Rethinking Retirement A Four-Pillar Framework for Security and Sustainability

Photo: Xavier Lorenzo / Moment via Getty Images

Introduction

America’s retirement system needs an overhaul. Many retirees face inadequate income and persistent uncertainty. On the bright side, however, most Americans do have more money than ever before to finance their retirement. Thus, reforming our retirement system will not require significant government resources. But it will require a fundamentally new approach that considers all potential sources of retirement income.

One key feature of our retirement system, the 401(k), was designed to generate wealth that supplements income from Social Security and defined-benefit plans. Contrary to many media stories,[1] these retirement accounts have not been a failure: they have boosted savings for an increasingly large share of Americans. Still, they need reform. In their current form, 401(k)s are not well suited to provide income after workers stop working. That must change, beginning with better ways to convert retirement savings into predictable income.

Since the 1990s, our retirement system has been based on three pillars: government benefits, pensions from employers, and additional private saving. This report redefines each pillar for the modern labor force and financial markets—and it proposes adding a fourth.

The first pillar consists of Social Security and other government benefits. To continue paying full benefits, Social Security needs to be reformed in the next 10 years. This can be done by increasing the early and normal retirement age and increasing taxes on higher earners. For many, that would mean a reduction in benefits, but any loss of income can be offset by other tweaks to our retirement account system.

Most often, 401(k)s function to supplement Social Security with private savings—the third pillar of our retirement system. In this role, they are treated as wealth: retirees either draw down their balances using crude spending rules or simply hold the assets. But 401(k)s should also contribute to the second pillar—employer-sponsored pensions—if converted into low-risk, predictable income through instruments such as annuities or laddered bond portfolios. The key difference between these two uses for 401(k)s is that the former involves more risk exposure than the latter.

As part of the second pillar, 401(k)s could provide retirees with stable income. Yet this option remains rare because of regulatory hurdles. Expanding it will require regulatory reform and a broader shift in how we view retirement accounts and investment during the saving years. The central policy goal of the second pillar should be to ensure that retirees have meaningful ways to transform accumulated wealth into secure income.

The extent to which individuals should use their retirement account as a part of pillar two or pillar three will vary, depending on their needs and preferences. Policymakers can support better choices by expanding access to quality, affordable investment advice; and by allowing retirement accounts to be aggregated on a single platform so that savers can weigh their options and make informed decisions.

Reimagining the retirement system requires adding a fourth pillar: working into retirement. Work need not be full-time—retirees should be able to enter and exit the labor force flexibly throughout their golden years. But right now, obstacles—on both the supply and demand side—prevent many older Americans from working at all, even if they would like to do so.

On the demand side, many older Americans would like to work longer but face discrimination in the labor market that keeps them from doing so. On the supply side, we could relax several regulations to make gig and contract work easier, creating more flexible work options that would better suit older Americans. In addition, revisiting the 1980 law that requires employers to provide health insurance even to workers who qualify for Medicare would make it significantly cheaper to hire older workers.

Getting More from America’s Retirement System

Most Americas are concerned that they do not have enough money to retire and will never have enough.[2] In some ways, this is surprising. While everyone could benefit from more savings, the boomer generation is entering retirement with more wealth than its predecessors—and the outlook is even better for the next generations. Defined-benefit pensions, which are mostly a thing of the past in the private sector, are often romanticized, but many proved unreliable; some plans faced financial difficulty and could not pay benefits, and only about 38% of workers had access to them—mostly the higher earners.[3] Retirees today typically have more assets and higher incomes than previous generations.[4]

But the current system has its shortfalls, fueling widespread anxiety about retirement, and these failures should be addressed. Many Americans are unsure as to how to finance retirement or even assess their own financial situation. Misleading or inaccurate information, combined with a lack of tools to make the most of retirement assets, leaves them feeling insecure and prone to poor spending and investment choices—which leads people to become more reliant on Social Security and makes necessary reform even more difficult.

The good news is that retirement in America is not as bleak as many believe. With relatively modest, low-cost policy interventions, we can improve retirement security for millions without adding strain to federal and state budgets.

A New Vision of Retirement: Revisiting the Three-Pillar Retirement Model

Our current retirement system lacks clear goals and objectives, partly because of how it evolved. It began with military pensions during the Civil War, which gave rise to workplace pensions in the early 20th century, especially for unionized workers. As people lived longer and the country became wealthier, the U.S.—like other developed nations—created a state-run pension (Social Security) during the Great Depression. Social Security serves multiple functions: it is a mandatory savings scheme, a form of insurance, and a redistributive mechanism that offers a higher replacement rate of working income to lower earners.

