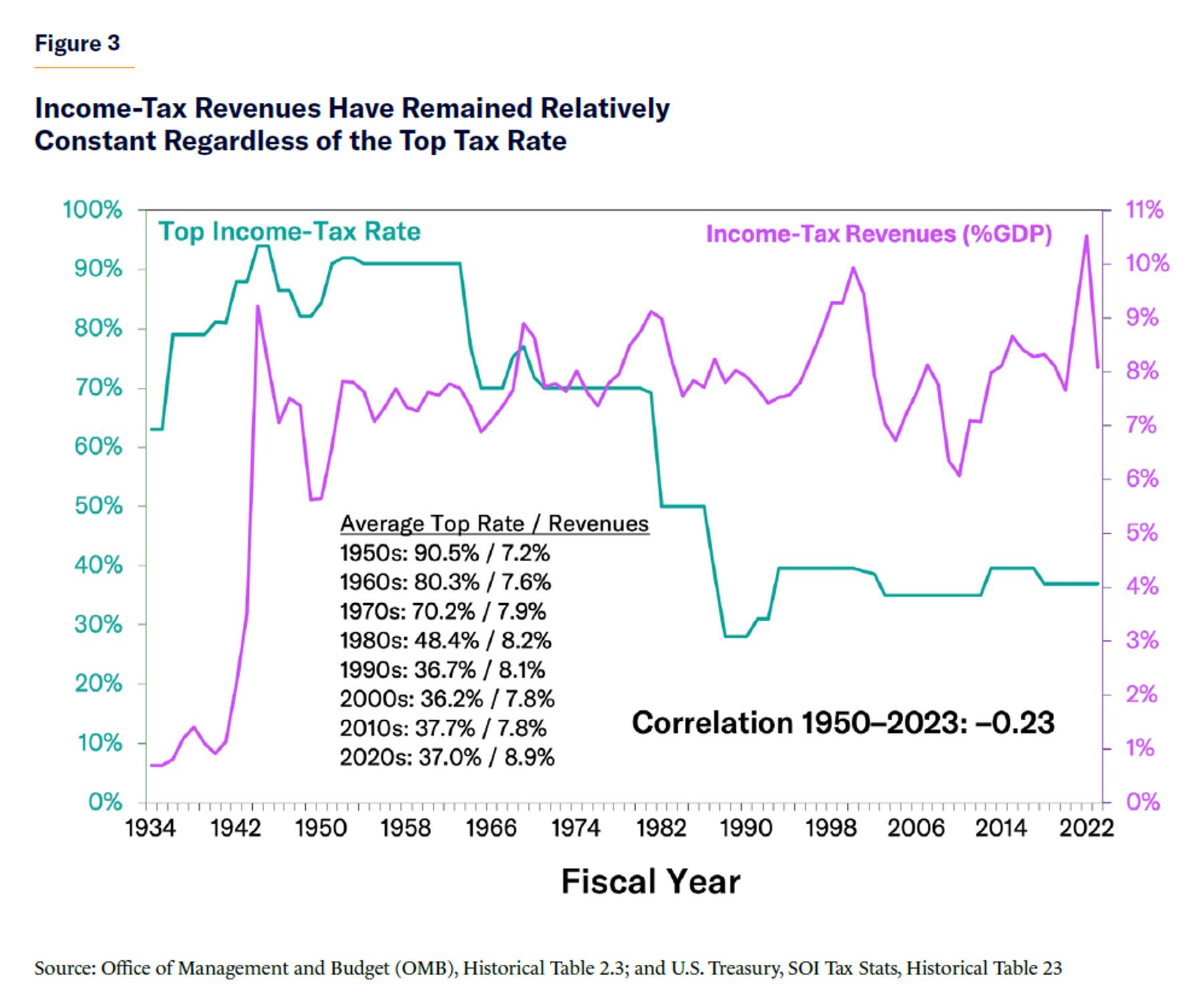

Figure 3 shows that the 1950s era of 91% top income-tax rates produced only 7.2% of GDP in income-tax revenues. As the top tax bracket fell to 70% in the 1960s and 1970s, income-tax revenues rose to 7.6% and then 7.9% of GDP, respectively. Following dramatic reductions of the top income-tax rates beginning in 1981, federal income-tax revenues have averaged 8.1% of GDP.[12]

Simply put, Washington collects more income-tax revenues (as a share of GDP) today with a top tax bracket of 37% than it collected in the 1950s with a 91% tax bracket. In fact, since 1950, the yearly correlation between the highest income-tax bracket and federal income-tax revenues as a share of the economy is –0.23, meaning that higher top tax rates are correlated with lower income-tax revenues.

Focusing too much on the highest marginal tax rate ignores other factors that heavily influence tax revenues. These include the income thresholds for every tax bracket, tax preferences that shield families from higher tax rates, incentives for tax avoidance (such as reclassifying income as capital gains or corporate income), tax evasion, and—most important—broader economic growth rates. Those who want to raise significant tax revenues from the wealthy might wish to consider reforms that affect those factors, as well as account for how they might offset the revenues from marginal tax-rate increases.

Tax data compiled by leading progressive economist Gabriel Zucman reveal that the average income-tax rate (including state taxes) of the highest-earning 1% of taxpayers was actually lower in the 1950s (14.1%) than in the 2010s (19.6%).[13] CBO data show that, even as the highest federal income-tax bracket fell from 70% to 37% between 1980 and 2019, the average income-tax rate paid by the top 1% remained at 23%.[14] IRS data show that only 1% of tax returns in 1958 were in federal income-tax brackets above 35%; and since 1962, the share of tax returns in a tax bracket above 28% has gone down only slightly, from 4% to 3%.[15] In short, the highest tax brackets reveal little about tax revenues and the actual tax rates paid by families.

The 1961 Case Study

For a case study of the failure of 91% income-tax rates, we can examine the 1961 IRS record. That year’s famous 91% income-tax bracket applied to taxable incomes above $400,000 for a married couple—the equivalent of $4.1 million in today’s dollars. Yet just 446 tax returns—or one in every 137,891 returns filed—paid income taxes in the 91% bracket. The $61 million in total tax revenue collected from this tax bracket (the current equivalent of $3 billion in today’s GDP) constituted just 0.1% of all income-tax revenues, or 0.01% of GDP.[16]

We can broaden the 1961 analysis by examining all 25 income-tax brackets between 52% and 91%. Relative to a 50% top marginal rate, these tax brackets collected just 0.11% of GDP, or 1% of income-tax revenues—the equivalent of $31 billion in today’s GDP. In short, all the additional revenue from the 25 tax brackets between 52% and 91% would—adjusted into today’s economy—finance the current federal government for a day and a half.[17]

That’s not all. Virtually all economists agree that tax rates at these levels reduce incentives to work, save, and invest (even if they disagree on the size of these economic losses). If several decades of excessive tax rates slowed long-term economic activity enough to shave even 0.5 percentage points off the total GDP, that would mean that these tax rates actually lost revenue, compared with having that extra economic activity to tax.

