Modeling Tax-Revenue Erosion in American Cities

Photo: tarabird / iStock Editorial / Getty Images Plus

Introduction

New York City has had its share of public health crises and pandemics, from cholera in the 1830s to influenza in 1918 and the coronavirus in 2020. Disease, after all, is one of the demons of density. In each instance, large numbers of people left the city, particularly higher-income residents with the means to move. And this year, according to one estimate, some 420,000 residents had left New York City by May.[1]

Yet even as many people throughout history have left cities during crises, in time they have returned and more new residents have followed in their wake. Physical and public health infrastructure improve in response, new jobs and firms are created, and cities like New York recover. The benefits from urban living outweigh its costs. Science is also more advanced than in previous public health crises, making cities not only more resilient and safer but also likelier to find better remedies faster.

Still, there is reason to be concerned that this time may be different—that out-migration from New York City will critically erode the city’s tax base over the long run. Technology has made it easier than ever to work remotely, and the pandemic has helped break down cultural and institutional barriers to remote work. During the pandemic, the share of fully remote U.S. workers has leaped from 5% to at least 50%. While we can’t predict how many workers will return to their offices after the pandemic ends, many will likely continue to work remotely. Even a small share of the workforce staying remote, to some degree, post-pandemic would have a large and lasting impact on the makeup of local economies such as New York’s.

Recent tax changes also might make New York’s fleeing high earners less enthusiastic about returning. The federal income-tax cap on the state and local tax deduction (known as the SALT cap), instituted in 2018, increased the effective state and local rates paid by many taxpayers throughout the country and, in effect, magnifies the higher marginal tax rates of the city relative to other competing jurisdictions. For a top-bracket New York City taxpayer, the combined federal, state, and local income tax actually increased by about 1.25 percentage points, despite the cut in federal rates.[2] Furthermore, a lower-tax state such as Florida suddenly became 3%–5% less expensive in taxation for wealthier residents than New York City. How these higher costs in taxes outweigh the other benefits that residents receive from living in New York remains to be seen, and taxpayers may have expected federal tax law to change or have been skittish to leave based on taxes alone, thus delaying potential relocations.