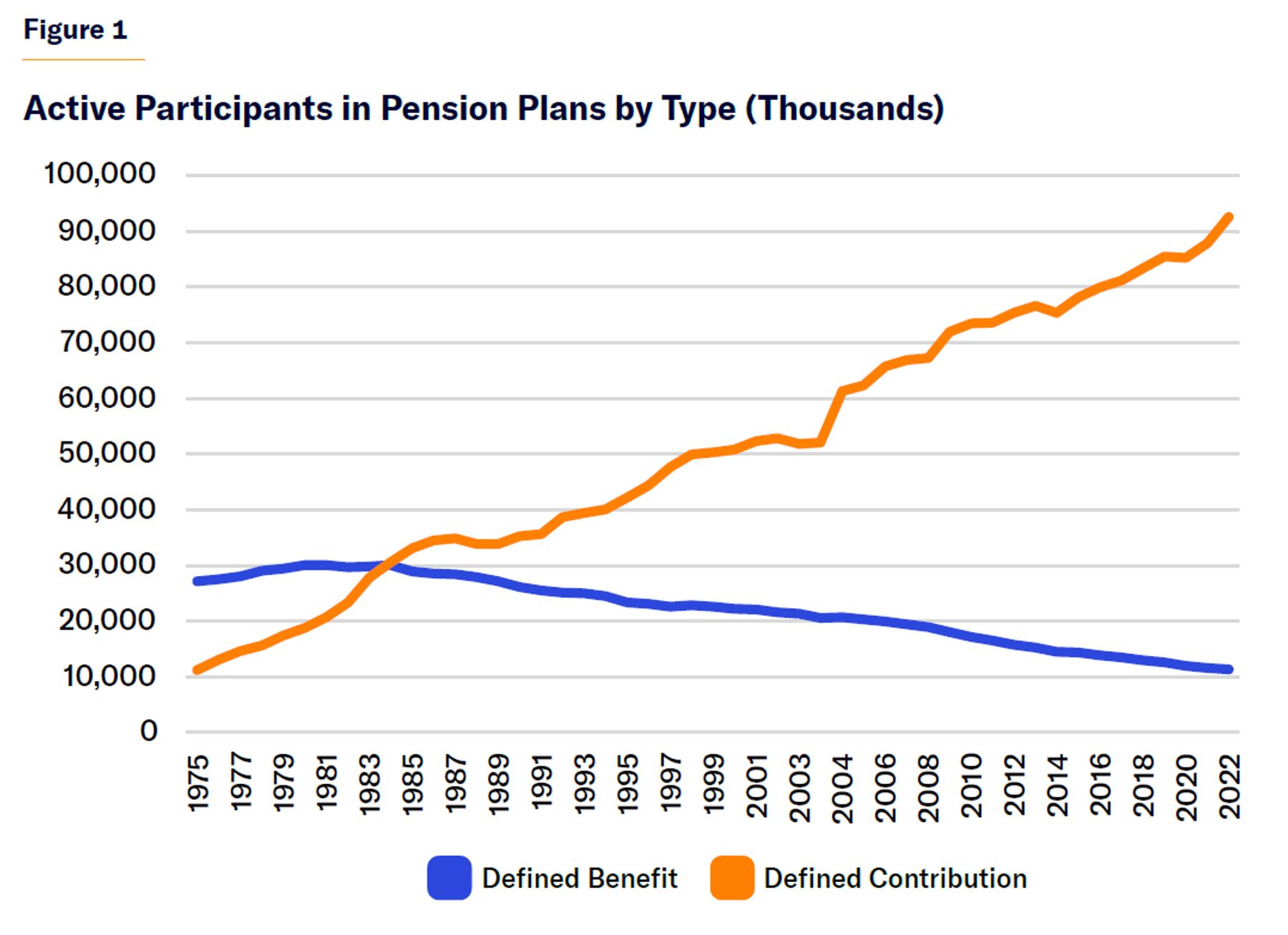

Throughout the 20th century, Social Security was expanded to cover more workers. And more firms offered private pensions to supplement (or, in the case of public-sector workers, replace) Social Security. Defined-benefit pensions could be fairly generous but only for workers who stayed at the same firm for most of their career. The fortunate few who combined a full pension with Social Security enjoyed worry-free retirement, which is what people often romanticize. But for most people, this was not the reality. Furthermore, that model was never sustainable. Providing such benefits and bearing all the risk proved costly for employers, who often underfunded pensions or failed to account for long-term liabilities.

