Targeted Unemployment Insurance: How Tax Rebate Loans Can Better Protect the Unemployed

Photo: designer491/iStock

Introduction

The purpose of unemployment insurance (UI) is to protect workers from temporary income shocks due to the loss of employment. Yet most UI spending goes to affluent households that already have substantial assets to draw on, while the low-income workers most exposed to unemployment risks are often ineligible for assistance.

How can this be the case? The neediest Americans lack access to substantial unemployment benefits due to the paucity of their prior UI payroll tax contributions. If assistance levels are instead tied to prior Old-Age, Survivors, and Disability Insurance (OASDI) payroll tax contributions, with repayment structured as an income-contingent loan, benefits can be provided at a higher level to more low-income households without deterring employment or otherwise encouraging inappropriate claims. Such an arrangement could also reduce needless public subsidies for wealthier households that have the capacity to privately insure and protect themselves against income fluctuations.

As this brief will argue, the federal government should allow unemployed workers to claim weekly benefits worth 50% of their average weekly income for the two previous tax years, up to $500, for up to six months. In effect, this approach would temporarily rebate workers’ Social Security payroll taxes from those two prior years. Households claiming such benefits shall subsequently be subject to an additional 2% income tax, until whatever assistance they have received has been paid back. The current UI program, with its 6% federal payroll tax on the first $7,000 of income, should be repealed.

Why Unemployment Insurance?

A reduction in earnings (typically due to the loss of employment) is the most common reason that previously nonpoor families fall below the poverty line in the United States.[1]

In April 2023, 3.4% of Americans were unemployed and looking for work.[2] The median duration of unemployment was 8.4 weeks, and the mean was 20.9 weeks; 21% of the unemployed had been out of work for more than six months.[3] U.S. workers born between 1957 and 1964 suffered an average 3.1 spells of unemployment during their prime employment years (between the ages of 25 and 54).[4]

After workers lose their jobs, bills keep coming—rent or mortgage payments, utilities, food, medical expenses, taxes, car loans, unexpected repairs or legal expenses. These bills cannot be avoided in the short run; yet in 2022, only 37% of households had saved at least a month of income to cover emergencies.[5] As a result, fluctuations in household wages and consumption levels are highly correlated.[6]

Workers are often laid off through no fault of their own, as their employer’s business strategy changes or demand for its products declines. Equivalent jobs are often available, but these may be harder to find if the reduction in demand stretches across an industry, a region, or the economy as a whole—as is typically the case in recessions. These are natural hazards (which workers cannot control), against which they often like to protect themselves by purchasing insurance.

But insurers cannot sell policies against the risk of employment loss as efficiently as they can sell life insurance against the loss of earnings due to death. This is due to the much greater prevalence of moral hazard (the ability of policyholders to trigger payouts as a result of their own choices).[7] Whereas life insurers can easily reserve payouts for victims of accidental death, policyholders could claim unemployment insurance payouts by voluntarily reducing their levels of work, by taking longer to find new employment, or by falsely claiming that they are not working. As a result, unemployment insurance must pay for substantial unemployment that results from the existence of insurance coverage, as well as costs resulting from the preexisting risk of unemployment. This typically makes private unemployment insurance unappealingly expensive.

Public subsidies can allow UI arrangements to operate indefinitely, regardless of the net insurance value for policyholders. Yet, even though publicly funded unemployment benefits can tolerate greater losses to moral hazard than voluntary commercial insurance, any public spending program must also limit this at some point, and all systems of unemployment benefits have extensive rules designed to mitigate the moral hazard to which they are exposed.