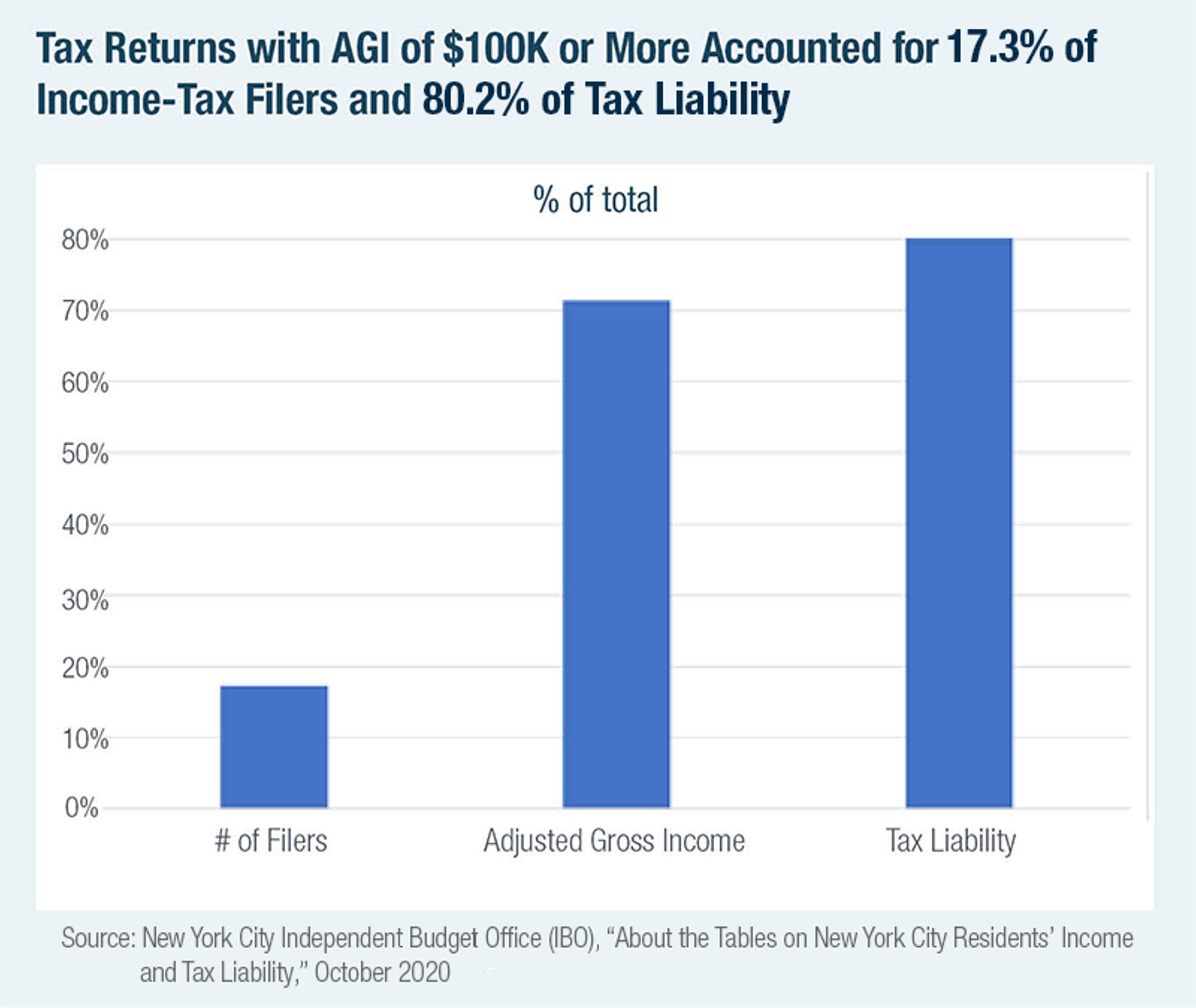

New York City is heavily dependent on its high earners for revenue. In 2018, the 17.3% of filers reporting $100,000 or more in adjusted gross income accounted for 80.2% of New York City’s income-tax revenue, which, in turn, accounts for 22.6% of the city’s total tax revenue.[3] Such taxes apply only to Gotham’s residents, thus providing an incentive to establish residency elsewhere, even to just outside the city’s boundaries. The city’s unincorporated business tax is easier to escape. It taxes firms operating in multiple jurisdictions based on where services are performed, so individuals working from a second home outside the city could allocate their income there, beyond the reach of the city’s tax. And, of course, anyone not living in or visiting New York City is unlikely to be paying the city’s sales taxes.

In this paper, we consider three scenarios for the future of New York City’s tax base. The first is a departure of 1% of the city’s high earners (defined in this brief as filers earning $100,000 or more in aggregate income) and a 5% decline in unincorporated business taxable (UBT) income. The city also would lose out on sales tax that otherwise would have been paid by departing high earners. This scenario would result in an annual loss of $220 million in tax revenue. The second scenario: if 3% of high-income New Yorkers left the city’s tax rolls and income subject to UBT dropped by 10%, the city loses out on an estimated $576 million every year. The third scenario: a 5% loss of New Yorkers earning $100,000 a year or more would result in an annual loss of $933 million in revenue, or roughly the amount that the city allocates for its Department of Health & Mental Hygiene, a public health agency now on the front lines of the Covid-19 pandemic.[4]

These estimates do not consider the impact that the loss of wealthy New Yorkers would have on other city revenue streams, such as the corporate income tax, or other harder-to-quantify spillover effects on the economy and other taxes. Rather, they represent the annual impact on a select set of local taxes of a one-time increase in out-migration, above and beyond New York’s regular annual net out-migration (for UBT, that is defined as an allocation of income outside New York City). Any increase in out-migration would likely occur over time, rather than all at once. Regardless of one’s opinions on the city’s wealthy, their tax contributions represent a disproportionate share of public revenues at a time of severe budget constraint and great need for city services. As such, New York City’s ability to attract and retain high earners will be crucial to the city’s recovery after the devastating impact of Covid-19 and urban unrest, among other recent challenges.

Historical Background

Great cities like New York are magnets for talent; proximity enables greater productivity as knowledge and know-how are more easily exchanged.[5] Density, as well as the interaction that it enables, allows cities to be more than the sum of their parts.

But density and interaction can also be a city’s Achilles heel. Viruses spread just easily as ideas, if not more so. In New York, people come into close contact with a large variety of people all day long. Recent studies have shown that it is not so much density as it is population and connectivity that have enabled the spread of Covid-19 in recent months; but for New York City, this is cold comfort.[5]

In the late 1700s and for much of the 1800s, New York City suffered regular and debilitating public health crises—from yellow fever epidemics in 1795, 1799, and 1803, to cholera in 1832, 1849, and 1866, along with countless more outbreaks.[7] About 1.5% of New York City’s population died from the yellow fever outbreaks in and after 1795, and 5% died in the 1832 cholera epidemic.[8] Several other epidemics in the 1800s claimed the lives of more than 4% of the city’s population.[9] By 1900, nearly 50% of all deaths in America’s major cities were caused by infectious illnesses.[10]

Yet just three decades later, in 1930, fewer than 20% of urban deaths in America were attributed to infectious disease. Urban leaders recognized the enormous toll exacted by pandemics and, at the beginning of the 20th century, began spending as much on clean water as the federal government spent on everything save the military and the post office.[11] These and other 20th-century advances in public health sharply curbed the urban death toll from disease. Though New York City’s percentage increase in mortality from the pandemic of Covid-19 has been the greatest since the cholera epidemic of the 1830s, overall mortality rates today are still only back to where they were in the early 1990s (approximately 9 per 1,000).[12]

Such dramatic advances in public health staved off not only death but regular bouts of pandemic-fueled out-migration. In 1795, about a quarter of the city’s population fled yellow fever in New York City.[13] And a third of the city’s population left to escape cholera in 1832.[14] The New Yorkers most likely to flee outbreaks were those residents most able to leave and with the greatest means, often heading to homes in the country.[15] In 1832, the New York Evening Post reported how, in the face of a deadly outbreak, “The roads, in all directions, were lined with well-filled stagecoaches, livery coaches, private vehicles and equestrians, all panic-struck, fleeing the city, as we may suppose the inhabitants of Pompeii fled when the red lava showered down upon their houses.”[16]

The ebbs and flows of epidemic, flight, and return reshaped cities and the areas to which urban residents fled. Sometimes flight led to permanent exodus and significant development in former outskirts, or what we might now refer to as suburbia. Before what became known as Greenwich Village was annexed into New York City, a yellow fever epidemic in 1822 caused mass migration to the then-small rural village, spurring rapid development north of the city’s borders.

