Testimony by Oren Cass Before the Senate Committee on Energy and Natural Resources

Good morning Chairman Murkowski, Ranking Member Cantwell, and Members of the Committee. Thank you for inviting me to participate in today’s hearing.

My name is Oren Cass. I am a senior fellow at the Manhattan Institute for Policy Research where my work addresses both energy and environmental policy.[1]

My testimony today focuses on the implications of the energy price environment for federal energy policy, and my primary message to the committee is this: Congress should design energy development policy independent of prevailing market prices, for three reasons:

- First, the primary impact of policy decisions will not be felt for years or even decades;

- Second, market prices and predictions say little about what future prices will actually be; and

- Third, innovation and exploration will dramatically and unpredictably change both the scale and economics of various resource bases.

Therefore, the appropriate federal role is to establish a clear, stable framework within which the private sector can make long-term investments wherever it chooses. The same policies that make sense in a low-price environment make sense in a high-price environment.

This approach is most likely to produce the most efficient allocation of resources and maximize domestic production of energy while minimizing its cost. As the boom of the past ten years illustrates, the resulting benefits are broad: reduced energy costs for households and businesses, increased employment, reduced dependence on imports and exposure to price volatility, and increased geostrategic power for the United States at the direct expense of many of the worst actors on the global stage.

Energy Policy Time Horizons

The exploration and extraction of natural resources occurs on decades-long timelines. Out-of-sight-of-land wells were first drilled in the Gulf of Mexico in the 1940s, but it was in the 1990s that technological advancements drove production costs down by 60 percent in a single decade[2] and output first exceeded 1 million barrels per day (bbl/d).[3] Even in the current price environment, the U.S. Energy Information Administration (EIA) forecasts a 10 percent increase next year, to more than 1.8 million bbl/d.[4]

Similarly, the revolution in shale production that has upended global markets over the past eight years began with research in the 1970s and required decades of small-scale advancements.[5] As recently as 2003, the U.S. Geological Survey (USGS) downgraded its estimate of undiscovered, technically recoverable resources (UTRR) in Texas’s Eagle Ford shale formation from 270 million bbl to 33 million bbl.[6] In 2015 alone, the formation produced more than 500 million bbl.[7]

Even well-understood and easily accessible resources take years to come online. As then-Senator Obama observed in a 2008 campaign speech, “George Bush's own Energy Department has said that if we opened up new areas to drilling today, we wouldn't see a single drop of oil for seven years. Seven years. And Senator McCain knows that, which is why he admitted that his plan would only provide ‘psychological’ relief to consumers.”[8] The seven years were up last year, in the midst of an oil glut.

When energy prices are high, opponents of expanding domestic production argue the timelines are too long to justify the approach. When energy prices are low, they ask “what’s the rush?”[9] But when anticipating resources that might come online a decade or more hence, the market price today is simply not relevant.

Long-Term Price Forecasts

If policymakers had any capacity to accurately predict long-term energy price trends, they might use those forecasts to craft today’s energy policy in anticipation of future price levels. They have no such ability. Indeed, policymakers of the early 2000s had no conception that oil prices might rise more than five-fold that decade, just as policymakers of the early 2010s had no conception prices might plunge back down.

To quote a recent paper in the Journal of Economic Perspectives by Christiane Baumeister and Lutz Kilian, “oil prices keep surprising economists, policymakers, consumers and financial market participants.”[10] Even financial market futures, they find, offer no meaningful guidance.

This should not be surprising. The determinants of long-term demand include not just economic growth and thus total energy demand, but also the evolution of energy consumption technologies that might change efficiency levels or the relative attractiveness of various forms of energy. Even if one could presume some reasonable level of global economic growth and energy efficiency improvement in the coming years, what share of new cars on the road will consume gasoline at all?

Supply projections are even less reliable. The scale and location of recoverable resources changes constantly, as does the cost of lifting those resources. As recently as 2010, the EIA forecast no upward trajectory in domestic oil production for the next five years. By 2015, its estimate for the year had increased 66 percent over its 2010 forecast.[11]

The picture looking forward is no clearer. Some analysts believe the U.S. shale boom is over. My Manhattan Institute colleague, Mark Mills, believes it is only just beginning and estimates that production costs will continue to decline until on par with those of Saudi Arabia.[12] None of which even considers the possibility that other countries with shale reserves—China chief among them—might succeed in development of their own,[13] or that the next “revolution” in oil sands or oil shale could be just around the corner. Finally, geopolitical events could at any moment cause substantial shocks in both short- and longer-term supplies.