Since 1979, effective tax rates on the richest 1% have remained steady, even as the top marginal tax rate fell nearly in half, because factors such as tax preferences and tax income thresholds also affect taxes paid. Perhaps today’s policymakers can better design tax increases to minimize the pitfalls of the older higher tax rates (even as tax planning grows more sophisticated and income becomes more mobile). However, it is simply false that the 1950s and 1960s prove that 90% tax brackets can raise significant tax revenues with minimal economic damage.

Myth 5: “Europe’s Higher Tax Revenues Derive from Aggressively Taxing the Rich”

American progressives often hold up Europe—especially the Scandinavian social democracies of Denmark, Finland, Norway, and Sweden—as successful tax-the-rich utopias that the U.S. should replicate. In reality, these European tax systems do not fit the American progressive image because their higher revenues are overwhelmingly raised through steep income, payroll, and consumption taxes on the middle class.

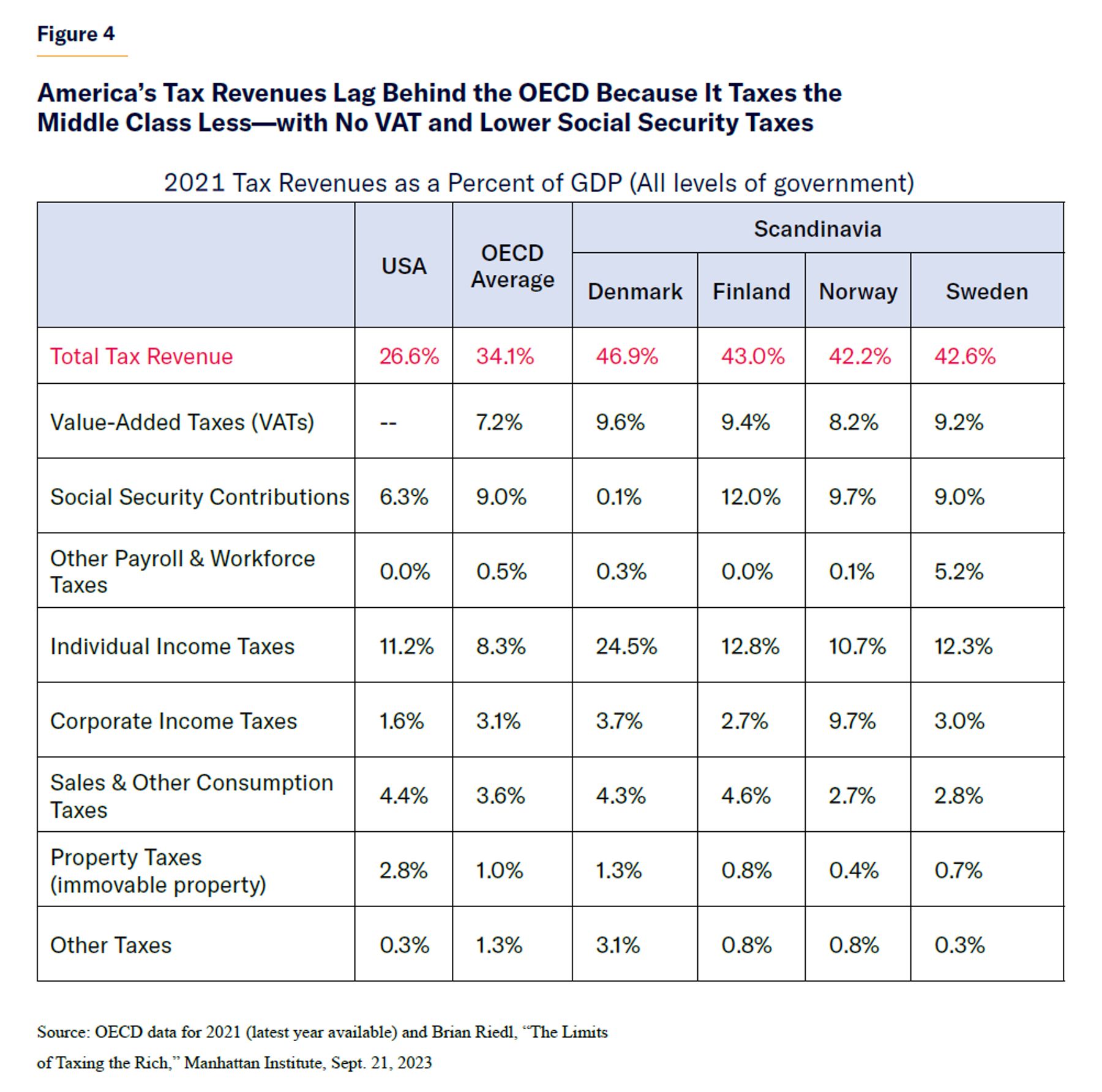

Finland, Norway, and Sweden do collect an average of 42.6% of GDP in taxes, versus 26.6% from America’s federal, state, and local governments. However, 14.5 of the 16-percentage-point overage comes from higher payroll taxes and value-added tax (VAT), which broadly hit the middle class. These nations’ individual income-tax revenues exceed those of the U.S. by just 0.8% of GDP, while their 3.5% of GDP advantage in corporate-tax revenues is overwhelmingly driven by Norway, with its massive oil and gas industry (by contrast, Finland and Sweden exceed the U.S. by 1% of GDP). These nations’ remaining taxes combined collect nearly 3% of GDP less than those in the U.S. (see Figure 4).[18]

A similar dynamic holds when comparing the U.S. with the other 37 OECD nations, which collect an average of 34.1% of GDP in tax revenues, compared with America’s 26.6%. Yet VAT revenues—which average 7.2% of GDP in OECD, versus none in America—account for nearly the entire difference. A total of 37 of the 38 OECD nations—all except the U.S.—impose VATs at rates ranging from 5% (Canada) to 27% (Hungary). The Scandinavian nations of Denmark, Finland, Norway, and Sweden each have VAT rates of about 24%–25% that collect an average of 9.1% of GDP, or roughly one-fifth to one-quarter of their total tax revenues. VATs (and, to a lesser extent, payroll taxes)—which are not particularly progressive—drive the vast majority of Europe’s tax-revenue advantage over the United States. Mimicking Scandinavia’s 9.1% of GDP in VAT revenues would require American taxes of $2.4 trillion per year, or nearly $18,000 per household.[19]