New York City’s Population, Pre- and Post-Pandemic

Even before the pandemic, New York City’s population was declining.[17] Between July 2018 and July 2019, New York saw net out-migration of approximately 1.6% of its population, and some 60% of net out-migrants decamped to the city’s suburbs and exurbs, as Bloomberg’s Justin Fox notes.[18] This pre-pandemic baseline is notable but hardly catastrophic. But according to a review of U.S. Postal Service data, New York City residents filed 295,103 change of address requests from March 1 through October 31, with each change possibly representing an entire household, each which may contain more than one person. Top destinations included the city’s suburbs in Long Island, Westchester, and New Jersey, with South Florida and Southern California as leading relocation spots outside of the New York metro area. The top Zip codes for departing New Yorkers represents a laundry list of its wealthiest What is not known is how many individuals these household address changes represent or just how permanent these requests are.[19] What is not known is how many will leave the New York City metro region entirely, which is greatly determined by job opportunities.

We know that people generally move locally far more often than they move between states. In addition, people are most likely to move for job opportunities and housing. People who are married, have children in the home, or own a house—often associated with higher incomes—tend not to move as often.[20]

The Internal Revenue Service (IRS) publishes state-specific data on taxpayer migration by income range; it also provides migration data for New York City specifically, but not by income range. This information is available in a reasonably consistent form for the 2012–18 tax-filing years.[21]

State-level IRS data show that more high earners (defined here as those with adjusted gross income of $100,000 or more) leave New York State every year than move in, but the numbers are not large.[22] For most of the last seven years, there has been a net out-migration of high earners from New York State of more than 1%; on average, slightly more than 2.5% of high earners left New York while slightly less than 1.5% of the total moved in to the state. The net out-migration rate of high earners increased by just under 0.5% between the first three years of the period (2012–14) and the last three years (2016–18).

Over the last three years, an average of 25,700 high earners left New York State annually. The net out-migration rate of those earning over $100,000 a year is greater in New York than in any other northeastern state; it also is greater than net out-migration flows of lower-income groups from New York. Despite this annual exodus, the number of high earners in New York rises virtually every year because more people are pushed into higher income brackets as a result of inflation and increased income. Such growth and vibrancy are benefits to the city and its tax base.

A greater share of residents, on net, leave New York City than the state as a whole, but we don’t know which income range they fall into.[23] However, we do know that the average income of those who moved to Florida from Manhattan has nearly doubled over the 2012–18 period.[24]

With the current pandemic, this trend is likely to intensify. A New York Times analysis of cell-phone location data concluded that about 5% of city residents left in March–April 2020, totaling some 420,000 people. Most people went to New York’s Long Island or Westchester, and to nearby counties in Pennsylvania, New Jersey, and Connecticut; Palm Beach County in Florida also was a top destination.[25] Such out-migration from New York City appears to have continued well into July 2020, the latest period for which we have data.[26] Some 17% of the pre-pandemic population of Manhattan is still gone from the city, while the share of departures from the city’s richest neighborhoods has reached as high as 50%.

Residents of Manhattan and wealthier areas of Brooklyn were far more likely to leave the city than those living in lower-income areas, according to Joshua Coven and Arpit Gupta of New York University.[27] Across New York City, higher-income census tracts had the highest shares of departing residents, while lower-income areas had the smallest percentages leaving.[28] Social network data from Facebook show New Yorkers departing to areas of the country where they had strong social connections, suggesting that they were likely sheltering in second homes or with family and friends. Even trash-collection data suggest that relatively fewer residents remained in richer areas of the city than in less well-off areas.[29]

The Manhattan Institute’s recent poll of New York City, conducted in early July 2020, found that two in five New Yorkers say that they would leave the city if they had the ability to live anywhere they wanted.[30] Those most able to afford New York City were the most willing to stay. Still, some 33% of those earning $125,000 a year or more said that they would move “somewhere outside of New York City, but nearby,” or “somewhere far away from New York City.”

Another survey commissioned by the Manhattan Institute in late July and early August found that 44% of New York City residents earning over $100,000 have considered moving out of the city over the previous four months.[31] (New York residents earning six figures make up 80% of NYC’s income-tax revenue.)[32] More than a third of respondents (37%) said that it was at least somewhat likely that they would have a new address outside New York City within the next two years.

Will Those Who Leave Stay Away?

In past epidemics, although the city saw significant out-migration, its population—including its high earners—returned after the crisis abated. But there are two reasons that this time might be different: the rise of remote work and changes in the tax code.