If we do not know what will happen, we must plan accordingly.

The Federal Opportunity

While domestic oil and gas production outside of federal control exploded from 2010–2013, increasing respectively by 52 percent and 29 percent, it fell during the same period on federal lands and waters, decreasing respectively by 16 and 24 percent.[14] One reason for this discrepancy is the disproportionate concentration of shale resources outside of federal control. But had those resources been under federal control and subject to the associated regulatory restrictions, permitting requirements, and political in-fighting, the development may never have happened at all. Looking beyond the shale boom and excluding North Dakota entirely, those states where the federal government controls less than 10 percent of land saw proved reserves increase 104 percent from 2008–2013, while those states where the federal government controls more than 50 percent of land saw reserves decline by 7 percent.[15]

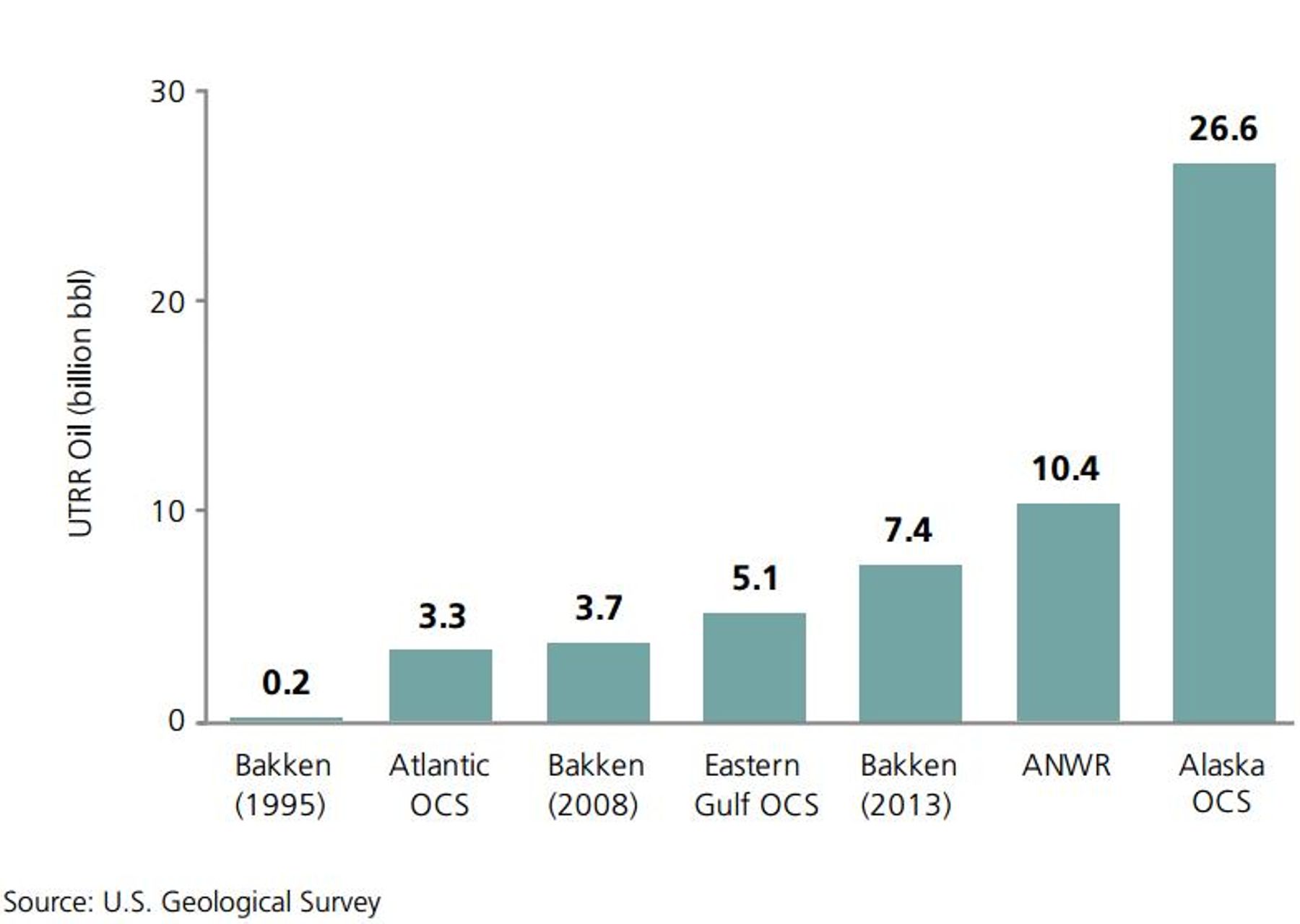

Yet, the off-limits federal resources may be far richer than those driving the shale boom. Off-limits areas of the Outer Continental Shelf (OCS) are estimated to contain more than 40 billion bbl of technically recoverable resources. The Arctic National Wildlife Refuge (ANWR) contains another 10 billion. By contrast, the entire Bakken Formation in North Dakota is estimated to contain less than 10 billion bbl and that estimate was less than 1 billion bbl until the formation was well into development (see figure).[16]

Further exploration could reveal some of these federal resources to be smaller in scale than the preliminary estimates indicate, however the more common experience has been for exploration and development to beget ever-larger discoveries over time. For instance, from 1996–2011, the U.S. government’s resource estimate for off-limits areas of the OCS changed little. But the Gulf of Mexico, under active development, saw its estimate increase five-fold—from a less-than-5 percent chance of finding 10 billion bbl to a best guess of nearly 50 billion bbl.[17]

Access to well-understood federal areas in the OCS and ANWR, as well as an opportunity to explore and invest in other onshore areas, has the potential for similar upside.

Stable, Pro-Production Policy

With no credible forecast of how energy markets will evolve, but with the opportunity for enormous production under its feet, the best course for the nation is to let markets work. Private industry is best positioned and incentivized to put its own capital behind its own judgments about what investments at what scale make sense where. It will place bets efficiently as long as it can trust the regulatory environment in which it must act. Government must make clear that it is “open for business,” supportive of efforts to expand production, and committed to not whiplashing policy back and forth in response to changing market conditions.

