Twenty-first century technology increases efficiency in ways that people could barely imagine just a few decades ago. Twenty years ago, instant communication via social media and app-based GPS navigation did not exist, but now have become indispensable to many. Blockchain, the technology behind “cryptocurrencies” such as Bitcoin and IBM’s recent exploration into logistics and package delivery systems, has the potential to be just as beneficial to consumers.

Blockchain technology as it applies to currencies is explained in the original paper on the technology by Satoshi Nakamoto. Nakamoto, a pseudonym used by the initial innovator(s) of the blockchain technology, reports on two basic ideas of the new technology.

First, financial transactions are all peer-to-peer, which eliminates the need for banks to act as intermediaries and allows for greater levels of anonymity.

Second, the technology creates a public ledger which can be accessed by every device on the network. The ledger, or “chain,” is formed by individual “blocks” and placed in chronological order. This creates a “blockchain” that acts as a ledger for every transaction that has ever taken place using the exchange. This ledger can never change.

Consumers benefit from blockchain technology in several ways. Allowing for transactions between individuals without banks acting as middlemen creates greater freedom to spend money at a lower cost. Encryption software that functions without personally identifying information creates a pseudo-anonymity that many value. Additionally, the chronology and availability of the ledger make it possible to know at what time transactions took place and which users were involved. Because every bitcoin is stamped with a key indicating its transfer to another user, it makes the currency easier to track.

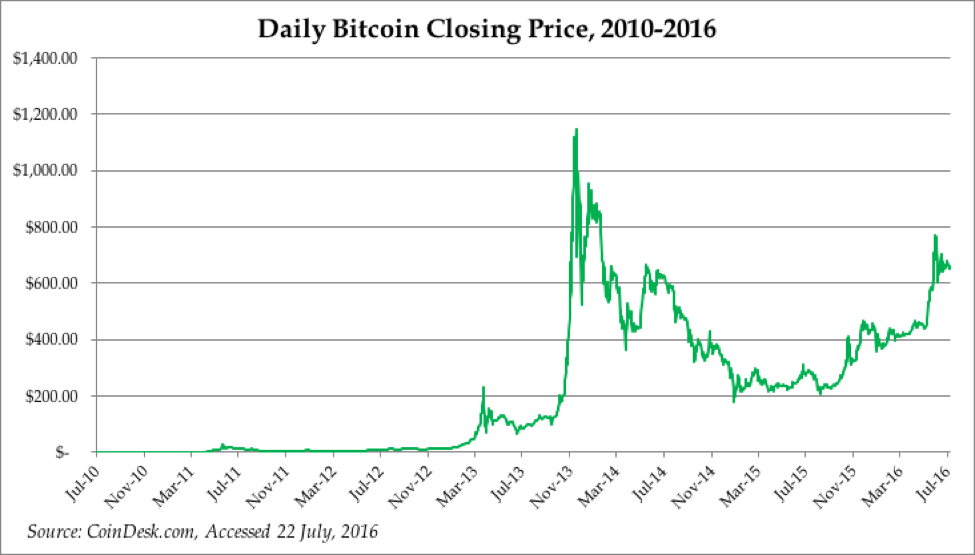

Even with these benefits, many have concerns about virtual currencies. For one, the technology is relatively new. It is not impervious to error, as evidenced by Bitcoin’s 2014 loss of $470 million in currency. A combination of technological glitches and fraud led to disappearing bitcoins that caused a 43 percent drop in Bitcoin’s stock prices from its all-time high (shown below). Prices have since risen by 17.3 percent.

Others highlight the use of virtual currencies in online criminal activity as a point of contention with the technology. Even within the last week, a district court in New York charged a Texas man with one count of securities fraud after he was found operating a Bitcoin Ponzi scheme. Based on average values of bitcoins during the scam, the court found that Trendon Shavers, the defendant, stole approximately $800,000.

A more familiar example is the arrest of Ross Ulbricht, operator of the “deep web” site Silk Road. The site was notorious for illegal drug trafficking, and many transactions between buyers and sellers were Bitcoin-based. After Ulbricht’s arrest, the FBI said it seized approximately 173, 991 bitcoins in the Silk Road case, at the time worth $33.6 million. Now this amount is worth about $114.15 million.

Bitcoin is already considered a commodity and taxed accordingly by the CFTC. Many people think that the above are reasons enough to regulate the virtual currency and its competitors. But there are some serious flaws in this argument.

First, take the problems with the technology itself. Bitcoin was the first to widely use the blockchain technology. Unfortunate as they are, technical glitches allow programmers to know what to fix and how to better develop software. This is part of what economists call “learning by doing.” As the name suggests, individuals and firms get better at developing products and using them more efficiently through trial and error. Similar to any other entrepreneurial venture, the product will either become more efficient with time as innovators seek to rectify existing problems with Bitcoin, or the technology will be replaced with another, more useful currency. The rapid decline in stock prices following Bitcoin’s 2014 technological glitch is evidence of such market responses.

Furthermore, the argument against Bitcoin’s use in illegal transactions blames the currency rather than the criminal. Drug trafficking can–and often does–happen absent the presence of Bitcoin. Cash and other hard assets such as jewelry have anonymity similar to bitcoin, yet regulators do not attribute criminal activity exclusively to these assets. But this is exactly what some, like Senator Joe Manchin (D-WV) in his 2014 letter to federal regulators, argue regarding Bitcoin. Although there is no direct individual identification associated with a public bitcoin key (identification), federal agents already have access to the public ledger and the transaction stamps just like everyone else.

Even if regulators could remove the anonymity aspect of Bitcoin, this would not be desirable, as no one wants every financial transaction they have ever made to be publically accessible. The Silk Road case shows that law enforcement can effectively stop crime through established means and seize cryptocurrencies in the aftermath. Rather than wasting the time of regulators and law enforcement, the American legal system should focus on the individuals committing crimes, not the medium of exchange.

Much to the chagrin of anti-blockchainers such as Senator Manchin, Federal Reserve Chairwoman Janet Yellen announced shortly after the senator’s letter that “the Federal Reserve simply does not have authority to supervise or regulate bitcoin in any way.” Assuming innovators in blockchain technology retain this autonomy in the coming years (although the SEC and CFTC also have some authority over aspects of blockchain currencies), we should expect companies like Bitcoin to become increasingly important to the 21st century economy.

By leaving investors and innovators free to experiment with their resources, the blockchain currency technology will either take off in a way we have yet to see or become obsolete. Individuals should be left to make their own financial decisions.

Conner Dwinell is an E21 contributor.

Interested in real economic insights? Want to stay ahead of the competition? Each weekday morning, E21 delivers a short email that includes E21 exclusive commentaries and the latest market news and updates from Washington. Sign up for the E21 Morning Ebrief.