Remote Work

Between 1960 and 2000, the share of the labor force working full-time at home never exceeded 3.5%, rising to only 5% by 2017.[33] The inclusion of those laboring out of the office in alternative workspaces, such as coffee shops, increased the remote share to 10%. A recent study using different data sources showed that in the initial response to the pandemic, the share of remote workers in America rose to 50% of the workforce by May 2020. By July, 22% of those who had initially switched to remote work had switched back to commuting.[34] Higher-income workers are much more likely to report being able to work from home,[35] and such work is generally believed to favor industries and occupations in which workers are better educated.[36] These types of educated workers and better-paying jobs are disproportionately concentrated in New York City. Moreover, the Northeast has the highest share of commuters switching to remote work.[37]

Recent surveys seem to indicate that a higher share of remote work may be here to stay, based on the preferences of workers and their employers. Many workers like working from home, with some even willing to accept lower pay to have the option.[38] A New York Times survey from July found that just 14% of New Yorkers currently working remotely say that their postcrisis ideal would be to return to the office full-time; the rest would either want to work from home one to four days a week (47%) or every day (40%).[39] Some 33% of New Yorkers currently working remotely say that they would move to a new city or state if remote work continued indefinitely.[40] As for employers, one-third of firms believe that remote work will remain more common after the Covid-19 crisis ends,[41] and almost a fifth of chief financial officers said that they planned to keep at least 20% of their workforce working remotely.[42] Overall, according to one recent analysis, an upper-bound estimate is that 37% of jobs in the U.S. might be possible to perform entirely at home over the longer term, although doing so might not be practical for many of these jobs.[43]

Tax Increases

Another factor that may weaken the city’s recovery in the wake of the pandemic is recent changes in tax laws—in particular, the cap on the state and local tax deduction, instituted in 2018 as part of the Tax Cuts and Jobs Act (TCJA). Previously, high state and local taxes were less of a burden on taxpayers who itemized their returns, as many could deduct these totals in calculating their federal taxable income. In 2017, the average state and local tax (SALT) deduction claimed in New York was $23,804.[44] Now, the most that can be deducted in federal tax filings is $10,000 in state and local taxes. This raises the effective state and local tax burden on wealthy filers. For a New York City taxpayer in the top income bracket, this effective increase in the impact of state and local taxes was large enough that the combined federal, state, and local income tax actually increased by about 1.25 percentage points despite the cut in federal rates.[45] Furthermore, the increase is greater where state and local taxes are high, such as New York, than where taxes are low, such as Florida. In New York City, some 10% of those filing income-tax returns were expected to see their tax burdens go up following the imposition of the SALT cap in 2018.[46]

An analysis of representative taxpayers conducted by the Citizens Budget Commission showed that this increase in state and local tax burdens could be quite large.[47] In 2017—prior to the SALT cap—taxpayers living in New York City with $1 million of income and two children paid nearly $50,000 more annually in combined federal, state, and local taxes than they would have if they lived in Florida. Now, under the 2018 tax law, the New York taxpayer owes $83,000 more than the Floridian. Total taxes would be 24% lower in Florida, amounting to an extra expense of 3.3% of income each year. If it was worth an extra $50,000 to live in New York previously, would it be worth an extra $83,000 now?

Existing research does not provide a clear answer as to whether these federally driven effective increases in New York taxes will induce wealthy individuals to leave New York City—or to stay away for good if they have already left. One study tracking 13 years of tax returns for millionaires across the country found that higher state taxes do lead to out-migration, but the effects were small—on average, a 1-percentage-point increase in tax differentials between states led to about a 0.2-percentage-point increase in the rate of net out-migration. This result was based on analysis of all U.S. taxpayers who earned $1 million or more in at least one year between 1999 and 2011. The relative increase in out-migration was greater for “persistent” millionaires who earned at least $1 million in eight of the years, but these people also tended to have lower baseline rates of out-migration.[48]

Other research has found bigger effects. A recent study of a large 2013 tax increase in California that raised rates 1%–3% on wealthier taxpayers found that it led to a 0.8% increase in out-migration. With the enactment of the SALT cap, a similar tax increase would have doubled the financial impact and likely further increased out-migration, according to the study.[49]

There is no simple answer to this question. Much of the research on the state and local tax deduction prior to 2018 found relatively little impact on taxpayer behavior, but past changes were much smaller than the TCJA change—and past research may not be a good guide.[50] Furthermore, taxpayers may expect the cap to be changed: the combination of scheduled federal tax changes in existing law, large federal budget deficits, and the possibility of different leadership in Washington all suggest that tax policies could change significantly in the next few years. Many high-income taxpayers might choose to wait until the dust settles before making major life decisions on the basis of tax considerations.

New York City’s Tax Base

In modeling our three possible scenarios for the future of the city’s tax base, we focus on three taxes: the personal income tax, the unincorporated business tax, and the sales tax.