In 1974, the Employer Retirement Income and Security Act forced corporations to better fund and account for the risk of their pension plans. As the true cost of defined-benefit pensions became more apparent, many private-sector firms phased them out. Instead, employers offered defined-contribution plans, such as the 401(k), which was created by legislation in 1978. These plans, which were viewed as a supplement for Social Security, were cheaper and less risky to employers. Defined-contribution plans made more sense for a mobile workforce in which most people have several employers throughout their career.[5]

About 60% of Americans today[6] have Social Security and a retirement account—their two main ways to save for retirement. But the purpose of a retirement account is not clear to many people. Is the goal to accumulate wealth, or to provide income, as a defined-benefit plan did? Improving the structure and design of 401(k) programs first requires that we understand their purpose.[7]

Three-Pillar System: The Old Ideal for the 20th Century

In 1994, the World Bank, drawing on the experience of several Latin American and Eastern European countries, proposed a multi-pillar retirement system model.[8] In this framework, income comes from three sources: government benefits, employer pensions, and individual savings. The approach was flexible enough to work across countries and remains common throughout the world. Each pillar had a distinct function. The first pillar, government benefits, offered a minimum-income floor that is paid for life and doesn’t vary with the market. This could be a flat benefit or, as with Social Security, a progressive one. It replaces most preretirement income for low earners but much less for higher earners.[9] Funding can be either advance-financed or pay-as-you-go, supported by taxes from current workers.

The second pillar is a mandatory savings scheme, offered by the government or employers. This could take the form of a defined-benefit pension or a defined-contribution plan, but participation would be mandatory. Importantly, this would be fully funded but not financed by taxes. According to the World Bank, these two pillars should be able to replace 40%–50% of preretirement income.

The third pillar is additional private savings, for those who are willing and able to save more. This can involve savings accounts, which might or might not have a tax benefit.

The current U.S. system is a hodgepodge of these three pillars. Social Security is a form of pillars one and two, and the 401(k) system is a mix of pillars two and three. But what each is meant to cover, from a risk perspective, is unclear.

The World Bank three-pillar model provides a useful framework to think about distributing risk and integrating state, occupational, and individual benefits. It was useful for developing countries as they reformed their retirement systems and made their pay-as-you-go state pensions more sustainable. It was also helpful for understanding the worldwide transition from defined-benefit to defined-contribution pensions.

But since the 1990s, the three-pillar model has fallen short. Defined-benefit plans have become even more rare in the private sector, and we now have the first generations retiring with 401(k)s. The three-pillar model has difficulty taking account of these developments because the retirement accounts that many countries adopted for pillar two largely focus on wealth rather than on income. The result is that retirement accounts have evolved without providing a good solution for longevity and income risk in retirement. People are therefore unsure of what their income can provide and are exposed to market shocks in their most vulnerable years. When the multi-pillar system was first developed, these issues were not as pressing because fewer people retired with defined-contribution assets.

Rethinking the Three Pillars

Reforming the retirement system requires redefining the three traditional pillars to reflect today’s realities, as well as adding a new pillar.

- Mandatory state benefit: A minimum guaranteed benefit that provides income redistribution and replacement (Social Security).

- Secure income from retirement accounts: Savings funded by employers, individuals, or both (401(k), IRA, etc.) that are converted into predictable income to supplement Social Security. This income could come from annuities, laddered bonds, or other low-risk options. Secure income is financed from a retirement account, funded either by an employer or individual or both.

- Market-based savings: Retirement accounts and other savings invested in riskier, liquid assets, which can fluctuate with markets but help cover discretionary expenses such as travel or dining; the balance between pillar two (secure income) and pillar three (market assets) will vary by individual, depending on preferences and needs.

- Part-time work: Continued participation in the labor force, in flexible or reduced roles, in order to supplement retirement savings and Social Security.

The updated versions of pillars two and three help turn defined-contribution plan assets into stable income. These offer a more flexible framework that can be scaled to the entire population, no matter their financial situation or risk tolerance.

The new pillar—part-time work—need not be arduous or time-consuming. Advances in technology now make flexible arrangements more feasible than ever, especially with new technology that offers flexibility. Beyond the significant financial benefits, staying connected to the labor force promotes mental and physical health. This pillar need not apply during all of retirement: some may choose to work in their sixties to mid-seventies and then fully retire; others might leave the labor force for a while and then return.