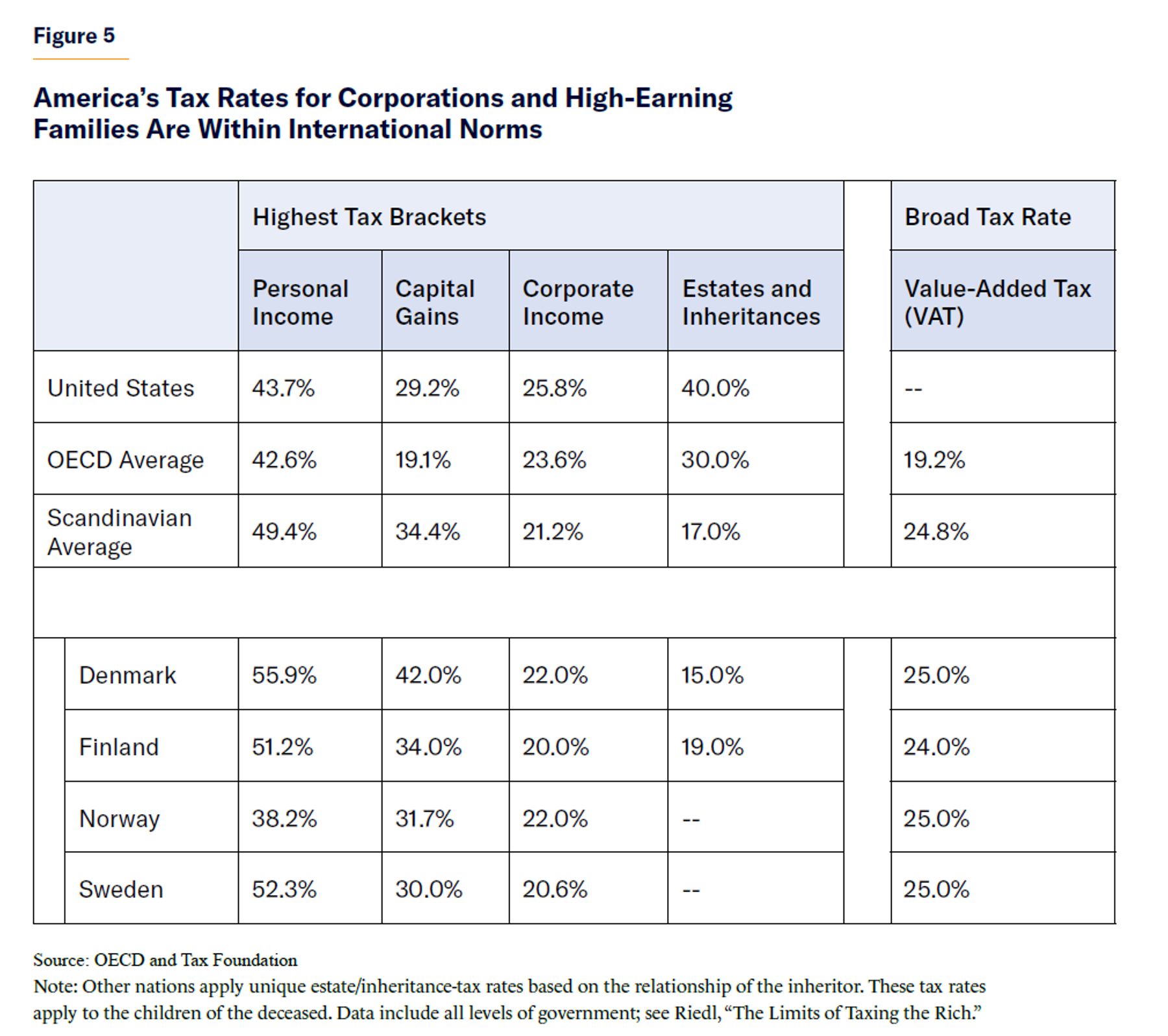

Moreover, top rates imposed on corporations and wealthy families in the U.S. often exceed OECD averages (see Figure 5). America’s top average income-tax bracket of 43.7% (including state) taxes slightly exceeds the OECD average of 42.6%. America’s highest tax brackets also exceed the OECD average for capital-gains taxes (29.2% vs. 19.1%), corporate income taxes (25.8% vs. 23.6%), and estate/inheritance taxes (40% vs. 30%). In fact, America’s corporate and estate/inheritance-tax rates well exceed those of all Scandinavian nations.[20]

Many European nations used to impose significantly higher tax rates on high-earners and corporations, as well as wealth taxes. But most of those nations abandoned such exorbitant tax rates after learning (the hard way) that such policies raised very little revenue while imposing substantial economic costs such as lower wages and fewer jobs—while driving businesses, capital, and wealth to more tax-friendly nations. Even in the U.S., the exit of several high-profile corporations to other nations—driven by a corporate-tax rate nearly double that of its competitors—forced a reduction in the corporate-tax rate in 2017 without significantly reducing corporate-tax revenues.

So while there are legitimate arguments for raising tax rates on corporations and wealthy Americans, such policies would not make the U.S. look more like Europe (or, in particular, Scandinavia), where taxes, in fact, fall very heavily on the middle class.

Myth 6: “ ‘Tax Cuts for the Rich’ Drive Soaring Budget Deficits”