Personal Income Tax

Revenue from the city’s income tax is highly dependent on upper-income filers, with a progressive structure rising to a top rate of 3.876%. The top 0.8% of tax filers (with adjusted gross incomes of $1 million or more) account for 40% of New York City’s income-tax revenue. As shown in Figure 1, taxpayers with adjusted gross incomes of $100,000 or more in 2018—more than 660,000 filers, or 17.3% of the total—account for 80.2% of the city’s income-tax liability. In other words, roughly one-sixth of New York City taxpayers pay four-fifths of the city’s income taxes.[51]

In contrast to most other jurisdictions, state law prohibits New York City’s income tax from being imposed on anyone but residents—there is no commuter tax. Thus, New York City residents who move and become nonresidents will escape the city income tax entirely, even if they continue to work or earn other income in New York City. They can do this even if they move to the city’s suburbs in Westchester or Long Island and remain New York State residents; such residents would continue to pay only the state income tax, not New York City’s.

However, a New York City resident cannot become a nonresident simply by moving to a second home in the Hamptons. The state tax department applies a two-pronged test to decide whether someone is a resident.[52] Persons are residents if:

- They are domiciled in New York City, meaning essentially that they have, intend to have, or intend to return to a permanent home in the city, even if they don’t spend much time there; or

- They are not domiciled in the city but spend part of at least 184 days of the year (i.e., just more than half a year) in the city.

But there is one related tax where work-from-home arrangements, even for a New York City-based business, might take substantial income of high earners off the tax rolls.[53]

Unincorporated Business Tax

New York City imposes a 4% tax on what are known as unincorporated businesses, such as partnerships, LLCs, and LLPs that carry on business wholly or partly in New York City. This tax often applies to white-collar partnerships, like some law firms, hedge funds, and accounting firms. The unincorporated business tax (UBT) accounted for $2 billion of revenue in 2019, or 3.3% of total city tax revenue.[54]

UBT is highly concentrated. 91% of UBT liability falls on so-called partnership taxpayers, the top 1% of which —138 firms—accounted for 44% of total UBT tax liability in 2016.[55] In 2016, the latest year for which published data are available, 32% of the tax liability was from law firms; 30% from securities and commodities brokers and dealers; approximately 20% from professional, technical, and managerial firms, such as accountancies; and another 9% from real-estate firms.

The financial industry provides an illustrative example of how this tax works. The majority of private equity funds and hedge funds are organized as LLPs or LLCs. Their profits typically come from a 2% management fee and a 20% share of the returns on invested capital (“carried interest”). In New York City, the management fees are subject to UBT, but carried interest is exempt. Both management fees and carried interest pass through to the New York City personal income-tax return and are taxed there.[56]

The tax is imposed on firms that do some or all of their business in New York City. For multijurisdictional firms, income is allocated to New York City based on the fraction of the firm’s receipts that occur within the city.[57] In most cases, receipts are treated as occurring where the service is performed.[58] If a service is performed from a partner’s home office in the Hamptons—even a rented home will do for this purpose—rather than from an office in the city, profits will be allocated outside New York City and will escape UBT.[57] (One exception is registered securities and commodities brokers and dealers, where receipts are treated as occurring where the customer is located.)[60] While some jurisdictions have changed their business-tax rules to avoid such a tax reduction, New York City has not done so. Philadelphia, for instance, deemed nonresident employees working from home because of Covid-19 who previously had performed taxable services physically in the city to be subject to the city’s equivalent of the UBT tax.[61]

Sales Tax

For the sales tax, we assume that sales-taxable purchases made by those leaving New York will also go elsewhere with them. We base these assumptions on the relationship between the sales-tax base and income, considering estimates of the portion of the sales-tax base paid by businesses and tourists.[62] The net impact of our analysis was that sales-taxable expenditures averaged approximately 21% of adjusted gross income of high-income taxpayers who leave New York.

Modeling the Revenue Impacts of Tax-Base Erosion in NYC

We consider the impacts of a 1%, 3%, or 5% departure rate of those making more than $100,000 a year (see Figure 2). “Departure” means leaving or establishing nonresident status. We assume that high earners leave at the same rates—that is, that the superrich do not leave at different rates from the very rich or very well-off.[63]

For the unincorporated business tax, “departure” means that a partner of a firm allocates his fraction of receipts outside the city’s boundaries. We assume that professional services such as legal, accounting, and some financial services will be more likely to allocate taxable receipts to places outside New York City, while services more likely to be performed in the city—such as arts and entertainment, trade, and real estate—will not.

In the first scenario (a 1% departure of high earners), we assume that 5% of affected services under the unincorporated business tax will be newly performed outside the city; in the middle (3% departure) and high (5% departure) scenarios, we assume that 10% and 15%, respectively, will be performed outside the city.[64] UBT assumptions do not quite parallel income-tax assumptions: the high assumption is three times the low estimate; whereas with the income tax, the high assumption is five times larger than the low assumption. This reflects the fact that the unincorporated business tax will be far easier to avoid than the personal income tax, particularly if remote work becomes more widespread, post-Covid. Several practitioners believe that actual out-migration could be greater.[65]

As shown in Figure 3, under the first scenario of a 1% departure of New York City residents earning $100,000 or more a year, the city’s tax receipts would decline by $220 million a year. This sum includes losses in personal income-tax receipts of $107 million, $84 million in unincorporated business tax revenue, and $29 million in sales taxes.