Implementing all four pillars will require significant, but low-cost, policy changes. Most Americans already participate in Social Security and hold a retirement account. Yet Social Security is on an unsustainable path and needs urgent reform—that has been a political nonstarter for decades. Reform may be more palatable, however, if framed as part of a broader overhaul of the whole retirement system. While some households might face lower benefits and changes to tax status, improvements to the other pillars can help offset these with other stable sources of income. Social Security reform must therefore be pursued alongside changes to the other pillars.

Pillars two and three require regulatory reform. The market currently offers few ways to turn retirement assets into income options, and Americans are accustomed to viewing their savings in terms of wealth. To encourage that shift, we can offer more tax benefits to annuitization and use technology to offer people more assistance in making complex financial decisions. Another roadblock is that plan record keepers—who administer workplace retirement accounts—are reluctant to make investments that shift the focus from wealth accumulation to income.

Pillar four will require policy changes that create better incentives for work at later ages, for workers as well as employers. Many Americans want to continue working but face age discrimination from their employers. Policy cannot solve this problem entirely but can make hiring older workers, even on a part-time basis, more appealing. Doing so will have macroeconomic benefits, since more people are working and paying taxes, which alleviates some of the financial pressure of an aging society.

This report outlines policy changes to make this framework a reality—improving retirement security for all Americans at little cost to taxpayers, young and old alike.

Pillar One: Social Security Reform

Social Security is on a course to insolvency. By the mid-2030s, revenue is projected to cover only about 85% of benefits. Without reform, retirees will face deep benefit cuts, workers will face steep tax hikes, or the government will have to commit to running larger deficits every year into perpetuity. None of these options is viable. The sooner action is taken, the less costly it will be.

Any successful reform to Social Security must begin with accepting reality. Contrary to progressive rhetoric, simply increasing taxes on higher earners—even at 1950s levels—will not fix the problem. It would simply increase marginal tax rates well above 50%, leaving little room to raise revenue for other priorities. A durable solution entails some combination of tax increases and benefit cuts. This may be politically toxic, but delay is costly. Many Americans have already lost confidence in the long-term viability of a program that is supposed to provide risk-free retirement income.[10] Putting the program on a sustainable path is critical to retirement security.

Any reform to Social Security should maintain some key aspects of the program. First, it must remain a form of insurance and forced savings that guarantees a minimum, risk-free income in retirement. Many people simply do not save adequately for retirement,[11] so a forced savings program is important in order to prevent people from ending up dependent on old-age welfare. Second, the program should remain universal—and not strictly a form of welfare—which has always been key to its popular support. Third, Social Security should continue to be redistributive, offering lower earners a higher replacement rate. The precise balance between universality and redistribution can be debated, but policymakers should not try to fundamentally change these key aspects of the Social Security program. Finally, any benefit cuts—whether through lower payments or a higher retirement age—should be phased in slowly and not applied to current or near-retirees, so that people have time to plan and save.

The first reform to consider is the retirement age. The normal retirement age has gradually risen and now stands at 67 for anyone born after 1960. But the early retirement age—when benefits first become available—has remained at 62.

Many Americans retire early: about 25% at 62 and about 50% before 67.[12] Some retire early for health or caretaking reasons, some because they want to, and others because they have problems finding work. Any meaningful reform must address early retirement: protecting those who cannot work longer while encouraging others to remain in the labor force. A sensible approach would be to raise the early retirement age from 62 to 65 over the next few decades and index the normal retirement age to life expectancy.

In practice, this approach would involve approximately a one-month increase in both retirement ages every two years—which would eliminate about 18% of the long-term shortfall.[13]

Opponents of raising the retirement age argue that those with physically demanding jobs often cannot continue to work into their late sixties. That concern is valid, but such jobs are becoming less common.[14] For the increasingly small group of people in this category, early retirement can continue to be an option. But that reality does not justify keeping early retirement open to everyone.

One approach suggested by the Social Security Administration is to create an exemption to any increases in the retirement age for low-income workers. In their calculations, they assumed that this exemption would be available for people who have paid in to the program for 25 years and have an averaged index monthly earnings (the average of their lifetime earnings adjusted for wage inflation) below 250% of the poverty level. If this exemption is paired with increasing the early and normal retirement age by one month every two years, only about 14% of the shortfall is eliminated.[15]

This exemption is a good start but might not go far enough. Another alternative is expanding disability to cover people who need to retire earlier with an exemption based on the nature of their work and their physical condition, rather than income alone.