The ineligibility of workers who voluntarily quit their jobs, along with the prospect of higher payroll tax rates for employers who fired workers at a higher rate, means that the magnitude of unemployment benefits does not tend to increase unemployment rates in the short run. But the provision of larger benefit levels tends to deter changes in skills, location, and behavior needed to return to productive work over time. Hence, larger benefits tend to influence the duration of unemployment.[8]

Beyond its efficacy as a method of targeting aid to those who are suddenly without income through no fault of their own, UI programs have also been justified as a method of smoothing household consumption, of tempering macroeconomic fluctuations in aggregate demand, and of allowing those out of work to seek the best job matches.[9] Indeed, if unemployment benefits loosen liquidity constraints in a way that allows job-seekers to be reemployed in more productive and better-paying jobs, some increase in the duration of unemployment may improve overall economic welfare.[10]

How It Works: Unemployment Insurance in the United States

The unemployment insurance (UI) system in the U.S. imposes a payroll tax on workers to fund monthly payments to qualified nonworkers. Established by the Social Security Act of 1935, it now covers 90% of the civilian labor force—excluding only the self-employed, workers on small farms, and household employees with earnings below qualifying thresholds.[11]

Federal law imposes a 6% payroll tax on employers for the first $7,000 of each employee’s annual earnings, the vast majority of which (5.4% of the 6%) states can claim by establishing their own UI systems conforming to broad federal rules. Since most workers earn far more than $7,000, the federal unemployment tax effectively imposes a $420 per-worker fee, whose real value has been declining with inflation since it was last adjusted in 1983.[12]

In 2022, the taxable wage base for state unemployment taxes extended beyond the federal minimum in 46 states (with a median base of $14,000, and up to $62,500 in Washington State).[13] The standard state unemployment tax rate was 5.4% in 21 states, but this automatically increases when states’ reserve of revenues to finance benefit claims is low.[14] States may adjust tax rates for particular employers, according to the relative proportion of their workers who have previously filed benefit claims. The share of wage income subject to state UI taxes averaged 0.43% nationwide (ranging from 0.12% in Florida to 1.33% in Alaska).[15]

To minimize moral hazard, states typically make workers ineligible for benefits if they quit employment voluntarily, were fired for misconduct, fail to comply with formal work search requirements, or refuse suitable employment without good cause. All states limit the duration of UI benefit claims (typically to 26 weeks, but with limits ranging from 16 weeks in Arkansas to 30 weeks in Massachusetts).[16] States also generally limit eligibility for UI in relation to the amount of earnings over the previous year subject to payroll taxes.[17] As a result, workers are rarely entitled to substantial benefits if they are self-employed, work on commission, or work part-time.

States also attempt to mitigate disincentives to work by setting UI benefit levels in rough proportion (often 50%) to weekly wages from a prior period of earnings (typically the previous year), up to the cap on the earnings base for the payroll tax. As a result, workers who previously had higher incomes tend to subsequently receive higher benefits. The magnitude of benefits tends to reflect that of unemployment tax revenues. Weekly payments in 2022 ranged from $10 to $284 in Louisiana, and from $55 to $1,461 in Massachusetts. By contrast, benefits were provided much more evenly in Arizona (which uses a more uniform formula tying benefits to prior wages), where the range was only $200–$240.[18]

Workers may claim partial unemployment benefits if their earnings fall below weekly benefit amounts, with weekly UI payments reduced dollar for dollar with earnings.[19] In the fourth quarter of 2022, UI benefits nationwide averaged $416 per week (ranging from $223 in Mississippi to $646 in Washington State), with beneficiaries claiming payments for 14 weeks—an average of $5,560 each.[20] UI benefits are themselves subject to federal income taxes but exempt from payroll taxes.

Individuals are more likely to be unwillingly unemployed during recessions, and their subsequent wage loss following reemployment is greater.[21] Under permanent law, states must provide an additional 13 weeks of extended benefits during times of high unemployment, with a 50% federal subsidy—and may provide up to an additional 20 weeks under these terms. In practice, Congress has routinely enacted ad hoc Emergency Unemployment Compensation (EUC) legislation (1958, 1961, 1971, 1974, 1982, 1991, 2002, 2008, and 2020) providing 100% federal funding for uniform federal benefits extending beyond normal UI time limits.

