When Government Sets Hospital Prices: Maryland's Experience

Photo: Peter Horrox / iStock / Getty Images Plus

“Medicare for All” proposals may vary greatly, but a common feature is their call for the regulation of prices for hospital care. This element has widespread support among establishment Democrats, and it lacks the enormous cost and controversy associated with other aspects of single-payer health care.

Comprehensive hospital-payment regulation is not a new idea: it’s been widely tried at the state level for half a century, including in Maryland—the only state where it remains. Maryland therefore provides a useful case study.

This report describes the history and workings of Maryland’s all-payer hospital-payment system. It reviews the arguments made in its favor as well as the causes for concern that have been raised. And it performs a comprehensive assessment of the state’s health-care system—in terms of cost, quality, and access to care.

Rather than reducing health-care costs in any significant way, Maryland’s payment-regulation experiment has, as this report explains, been captured by the hospitals that it was intended to regulate. The regulation is loose and does little to distinguish the state from its peers in a variety of metrics—except for one crucial fact: the system allows the state to claim higher reimbursements from the federal government for Medicare patients. Decades of regulations have induced unintended consequences, too, which have been patched with further regulations, inducing further unintended consequences. Nevertheless, Maryland’s payment system survives because it entitles the state’s hospitals to a unique $2 billion annual windfall from Medicare.

The broader lesson: Maryland-style hospital-payment regulation is not a solution to the problems resulting from the absence of competitive market forces in U.S. hospital care. It is, instead, a product of the protectionist political dynamics that have prevented such competition from emerging. The adoption of all-payer rate-setting on a national level would establish additional barriers to price competition, thereby making it harder to reduce America’s health-care costs.

Introduction

Government regulation designed to slow the growth of hospital prices is a common feature of current single-payer health-care reform proposals among U.S. Democratic presidential hopefuls.[1] Regulating hospital prices while maintaining private insurance is widely acknowledged to be more politically feasible than single-payer health care, and is therefore embraced by some advocates as a “back-door to single-payer.”[2]

Hospital-payment regulation has been tried at the state level for many years. It remains in existence in Maryland, where a regulatory commission sets prices to be paid—by private insurers, government programs, and individuals—for every medical service delivered by each of the state’s 46 hospitals. Advocates argue that this arrangement prevents hospitals from using their market power to inflate prices, discourages hospital facilities from incurring unnecessary costs, and guarantees better access to care for needy communities.

Yet after more than four decades, health care in Maryland is not, as this paper demonstrates, perceptibly cheaper than in neighboring states; levels of quality and access to care are not significantly different, either. The system’s complex rules, however, do prevent cheaper providers from challenging incumbents and prohibit insurers from negotiating discounts with in-network hospitals.

Why, then, does Maryland’s system endure? One big reason: it allows the state’s hospitals to charge the federal government 40%–60% more for Medicare services than do hospitals in other states. This $2.3 billion annual windfall to Maryland’s hospitals helps keep politically powerful stakeholders incentivized to preserve the status quo.

The Argument for Hospital-Payment Regulation

Ongoing proposals for the comprehensive purchase of health-care services by the U.S. government (“single-payer health care”) have stirred much controversy. Because adopting single-payer health care would require enormous increases in taxes and the abolition of private insurance, sophisticated advocates of greater government control of health-care services tend to prefer an alternative arrangement, “all-payer rate-setting.”

Under such a model, the government would control the price, quality, volume, and apportionment of medical services delivered, without necessarily eliminating the management of claims by private insurers, employer contributions for coverage, or market-driven innovations in the package of benefits available to enrollees. Variations of the all-payer model exist in, among others, Switzerland, Germany, and France. (Before it deregulated, the Netherlands also had an all-payer model.)[3] In the U.S., all-payer rate-setting regulations that fix prices across the board for hospital care were once common at the state level. Today, they remain in effect only in Maryland.

Although increased spending under the 2010 Affordable Care Act (ACA) may have reduced the number of Americans without health insurance, the ACA has failed to reduce the actual cost of medical care. For example, from 2000 to 2019, average prices for hospital services doubled, even after accounting for the general rate of inflation.[4] A group of prominent liberal health-policy analysts, senior Obama administration officials, and Democratic politicians has argued that the ACA should be followed by a second wave of reforms to constrain the growth of health-care costs, the centerpiece of which would be all-payer rate-setting.[5]

According to this view, payment regulation would limit the market power of hospitals, which seek to impose ever-higher rates. Because insurers often pass inflated costs on to employers, insurers lack sufficient incentives to negotiate good rates by, say, threatening to exclude hospitals from their networks.[6] Payment regulation would incentivize insurers to focus on improving their benefit packages and offering lower premiums rather than wielding their market power to extract discounts from hospitals.[7] (In recent years, hospitals have used the threat of exorbitant rates for emergency care to out-of-network patients to force insurers to agree to increasingly generous payment terms for in-network care.)[8]

Even if regulated prices were established at existing rates, some analysts believe that they could save money over time by slowing the growth of costs:[9] fixed fees might discourage hospitals from making costly investments to expand capacity, while encouraging hospitals to shed costs involved in the delivery of care—by reducing lengths of stay, eliminating overcapacity, and implementing cost-reducing innovations. Price caps could also protect low-income patients from paying for increases in the level of care that they cannot afford; or prevent hospitals from inflating costs by spending on amenities that are intended to attract wealthier, privately insured patients.[10]

By seeking a more equal distribution of costs between payers, all-payer rate-setting aims to avoid the phenomenon whereby hospitals overcharge privately insured patients in order to cross-subsidize indigent care.[11] While uninsured patients are often charged more than twice the rates that insurers must pay for care, Maryland designed its system of fixed prices to entitle uninsured patients to the same rates paid by most private insurers.[12] This may help rationalize the financing of uncompensated (charity) care by making hospitals more transparent about the amount of it that they provide.

Hospitals located in communities with large numbers of uninsured, or underinsured, patients tend to struggle financially because they must provide substantial amounts of care for which they are not compensated. The traditional business model of nonprofit hospitals is to cross-subsidize charity care by overcharging privately insured patients, but their capacity to do so may be threatened by price competition. The Maryland model attempts to secure both the solvency of hospitals and access to care for patients in low-income communities by controlling the expansion of capacity by potential competitors or the ability of managed-care organizations to constrain hospital revenues.[13]

For its boosters, all-payer rate-setting can eliminate the costs of negotiating over fees and reduce the administrative burden of dealing with multiple prices for the same service.[14] By aligning billing systems across multiple payers, all-payer rate-setting can also facilitate the deployment of innovative payment reforms that are oriented toward politically determined “social value” priorities rather than consumer demand.[15]

In rural areas, there may not be sufficient patient volumes to generate revenues to support high-quality, full-service hospitals. Maryland’s exemption from standard Medicare payment rules makes it easier to concentrate public subsidies on maintaining essential emergency-care services. By penalizing hospitals for exceeding aggregate spending targets, Maryland hopes to discourage hospitals from inflating the volumes of services provided, to encourage the use of cost-effective treatment alternatives, and to discourage readmissions.[16]

The Maryland Model: A Brief History

Until the 1980s, most health insurers and entitlements programs in the U.S. paid hospitals according to the costs that they incurred in delivering care. Such open-ended, cost-based reimbursements greatly inflated the expense of hospital care.[17] As hospital spending more than doubled in real terms between 1960 and 1970, employers, as well as federal and state governments, were eager to constrain rising costs.[18] Section 222 of the Social Security Amendments Act of 1972 gave states the authority to establish uniform-payment arrangements for hospital services by establishing exemptions from Medicare’s cost-based payment requirements.[19]

With Maryland’s hospital costs 24% above the national average, the state was eager to cap the reimbursements that hospitals could claim from public and private payers.[20] Maryland legislators thus initially proposed hospital-rate regulation to slow rising costs. Yet they were able to win the support of the Maryland Hospital Association because the state’s hospitals desired help financing the growing levels of uncompensated care.[21] Following the lead of New York, Maryland established an independent agency in 1971, the Health Services Cost Review Commission (HSCRC), with the authority to set rates for hospital inpatient care, starting in 1974.[22]

Maryland’s all-payer rate-setting system initially required annual waivers from standard Medicare and Medicaid payment arrangements to be approved by the U.S. Department of Health and Human Services. However, in 1980, Rep. Barbara Mikulski (D., Maryland) successfully sponsored federal legislation that granted Maryland the unique right to automatic reapproval, conditional on meeting a “waiver test.”[23]

Under the waiver, Maryland could set its own Medicare rates (and claim whatever associated additional revenue might come from the federal government), so long as: (1) the same rates also applied to Medicaid, private insurers, and individuals purchasing care out-of-pocket; and (2) the cumulative rate of increase in Medicare payments per inpatient admission relative to January 1, 1981, was less than the U.S. average.[24]

Connecticut, Maine, Massachusetts, Minnesota, New Jersey, New York, Washington, Wisconsin, and West Virginia also established systems to regulate rates paid by private insurers for inpatient hospital care. In Massachusetts, New Jersey, and New York, as well as in Maryland, these regulated rates applied to Medicare, too. However, only Maryland sought to entrench its waiver from Medicare rates into federal law.[25]

The Tax Equity and Fiscal Responsibility Act of 1982 established a detailed set of payment rates for Medicare inpatient hospital care, displacing cost-based reimbursement nationwide. New York and Massachusetts allowed their waivers from the national system to expire in 1985, followed by New Jersey in 1989, as academic medical centers in that state estimated that the new national rates would allow hospitals to reap lucrative Graduate Medical Education add-ons (federal subsidies for hospitals that train medical residents).[26]