Another criticism of increasing the retirement age is that it makes the program more regressive because lower earners tend to die earlier and have fewer years to collect benefits. This can be addressed by making the program more progressive in other ways—by decreasing benefits for high earners or lowering the replacement rate on the highest tier of income. One idea is to determine benefits for those with incomes above the 30th percentile using price inflation rather than wage inflation. Currently, Social Security benefits are calculated by taking the 35 highest-earning years and indexing past wages to current dollars. A progressive replacement-rate formula is then applied to that average income: 90% of the first $1,226, 32% of earnings between $1,226 and $7,391, and 15% above $7,391, up to a maximum benefit. Using price inflation rather than wage inflation to calculating average income for the higher earners would lead to lower benefits because price inflation tends to grow at a lower rate. According to the Office of the Chief Actuary at the Social Security Administration, this proposal would reduce 44% of the long-term shortfall.[16]

Another possible reform is to increase the payroll tax on income above $250,000. The increase should be lower than the 12.6% rate that some Democrats have proposed, which would be an enormous hike and leave little room for other tax increases. But we could introduce a smaller tax, similar to the Medicare premium of 2% on income above $200,000 (in 2017 wages). If benefits are not increased, this would reduce another 7% of the shortfall.[17]

Ultimately, policymakers will need to pull some combination of three levers: raising the retirement age, increasing taxes, and reducing benefits. This brief’s plan—raising the retirement age and making benefits more progressive—would close about 65% of the funding gap. Additional steps, such as deeper benefit cuts or higher taxes, might still be needed to restore solvency. But the plan preserves the program’s core principles: forced savings, universal insurance, and redistribution—features that have long underpinned Social Security’s popularity.

Pillars Two and Three: Income from Defined-Contribution Plans

Social Security is important but is not and should not be the only source of income for most retirees. Unless they are very low earners who get a relatively high replacement rate from the Social Security, they will need to rely on other forms of income.

For about 60% of Americans, that saving comes from some form of workplace pension benefit, either a defined-contribution or defined-benefit plan. Defined-benefit plans were more popular in the 1960s and 1970s but proved too expensive for most firms. Since the 1980s, defined-contribution plans, to which both employers and employees contribute, have become more common for private-sector workers. Shifting risk to workers is not always popular but made it possible to expand coverage to millions more workers.

In many ways, the shift to 401(k)s has been successful: more Americans have retirement assets than ever before. But the defined-contribution system can be improved. The problem with the current system is that it was originally designed to supplement a defined-benefit plan, not replace it. That is why individual retirement accounts are still designed and understood as a way to build wealth rather than to provide income in retirement.

These goals—building wealth vs. providing income—may sound similar, but they require different investment strategies and communication from the start. Wealth accumulation focuses on maintaining or growing assets, while income in retirement requires converting savings into predictable cash flows. Nearly every aspect of the 401(k) system emphasizes wealth accumulation, from the way assets are invested to how plan materials define success. Lacking tools to think in income terms, many retirees fall back on crude rules of thumb, such as withdrawing 4% annually or relying on required minimum distributions (RMD).[18] That leaves them exposed to big swings in income each year.[19]

The most straightforward solution would be to offer simple, inflation-linked annuities within the retirement plans. As participants approach retirement, they can see how much income they can get from their wealth, depending on how much of it they want to annuitize and when.

But the market for annuities remains thin, and demand is limited. Scholars have offered several explanations for this: low interest rates have made annuities expensive; savers often lack education or access; many prefer liquidity for health expenses or inheritance; and some simply distrust insurers.[20] Reluctance is compounded by the fact that most retirement plans are not set up to offer annuities as in-plan options. Yet as more Americans retire and seek stable income, demand for income-oriented strategies will grow. Experiences in the U.K. and Chile offer lessons for how to make this market work better in the United States.