The Covid-19 pandemic caused an unprecedented surge in unemployment compensation. In February 2020, 1.9 million Americans claimed standard unemployment benefits, which surged to 20.9 million in May 2020, before gradually falling to 1.3 million by May 2022.[22] Eligibility and emergency pandemic unemployment benefits were further expanded under the CARES Act. Spending on unemployment benefits surged from $27 billion in 2019 to $472 billion in 2020, before falling back to $48 billion in 2022.[23]

Assessing American Unemployment Benefits

How UI Benefits Compare Across the Developed World

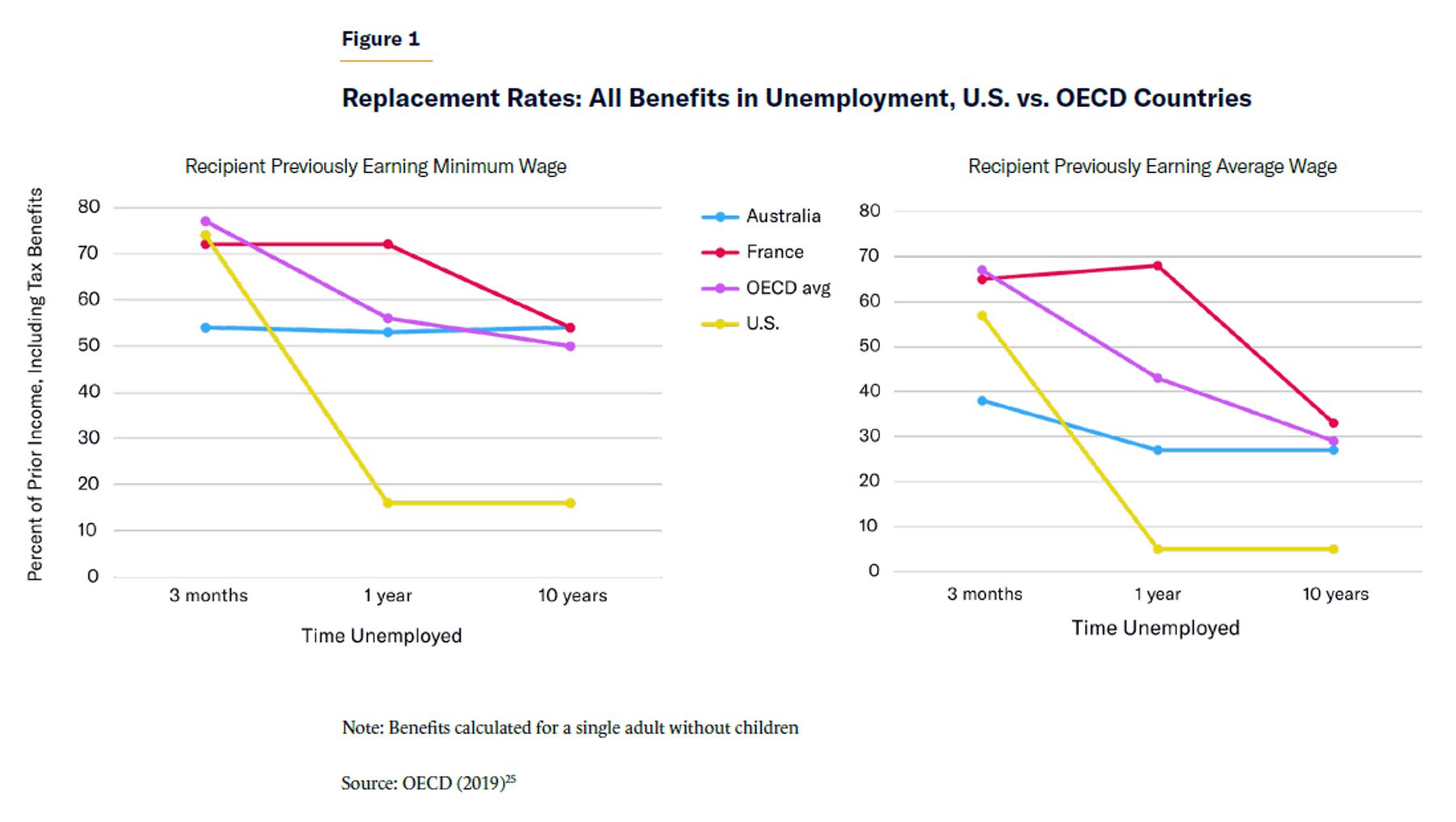

The American UI system is already better targeted than similar unemployment benefit programs in many other countries. Unemployment benefits in the U.S. offset much of the overall short-term decline in consumption resulting from adverse shocks to employment.[24] At the same time, because the cash benefits provided reduce rapidly over time in the U.S., they do less to increase the duration of unemployment than unemployment benefits in other developed countries (Figure 1).

This allows U.S. unemployment benefits to be more responsive to business-cycle downturns, such as the 2010 recession. From 2005 to 2010 to 2015, U.S. expenditures on unemployment compensation bounced from 0.3% up to 1.1% and down again to 0.2% of GDP, respectively, as the nation passed through recession. Expenditures on unemployment compensation were far less responsive at 0.7%, 0.9%, and 0.7% of GDP, respectively, across the OECD.[26]

Since the 1970s, as the generosity and duration of unemployment benefits have grown, unemployment in Europe has become persistently higher and longer-lasting than in the United States.[27] In the first quarter of 2023, 3.5% of the labor force were unemployed in the U.S., compared with 6.0% in the European Union.[28] Whereas the proportion of unemployed people who were out of work for more than 12 months in the U.S. was 23%, it was 39% in the E.U.[29]