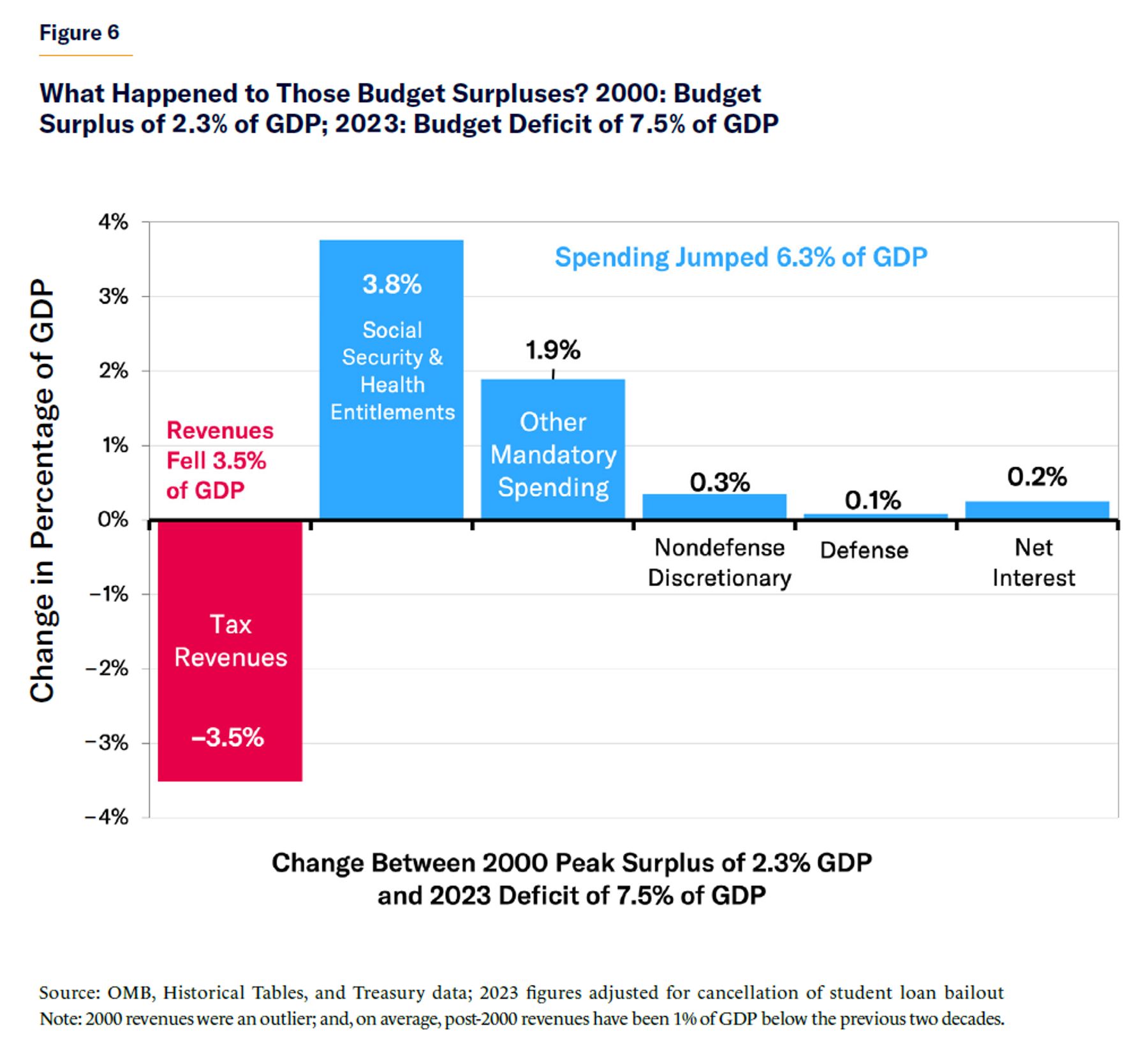

Another leading progressive myth is a reflexive tendency to blame virtually all budget deficits on Republican “tax cuts for the rich.” The budget math shows otherwise. Between 2000 and 2023, Washington’s annual fiscal position declined by 9.8% of GDP (from a 2.3% of GDP budget surplus to a 7.5% budget deficit).[21] This decline was driven by annual spending rising by 6.3% of GDP; the bursting of the 2000 revenue bubble, which reduced long-term revenues by 1.5% of GDP; and tax cuts costing 2.0% of GDP. Furthermore, more than two-thirds of the benefits from those tax cuts were distributed to middle- and lower-income families. That means that “tax cuts for the rich” have cost the federal budget 0.6% of GDP since 2000, out of a 9.8% of GDP shift from annual budget surpluses to deficits. Spending increases, economic factors, and tax cuts for the non-wealthy account for the remaining 9.2% of GDP fiscal decline (see Figure 6).