As managed care began to allow private insurers to constrain hospital spending through the formation of networks of preferred providers—which allowed insurers to negotiate discounts of 30%–40% from statutory rates and reduced volumes of services—rate regulation no longer seemed necessary to reduce costs.[27] As hospitals were no longer able to reap guaranteed revenue from protected markups that had been designed to allow them to cross-subsidize uncompensated care, liberal support for rate-setting faded.[28] Massachusetts abandoned the regulation of rates paid by private insurers in 1991, followed by New Jersey in 1992, and New York in 1997.[29]

As the only all-payer state under unified Democratic Party control throughout the 1990s, Maryland enacted tough limits on the discounts that hospitals could provide to insurers.[30] The state banned any discount greater than 4%, while permitting discounts only for a subset of plans meeting specific benefit and enrollment regulations.[31]

Over the past three decades, Congress repeatedly enacted legislation that cut rates paid by Medicare and Medicaid for hospital services in return for expansions of Medicaid eligibility.[32] Growing hospital consolidation and a legislative backlash to managed care at the state level weakened the negotiating power of health maintenance organizations (HMOs) and empowered hospitals to demand ever-higher reimbursements from private insurers.[33]

These trends have widened the nationwide disparity between private and Medicare rates: in 1997, private rates were 13% higher; in 2016, they were 67% higher. As a result, the value of the waiver allowing Maryland to claim Medicare reimbursements from the federal government at the same rates that it sets for private insurers has soared.[34] While Medicare reimbursements per case in Maryland increased from $2,876 in 1996 to $4,150 in 2007, they rose only from $2,484 to $3,047 nationwide.[35] According to one estimate, in 2014, the waiver brought Maryland an additional $2.3 billion in Medicare and Medicaid revenue from the federal government—a substantial portion of the state’s $16 billion total hospital revenues.[36] While Maryland’s commercial hospital payment rates in 2015 were 13% lower than national levels, its Medicare rates were 40% higher than standard rates for inpatient services and 60% higher for outpatient services.[37]

The Maryland Model: A Closer Look

Maryland’s hospital-payment regulation system is managed by the Health Services Cost Review Commission, a seven-member independent commission appointed by the governor to staggered four-year terms. HSCRC has broad discretion to fix payments for hospital services.[38] Its enabling legislation sets out five goals:[39]

- Constrain hospital costs

- Ensure access to hospital care for all citizens

- Improve the fairness of hospital financing

- Secure financial stability for hospitals

- Make all institutions accountable to the public

The payment system for hospital inpatient care established by HSCRC resembles that of Medicare, but it has long differed in two important ways. First, whereas Medicare pays all hospitals according to the same rules, Maryland’s payments to hospitals built upon price differences between hospitals at the time the system was established. Second, whereas Medicare pays hospitals fixed amounts per patient admitted per given diagnosis, Maryland both caps the total amount that hospitals may charge for patients in aggregate and allows hospitals to vary the amount billed from patient to patient, according to the specific costs incurred in delivering services.[40]

As hospital costs consist, to a large extent, of fixed costs (50%, according to HSCRC’s estimate), their incorporation into regulatorily established rates provides a significant incentive to inflate volumes, by increasing the number of admissions or by unbundling care into multiple claims.[41] Until recently, Maryland’s payment model did little to constrain attempts by hospitals to drive up revenues by inflating their number of reimbursement claims, other than adjusting rates to slightly redistribute funds from relatively high-volume to low-volume hospitals to counterbalance fluctuations in demand.[42]

For many years, inflated volumes made it easier for Maryland to meet its Medicare waiver test (keeping the growth of Medicare costs per inpatient admission below the U.S. average). Yet over time, this dynamic became increasingly outweighed by other incentives of the state’s system. Specifically, fixed fees for inpatient care encouraged hospitals to shift services to outpatient facilities, which were exempt from price regulations. This practice left hospitals delivering inpatient care to cases with disproportionately complex medical needs. The result: Maryland’s Medicare costs per admission began to increase relative to the rest of the nation.[43] As the growth of national Medicare costs began to slow, Maryland came increasingly close to failing its waiver test (with the margin by which it met its goal shrinking from over 10% during 1998–2010, to 2% during 2012–14). The margin is expected to continue declining, putting the state’s lucrative revenue bonus at risk.[44]

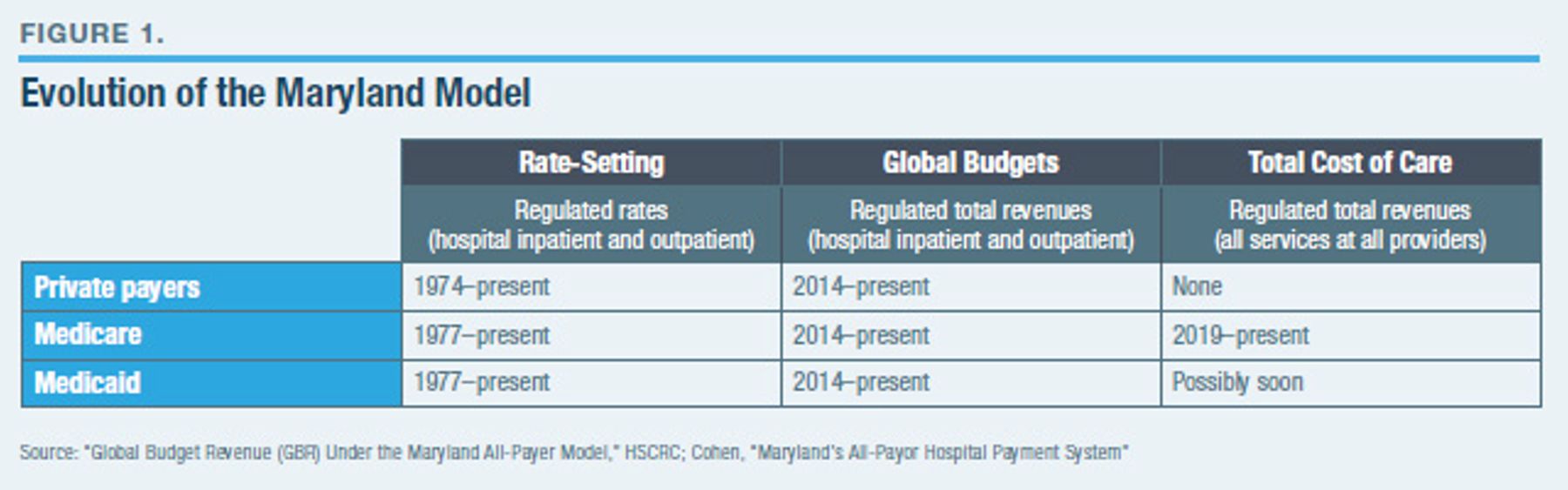

In 2014, Maryland abandoned its traditional waiver and rate-setting system, replacing it with a new agreement with the federal government, “Global Budgets” (Figure 1), under which Maryland regulates hospitals’ total revenues as well as their rates. (Such a system had been tried since 2011 in 10 of the state’s rural hospitals, with the objective of guaranteeing revenue levels to facilities delivering care to geographically defined populations.)[45]

Starting in 2014—to address concerns about inflated volumes and to qualify for the waiver that allowed its hospitals to claim Medicare reimbursements above standard rates from the federal government—Maryland was required to meet the following statewide criteria:[46]

- Hospital revenue per capita not growing more than 3.58% per year

- Medicare hospital spending reduced by $330 million over five years relative to the U.S. average

- Medicare total spending growth lower than the U.S. average

- Hospital-acquired medical conditions, such as infections, reduced by 30% over five years

- Medicare readmissions rate reduced to the U.S. average within five years

Although hospitals are allowed a set Global Budget, they are paid on a fee-for-service basis. HSCRC established a target Global Budget of allowed spending for all hospital services (inpatient and outpatient but excluding physician fees) at each of Maryland’s 46 hospitals, based on existing levels of spending and annual updated factors (discussed below). For each hospital, targets were divided by the expected volume of medical cases to be treated in order to calculate permitted rates for various patients and services.

Hospitals are allowed to adjust rates up or down (by 10%, with permission from HSCRC; and by 5%, without HSCRC’s permission) within the year to reach their Global Budget targets.[47] Hospitals that fail to hit their targets have their Global Budgets for the subsequent year reduced by up to 50% of any overspending; underspending hospitals are allowed to make up for the revenue shortfall with an increase in the Global Budget for the subsequent year of up to 1.4%.[48]

Global Budget targets are updated annually to adjust for inflation of input prices, improvements in productivity, and upgrades to hospitals.[49] These adjustments also include rewards or penalties for performance on a variety of metrics relating to efficiency, adherence to care processes, mortality rates, readmissions, and hospital-acquired conditions.[50] Further adjustments are made to account for shifts in the share and pattern of demand for various services between hospitals, the age and growth of populations in hospital catchment areas, levels of uncompensated care, the number of patient transfers to academic medical centers, growth in demand for costly specialized services, and other miscellaneous factors.

Following the ACA and the Medicare and CHIP Reauthorization Act (MACRA) of 2015, the Obama administration became increasingly keen to reform Medicare from retrospective fee-for-service reimbursements toward prospective capitated payments that would empower integrated medical systems to take responsibility for the total medical costs of beneficiaries within designated catchment areas.[51] In most states, it has been hard to entice providers to participate in such arrangements; but Maryland hospitals were willing to accept such a shift in order to receive reauthorization of the lucrative waiver bonus to standard Medicare rates.