How UI Benefits Compare Across States and Households

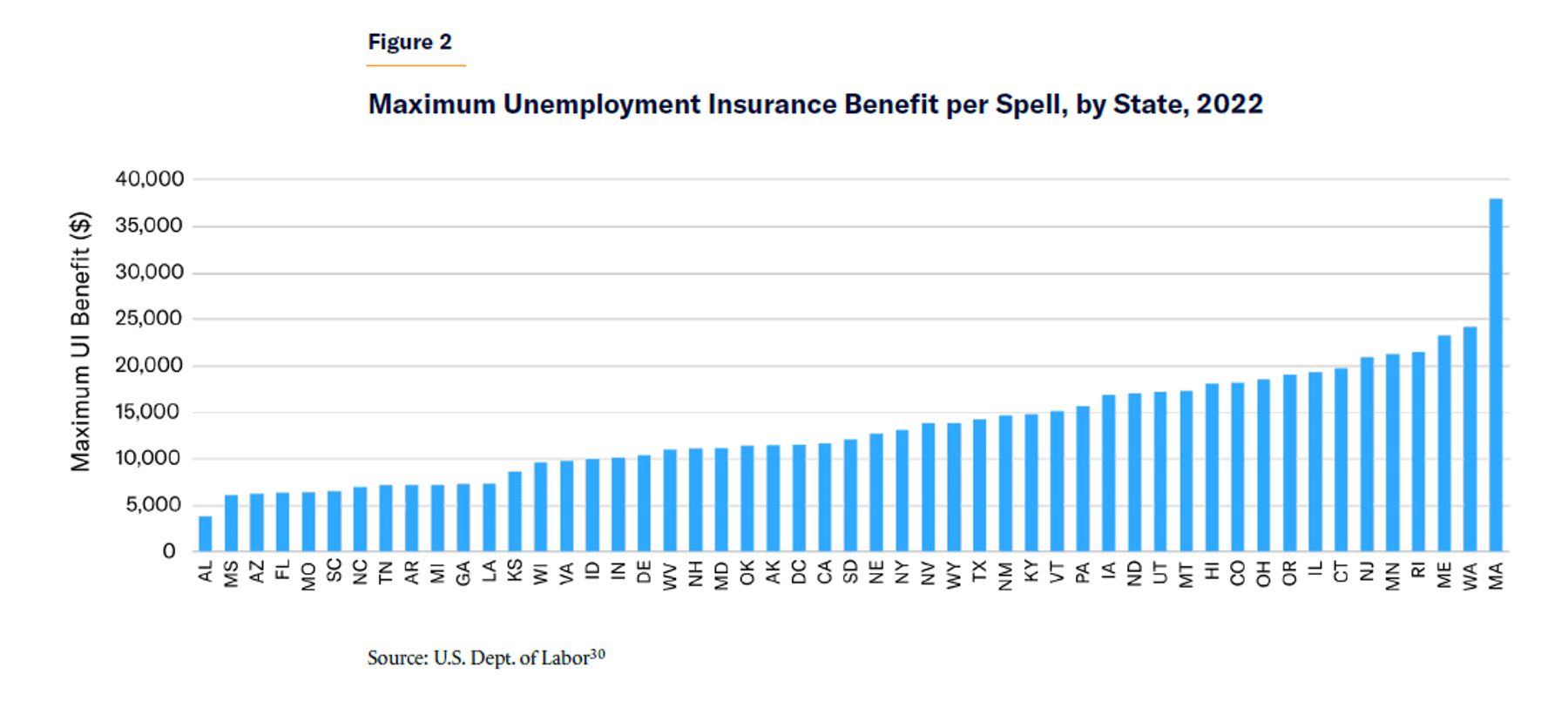

Although overall unemployment benefits in the U.S. may seem well-focused relative to other nations, there is great variation across the country (Figure 2). Due to the interaction of benefit caps and time limits, the maximum UI benefit that could be claimed for a spell of unemployment in 2022 ranged from $3,850 in Alabama (for those who previously earned more than $16,500) to $37,986 in Massachusetts (for those who previously earned more than $70,345). In some states, benefits are clearly inadequate to prevent households from falling into poverty; in others, they provide large payments to households with the capacity to save and borrow.

Rates of eligibility and take-up of benefits range widely: in the fourth quarter of 2022, the proportion of unemployed residents entitled to UI benefits ranged from 59% in New Jersey to 7% in Alabama. Across the country, only 25% of those unemployed and seeking work received UI benefits.[31]

Low-income Americans have higher rates of unemployment than the general U.S. population. But the linkage of benefit levels to prior earnings and the larger maximum benefits provided in wealthier states mean that low-income UI beneficiaries tend to receive lower payments than more affluent Americans. This disparity is exacerbated by the much greater likelihood that poorer workers will be entirely ineligible for benefits.