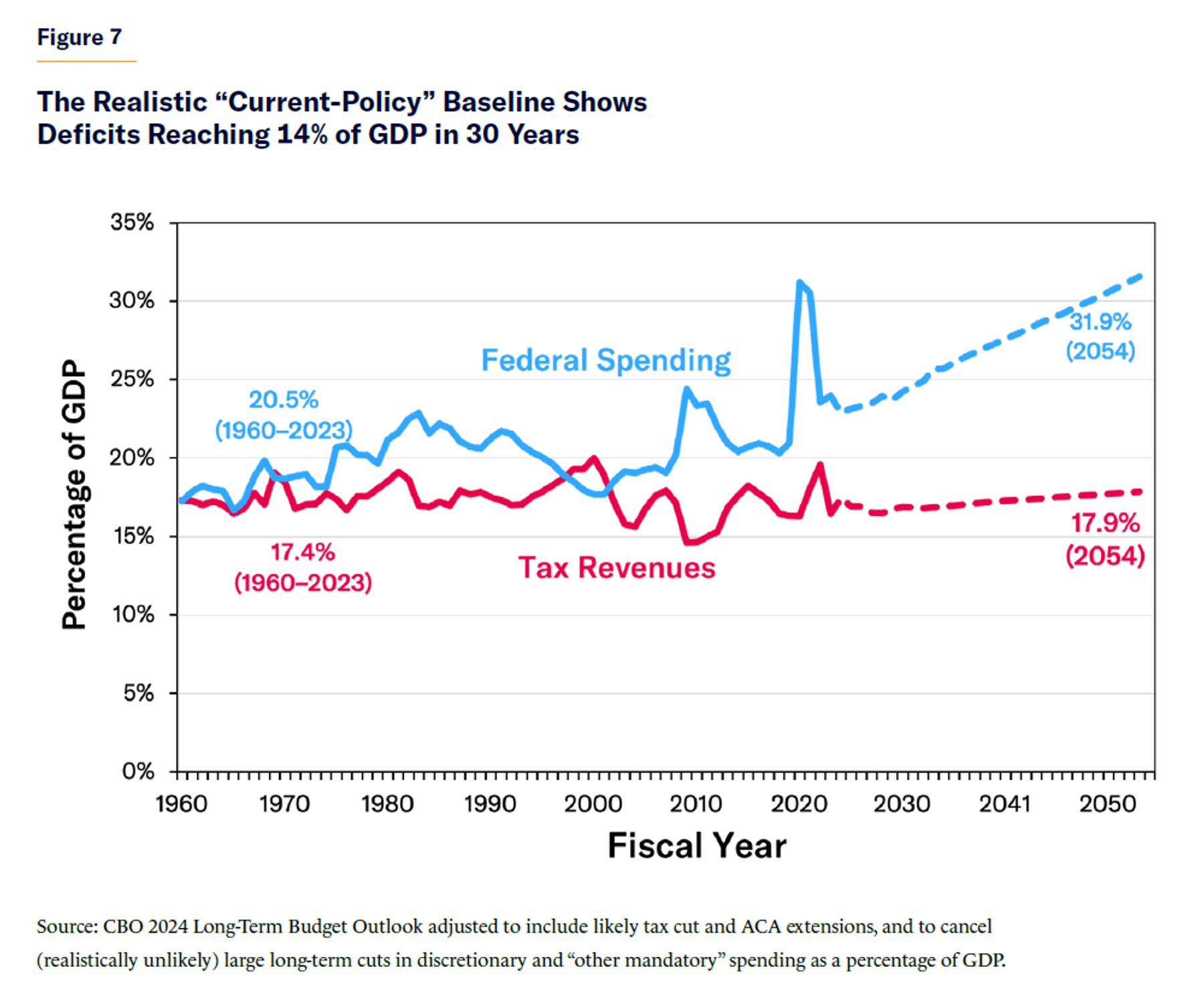

Nor are future deficit projections driven by declining tax revenues. Since 1960, tax revenues have typically remained close to their average level of 17.4% of GDP. And over the next 30 years, tax revenues are projected to range between 17.9% and 18.9% of GDP, depending on whether the 2017 tax cuts are extended. However, federal spending—which has averaged 20% of GDP since 1960—has already risen to a current level of 24% of GDP and is projected to leap as high as 32% of GDP over 30 years (see Figure 7).[22] These tax-revenue levels are surely lower than many progressives would prefer, and probably lower than the revenue level required for a bipartisan solution to stabilize the debt. But it is simply mathematically incorrect to claim that soaring projected budget deficits are driven by declining revenues rather than rising spending levels as a share of the economy. In other words, falling tax revenues are not creating the problem of surging deficits, although some degree of higher taxes will likely be part of a balanced solution.

Myth 7: “Taxing Millionaires and Corporations Can Eliminate the Deficit”

Just as “tax cuts for the rich” are falsely blamed for causing nearly all budget deficits, it is commonly claimed that raising taxes on corporations and wealthy families can eliminate budget deficits and even finance a Scandinavian-style welfare state. Once again, the uncompromising math shows otherwise.

Let’s begin with an extreme example. Even seizing all the wealth from America’s 800 billionaires—every home, business, investment, car, and yacht—and somehow reselling it all for full market value would raise only enough revenue to finance the federal government one time for eight months (while cratering the stock market, where much of that wealth had been held).[23] Taxing million-dollar earners at 100% marginal tax rates would not balance the long-term budget even if each of these taxpayers continued working for zero net pay. Only slightly more realistically, a Bernie Sanders–style tax agenda consisting of federal income-tax rates as high as 52%, capital-gains tax rates of 62%, a 35% corporate tax that includes all multinational income, a 12.4% Social-Security payroll tax on wages above $250,000, a wealth tax at a rate as high as 8%, an estate-tax rate as high as 77%, new financial transaction taxes, and countless other surtaxes and tax increases would raise, at most, 2% of GDP in tax revenues out of a current-policy budget deficit heading to 9% of GDP in a decade and 14% of GDP in three decades.[24] Even those revenue figures implausibly assume that people and corporations would continue working, saving, and investing, despite combined (federal and state) marginal tax rates on labor and investment approaching 80% to 100%. Actual tax revenues would likely increase by closer to 1% of GDP.

The mathematical reality is that there are simply not enough millionaires, billionaires, and undertaxed corporations to close a 30-year budget deficit of $115 trillion–$180 trillion (depending on the baseline used). A federal tax system that set every “tax the rich” policy dial at its revenue-maximizing levels—without regard to the resulting economic damage—could raise, at most, 1%–2% of GDP in new revenues (while surely killing jobs and lowering wages across the economy). Obviously, deficit reduction should put all policies on the table, including some new upper-income taxes. However, middle-class taxes finance most of Europe’s exorbitant spending levels, and they would have to provide the bulk of any tax-heavy solution to America’s budget deficits.

Myth 8: “Most of the 2017 Tax Cuts Went to Corporations and the Wealthy”

President Biden and other Democrats regularly decry the 2017 TCJA as nothing more than “tax cuts for the rich.” In fact, President Biden has tried to have it both ways by supporting both a full expiration of the law (including claiming full expiration revenues in his budget proposal), while also promising that taxes will not rise for any family earning under $400,000 annually. In reality, approximately 70% of TCJA’s benefits went to middle- and lower-income earners.[25]