To address concerns that Maryland hospitals were evading cost controls with inflated volumes of care at off-campus outpatient settings, a new arrangement was established whereby hospitals bear some responsibility for the total cost of care (TCOC) incurred by Medicare beneficiaries assigned to them. Hospitals’ participation in this arrangement was voluntary from July 2017 to December 2018; in January 2019, it became mandatory under a new waiver agreement that requires the state to:[52]

- Achieve all-payer total hospital per-capita revenue growth of no more than 3.58% per year

- Achieve Medicare annual TCOC savings of $300 million by the end of 2023

- Establish population-centered quality measures

Under this new arrangement, each hospital is partially responsible for the TCOC delivered to a designated portion of the state’s Medicare beneficiaries. Patients are automatically assigned to hospitals depending on the referral patterns of their primary-care physician or their geographic location (if association with physicians can’t be identified).[53] If total Medicare spending on hospitals’ attributed beneficiaries exceeds a permitted benchmark, hospitals face penalties of up to 0.5% of federal Medicare revenue for the following year.[54] This benchmark is updated annually by the expected nationwide growth of Medicare spending (minus one-third of a percentage point) and is adjusted for demographic change.[55] Hospitals are expected to restrict access to care and pass incentives on to associated physicians to reduce costs.

To get the support of physicians, Maryland, in conjunction with the Centers for Medicare and Medicaid Services (CMS), established the Maryland Primary Care Program (MDPCP).[56] Starting in 2019, physicians receive additional monthly payments from the federal government in return for monitoring Medicare patients and more closely integrating with hospitals responsible for reducing Medicare patients’ TCOC.[57]

TCOC or MDPCP programs apply only to Medicare beneficiaries. While they may soon be extended to Medicaid enrollees, there are no moves to apply such incentives to the delivery of care to privately insured patients. Indeed, no state has ever established all-payer rate-setting that includes physician fees, and Maryland has no plans to do so in the foreseeable future.[58]

The Flaws of Maryland’s Hospital Price-Fixing System

In his landmark 1971 article “The Theory of Economic Regulation,” Nobel Prize–winning economist George Stigler argued that regulation is often sought and shaped by incumbents to retard the entry of new firms, in order to allow what otherwise would be a competitive industry to act as though it were a monopoly.[59] Maryland’s regulatory system has been subject to such pressures.

In a free market, cartels seeking to collude for the sake of fixing prices face the threat of new entrants, the risk of participants cheating on agreements, and the difficulty of coordinating collective action in response to changing economic conditions.[60] By setting prices for all inpatient services at each of the state’s hospitals and by penalizing hospitals whose volumes expand at the expense of rivals, Maryland’s rate-setting protects incumbent hospitals from these competitive threats. The premium rates that larger hospitals could command are permanently enshrined. And these hospitals are able to mandate charges for initiatives that they want to undertake, driving up costs for potential competitors.

Unsurprisingly, Maryland’s system has always been enthusiastically supported by the state’s hospitals. “The dirty secret,” remarked a trustee of the Maryland Hospital Association, “is that the legislation was drafted by the Maryland Hospital Association.” A Blue Cross lobbyist of the era noted: “The hospitals got together and wrote up the best legislation they could perceive—it guaranteed profit and success.”[61]

The state’s hospitals claim that rate-setting is needed to safeguard revenues for the provision of uncompensated care. In reality, it does little to shift resources from affluent communities to hospitals facing the greatest uncompensated care burden. Indeed, it does far less to shift resources than would a direct appropriation to ensure that additional revenues are employed to provide charity care.

In general, price regulation is most able to improve outcomes for consumers in markets that have substantial natural barriers to competition, a few homogenous products, few providers to be monitored, and a single measurable objective. Hospital care, however, offers a dramatically different set of circumstances.[62]

Even though HSCRC has attempted to impose rewards and penalties for compliance with quality metrics, the primary incentive to maintain quality standards will always be the value of a good reputation (associated with often hard-to-measure factors, such as attentive staff, well-maintained facilities, physician quality, cutting-edge equipment, and high standards of cleanliness) for attracting patients.[63] Fixed pricing truncates the competitive rewards for investing to create a superior product. If it leads to excess demand and shortages, fixed pricing may lead to a deterioration in quality over time as well.[64] An arrangement by which prices are deliberately fixed at different levels, at alternative facilities, for largely political reasons, is at odds with initiatives for active patient consumerism that Maryland has itself promoted.[65]

Decades of reform have seen layers of regulations piled up to deal with the unintended consequences of previous regulation—in turn, generating still additional challenges that must be addressed with still further regulation. Initially, rates were set in proportion to what were judged to be reasonable levels of average cost for treating patients with various diagnoses. But as fixed costs of hospital care are substantial, average costs can be greatly reduced by increasing output; this gave hospitals a great incentive to cover whatever costs they incur simply by inflating volumes.

Although penalties imposed on hospitals for exceeding Global Budgets reduce the incentive to inflate volumes, they also penalize hospitals that attract more patients by offering better care. If, say, one department at a hospital attracts more patients, it reduces funds available for other services, causing the hospital to choose between starving service lines in need or those that excel. Penalties also push hospitals to cherry-pick easy-to-treat patients. Even if regulators could penalize attempts by hospitals to actively appeal to low-cost patients, it would be hard to police and prevent the absence of investment in (costly) expansions of capacity or upgrades to services.

To offset the implicit penalty that Global Budgets impose on hospitals that attract more patients, HSCRC imposed an additional layer of regulations to payment calculations, “market-shift adjustment” (MSA), to shift funds from hospitals losing patients to those gaining them. Yet the MSA methodology is not transparent or well understood by market participants. It reduces hospitals’ Global Budgets if volumes decline within service lines, but only if declines are matched by volume increases at other hospitals.

Conversely, limits on permitted hospital price increases (5%, or 10% with review) may lock hospitals into difficult financial circumstances if they greatly undershoot their permitted budgets.[66] Given the enormous complexity of various overlaid and interacting payment adjustments, even sophisticated hospital systems increasingly have little idea about what their marginal revenues will be for attracting additional patients of various types.

Well-meaning incentives (e.g., to reduce readmissions) entangled incomprehensibly with these broader adjustments have little impact if their net effect is unclear. The upshot: hospitals often treat their revenues as lump-sum allocations, with adjustments to Global Budgets to be sought through special dispensation from HSCRC. As a result, the distribution of funds loses its link to patient demands and, instead, increasingly responds to the political power and preferences of hospitals.

At present, two of seven seats on HSCRC’s rate-setting commission are occupied by hospital executives. When regulators meet monthly to adjust fees, the rate-setting process is dominated by hospitals. HSCRC staff, for example, receive detailed comments from each hospital about their own revenue needs, with little countervailing input from insurers. Cost-conscious HMOs are generally absent.[67] An asymmetry of information in the rate-setting process gives hospitals an inherent advantage: they understand their cost functions and client populations better than the regulators who monitor them. Hospitals tend to argue points of equity to evade penalties related to efficiency; and, to avoid penalties related to equity, hospitals often justify their behavior on grounds of efficiency. These conditions favor incumbents and create further pressure to reduce potentially unpredictable elements of competition, making it nearly impossible for disruptive innovations (such as new institutions or methods of delivering care) to displace established institutions.[68] The net effect of greater politicization of pricing tends to be lower-quality care, delivered to fewer patients, at higher cost.

Hospitals tend to view regulated prices with a mind-set similar to that of tax professionals examining the IRS code, looking for every loophole and combination of rules that can possibly be contorted and exploited. In policing such attempts, regulators will always be “trailing the market.” The political ability to reform a fait accompli is limited, too.[69]

Fixed fees for hospital services have, as noted, led Maryland hospitals to divert care to other settings, such as outpatient surgery centers, which they own but which are exempt from HSCRC’s jurisdiction. For instance, in addition to its four hospitals, Johns Hopkins has three “surgery centers” that are not subject to price caps.[70] Likewise, Maryland’s highly regulated system of payments for hospital care sits uneasily alongside its absence of regulations for physician services. Physicians remain best paid for delivering costly procedures to patients within hospitals, even though hospitals are increasingly incentivized to keep such patients out.

To address this problem, Maryland has sought to punish hospitals for inflated TCOC. Once again, however, this imperfect solution to problems caused by regulation has created fresh problems. Hospitals find themselves penalized when patients attributed to them get sick—even though hospitals have control over only a small portion of total health-care expenditures, and physicians have more influence over patient referrals. If a hospital is thrifty with the delivery of services, it may still be penalized for inflated costs if, say, patients patronize costlier rivals, or if patients incur Medicare-covered expenditures while in Florida for the winter.

A hospital may be assigned responsibility for costs incurred by patients living many miles away—who may never even have heard of the hospital—based on the overall pattern of referrals made by physicians whom those patients have visited. In urban and suburban areas, hospital service areas are likely to overlap greatly, and the allocation of patients to hospitals is unlikely to correlate with great accuracy. Nor are hospitals able to reward patients for staying in-network or eschewing low-value utilization, as managed-care organizations do.

Penalties for high costs necessarily fall heaviest on hospitals in declining communities that are responsible for treating poorer and sicker patients. The potential penalty for hospitals associated with the TCOC is therefore capped at 1% of their revenue, with the costliest percentile of patients ignored in calculating penalties.[71] The TCOC penalty is thus mostly symbolic and will likely remain so, doing little to constrain costs beyond hospitals. Many unregulated prices and quantities remain, particularly for physician services under commercial insurance.