UI excludes many workers with irregular employment (such as the self-employed, farmers, or gig workers), who most need protection from income shocks. Low-wage workers claim UI benefits less often and have their claims challenged more frequently.[32] In 2019, less than 5% of UI expenditure went to families with incomes below the poverty level, while 64% went to those with income above the median (Table 1).

Table 1

Distribution of Unemployment and Unemployment Compensation, 2019

| Family Income | Below Federal Poverty Level | Below 2x Federal Poverty Level | Above Median (>$56,491) | Above 2x Median (>$112,982) |

|---|---|---|---|---|

| Share of total population | 12.3% | 29.4% | 50.0% | 23.4% |

| Share of those unemployed | 20.3% | 41.0% | 39.4% | 17.4% |

| Share of UI claimants | 6.3% | 22.3% | 59.7% | 26.6% |

| Share of UI spending | 4.6% | 20.8% | 63.5% | 31.5% |

| Average benefit per UI claimant | $3,915 | $5,023 | $5,716 | $6,355 |

| Average benefit per unemployed | $392 | $881 | $2,858 | $3,177 |

UI often provides little or no assistance to those who need it most. It is only for individuals in the lowest quintile of liquidity that increases in UI benefits lead to significantly higher subsequent earnings through improved job search.[34] As Duke University economist Gregor Jarosch noted, it is the “slippery bottom rungs” of the job ladder, before individuals have been able to build savings or collateral, where “unemployment spells beget unemployment spells.”[35]

Low-income households rarely accumulate enough precautionary savings to make up for income declines.[36] Nor do they possess the collateral needed to secure access to commercial loans on terms that make them useful as an economic safety net.[37] Consumption expenditures are much more responsive to changes in income for low-education or low-wealth groups.[38]