The second scenario, a 3% departure of high earners, results in annual losses of $322 million in personal income-tax revenue, $169 million from the unincorporated business tax, and $86 million in sales-tax revenue. In all, total annual losses in revenue reach about $576 million, a sum nearly $40 million greater than what the city allocated for Youth & Community Development in FY2021.

The third scenario, in which 5% of higher earners depart, would result in annual losses of $536 million in personal income-tax revenue, $253 million from the unincorporated business tax, and $144 million in sales-tax revenue. In all, total annual losses in revenue would total $933 million, greater than the amount that the city spends on its Department of Health & Mental Hygiene, which is tasked with public health and pandemic responses.

In the Appendix, we provide estimates of potential revenue losses under our three scenarios for the subset of high earners with $200,000 or more of adjusted gross income.

Conclusions

New York City’s dependence on high earners for revenue makes it uniquely vulnerable to tax-base erosion during periods of sustained out-migration. Given three years of declining population culminating in this year’s global pandemic and urban unrest—as well as tax increases (due to a lower SALT cap) and likely changes to the nature of work—the potential for lost tax revenue as a result of the departure of New York’s wealthiest is among the most pressing issues that the city faces. According to our estimates, New York City may lose roughly $220 million annually in income, sales, and unincorporated business taxes from a 1% departure of those earning $100,000 or more a year—rising to over $580 million annually with a 3% departure and over $900 million from a 5% departure. These are not forecasts but best-guess scenarios of what might happen if a one-time departure of wealthy New Yorkers meets or exceeds outflows of recent history, without the comfort of additional revenues or renewed economic prosperity. If out-migration were sustained for several years, the impact would grow over time.

To some, these figures may seem like a drop in the bucket relative to New York City’s $88 billion budget in fiscal year 2021. But amid a devastating pandemic and historic economic downturn, the city badly needs revenue. Indeed, the situation is so dire that Mayor Bill de Blasio is calling for emergency borrowing powers that were last utilized after the attacks of September 11, 2001.

Post-coronavirus, New York City’s leaders should emphasize growth—a Big Apple growing into a Bigger Apple, with a thriving economy, healthy finances, and increasing competitiveness. Whether through taxes paid or wealth created, this future will involve, but should by no means be exclusive to, those earning relatively high sums. Yet according to the Manhattan Institute’s July–August 2020 poll of six-figure earners in New York City, some 44% say that they have considered relocating outside the city in the past four months, with cost of living and crime cited as the biggest reasons.[66] The risk of out-migration may well be influenced by the decisions made by New York City’s leaders—whether work and life in the city will be made costlier and less safe, or whether the city’s cherished arts and dining scenes are to survive—all while remote work and cheaper locales beckon.

New York City has long emerged from crises stronger than ever. But the questions today are: When will New York City recover? And what might Gotham endure until that day? The answers, it seems, carry a hefty price tag.

Appendix: Estimates for High Earners Making $200,000 or More

The table below provides estimates of potential revenue losses under our three scenarios for the subset of high earners with $200,000 or more of adjusted gross income. The estimated losses are not markedly smaller than those for high earners with $100,000 or more of adjusted gross income because income-tax liability and business income are highly concentrated among taxpayers with very high income.

Endnotes

- Kevin Quealy, “The Richest Neighborhoods Emptied Out Most as Coronavirus Hit New York City,” New York Times, May 15, 2020.

- E. J. McMahon, “Testimony: FY2020 New York State Budget—Taxes,” Empire Center for Public Policy, Aug. 5, 2020.

- New York City Independent Budget Office (IBO), “About the Tables on New York City Residents’ Income and Tax Liability,” October 2020; NYC Office of Management and Budget (OMB), “Tax Revenue Forecasting Documentation,” May 2019.

- NYC Office of Management and Budget (OMB), Agency Budgets & Projections.

- Edward L. Glaeser, “Urban Colossus: Why Is New York America’s Largest City?” Economic Policy Review 11, no. 2 (December 2005): 7–24.

- Michael Hendrix, “Understanding Crowding and Covid-19,” City Journal, July 7, 2020.

- “Yellow Fever Epidemic (1795–1804),” NYCdata, Weissman Center for International Business, Baruch College /CUNY; Richard Plunz and Andrés Álvarez-Dávila, “Density, Equity, and the History of Epidemics in New York City,” State of the Planet (blog), June 30, 2020.

- Lorna Ebner, “Quarantine in Nineteenth-Century New York,” Books, Health, and History (blog), Apr. 14, 2020.

- Plunz and Álvarez-Dávila, “Density, Equity.” The relative rise in the death rates from those epidemics was not as large as modern epidemics because the normal death rate—i.e., without considering the effects of epidemics—was much higher then.

- David M. Cutler and Grant Miller, “The Role of Public Health Improvements in Health Advances: The 20th-Century United States,” NBER working paper no. 10511 (May 31, 2004).

- Edward L. Glaeser, “The Historic Vitality of Cities,” in Revitalizing American Cities, ed. Susan M. Wachter and Kimberly A. Zeuli (Philadelphia: University of Pennsylvania Press, 2014).