Changing the Focus to Income: The Case of Chile

Chile is one of the few countries with individual pension accounts that have been successful in providing retirees with stable income. In 1981, Chile moved to an individual account system, in which workers contribute some of their income to an account with investment options that they can choose. This system has allowed Chile to become one of the few countries with a well-functioning annuity market: more than 60% of retiring Chileans buy annuities.[21]

One reason annuities are so popular in Chile is that the alternative is limited. Traditionally, Chile did not have a significant Social Security-style pension that guaranteed lifetime income. Instead, retirees who do not buy an annuity must enter a government-run phased withdrawal program, which pays out their savings in installments. If their savings are too low, the government provides a minimum benefit. Wealthier retirees sometimes choose phased withdrawals because the money remains liquid—and whatever is left can be passed on to heirs if they die before the account is exhausted.

But most Chileans chose the annuity. They can comparison-shop in the years leading up to retirement, using a government website that lists annuity prices from about a dozen providers and with comparisons with the payouts from the withdrawal program.

Chile’s experience shows that a successful annuity market is possible and that, with the right technology and communications, many people can think in terms of income and make an informed choice about buying an annuity. However, some research suggests that the annuity market would not work quite as well if the Chileans also had a state benefit or the option of partial annuitization.[22]

The success of the Chilean annuity program must be tempered with the experience in the United Kingdom. Until 2015, U.K. retirees were required to buy an annuity with the pension savings from their employer-sponsored accounts.[23] But the requirement was very unpopular and was therefore repealed, so savers can now simply spend down their savings as they wish. Upon retirement, 25% of the account can be taken as a tax-free lump sum, and the rest is taxed as income as it is withdrawn. Retirees may choose some kind of drawdown plan that helps them know what to spend each year, but their assets are still invested in markets and subject to fluctuations.

The reason for the unpopularity of annuities may have been the low-rate environment that made them very expensive. Demand fell after 2015; but notably, as rates increased, demand for annuities has returned and may exceed demand before the annuity requirement was repealed.[24]

A government-run platform—which can be fed into record keepers or hosted by a government agency—is also possible in the United States. Currently, the process of buying an annuity is not simple. Most people go through brokers who have mixed incentives and often try to up-sell complex features—including the promise of liquidity. This has helped give annuities a bad name, which can make people more reluctant to hand over the wealth that they have accumulated.

A better solution would be to let participants buy an annuity—or opt in to an income option—directly on their retirement plan’s website. But plan sponsors face hurdles. As fiduciaries, they worry about liability if an insurer later fails to make payments or if participants regret the purchase. Congress addressed this in 2008 with a “safe harbor” provision that shields sponsors from liability if the annuity provider is financially sound. Yet the criteria were vague and difficult to apply, so most sponsors remained cautious. The SECURE Act of 2019 attempted to clarify the rules,[25] but many in the industry argue that it still falls short.[26]

The other hurdle is record keepers, who keep track of pension contributions and asset returns. Sometimes the record keeper is the provider (Vanguard, Fidelity) but can also be a payroll company (ADP), an insurance or investment company (Empower, Prudential), or simply an independent record keeper. Because record keeping is a low-margin business that carries a significant liability for any errors, many have been hesitant to include income estimates and offer annuities on their platform.[27] In addition, it can be costly to develop the technology necessary to offer multiple income options (including fresh annuity prices). A GAO report found that insurance companies that act as record keepers sometimes offer only their own annuities, which are often complex, high-fee products.[28] According to GAO, large plan sponsors would have to demand that record keepers invest the resources to allow for annuities to be on the platform and offer more annuity options.

But regulation can make this happen. One possibility is for the government to host an annuity auction website where several high-quality insurers offer annuities with real-time quotes—similar to what is used currently in Chile and used to be available in the United Kingdom. Record keepers can include this on their platforms, along with Social Security cost projections.

Another option is to set an income strategy as the Qualified Default Investment Alternative (QDIA) after participants retire. Today, more retirees than ever keep their savings in 401(k)s; yet the retirement phase requires a different approach and greater guidance. The industry has lobbied to make annuities the default, but that would lock participants into costly and illiquid products. A better default would be a laddered bond portfolio—bonds structured to provide steady annual income through coupon payments or maturities. This approach mimics the predictability of an annuity but remains liquid and reversible. Paired with a deferred annuity, it can also provide protection against outliving one’s assets.