By contrast, affluent households are generally able to protect themselves from income shocks. U.S. households with workers in the labor force had a median net worth of $117,700 in 2020; 24% had a net worth over $500,000, while 31% owned less than $25,000.[39] The liquid assets accumulated by the median college graduate are sufficient to cover 124% of the income loss from unemployment, while liquid assets held by the median high school dropout cover only 5%.[40] The provision of UI benefits reduces households’ holdings of financial assets, crowding out half of private savings for the typical unemployment spell.[41]

Even if they lack liquid financial assets, wealthier households possess a capacity to borrow to make up for fluctuations in income, which poorer households lack.[42] A 2020 study of mass layoffs found workers losing their job to have access to unused revolving credit allowing them to replace an average of 44% of their prior income—a greater proportion of full-year earnings than UI typically replaces.[43] Workers with credit scores in the two top quintiles in practice borrowed to make up for 12% of their lost earnings.[44] Furthermore, working households with few liquid assets that suffer income shocks are more likely to refinance mortgages, and they convert 60% of funds removed into consumption.[45]

Because UI tax levels are not exactly proportional to the benefits that workers claim, the system often acts as a subsidy for firms to temporarily fire employees in line with fluctuations in demand, leaving workers with merely seasonal employment.[46] Indeed, most workers laid off are subsequently rehired by the same employer—particularly in business-cycle downturns.[47] To the extent that UI taxes on businesses are “experience rated” (i.e. adjusted to reflect the magnitude of UI claims made by past employees), UI taxes will tend to concentrate the burden of paying for benefits on businesses in declining industries.

Loans Target Assistance Better than Insurance

Americans need to pay their bills and have some amount of cash on hand, especially when they face unexpected hardships like unemployment. The primary objective of UI is to solve a liquidity problem faced by households that are normally not poor and are capable of supporting themselves.

More than two centuries ago, political reformer Jeremy Bentham suggested: “The best mode of relieving temporary indigence, on the part of the self-maintaining poor, is—not by donations, but by loans. Loans preserve unimpaired the spirit of frugality and industry; donations impair it, by leading them to transfer their dependence from their own exertions to those of others.” He went on to argue: “By loans made at a reduced rate,” it might be possible to “afford an immense mass of substantial and unexceptionable relief, without injury either to their own purse, or to the morals of those whose momentary feelings they relieve.”[48]

Financing assistance for the unemployed through loans limits the leakage of aid to those who could work, without depleting scarce fiscal capacity. Unlike experience rating of insurance, which imposes premiums in rough proportion to broad categories of past claims, formal loan arrangements distribute responsibility for payment in exact proportion to liabilities which are subsequently incurred. This makes loans better suited to smoothing consumption for younger households that have not yet accumulated substantial assets, and whose greatest ability to pay lies more in the future.[49] The more individual financial responsibility for funds is preserved over the long term, the more freedom, flexibility, and responsiveness can also be afforded in the distribution of assistance in the short run.

Households’ exposure to unemployment varies greatly by industry, individual business, family circumstance, worker age, and skills, while their ability to privately insure against declines in income depends on their personal savings, assets, credit rating, and ability to draw on private and informal aid resources. As a result, households’ need for public subsidies depends on highly heterogenous considerations, best known to themselves and poorly identified by the political process.

Structuring aid as subsidized loans achieves the best alignment of assistance with temporary need because the obligation to repay ensures that only those who need the help will opt to incur the responsibility. This targets assistance at those in need more accurately than merely distributing handouts according to membership in broad categories, which statutes must use to designate the “needy.”

Most higher-income households have the capacity to absorb income shocks privately (by saving, borrowing, or restructuring consumption) far more cost-effectively than through public unemployment insurance programs. That is fortunate because proportionately large shocks to the incomes of affluent households would be much costlier to insure with public funds. Yet, as has already been noted, most low-income households (often those early in their careers) have not yet accumulated substantial savings or the collateral needed to access affordable private loans to absorb temporary income shocks.