The objective should not be simply to open as much land as quickly as possible. Industry lacks capacity to invest everywhere at once and government lacks capacity to provide the requisite oversight. Rather, reforms should focus on the establishment of a clear and legally-binding (i.e., legislated) roadmap for the opening of new on- and offshore areas over the coming five- and ten-year periods, including ANWR and off-limits OCS areas. USGS should regularly update inventories of federal lands and waters and EIA should forecast development timelines and peak output levels that can form a baseline against which to measure achieved production increases. States should be granted permitting authority over lands within their borders and clear procedures and timelines should be established for permitting processes that remain at the federal level.

In addition, downstream timelines must be shortened. Not only does it take years or decades for new resources to come online, but it can take just as long to construct the infrastructure needed to transport and use the resulting fuel. Pipelines and export terminals for both oil and natural gas should be deemed in the national interest and subject to a straightforward approval process with a clear timeline. Energy products should be placed on the same legal footing as other commodities for export. And environmental laws should be amended to eliminate the heightened “new source” burdens that new and expanded power plants, refineries, and manufacturing facilities face as compared to existing ones.

- - -

If the question is what resources will America and the world need ten, twenty, or thirty years from now, the answer is that no one knows. But if the question is what course to pursue, we do know: innovation and exploration have always benefited the nation and in hindsight we are always glad they occurred. The moment when new supply seems least critical is no less a moment when future investment should be invited.

The energy revolution unleashed by new oil and gas production on private lands has brought enormous benefits to the America’s economy, its geopolitical power, and its household budgets. This nation has the resources under federal lands and waters to repeat that experience. But the necessary long-term planning and investment will only occur if the federal government replicates the stable and supportive framework that private industry has encountered on private and state-controlled land.

Thank you again for the opportunity to appear before the Committee. I hope my testimony will be helpful to you as you consider appropriate federal energy policy in the context of fluctuating energy prices.

[1] For additional detail and analysis on many of the points contained in this testimony, see Oren Cass, “Step on the Gas: How to Extend America’s Energy Advantage,” Manhattan Institute for Policy Research, July 2015, https://www.manhattan-institute.org/pdf/ib_35.pdf.