The principle of fee equality between payers seems to be breaking down, too. In 2017, all-payer per-capita hospital revenues increased by 3.9%, while Medicare revenues increased by only 1.9%.[72] In 2018, all-payer revenues increased by 0.35%, while Medicare revenues actually declined by 2.5%.[73] As a result, HSCRC voted to expand the permitted discount for Medicare, from 6% to 7.7%.[74]

Although the ever-shifting justifications for Maryland’s system, along with the ever-accumulating layers of regulation, may seem senseless, they can be understood as oriented toward the ultimate purpose of qualifying Maryland for its lucrative waiver reauthorization. Authorized rates are carefully calibrated by HSCRC to optimize performance on the waiver metrics agreed upon with CMS, neglecting unmeasured variables.[75] This waiver is widely understood to be the linchpin of the system. Political support for rate regulation would collapse if hospitals lost access to these additional revenues.[76] Few stakeholders or state officials have incentives to ask difficult questions or to publicize the flaws of rate regulation in a manner that might put the waiver bonus at risk.[77]

The cost-control tools of rate-setting and Global Budgets are crude substitutes for competition and managed care. The fact that hospital protectionism has led to inflated prices elsewhere in the U.S. does not mean that rate-setting is likely to reduce costs. On the contrary, rate-setting strengthens the capacity of hospitals to impede price competition.[78] Nor does rate-setting impede the ability of hospitals to consolidate with physician practices for the sake of gaining leverage over HMOs, which seek to negotiate contract terms that would enable them to restrict volumes.[79] Restrictions on managed-care plans negotiating discounts from in-network providers further impedes cost control.[80] Although all-payer rate-setting is often compared with the provider payment regulations under which Medicare Advantage (MA) plans operate, a critical difference is that MA statutory rates serve as a ceiling on prices for out-of-network emergency care.

Yet in the Maryland model, they serve as a price floor for all services.

How Do Maryland’s Health-Care Costs and Outcomes Compare with Those of Other States?.

On the core metric relevant to waiver reauthorizations—hospital costs per admission—the Maryland model has performed impressively. From 1975 to 2005, hospital costs per admission fell from 23.6% above the U.S. average to 5.1% below, the lowest rate of increase of any state.[81] Yet, from 1976 to 2011, the number of admissions (which was irrelevant to the waiver during this period) soared by 110% in Maryland, compared with a 60% rise nationwide.[82] From 1991 to 2009, hospital costs per capita and health-care spending per capita grew faster in Maryland than in neighboring states and in the U.S. as a whole.[83]

The recent experience with Global Budgets evinces a similar mix of good performance on waiver metrics and unimpressive results elsewhere. Officially, the rate of all-payer hospital revenue growth was 1.53% per capita (target: 1.55%); the cumulative five-year reduction in Medicare hospital spending was $586 million (target: $330 million); Medicare cumulative TCOC savings were $461 million (2% below target); the reduction in hospital-acquired conditions was 44% (target: 30%), and the rate of hospital readmissions was successfully reduced below the U.S. average (from 11.9% above in 2012 to 0.3% below in 2018).[84]

The most recent CMS evaluation of the Maryland model used data from 2014 to 2017 to assess the state’s hospital costs relative to a comparison group of similar out-of-state facilities, controlling for demographic and medical differences in patients.[85] CMS found that Maryland’s Medicare spending per beneficiary was down 3%, with declining inpatient volumes and a slight increase in outpatient care. For commercially insured patients, it found that the level of per-capita spending in Maryland relative to the comparison group remained the same, even though the volume of care declined (by 4% for inpatient settings and by 3% for emergency and outpatient settings).

An independent analysis comparing Maryland hospitals with a matched out-of-state control group of hospitals found no significant change in hospital utilization among the state’s Medicare patients in 2014–15, following the introduction of Global Budgets, relative to 2009–13.[86] There were no changes to levels of admissions, the number of observation stays, the level of readmissions within 30 days, the number of emergency-department visits, and levels of primary-care utilization. Only slight reductions in hospital utilization were observed, which disappeared when the difference in ex ante trends from the matched group were controlled for.

Studies of the earlier Global Budgets experiment in rural areas similarly failed to find statistically significant reductions in hospital utilization or readmissions linked to the introduction of the system.[87] Yet these studies acknowledge the difficulty of identifying an appropriate control group as a counterfactual for rural Maryland hospitals, especially when rural hospital utilization is declining nationwide.

The value of longitudinal data for analyzing Maryland’s all-payer system is therefore likely to be limited. This is particularly true for recent reforms, which have coincided with the implementation of the ACA and MACRA. Advocates of Global Budgets argue that “hospitals may need time to implement new care management programs and reconfigure capacity,” and so the benefits “might not be detectable after only one or two years.”[88] A cross-sectional analysis—which acknowledges exogenous differences between Maryland, neighboring states, and the U.S. as a whole—is therefore the best perspective from which to assess the Maryland model. Because hospital-payment regulation has been deliberately designed to evolve away from inherited market rates, it makes sense to compare the product of that process with the evolved product in the absence of regulations.

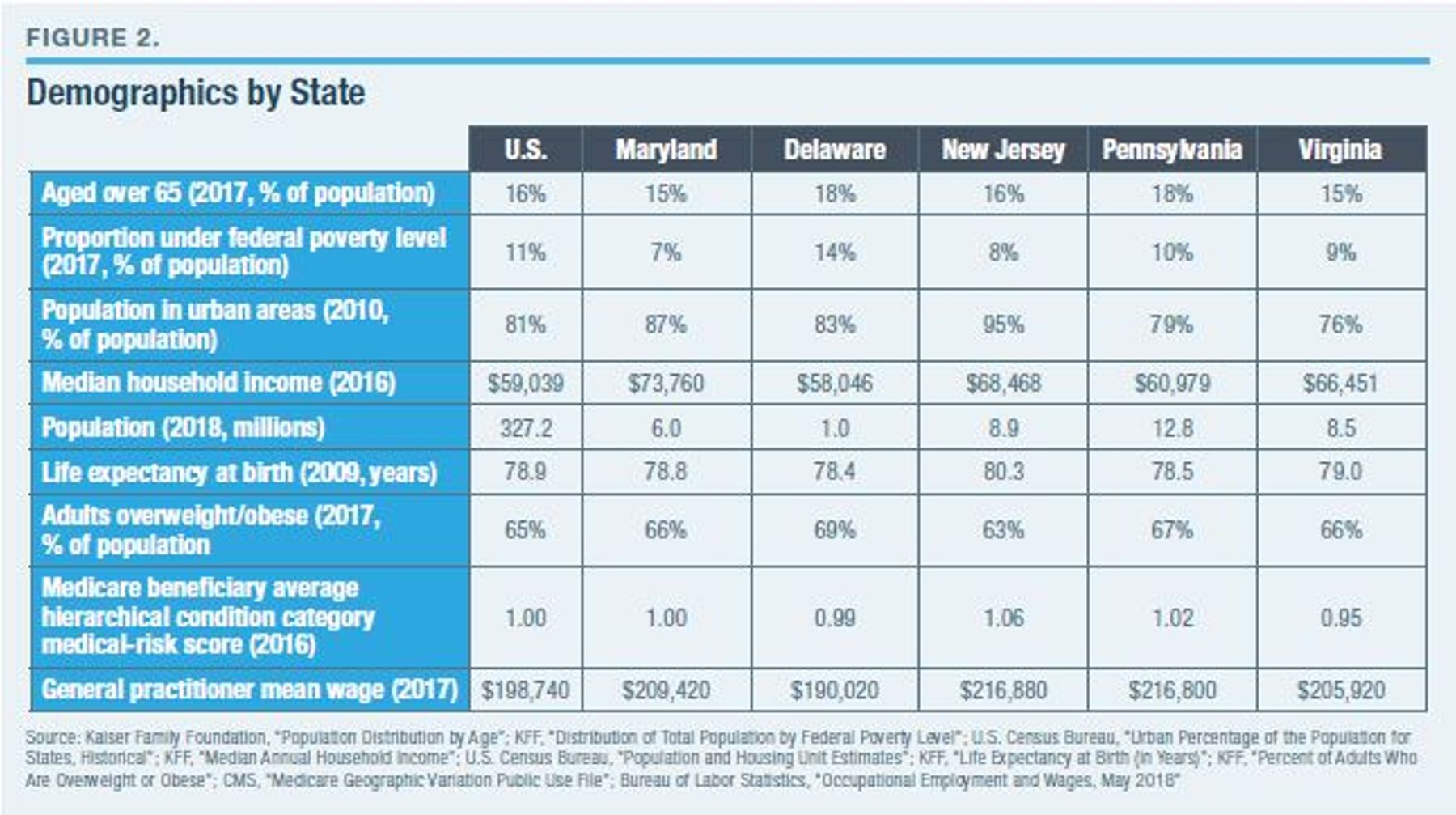

In terms of demographics and level of medical needs, Maryland is slightly more affluent and urbanized than the U.S. average (Figure 2). When Maryland is compared with other mid-Atlantic states, we see that Delaware is significantly less affluent, while Pennsylvania and Virginia are more rural. New Jersey is, in many respects, most similar to Maryland.