Another challenge is a duration mismatch between common savings vehicles. One common vehicle is the target date fund, which at first is invested in equity, but invests more in bonds as the plan participation ages. A target date fund typically invests half in bonds and half in stocks at retirement age and beyond. The bonds are mostly short-term, which ensures a more stable nominal value. But a bond portfolio that can deliver consistent income—such as a laddered bond option—has the duration of longer bills. This exposes savers to risk with the income they get in retirement because the value of an annuity or laddered bond portfolio moves more than the value of their assets. The result is that income in retirement can vary greatly, depending on where rates happened to be on the day they retired.[29]

Again, regulation and technology can solve this problem. Target date funds that meet QDIA standards can invest their fixed-income portfolio in longer-duration bonds. This would mean more variable asset balances, which might make savers hesitant, so savers should be encouraged to think of their retirement accounts as income in the future. The SECURE Act required income estimates on 401(k) statements in addition to the account balance. That was is a good start, but income estimates are often not featured prominently; the account balance is still the primary goal.

Another challenge is that many Americans retire with several accounts across different employers, with some workers accumulating as many as 10 accounts.[30] It is not uncommon for some savers to lose track of these accounts. To achieve the best possible annuity terms, these accounts must be combined. Also, realistic income projections require information about a person’s full financial situation, which includes active live estimates of the balances of every account. Regulation should make the process of rolling over retirement accounts easier. Currently, when you change jobs, taking your retirement account with you to your new job requires much paperwork. One way to address this problem has been implemented in the Netherlands:[31] a government-hosted dashboard that tracks all accounts through one’s Social Security number. The same platform can include various income quotes on annuities, on a live auction, if retirees wish to annuitize some fraction of their income.

Pillar Three: Riskier Income

Not all retirement savings need to go toward income products like annuities. Some savings should stay as wealth and can be invested with this purpose. Retirement wealth may go toward funding health care, end-of-life expenses, or to an inheritance for children. It can also fund income, especially for discretionary spending. This is essentially what people do now with their retirement account and other assets.

Some people may feel that Social Security provides enough for their predictable income needs and will thus invest all their retirement savings in riskier assets and spend only their RMDs or use a crude spending rule like the 4% strategy. Others will prefer the security of an income-based solution that is protected from market and inflation risk and invest all their retirement assets in an annuity or equivalent. The right combination is unique to each family, depending on the amount that they have saved, their sense of longevity, their spending needs, and their risk aversion. Two families with near-identical asset balances may have very different preferences.

The challenge for retirement policy is to help people make the right choice in a way that is scalable to the entire American population. This can be achieved with better technology that can help families weigh the trade-offs and see how much of their retirement assets should support income and how much should be kept as wealth. This may include access to financial planning websites that input Social Security data, annuitized income, and financial wealth.

Much of the burden will fall on record keepers—the firms that keep track of pension accounts, salaries, contributions, and asset returns—which in the past have been slow and reluctant to innovate and offer plan participants access to better financial planning tools. But the burgeoning fintech industry may offer more options to savers who can’t afford advice. Tools like artificial intelligence can offer these savers sophisticated income and wealth strategies.

Pillar Four: Working Longer and Better

The fourth pillar is income from work. Work in retirement has become a politically divisive issue. Some claim that work is necessarily physically arduous for most older Americans.[32] But there is no evidence that this will necessarily be true going forward, as fewer jobs are physically demanding and as older workers gain other options.

According to the 2024 Current Population Survey, about 16% of Americans over age 65 are still in the labor force, and they tend to be better educated. How much of this is due to the voluntary decision to retire and the people who have been pushed out of their jobs is unclear.

Working longer offers many benefits, including healthier aging,[33] socialization, and a sense of purpose—and, of course, it can be financially transformative for retired households. But working past 65 or even 70 need not resemble work at younger ages. Instead, the future of retirement may be semiretirement: working part-time or going back and forth into the labor market with more flexibility. A few regulatory changes, both to enhance labor-market fluidity and counter age discrimination, will help make this possible.

New technology has made work from home or gig work increasingly possible, which opens up more options for flexible and less physically taxing work that is ideally suited to semiretirees. This may explain why older Americans are one of the largest growing groups of entrepreneurs,[34] as they are forming small businesses and consultancies that offer more flexibility and income. Data from the Current Population Survey reveal that in 2024, 4.7% of Americans over 65 were self-employed, compared with 3.9% in 2000. Most of the growth was in unincorporated businesses. Self-employment rates for other groups stayed flat or even fell.

But challenges remain on both the supply and demand side when it comes to older workers. On the demand side (the desire to hire older workers), many who want to work face age discrimination in their current job or when seeking a new job that better suits their lifestyle. This could be addressed by regulations that make it more cost-effective to retain older workers and increase the demand for them. On the supply side (older workers who are available to work), we can tweak Social Security to encourage more people to work longer in a variety of arrangements that suit their financial needs and lifestyle.