- Justin Fox, “Covid-19 Death Rates in New York City Are Likely to Top 1918 Flu,” Bloomberg, Aug. 24, 2020.

- An estimated 12,000–15,000 people left when the city’s population was about 50,000. James E. Cronin, ed., The Diary of Elihu Hubbard Smith (1771–1798) (Philadelphia: American Philosophical Society, 1973), cited in Bob Arnebeck, “Yellow Fever in New York City 1791–1799,” presentation at the 26th Conference on New York State History, June 9–11, 2005; C. E. Heaton, “Yellow Fever in New York City,” Bulletin of the Medical Library Association 34, no. 2 (April 1946): 67–78.

- An estimated 70,000 people left when the city’s population was 202,000. J. S. Chambers, The Conquest of Cholera: America’s Greatest Scourge (New York: Macmillan, 1938), 63, cited in Ebner, “Quarantine in Nineteenth-Century New York.” Population estimates based on Campbell Gibson and Kay Jung, “Historical Census Population Totals, 1790 to 1990 for Large Cities,” census bureau, February 2005. See also Anne Garner, “Cholera Comes to New York City,” Books, Health, and History (blog), Feb. 3, 2015.

- John Noble Wilford, “How Epidemics Helped Shape the Modern Metropolis,” New York Times, Apr. 15, 2008.

- Quoted in ibid.

- Current estimates of New York City’s population for July 2019, NYC Dept. of City Planning, Population Division.

- Justin Fox, “Talk of New York City Exodus to Suburbs Is Ahead of Reality,” Bloomberg, Sept. 2, 2020.

- Melissa Klein, “New Stats Reveal Massive NYC Exodus Amid Coronavirus, Crime,” New York Post, Nov. 14, 2020.

- See, e.g., Stanley J. Rolark, Alison Fields, and William Frey, “Migration Data from the U.S. Census Bureau,” U.S. Census Bureau, webinar presented Nov. 15, 2011; Alicia Modestino, “Voting with Their Feet? Local Economic Conditions and Migration Patterns in New England,” Federal Reserve Board of Boston, working paper no. 09-1, Aug. 7, 2012; Raven Molloy, Christopher L. Smith, and Abigail K. Wozniak, “Internal Migration in the United States,” Journal of Economic Perspectives 25, no. 3 (Summer 2011): 173–96.

- The years given are years in which tax returns are filed, not tax years. E.g., the 2018 filing year generally would include returns for the 2017 tax year (most of us file our returns in April of the next year). Thus, these data are not yet affected by the Tax Cuts and Jobs Act, which took effect in the 2018 tax year.

- Authors’ analysis of data available at https://www.irs.gov/statistics/soi-tax-stats-migration-data.

- These data are available by county; we aggregated the five counties (boroughs) of New York City to develop estimates for the city.

- McMahon, “FY2021 New York State Budget—Taxes.”

- Kevin Quealy, “The Richest Neighborhoods Emptied Out Most as Coronavirus Hit New York City,” New York Times, May 15, 2020.

- Joshua Coven, Arpit Gupta, and Iris Yao, “Urban Flight Seeded the COVID-19 Pandemic Across the United States,” SSRN, Oct. 14, 2020.

- Joshua Coven and Arpit Gupta, “Disparities in Mobility Responses to Covid-19,” working paper, May 15, 2020.

- Ibid., fig. III.

- Trash collection citywide in March was up 4.1%. However, it was down by 5% on the Lower East Side and down in several other Manhattan neighborhoods. But it was up in many parts of Queens and Staten Island. Gabriel Sandoval, Ann Choi, and Rosa Goldensohn, “Garbage Pickups Tell Tale of Two Cities as Manhattan Shrinks,” The City, Apr. 12, 2020.

- Michael Hendrix, “Taking the City’s Temperature: What New Yorkers Say About Crime, the Cost of Living, Schools, and Reform,” Manhattan Institute for Policy Research, Sept. 3, 2020.

- Michael Hendrix, “A Survey of New York City’s High-Income Earners: The Future of Work and the Quality of Life,” Manhattan Institute for Policy Research, Sept. 14, 2020.

- Andrew Perry, “Personal Income Tax Revenues in New York State and City,” Citizens Budget Commission, Aug. 13, 2019.

- Matt S. Clancy, “Remote Work’s Time Has Come,” City Journal, Spring 2020.

- Erik Brynjolfsson et al., “COVID-19 and Remote Work: An Early Look at US Data,” NBER working paper no. 27344, June 2020.

- Katherine Guyot and Isabel V. Sawhill, “Telecommuting Will Likely Continue Long After the Pandemic,” Brookings Institution (blog), Apr. 6, 2020.

- Alexander W. Bartik et al., “What Jobs Are Being Done at Home During the Covid-19 Crisis? Evidence from Firm-Level Surveys,” NBER working paper no. 27422, June 2020.

- Brynjolfsson et al., “COVID-19 and Remote Work.”

- Guyot and Sawhill, “Telecommuting Will Likely Continue.”

- Claire Cain Miller, “Is the Five-Day Office Week Over?” The Upshot (blog), New York Times, July 2, 2020.