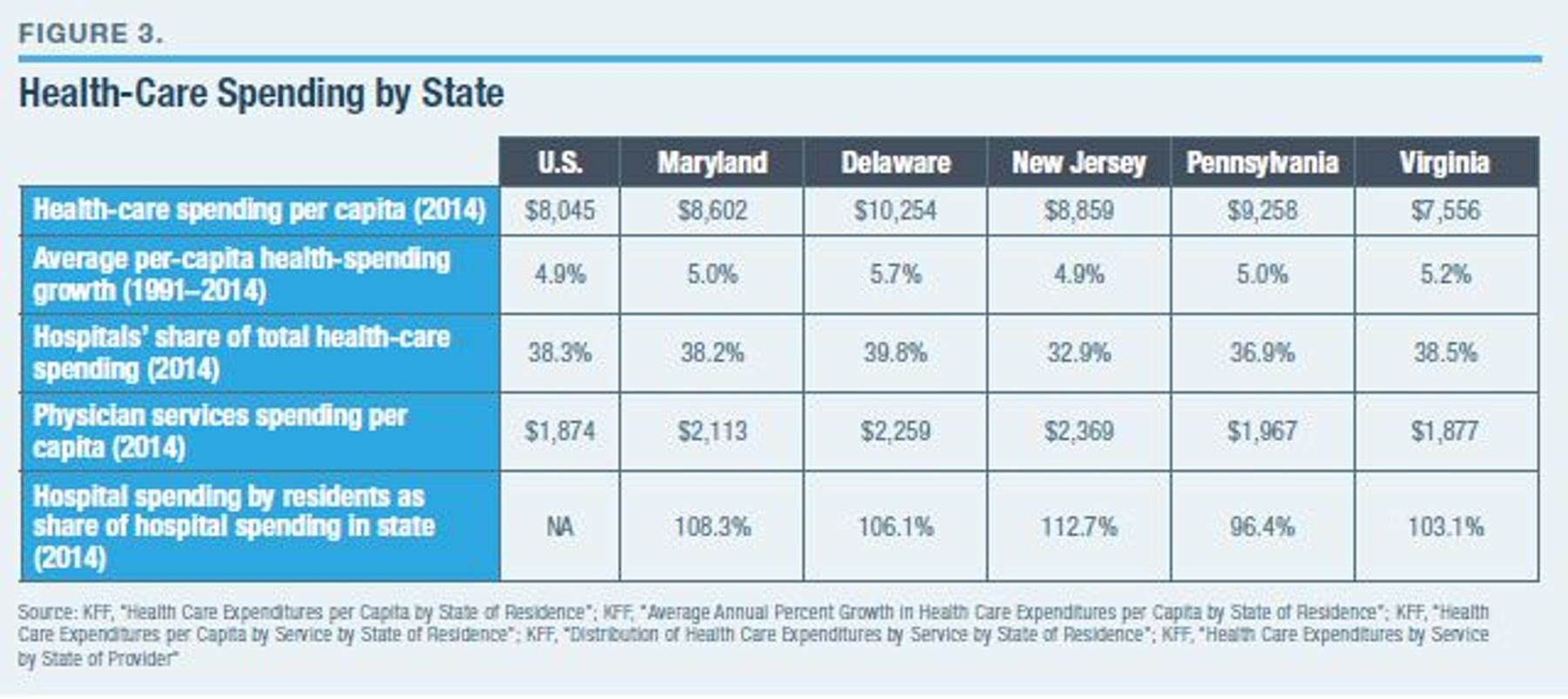

Maryland’s level of health-care spending per capita is slightly above the U.S. average, and it is similar to that of neighboring states, particularly New Jersey (Figure 3). The rate of health-care spending growth in Maryland over the past few decades is also in line with regional and national norms. Maryland’s level of spending on physician services is slightly higher than the U.S. average, but it’s not out of line with neighboring states. Evidence that Maryland rate-setting has served to divert hospital care out-of-state is inconclusive: consumption of hospital services by Maryland residents is 8.3% higher than the amount of health-care services delivered within the state. New Jersey, though, has an even greater disparity.

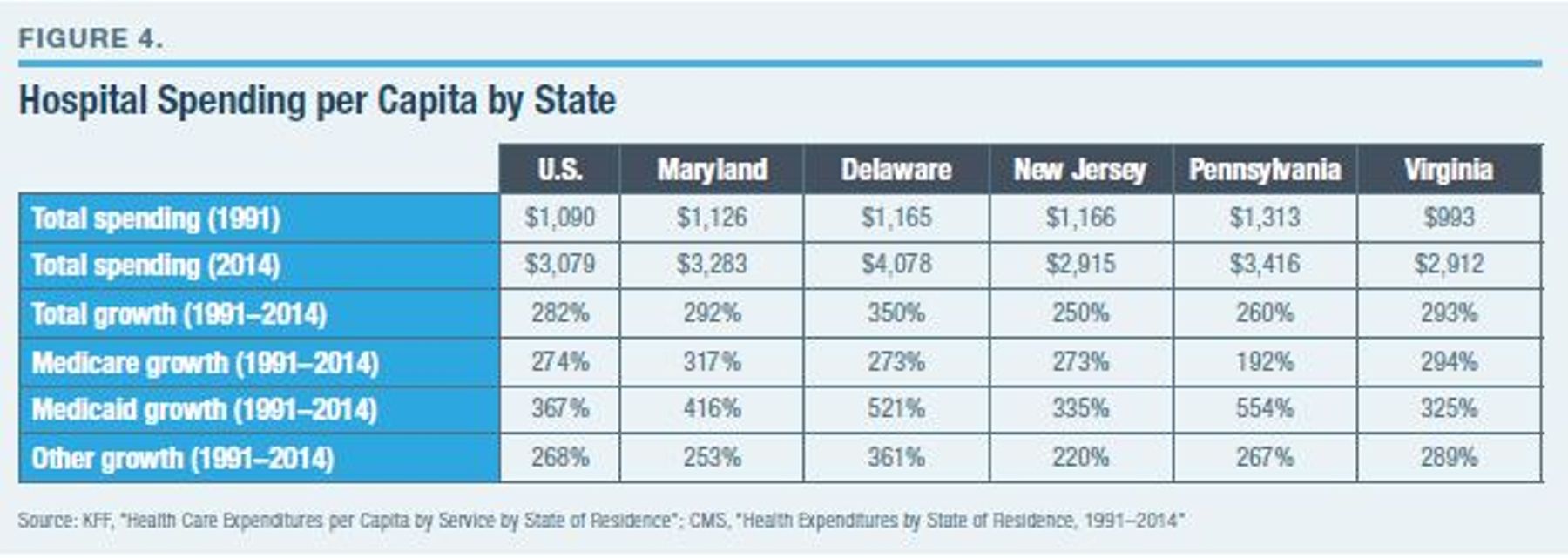

Hospital spending per capita is lower in Virginia and New Jersey; in the latter, it is particularly low as a share of total health-care spending. But levels of hospital spending in Maryland are also unexceptional, by national and regional standards. Maryland’s rate of Medicare hospital spending growth per capita has greatly exceeded that of other states. Yet its rate of total per-capita hospital spending growth has also exceeded the U.S. average in recent decades (Figure 4). While Maryland’s total hospital spending per capita slightly lagged that of New Jersey in 1991, Maryland’s total spending level surpassed New Jersey’s after the latter abandoned rate-setting.

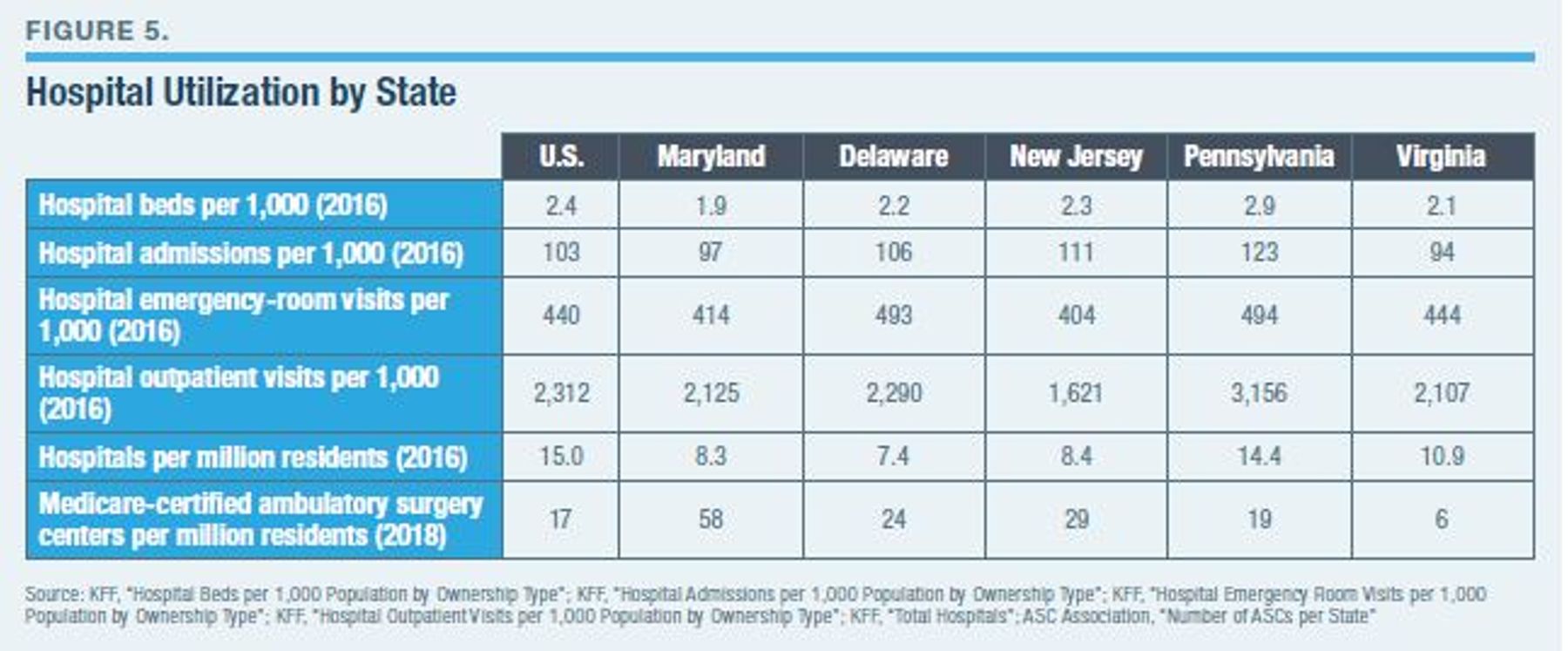

On a per-capita basis, Maryland saw slightly lower levels of hospital admissions and has fewer hospital beds than most neighboring states or the U.S. as a whole, but many more ambulatory surgery centers than any other state (Figure 5). This lends support to the notion that commercially insured patients in Maryland are diverted to a nonhospital setting in which prices are unregulated.