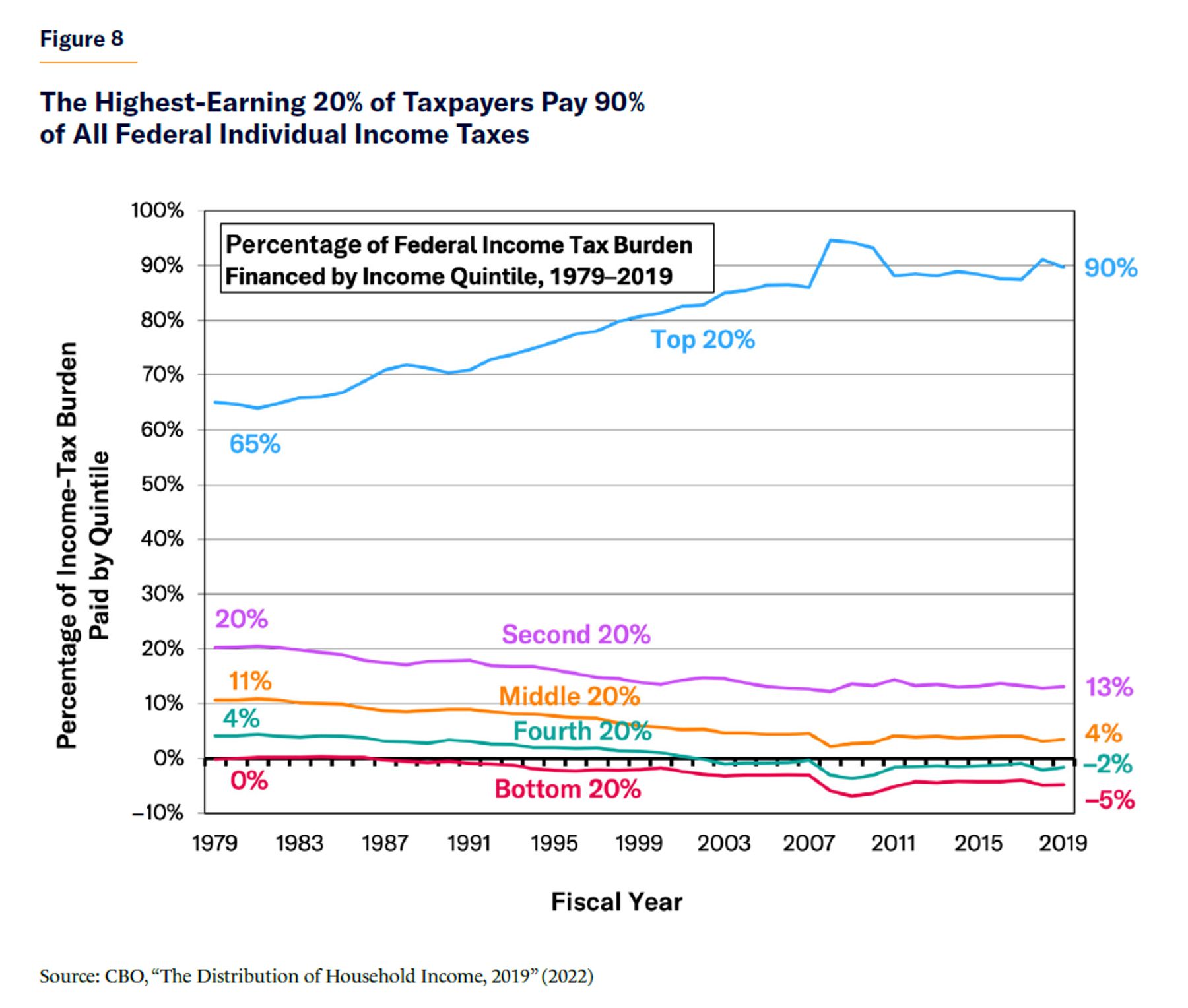

Overall, TCJA’s individual income-tax cuts were distributed roughly in proportion to the pre-TCJA income-tax burden. CBO data show that the average income-tax rate paid by each income group declined by approximately 1 percentage point between 2017 and 2019.[26] For example, the average income-tax rate paid by the highest-earning 1% fell from 24% to 23%, while middle-quintile earners saw their average income-tax rate dip from 3% to 2%. Reducing the taxes of each earning group by roughly 1% of their income means that families with higher incomes will save more actual dollars than low-earners. However, this proportional tax cut meant that the distribution of the income-tax burden remained roughly similar following TCJA, with the highest-earning 1% of families continuing to pay 39% of all federal income taxes, the top-earning quintile still paying nearly 90% of the total income taxes, and the middle-earning quintile paying 4% of all income taxes, according to CBO tax data (see Figure 8).[27]

Nor did tax cuts for large corporations contribute a large share of TCJA’s $1.5 trillion 10-year cost. The corporate-tax-rate reductions, business-expensing provisions, and other business and international tax cuts cost $1.839 trillion over the decade. However, TCJA’s corporate- and international-tax increases offset $1.519 trillion of that cost—leaving a net cost of $320 billion over the decade.[28] Even that likely overstates the cost, because Congress’s Joint Committee on Taxation determined that TCJA’s additional economic growth—resulting mostly from the corporate-tax reforms—would offset $385 billion of TCJA’s total 10-year cost.29 This suggests that the corporate- and international-tax cuts were almost entirely paid for in offsetting tax increases and additional economic activity.[30] Nearly all TCJA’s costs were driven by the individual and estate-tax cuts.

Myth 9: “Repealing All Post-1980 Tax Cuts Provides Painless Deficit Reduction”

The myth that “tax cuts for the rich” are solely responsible for rising budget deficits often gives way to calls to repeal the 2017 Trump tax cuts, the 2001 Bush tax cuts, and even the 1981 Reagan tax cuts. While repealing these would significantly increase tax revenues, such reforms would also substantially raise taxes for low- and middle-earning families (not just the wealthy), and repeal some broadly popular tax reforms.

For starters, repealing the 2017 tax cuts would mean significant across-the-board tax increases. The $2,000 child credit would fall to $1,000, marginal tax rates would rise, and more families would be required to itemize their tax returns just to receive the same tax savings. Overall, the Tax Policy Center notes that repealing the 2017 tax cuts would raise taxes by roughly $1,000 for the typical median-earning family, and nearly $1,600 for families with average incomes.[31] Returning the corporate-tax rate to 35% (and repealing the savings that offset much of this tax-rate reduction) would also bring back the highest corporate-tax rate in the developed world.

Going further, returning to the 2000 federal tax code—which includes repealing both President Trump’s 2017 tax cuts and President George W. Bush’s 2001 tax cuts—would raise taxes even higher. Repealing those laws would further reduce the child tax credit to $500, bring back the “marriage penalty” that raised taxes on married couples, and raise even the bottom tax brackets. Such policies would bring new income-tax liabilities to more than 10 million families that have been removed from the income-tax rolls by the 2001 and 2017 tax cuts.[32]

Kyle Pomerleau of the American Enterprise Institute calculated that returning to the 1997 tax code (roughly similar to 2000 for income taxes, while also preceding the 1998 implementation of the initial $500 child tax credit) would raise income and payroll taxes by $3,410 per family. This includes higher taxes of $3,054 for median earners, $1,139 for the second-lowest earning quintile, and $6,195 for above-average earners in the second-highest earning quintile. The top-earning 1% would see a typical tax increase exceeding $25,000. Additionally, by returning to the 1997 parameters for the Alternative Minimum Tax (AMT), which was not automatically indexed for inflation, nearly 50 million Americans would lose the value of many of their tax preferences.[33]

Most aggressive are calls for repealing the past four decades of conservative tax reforms and returning to the 1980 pre-Reagan tax code. Many progressives may welcome a return to that era’s top income-tax bracket of 70%. But the rest of the 1980 tax code would mean dramatically higher taxes across the board. CBO reports that returning to the average tax rates of 1980 would mean an 11-percentage-point increase in average income-tax rates for the bottom-earning quintile, a 6.2-percentage-point increase for the second-lowest quintile, a 5.5-percentage- point increase for middle-earners, and a 4.7-percentage-point increase for the second-highest quintile. Meanwhile, the highest quintile’s income taxes would rise by just 1.2 percentage points. For the median-earning family, this would translate to a $4,500 tax increase.[34]

Yet even these figures downplay the tax hike. One of the central (and costliest) aspects of the 1981 tax cuts was the requirement that all future income-tax-bracket thresholds be adjusted annually for inflation. Before then, the high inflation of the 1970s automatically pushed families into higher income-tax brackets even if their incomes rose only enough to cover inflation (Congress had occasionally passed laws raising the income-tax-bracket thresholds, but not by enough to keep up with inflation). Truly canceling all post-1981 tax cuts would mean returning to an income-tax code that was not indexed for inflation and remained at 1980 tax brackets. Accordingly, a married couple with two children earning $70,000 today would find itself in a 54% marginal tax bracket under the 1980 tax code. Even an impoverished couple with two children earning just $20,000 would find itself in a 21% marginal tax bracket.[35] Families earning $120,000 would face a top marginal income-tax rate of 64%. This is all in addition to payroll, state, and other taxes that add as much as 28% to marginal tax rates.