- Anya Strzemien et al., “Out of Office: A Survey of Our New Work Lives,” New York Times, Aug. 20, 2020.

- Bartik et al., “What Jobs Are Being Done at Home?”

- Guyot and Sawhill, “Telecommuting Will Likely Continue.”

- Jonathan I. Dingel and Brent Neiman, “How Many Jobs Can Be Done at Home?” white paper, Becker Friedman Institute for Economics at University of Chicago, June 2020; Mark P. Mills, “Technology and the City: Working from Home Has Benefits, but the Downsides Are Real, Too,” City Journal, Sept. 2, 2020.

- Grant A. Driessen and Joseph S. Hughes, “The SALT Cap: Overview and Analysis,” Congressional Research Service, report no. R46246, Mar. 6, 2020.

- McMahon, “Testimony: FY2020 New York State Budget—Taxes.”

- Andrew Rein, “Practical Policy in Challenging Circumstances: How NYS and NYC Should Respond to the Tax Cuts and Jobs Act,” Citizens Budget Commission of New York, Mar. 18, 2018.

- Ibid.

- Cristobal Young et al., “Millionaire Migration and Taxation of the Elite: Evidence from Administrative Data,” American Sociological Review 81, no. 3 (June 2016): 421–46; see also James W. Wetzler, “Taxation of Millionaires in New York,” Tax Notes, Oct. 10, 2016, p. 7.

- Joshua D. Rauh and Ryan Shyu, “Behavioral Response to State Income Taxation of High Earners: Evidence from California,” SSRN, July 2020.

- Frank Sammartino and Kim Rueben, “Revisiting the State and Local Tax Deduction,” Tax Policy Center, Mar. 31, 2016.

- NYC IBO, “About the Tables on New York City Residents’ Income and Tax Liability,” October 2020.

- NYS Dept. of Taxation and Finance, “Income Tax Definitions.”

- This report does not constitute tax or legal advice.

- NYC OMB, “Tax Revenue Forecasting Documentation,” 89.

- NYC Dept. of Finance, Division of Tax Policy and Data Analytics, “Statistical Profiles of New York City Business Income Taxes: Tax Year 2016,” May 2020.

- NYC OMB, “Tax Revenue Forecasting Documentation,” 92–93.

- This is known as a single-factor receipts formula, which was phased in over 10 years, beginning in 2009. Previously, income was allocated using a three-factor formula that considered payroll, property, and receipts.

- Mark H. Levin, “New York City Makes Major Changes to the Unincorporated Business Tax,” CPA Journal 76, no. 4 (April 2006): 48.

- Richard Goldstein, “NYC Unincorporated Business Tax: Impact of Telecommuting on Allocation of Income from Taxable Services,” Berdon LLP, July 30, 2020. Under rules that were in place many years earlier, receipts were sourced to where the service was controlled rather than where it was performed. Under those earlier rules, the Hamptons receipts would be sourced to New York City if the service was controlled from New York City headquarters. See Levin, “New York City Makes Major Changes to the Unincorporated Business Tax”; Robert Frank, “The App That Traders Are Using to Avoid a New York City Tax During the Coronavirus Pandemic,” CNBC, July 15, 2020; Alan S. Kufeld, Sandy Weinberg, and Steven J. Eller, “Employees Telecommuting Due to COVID-19 Create Potential NYC Unincorporated Business Tax Savings Opportunity,” PKF O’Connor Davies, Aug. 6, 2020.

- Debra S. Herman and Elizabeth Pascal, “New York City Taxes: A Quick Primer for Businesses,” New York State Society of CPAs, Feb. 1, 2020. Exactly how the sourcing rules will be applied is subject to uncertainty; see Irwin M. Slomka, “New York City Retracts Policy Regarding Broker-Dealer Sourcing for Non-Registered Broker-Dealers,” International Law Office, Jan. 17, 2017.

- Goldstein, “NYC Unincorporated Business Tax.”

- We estimate that the business share of the sales tax is 42%, based upon Andrew Phillips and Muath Ibaid, “The Impact of Imposing Sales Taxes on Business Inputs,” prepared for the State Tax Research Institute and the Council on State Taxation, Ernst & Young LLP, May 2019. We estimate that tourists paid 80% of hotel taxable sales, 50% of arts and recreation, 24% of food and beverage service sales, and 18% of retail sales, based on our review of “Destination New York,” Center for an Urban Future, May 2018.

- Thus, the average income of those leaving is the same as the average income of the group overall, which was about $950,000 in 2017.

- We assume that there will be a smaller proportion of financial services newly allocated out of the city than of other professional services because registered broker-dealers are able to allocate services based on the location of the customer, and a substantial share of receipts in this industry might not be affected.

- We spoke with a tax practitioner who advises unincorporated business owners; this person believed that the out-allocation of business income in affected industries could be substantially greater than 15%. One real-estate analyst we spoke with believed that the out-migration of high earners is likely to be greater than we assume here.

- Hendrix, “A Survey of New York City’s High-Income Earners.”

Photo: tarabird / iStock Editorial / Getty Images Plus

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).