In 2019, while the median income of American households headed by adults younger than 35 was only slightly higher than the median income for those over the age of 75 ($48,600 vs. $43,100), their median net worth was much lower ($14,000 vs. $254,800).[50] As Social Security currently redistributes enormously from early in workers’ careers to late in life, younger workers are left much more exposed to income fluctuations.

Several economists, including Nobel Prize winner Joseph Stiglitz, have suggested that workers’ future Social Security benefits could be seen as a form of collateral, from which households should be allowed to borrow to smooth short-term income shocks earlier in life. Given that UI benefits are typically capped at less than six months, allowing households to borrow just 1% of their future Social Security benefits would leave them with more income than they are currently able to access from UI, without adding to long-term government expenditures. In fact, since the median spell of unemployment lasts for only eight weeks, this would cover multiple such spells.[51]

But government loans often come with high default risks, crowd out more appropriately priced sources of credit, and commit policymakers to huge implicit interest-rate subsidies that wealthy households might be most able to take advantage of.[52] Liabilities associated with public credit programs are typically off-budget and often “used to shelter programs that otherwise could not compete successfully for scarce resources,” as political scientist Dennis Ippolito stated.[53] As the cost of loan subsidies is diffused and largely hidden, the distributive effect may be hard to control.

Furthermore, elected officials are often tempted to defer, forgive, or gradually expand exemptions from repayment of public loans (by income threshold, for special crises such as a pandemic, to compensate service in the military or other favored activities, and so on). A system of large public loans to the unemployed would therefore be unlikely to receive substantial repayment if it relies on diminishment of far-in-the-future Social Security benefits, given the time horizon involved.

These risks may be mitigated by requiring gradual repayment through a tax on income that begins immediately upon resuming work, prior to the claiming of Social Security benefits. Such a tax would also replenish the capacity of households to borrow funds to protect themselves from subsequent income shocks. Indeed, the government’s income tax powers may enable it a capacity to profitably collect repayment for loans that private lenders lack.[54]

Policy Recommendation: Focused and Responsive Benefits

Unemployment insurance should be reestablished as a fully national program, entitling workers who have been fired without cause to a replenishable 26 weeks of benefits, while they remain out of work. Eligibility should be expanded to part-time, self-employed, or gig workers who are actively seeking employment. Weekly benefit payments would be set at 50% of the worker’s average weekly declared income for the previous two completed tax years, up to a maximum of $500 per individual, and would remain subject to income taxation.[55] Unreimbursed benefits should be capped at $18,000 per tax household. Fully federal EUC payments should still be provided in recessions, under existing eligibility conditions, to those who have been out of work for more than 26 weeks within a year.

The federal unemployment tax should be repealed. Instead, the worker’s household shall subsequently pay an additional income tax of 2% without deductions, until the value of benefits received (including interest at the federal funds rate) has been paid off.[56] If benefits received by workers have not been paid off when they claim Social Security Old-Age, Survivors, and Disability Insurance, their primary insurance amount for OASDI (the retirement benefit a person would receive at the normal retirement age) should be reduced proportionately, repaying the loan.

To the extent that workers have not used up all 26 weeks of UI, or in proportion to the amount they have paid off, they would be allowed to draw additional UI payments.

Justification: Ex Ante vs. Ex Post Financing

The proposed reform would internalize the cost and benefits of the UI program to households, making liquidity more readily available to those who need it, without unduly deterring work or rewarding inappropriate unemployment claims.

The value of the maximum weekly benefit to which workers would be entitled (50% of the two previous years’ average weekly income for up to 26 weeks, as stated earlier) comes to 12.5% of their total declared income over those two years, up to a cap of $500 per week. Since workers are subject to a 12.4% OASDI payroll tax over at least those two years, benefit payments can effectively be viewed as a temporary rebate of past tax payments.[57]

Shifting the calculation of benefits from UI to OASDI payroll tax payments, while also requiring subsequent repayment, would allow eligibility for UI to be expanded to workers with irregular employment situations (such as those with multiple jobs, gig workers, or the self-employed), who are currently most exposed to the risk of unemployment. By switching from ex ante to ex post financing of benefits, the reform would increase access to assistance for households early in their careers and shift the burden of payment to stages in life when their incomes are higher.