Clearly, the tax cuts of 1981, 2001, and 2017—much maligned by progressives—reflect a broad bipartisan consensus against dramatically higher tax rates for low- and middle-income families. High-earners surely saved money as well, although most of the total deficit cost of these tax cuts came from families outside the top-earning 10%.

Notably, although there have been major tax cuts since 1980, income-tax revenues as a share of the economy have remained steady and even slightly increased. This is partly because many of the tax cuts merely offset an automatic long-term tax increase known as “real bracket creep.” Even though the thresholds of each income-tax bracket are now automatically indexed to inflation, income and wages typically grow faster than inflation, thus moving many families into higher marginal tax brackets. This raises their average income-tax rate over time. As average tax rates rise, real bracket creep has historically increased annual income-tax revenues by as much as 0.3%–0.5% of GDP each decade. Consequently, income-tax cuts of roughly 1% of GDP every 20 years (in 1981, 2001, and 2017) essentially canceled out real bracket creep and returned average income-tax rates closer to the earlier levels.[36] Put simply, the federal income-tax code automatically raises average income-tax rates over time, and occasional tax cuts can reverse those tax increases and return average tax rates to normal levels.

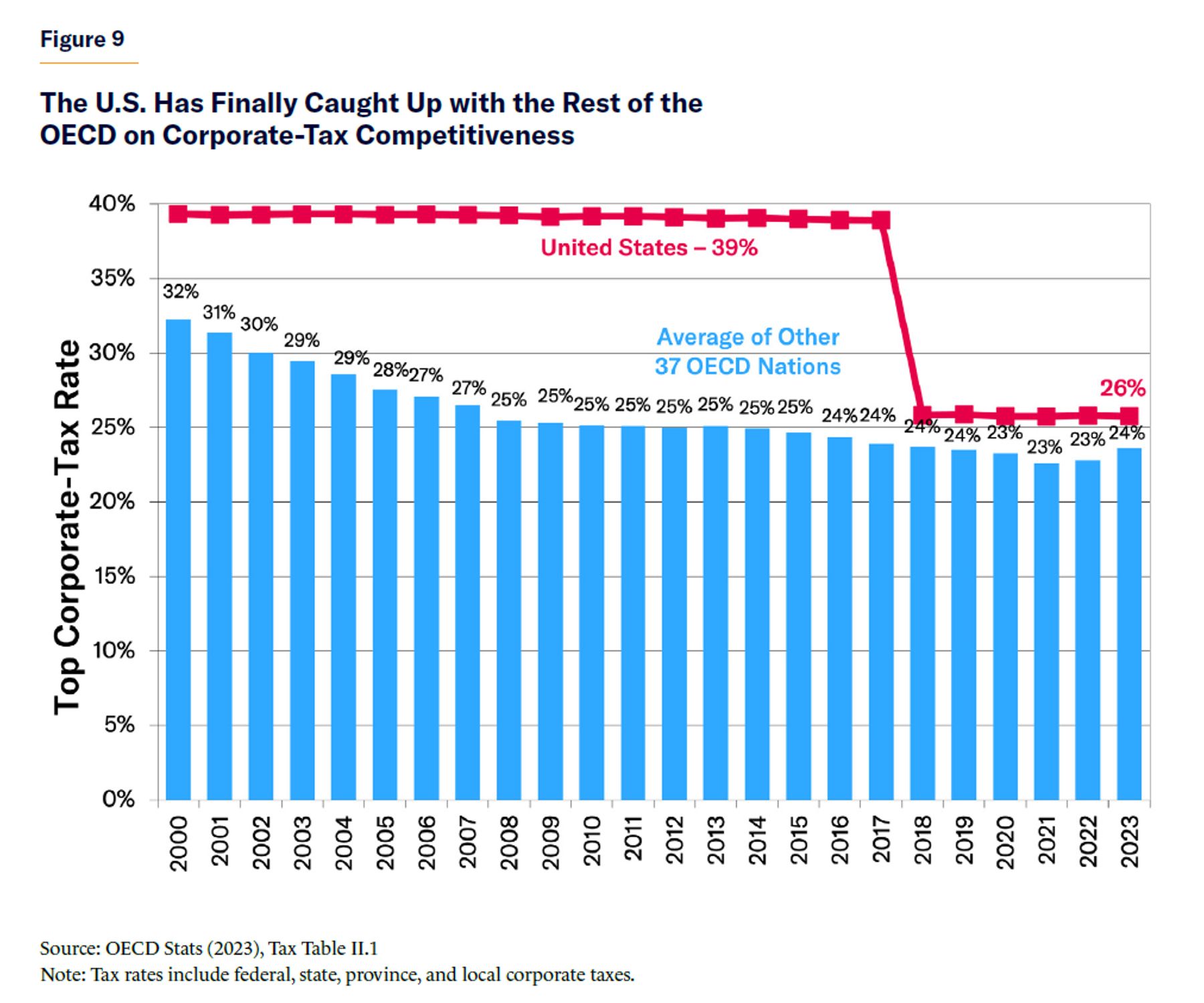

Myth 10: “America’s Corporate Taxes Are Far Below International Standards”

Advocates of substantially higher corporate taxes often assert that the U.S. currently coddles corporations by taxing them far below international norms. Once again, this is false. When including state taxes, America’s 25.8% statutory corporate-tax rate is tied for the 13th-highest among 38 OECD nations—and exceeds all four Nordic nations, which range from 20% to 22%. In fact, before the 2017 tax cuts, the U.S. corporate-tax rate of 39% (including state taxes) exceeded that of all other OECD nations (see Figure 9).[37]

Yes, tax preferences lower the effective tax rate paid by American corporations—just as they do for corporations in other nations. Yet America’s composite effective average tax rate of 22.3% exceeds that of the OECD average and all Scandinavian nations.

Despite lower average tax rates, America’s current 1.8% of GDP in corporate-tax revenues slightly trails the 2%–3% of GDP collected by Germany, France, Finland, Sweden, and the United Kingdom. However, the U.S. figure rises to 3.0% of GDP when including the taxes paid by pass-through businesses, which are processed through the individual income-tax code.

The long-term global trend has been for nations to reduce corporate-tax rates in order to attract investment, enhance competitiveness, and raise wages. Since the 1980s, the average worldwide corporate-tax rate has fallen from 40.1% to 23.4% (or from 46.5% to 25.4%, when weighted by GDP). Within the OECD, the average corporate-tax rate since 1980 has fallen by half, from 47% to 23.6%—yet corporate-tax revenues have increased by 0.5% of GDP among the same group of nations.