Demand Side

Many older Americans would like to work longer but have problems finding work or are forced into an earlier retirement than they would prefer. One report suggests that more than half of older workers are pushed out of jobs before they want to leave, at which point it can be extremely difficult to find new work.[35] In some cases, this is due to simple age discrimination. But employers might be worried about the risk of running afoul of age-discrimination laws that make it harder to fire older workers. Older workers also cost more: they have been at work longer and earn higher salaries. They might also add to health-insurance costs by requiring more health-care services and making the pool of workers less desirable to insurance carriers.

A way to encourage employers to hire and retain older workers is to make them cheaper. We can reduce the payroll tax for workers over 62 who already have 35 years of paying in to Social Security.[36] Another option relates to health care. Employers are currently required to offer health insurance to all employees, no matter their age. In 1980, Congress passed the Medicare Secondary Payer Provision, which makes Medicare the secondary payer if an eligible worker has access to an employer health plan. The result is that older workers still are on employer health insurance. The goal of the legislation was to keep employers from shifting costs to Medicare, but as people need and desire to work longer, this may be counterproductive. Repealing it would indeed put more costs on Medicare, but if it increased the demand for older workers and kept them in the labor force for longer, it would mean more tax revenue, including payments into Medicare.

The Secondary Payer Provision makes older workers more expensive and less desirable. It drives up premiums because older people require more health-care services. One option is to repeal Secondary Payer Provisions so that employers do not have to offer insurance to anyone who is Medicare-eligible. And they will not have to pay Medicare premiums, which would not only lower health-insurance premiums for all other employees but would make older workers cheaper relative to younger workers, since health care is a significant expense.

Older Americans who desire a more flexible arrangement may prefer to work as contractors or do gig work—but the government can stand in the way. States like California should repeal laws like AB5, which forces employers to recognize their contractors as employees who are eligible for health care, minimum wages, and overtime. AB5 resulted in a decline in self-employment in California and little increase in the number of employees.[37]

At the federal level, the Department of Labor should reinstate the independent contractor status under the Fair Labor Standards Act,[38] a rule that was initially enacted during the first Trump administration but replaced during the Biden administration with a rule that emulates many features of AB5.

Supply Side

We can also tweak policy to encourage more work. For example, people who retire early are still subject to an earnings test, or their benefit is reduced for each dollar earned above a certain threshold. This used to be the case for everyone who claimed Social Security, but it no longer applies to people above the full retirement age. Recipients do get a credit that results in higher benefits in the future for the forgone benefits, but many people view the earnings test as another tax on work.[39] Eugene Steuerle of the Urban Institute has suggested allowing Social Security recipients, of all ages, the option to take partial benefits.[40] These could supplement part-time work, and the part of the benefit they delay would also receive credits. Ideally, benefits could be adjusted as retirees’ income needs and incomes change from one year to the next. This not only increases the incentives to work but, because the benefit is quite generous, helps smooth income variability for retirees pursuing flexible arrangements like entrepreneurship and gig work.

There is no earnings test for workers beyond the full retirement age, and retirees can pause and reclaim benefits and get credits for declaring income from work, though the process for doing so is not widely known or transparent to beneficiaries. This can easily be fixed with technology on the Social Security website that would enable retirees to adjust benefits with their needs.

Another potential change is increasing the age at which retirees can delay Social Security. Currently, there is no benefit to delaying Social Security past age 70, but there are substantial financial benefits to waiting until then. This age can be increased to 75 or just increased with the normal retirement age proposed in an earlier section of this paper.

Reframing Retirement

The American retirement system works much better than it gets credit for: many Americans have acquired substantial assets; Social Security needs reform, but it can be fixed without a total overhaul; and, as people live longer and healthier lives, they have more options to work longer, which provides another source of income. Technology has opened new possibilities in terms of advice in asset management that can improve retirees’ experience with their 401(k)-type plans and Social Security. Technology can make possible new forms of work that provide different forms of income in retirement.

Many low-hanging reforms could raise retirement income and reduce risk for retirees. Yet our system remains hamstrung by an outdated mind-set that treats each source of income in isolation. We need to rethink retirement financing as an integrated whole, combining multiple sources of income and insurance. Done right, reform could dramatically improve retirement security for Americans—at little cost to taxpayers, while putting the country on a more sustainable fiscal path.

Endnotes

Photo: Xavier Lorenzo / Moment via Getty Images

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).