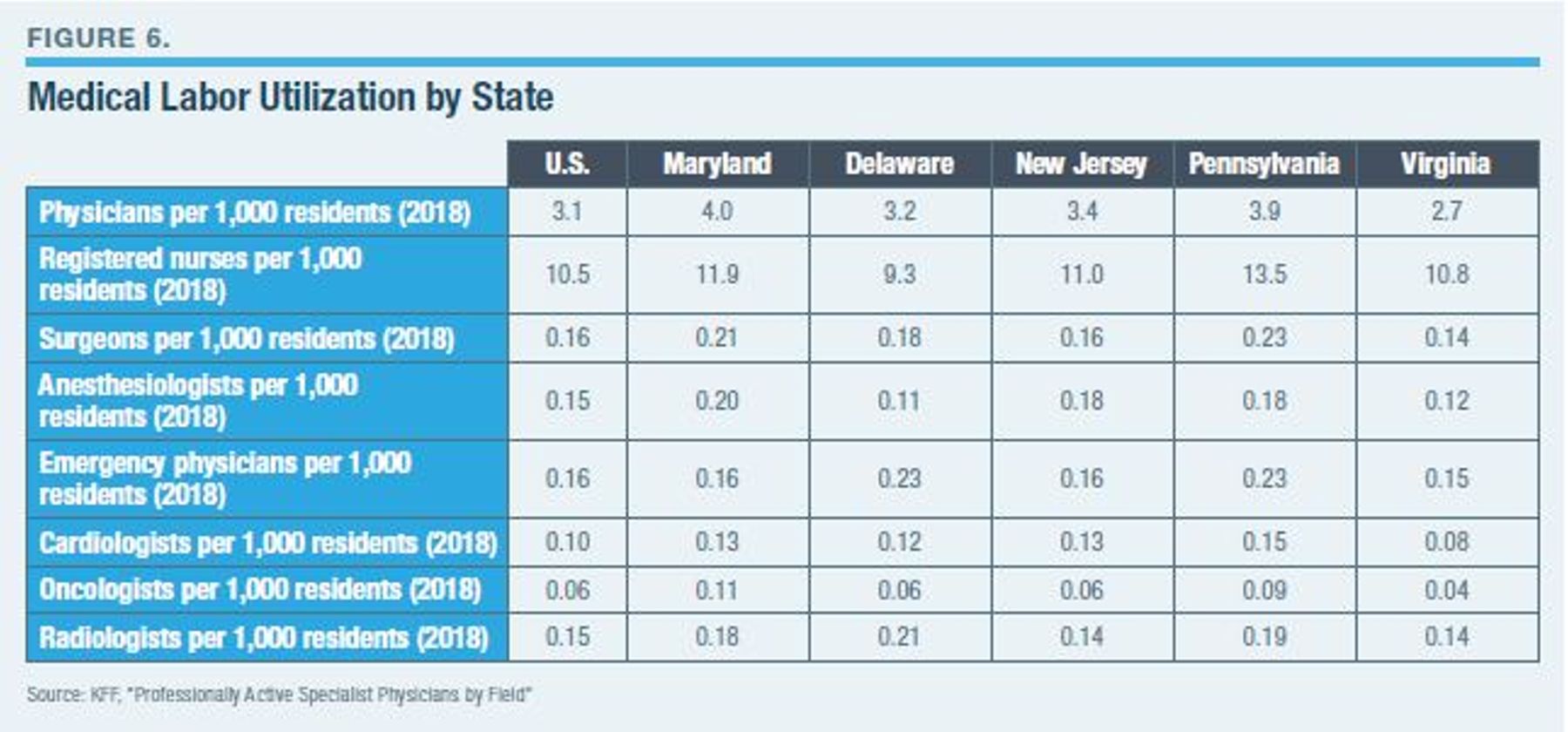

Because nonhospital medical facilities are exempt from HSCRC regulations, quantifying the utilization of ambulatory surgery centers is difficult. Examining employment of different types of labor, however, can help fill the gaps. Maryland’s relatively high number of physicians of all kinds stands in stark contrast to its relatively low hospital-service volumes. The former increased by 120% per capita from 1975 to 2013, while the U.S. average rose by only 92%. That Maryland has relatively many anesthesiologists, radiologists, and surgeons—despite having relatively low hospital utilization—reflects the unregulated nature of physician fees. This, again, suggests a significant diversion of volumes to ambulatory surgery centers. The extremely high number of oncologists (83% more than the U.S. average, per capita) may be due to a combination of Maryland’s high Medicare hospital reimbursement rates and 340B discounts for physician-administered drugs, which together make the practice of oncology particularly lucrative in Maryland (Figure 6).[89]

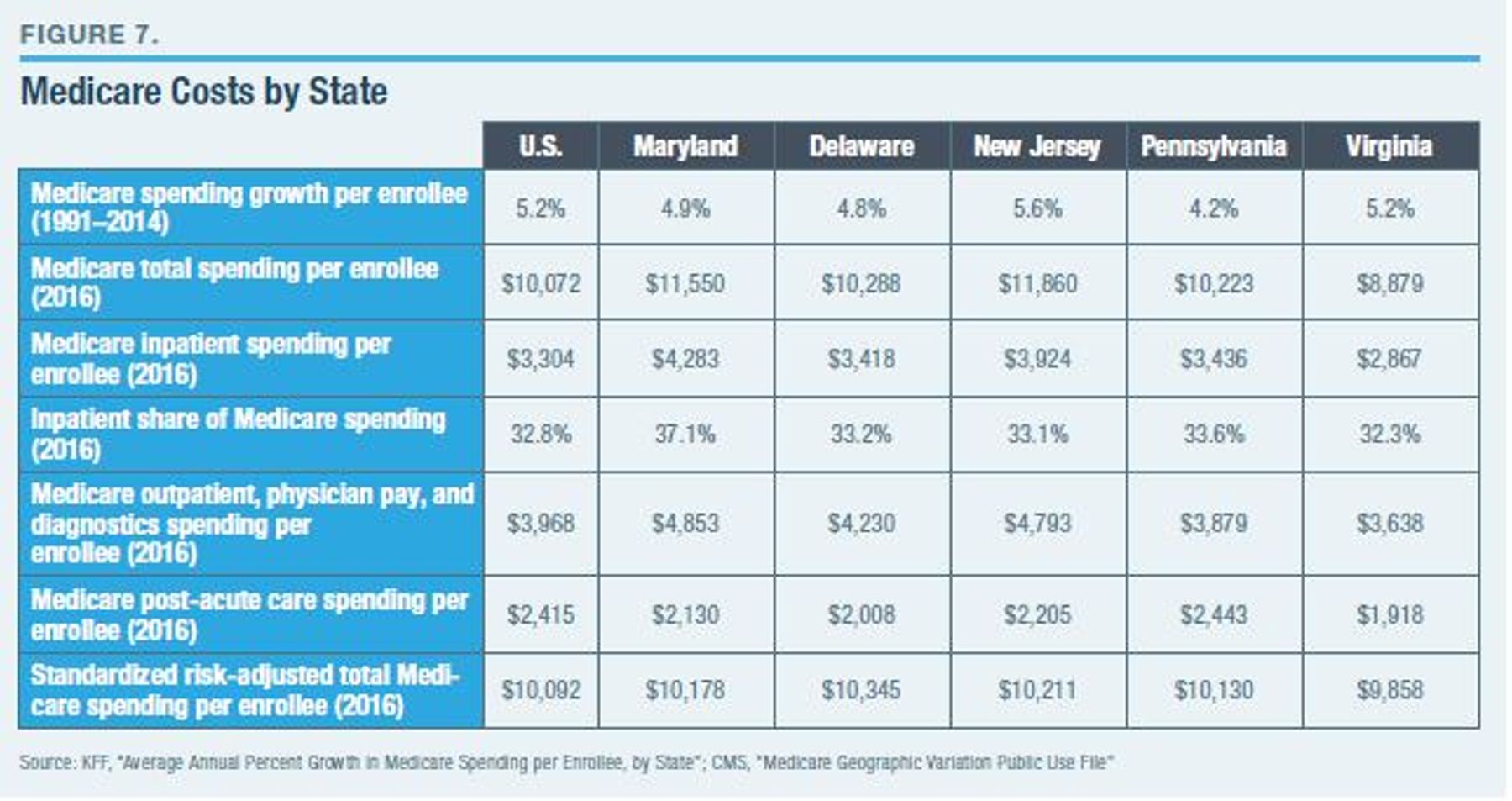

As a consequence of its waiver, Maryland’s level of inpatient hospital spending per Medicare enrollee was 30% greater in 2016 than the U.S. average and significantly above the levels in neighboring states (Figure 7). Hospital costs accounted for a much larger share of Maryland’s Medicare spending; but after accounting for differences in beneficiary health status and differences in Medicare payment levels, Maryland’s level of Medicare spending was only 0.01% greater than national levels. This suggests that Maryland’s levels of utilization for comparable Medicare patients were not exceptional.