Extending the period to 1965–2019 shows OECD corporate-tax revenues jumping from an average of 2.1% to 3.0% of GDP, despite (or, perhaps, driven by) substantial reductions in corporate-income-tax rates. All in all, U.S. corporate-tax rates and broad business-tax revenues (including pass-through businesses paying the individual income tax) are comfortably within the European and OECD consensus.

Conclusion

Destructive tax policies often result from both parties relying on a series of outdated, simplistic, and false assumptions about the federal tax system and its relationship to the economy. With budget deficits soaring and Congress preparing for the potential renewal of the 2017 tax cuts, it is more important than ever for both sides to challenge their assumptions and rely on modern tax data and research to guide their approaches. Otherwise, an excessively flawed tax code risks punishing families, discouraging economic growth, and lacking sufficient revenue to finance the federal government.

Bonus Section of Smaller Myths

Myth: “Tariffs Are Taxes on Foreigners, Not Americans.” A tariff is a tax paid by U.S. importers of foreign goods. The purpose is to raise the price of imports so high that American consumers switch to lower-priced domestically produced alternatives. Thus, the tax is directly paid by the American company importing the good and then passed on to American consumers in the form of higher prices. Imposing tariffs on Chinese goods does not mean that China will send a tariff tax payment to Washington, DC.

Myth: “Uncapping the FICA Tax Can Fund Social Security Forever.” Social Security’s annual funding shortfall is projected to level off around 1.6% of GDP by the 2030s. Applying Social Security payroll taxes to all income would raise federal revenues by approximately 0.9% of GDP—closing roughly half the Social Security shortfall (even if these added taxes earn no additional benefits). In fact, the Social Security Administration calculates that, even if the cap were eliminated, Social Security would return to deficits within five years. Furthermore, uncapping the FICA tax would essentially use up all available tax-rate hikes on the rich, leaving none left to close the larger Medicare shortfall, or finance other progressive priorities. In that context, subsidizing (mostly wealthy) baby boomers is an odd way to spend all remaining income taxes available from the rich.[38]

Myth: “TCJA Dramatically Raised Low-Income Taxes.” Shortly after TCJA was enacted, Nobel laureate Joseph Stiglitz asserted in the New York Times that lowearners would see a net tax increase under the law.[39] This false claim was based on a misreading of a tax distribution table released by the Joint Committee on Taxation.[40]

That table combined two different sets of reforms: 1) The 2017 tax provisions that reduced taxes across the board (with minor exceptions at higher incomes); and 2) A provision allowing families to voluntarily opt out of the Affordable Care Act’s (ACA) individual mandate to purchase health coverage. Families who no longer have ACA health coverage expenses would no longer need federal reimbursements of those expenses. Stiglitz misread the end of these federal health reimbursement payments as a TCJA tax increase, even though this separate health-care reform was voluntary for families and created no new net costs (i.e., opting out of both a $2,000 coverage cost and accompanying $2,000 reimbursement of that cost). TCJA contained no provisions that would raise taxes on a large number of low-income families.

Myth: “Payroll Taxes Fund All of Medicare.” The 2.7% Medicare payroll tax raises 1.6% of GDP annually and is projected to remain at this level over the long term. Yet Medicare spending—net of Medicare premiums paid—is 3.1% of GDP and set to rise to 5.4% of GDP over three decades.[41] Thus, Medicare is projected to produce a 30-year shortfall of $49 trillion (which will, in turn, raise national debt interest costs by $38 trillion over that period).[42] Such unsustainable shortfalls will require some combination of reduced health spending, higher revenues, and higher Medicare premiums.

Myth: “The SALT Deduction Eliminates Double Taxation.” Double taxation occurs when the same government entity taxes the same income twice in a similar fashion, before that income can be applied to a new income-producing transaction.

For example, the federal government assesses income taxes and then estate taxes on the same earnings. However, applying both federal and state taxes to the same income is not double taxation because they represent different levels of government taxing income for their own unique purposes. Paying federal taxes to finance the military and also paying state taxes to finance schools does not represent duplicative taxation. This means that the federal deduction for state and local taxes (SALT)—which is meant to offset “double taxation” between state and federal taxes—is logically unnecessary.One level of government is under no obligation to provide a tax deduction for the tax-and-spending activities of a different level of government.

Myth: “Corporate Taxes Are Paid by Corporate Fat Cats.” Corporate taxes are not paid out of the CEO’s salary or by a nameless, faceless corporate entity. A company is just a collection of owners and workers who serve customers. Thus, the cost of corporate taxes must ultimately be passed on to one or more of the firm’s: A) owners, through lower investment returns; B) workers, through lower wages; or C) customers, through higher prices.[43] Even the owners typically consist not of fat-cat billionaires but rather, millions of individuals holding company stocks in mutual funds and index funds in their retirement plan. Thus, corporate taxes typically cost workers, consumers, and Americans with retirement plans. Very little is coming out of the CEO’s pocket.[44]

Myth: “Tax Rebates Grow the Economy by Putting Money in People’s Pockets.” The government budget restraint shows that every dollar that federal spending injects into the economy must first be taxed or borrowed out of the economy.[45] The same budget restraint means that every dollar of tax cuts that adds purchasing power must be financed by either government spending cuts (if offset by Congress) or additional government borrowing (if added to the deficit)—both of which remove a dollar of purchasing power from the spending recipient or investor. This means that tax rebates merely redistribute existing purchasing power. And while some suggest that such policies increase demand by redistributing money from savers to spenders, the reality is that the vast majority of savings would have otherwise been recirculated into spending through the financial system anyway. Nor do tax rebates add to the economy’s supply side by encouraging production. Consequently, tax rebates have typically failed to produce their intended economic growth results.[46]

Myth: “Supply-Side Policies Are About Giving Rich People Money to Spend.” As a corollary to the myth above, critics claim that supply-side tax cuts merely give rich people money to spend in the hopes that their purchases will trickle down to the rest. But that is a Keynesian, demand-focused framework. Supply-side economics recognizes that tax cuts may not immediately increase demand—as the offsetting spending cuts or government borrowing will negate any increase in purchasing power—but that lower marginal tax rates may encourage people and businesses to work, save, invest, and be productive, thus expanding the economy’s supply side and bringing growth. In other words, the economic growth is driven not by the tax cut itself but by the resulting behavioral changes that produce more output. Such policies need not be aimed at wealthy individuals—and indeed, may instead take the form of supply-side

spending programs that are meant to encourage work and productivity.

Endnotes

Photo by Spencer Platt/Getty Images

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).