The susceptibility of benefits to progressive income taxes would generate an implicit penalty for claiming benefits in relatively high-income years.[58] This would nudge households to reserve claims for relatively low-income years during their careers, when assistance is most needed and other options are more limited. It would also deter high-income households from claiming the benefit purely to receive an implicit interest-rate subsidy.

Since this policy encourages those who can privately insure against income shocks to do so, it concentrates implicit interest-rate subsidies on lower-income households. This increases access to assistance for those who have not yet accumulated substantial private assets, while increasing the incentive for relatively affluent households to save. It would also permit the elimination of UI taxes, which deter employers from hiring workers at high risk of unemployment.

Repayment terms would not be onerous: with an additional 2% income tax without deductions, it would take just 3.9 years for a household with the median income to fully pay off the $5,500 average current UI claim (with real interest rates at 0% and assuming no dynamic effects).[59] If none of the loan had been repaid through the income tax, the worker’s retirement age to qualify for OASI benefits would be delayed by just three to four months to pay for the average UI claim under this proposal.[60] The $18,000 maximum amount would be paid off in 8.4 years through additional income taxation by the median married-couple household.[61] In the most extreme possible scenario, where both workers make maximum UI claims before both are unable to work because of disability at the full retirement age the following year, monthly OASDI benefit payments would be reduced by 5.4%.[62]

Benefits to Federalizing Unemployment Assistance

Federalizing unemployment benefits would simplify the program, improve its administration, and avert the need for complex structures of financial assistance to states.[63] It would also raise the assistance available to households in states that currently have meager UI benefits and would allow benefits to better support job search across state lines. Since benefit levels would not exceed 50% of individual workers’ average prior wages, there is no need for state involvement to adjust benefit levels for regional wage disparities.

Federalizing benefits would also facilitate coordination of the program with any temporary federal EUC enacted in recessions.[64] The revised UI system would reduce the moral hazard associated with the EUC program, by effectively establishing a 26-week waiting period for benefits, for which beneficiaries would gain temporary assistance but ultimately be financially responsible.

The Merits of Income-Contingent Loans

In an era when the economic risks to which households are exposed are increasingly diverse, social insurance programs operating under broad bureaucratic rules are less likely to help smooth consumption over an individual’s life cycle.[65] By contrast, individual control over resources becomes more valuable, and so income-contingent loans to individuals can do more to improve social welfare.[66]

Unfortunately, previous proposals to allow the unemployed to borrow funds from their future Social Security benefits have failed to incorporate appropriate safeguards against the temptation for politicians to forgive or bail out loans. Without such safeguards, those proposals would likely turn into poorly targeted entitlement expansions.[67]

Subsidized loans should not replace all social welfare benefits, but they are better suited to provide protection from temporary income shocks, which involve high moral hazard and limited downside liability, and where the capacity of households to self-insure is hard to identify. Subsidized loans would be a bad way to finance benefits for the elderly or permanently disabled, for instance, but may be preferable as a method of financing unemployment benefits, short-term sickness benefits, or paid family leave.[68] For early-in-life job search and child-rearing expenditures, public assistance programs that provide liquidity would benefit from an ex post repayment structure—as is already the case with income-contingent aspects of loans to students in higher education.[69]

About the Author

Chris Pope is a senior fellow at the Manhattan Institute. Previously, he was director of policy research at West Health, a nonprofit medical research organization; health-policy fellow at the U.S. House Committee on Energy and Commerce; and research manager at the American Enterprise Institute. Pope’s research focuses on health-care payment policy, and he has recently published reports on hospital-market regulation, entitlement design, and insurance-market reform. His work has appeared in, among others, the Wall Street Journal, Health Affairs, U.S. News & World Report, and Politico.

Pope holds a BSc in government and economics from the London School of Economics and an MA and a PhD in political science from Washington University in St. Louis.

Endnotes

Photo: designer491/iStock

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).