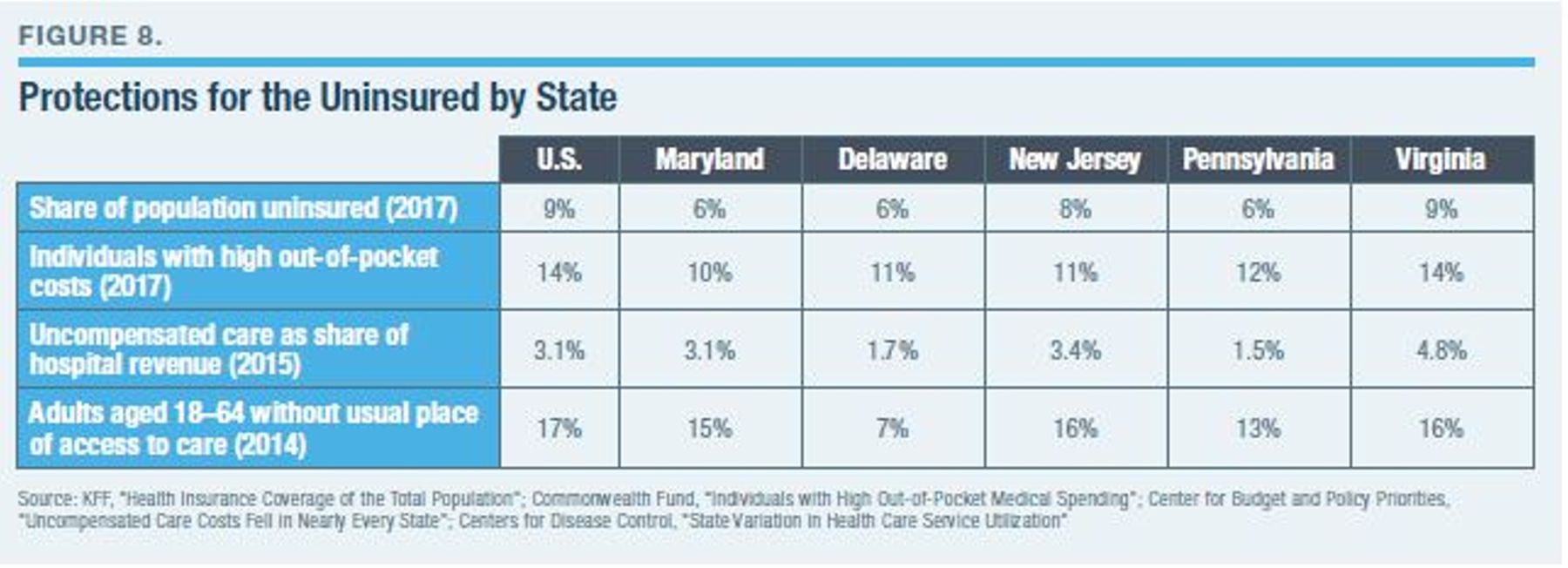

The Maryland model is, as noted, intended to help the state’s hospitals provide greater levels of uncompensated care. Yet Maryland’s level of uncompensated care as a share of hospital revenue was identical to the U.S. average in 2015 (3.1%), as well as roughly in the middle of the range of neighboring states, from 1.5% in Pennsylvania to 4.8% in Virginia (Figure 8). Maryland has a smaller share of its population reporting high out-of-pocket costs than the U.S. average. But that share is similar to the share in states with a similar percentage of the population uninsured. The share of Maryland’s population without a usual place of access to care is only slightly less than the U.S. average (15% vs. 17%) and, again, is inside the range of other states in the region.

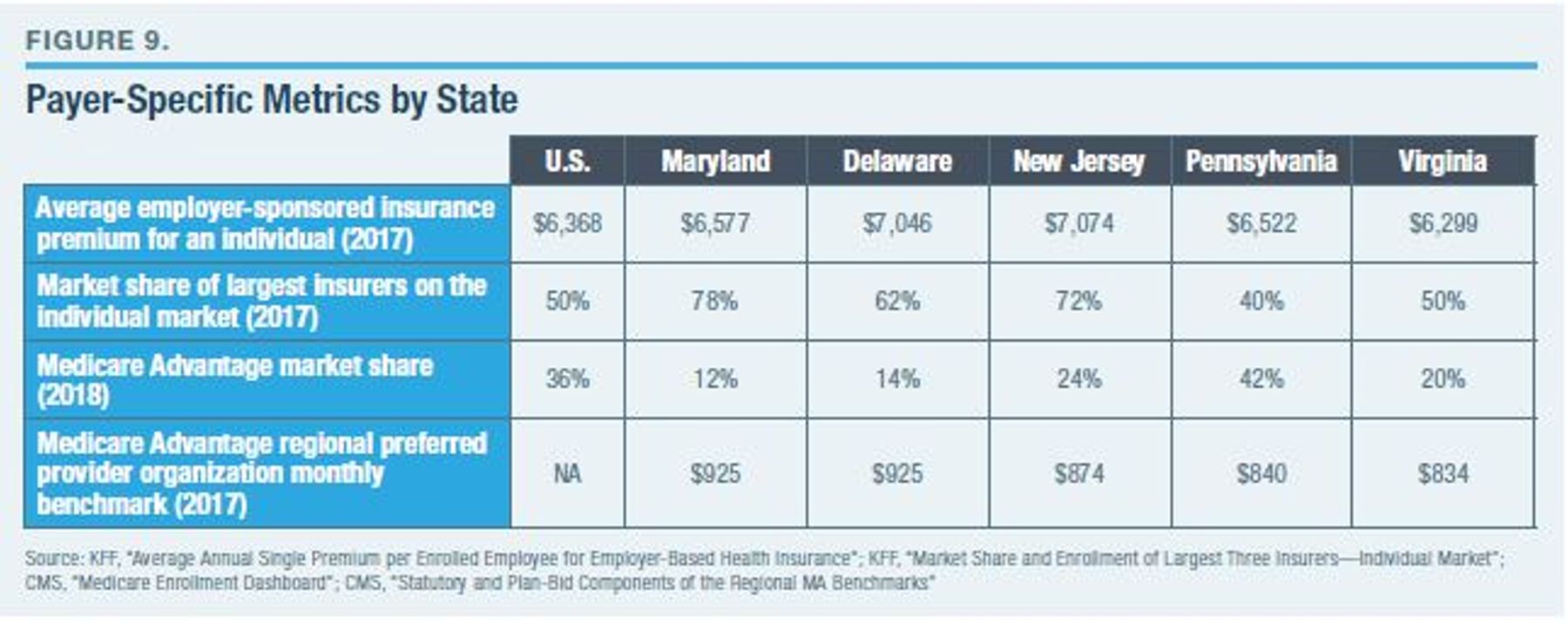

The inflated Medicare rates intended to finance uncompensated care in Maryland do not appear to have greatly reduced the cost burden borne by private insurance. Premiums for individuals on the employer-sponsored market (which are less skewed by risk segmentation than the nongroup market) are higher in Maryland than the U.S. average and are also within the range of neighboring states (Figure 9). Nor does rate-setting appear to have made Maryland’s insurance market more competitive by preventing insurers from using leverage with providers to get better prices than competitors: Maryland’s insurance market is more dominated by a single carrier (CareFirst) than are the insurance markets of neighboring states or markets across the U.S. as a whole.

The Maryland model has also failed to prevent hospital consolidation. In fact, the share of the state’s hospitals in multihospital systems has risen more (from 49% in 2003 to 66% in 2016) than the U.S. average (where it increased from 54% to 67% during the same period).[90] Restrictions on managed-care discounts appear to have hindered the growth of Medicare Advantage in Maryland: the share of Medicare beneficiaries enrolled in MA lags below levels nationwide and in neighboring states—despite relatively high benchmark payments to plans. Hospitals in Maryland may be reluctant to offer attractive terms to HMOs, which might trim their otherwise-lucrative Medicare waiver revenues.