[2] “The Offshore Petroleum Industry in the Gulf of Mexico: A Continuum of Activities,” Bureau of Ocean Energy Management, 2008, https://www.boem.gov/Offshore-Petroleum-Industry-Organizational-Scheme/.

[3] “Federal Offshore—Gulf of Mexico Field Production of Crude Oil,” EIA, https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=pet&s=mcrfp3fm2&f=a (accessed April 15, 2016).

[4] Matt Egan, “U.S. Gulf of Mexico Pumping Oil Like Never Before,” CNN Money, March 11, 2016, https://money.cnn.com/2016/03/11/investing/gulf-of-mexico-record-oil-production/.

[5] Loren King et al, “Lessons from the Shale Revolution,” Breakthrough Institute, April 2015, https://thebreakthrough.org/images/pdfs/Lessons_from_the_Shale_Revolution.pdf.

[6] S. M. Condon and T. S. Dyman, “2003 Geologic Assessment of Undiscovered Conventional Oil and Gas Resources in the Upper Cretaceous Navarro and Taylor Groups, Western Gulf Province, Texas,” USGS, 2006, https://pubs.usgs.gov/dds/dds-069/dds-069-h/REPORTS/69_H_CH_2.pdf.

[7] “Drilling Productivity Report,” EIA, https://www.eia.gov/petroleum/drilling (accessed April 15, 2016).

[8] Remarks by Senator Barack Obama (Lansing, MI), August 4, 2008, https://www.nytimes.com/2008/08/04/us/politics/04text-obama.html.

[9] See, e.g., Carol Browner and Michael Conathan, “What the BP Oil Disaster Tells Us About Arctic Drilling: Keep Out!,” Newsweek, April 20, 2015, https://www.newsweek.com/what-bp-oil-disaster-tells-us-about-arctic-drilling-keep-out-323475 (“But for the American people who, after all, own any oil that might be locked beneath the Arctic seabed, there’s no rush. Domestic oil and gas production is already at record levels, and according to even oil and gas industry projections, continued technological innovation means that economic growth no longer requires an equivalent growth in fossil fuel consumption.”).

[10] Christiane Baumeister and Lutz Kilian, “Forty Years of Oil Price Fluctuations: Why the Price of Oil May Still Surprise Us,” Journal of Economic Perspectives, Winter 2016, https://www-personal.umich.edu/~lkilian/bk8_110215r1.pdf; see also Brad Plumer, “Why Crude Oil Prices Keep Taking Us By Surprise,” Vox, April 14, 2016, https://www.vox.com/2016/4/13/11401564/crude-oil-prices-predictions.

[11] “Annual Energy Outlook 2010,” EIA, April 2010, https://www.eia.gov/forecasts/archive/aeo10/pdf/0383(2010).pdf (table A11); “Annual Energy Outlook 2015,” EIA, April 2015, https://www.eia.gov/forecasts/aeo/tables_ref.cfm (table A11).

[12] Mark P. Mills, “Shale 2.0: Technology and the Coming Big-Data Revolution in America’s Shale Fields,” Manhattan Institute for Policy Research, May 2015, https://www.manhattan-institute.org/pdf/eper_16.pdf.

[13] “Argentina and China Lead Shale Development Outside North America In First-Half 2015,” EIA, June 26, 2015, https://www.eia.gov/todayinenergy/detail.cfm?id=21832.

[14] “Sales of Fossil Fuels Produced from Federal and Indian Lands, FY 2003 through FY 2013,” EIA, June 19, 2014, https://www.eia.gov/analysis/requests/federallands ( table 1.g).

[15] Ross W. Gorte et al., “Federal Land Ownership: Overview and Data,” CRS, February 8, 2012, https://fas.org/sgp/crs/misc/R42346.pdf (table 1, federal ownership of state land); “Crude Oil Proved Reserves, Reserves Changes, and Production,” EIA, December 4, 2014, https://www.eia.gov/dnav/pet/pet_crd_pres_a_epc0_r01_mmbbl_a.htm (reserves growth by state).

[16] Supra note 1 (figure 7).

[17] “Assessment of Undiscovered Technically Recoverable Oil and Gas Resources of the Nation’s Outer Continental Shelf, 2011,” Bureau of Ocean Energy Management (BOEM), November 2011, https://www.boem.gov/uploadedfiles/2011_ national_assessment_factsheet.pdf.

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).