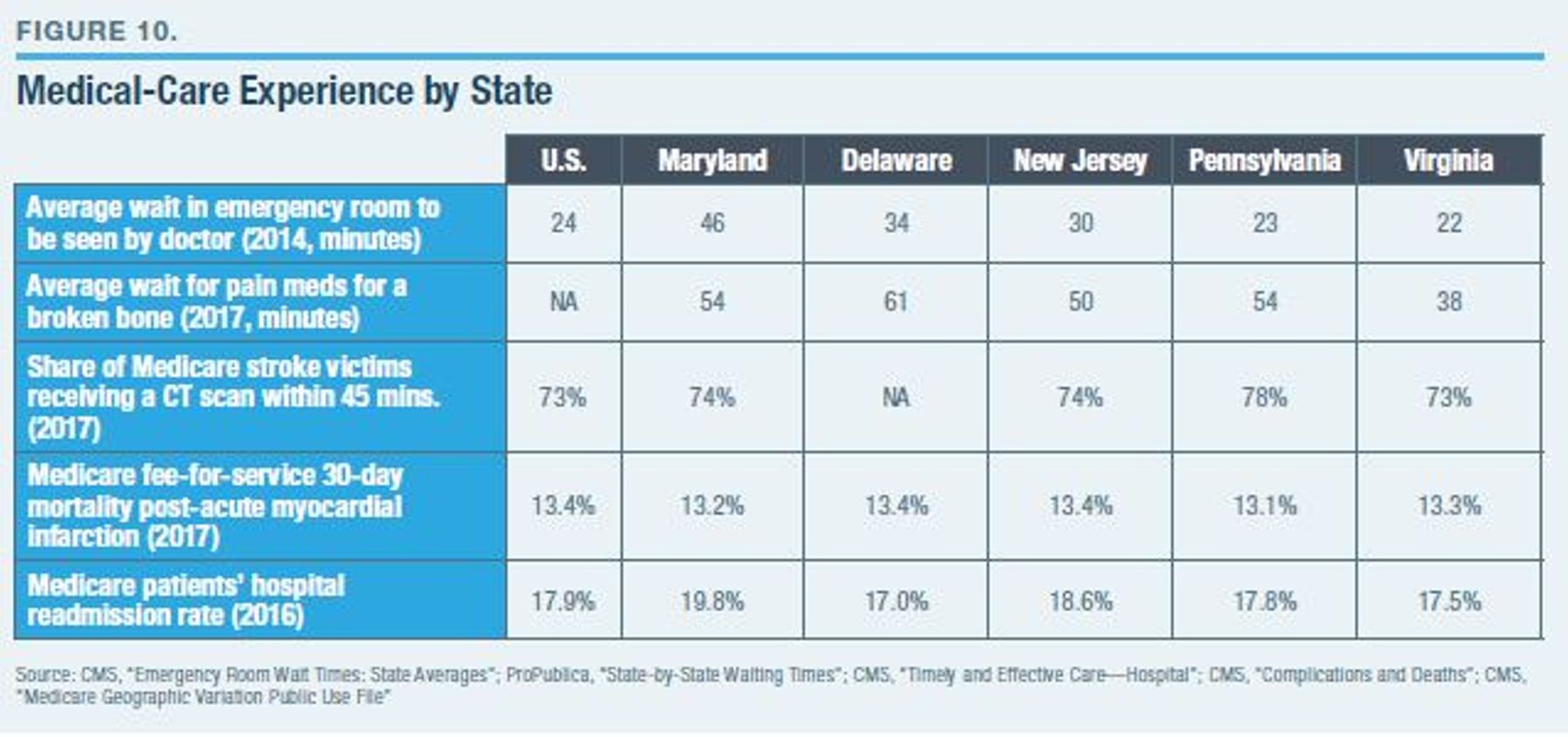

Maryland patients must wait longer, on average, to be seen after arriving in the emergency room than those in any other U.S. state, with a waiting time almost double the U.S. average. Nonetheless, the state was not an outlier on waiting times for certain metrics, such as receiving pain medications for a broken bone or the share of stroke patients receiving a CT scan within 45 minutes (Figure 10). However, anecdotal evidence suggests that Maryland hospitals have failed to adequately expand capacity for treating mental-health and substance-abuse disorders in response to the opioid crisis, which has hit the region particularly hard.[91]

Maryland hospitals do not differ greatly from those nationwide or in neighboring states on general metrics of care quality, such as mortality rates following a heart attack or adherence to standard processes of care. Rates of patient readmissions, which had been significantly higher at Maryland hospitals, have now fallen to about the U.S. average.

Conclusion

Maryland’s hospital-payment regulation would not have been enacted without the support of the state’s hospitals, has been shaped primarily by those hospitals over time, and would be repealed (as were those in other states) if it were no longer in such hospitals’ interests. The state’s hospitals are happy to jump through regulatory hoops to qualify for extra federal funds. Yet the political consensus undergirding the system would shatter if the Maryland model ever served to reduce hospitals’ overall revenues.

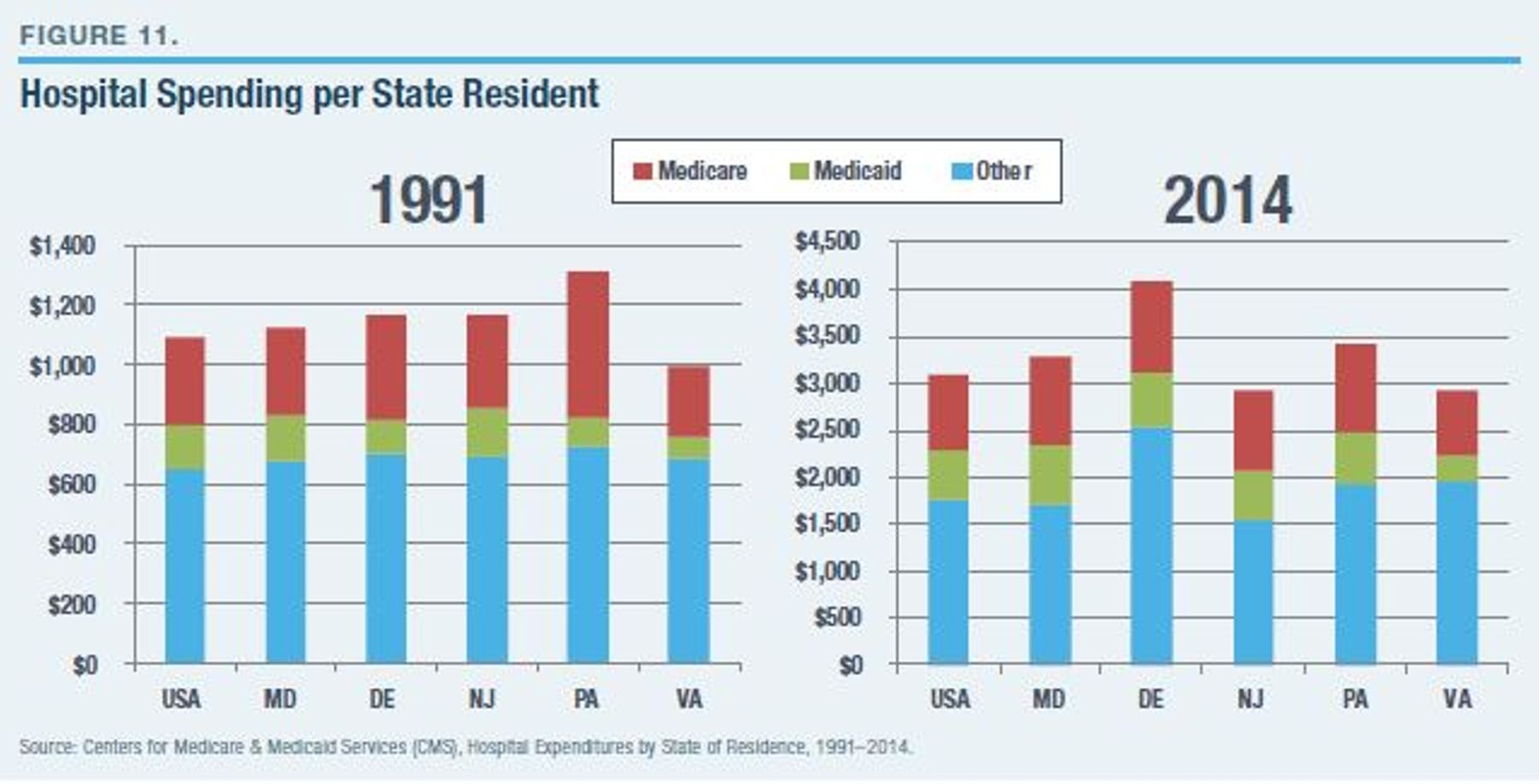

Overall hospital revenue levels in Maryland do not differ greatly from those in neighboring states, and the Maryland model retains broad loopholes so that its constraints are easy to avoid (Figure 11). The elimination of these loopholes is widely recognized to be a political nonstarter. Indeed, the political desire to protect existing capacity, which makes hospital care expensive in the other 49 states, also makes administered prices for hospital care expensive in Maryland.[92]

As a result, although hospital price regulation in Maryland has reduced spending on a few target metrics, it has not demonstrably saved money overall. At the same time, it hasn’t created any great shortages or deterioration in access to care. And there is little evidence that the Maryland model has yielded a great expansion of charity care to fill otherwise unmet needs. Overall, there seems to be little to justify the multibillion-dollar cost of inflated Medicare payments made by the federal government—other than the fear of short-term disruption that would result if it were taken away.

While price caps may make sense in the limited context of services that insurers are mandated to pay for, such as out-of-network emergency care, there is little justification for the kind of comprehensive price floor that exists in Maryland.[93] Indeed, unlike Medicare Advantage’s payment rules, the Maryland model does not empower managed-care organizations to cut costs. Nevertheless, it cripples the ability of insurers to negotiate discounts. Inflated costs are a problem in America’s hospital sector. But they result from a deficiency, not an excess, of price competition. Maryland’s price-fixing exacerbates this problem.

Endnotes

Photo: Peter Horrox / iStock / Getty Images Plus

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).