How to Lower Student Loan Defaults: Simplify Enrollment in Income-Driven Repayment Plans

Photo: Tero Vesalainen / iStock / Getty Images Plus

U.S. student debt now exceeds $1.6 trillion, and default rates are higher than for any other type of household debt. Yet even as many students struggle to make their monthly payments, few take advantage of a federal program that would make them more affordable. A variety of income-driven repayment (IDR) plans allow borrowers to pay a fixed percentage of their income, rather than a fixed amount, which reduces monthly payments.

Under an IDR plan, borrowers pay a fixed percentage of their income for a fixed number of years. If the full balance is not repaid by the end, the remaining balance is forgiven. Despite the advantages of IDR, fewer than 30% of all student borrowers were enrolled as of 2018.

The program is underutilized because the paper application process is unnecessarily complex—unlike, in countries such as the U.K. and Australia, where enrollment in IDR programs is automatic. In the U.S., one simple, low-cost policy change could boost enrollment and reduce student loan defaults: replace cumbersome paperwork with a streamlined, online application.

Introduction

U.S. student loan debt has reached a record high, exceeding $1.6 trillion, and shows no signs of slowing. Student borrowing is growing faster than inflation, and default rates for student loans are higher than those for any other type of household debt.[1] However, even as many students struggle to make their monthly payments, few take advantage of a federal program that would make them more affordable. Income-driven repayment (IDR) allows borrowers to pay a fixed percentage of their income, rather than a fixed amount, which reduces monthly payments and helps avoid default. The program is underutilized because policymakers have made it unnecessarily complex and difficult for students to enroll.

Under an IDR plan, borrowers pay a fixed percentage of their income for a fixed number of years. If the full balance is not repaid by the end, the remaining balance is forgiven.

Enrollment in IDR plans has increased in recent years, including a 55% jump among Direct Loan borrowers.[2] However, even with a notable increase in IDR enrollment since 2013, participation in these plans remains low, despite their generous benefits. As of 2018, fewer than 30% of all student borrowers were enrolled in this optional federal program.

So why do student borrowers, especially those who are eligible and would benefit from the program, fail to enroll in IDR? Because policymakers have made it too difficult. Borrowers must opt into IDR and complete onerous paperwork. In many countries, such as the U.K. and Australia, enrollment in IDR programs is automatic.

But one simple and low-cost policy change could boost enrollment in these plans and reduce the number of student loan defaults. Replacing the cumbersome paper-based application system with a streamlined electronic enrollment process would make it much easier for students to take advantage of IDR.

A Patchwork of Complex Choices

Traditional student loan repayment works much like fixed-rate mortgage repayment: borrowers make a fixed monthly payment for 10 years. Those with large balances can extend the student loan repayment period up to 30 years, based on a legislated schedule. Monthly payments do not fluctuate with income; but in some circumstances, payment can be delayed through deferment or forbearance. Deferment allows a delay of up to three years if the borrower is in school or experiences financial hardship from unemployment or underemployment. Military deferment allows unlimited payment delays. Forbearance allows reduced or zero payments for up to 12 months in cases of severe financial hardship, illness, or employment in certain areas of public service.

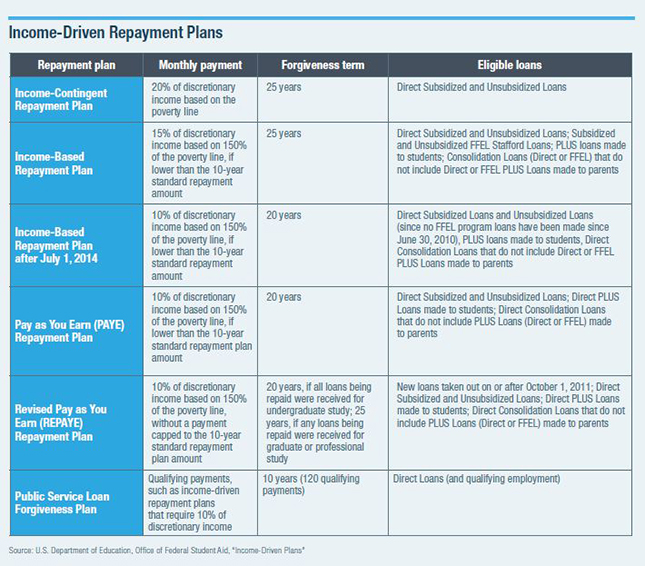

In 1993, the federal government introduced a new type of repayment contract when it rolled out the first income-driven repayment plan. Under this new plan, called Income Contingent Repayment (ICR), borrowers could pay 20% of their discretionary income each month and have remaining loan balances forgiven after 25 years. In 2007, Congress passed the College Cost Reduction and Access Act, and created the more generous Income-Based Repayment (IBR) plan. This plan allowed borrowers to pay 15% of their discretionary income each month. The IBR plan became available to student borrowers on July 1, 2009. In 2010, Congress further expanded the IBR plan, allowing borrowers to pay only 10% of their discretionary income each month, with remaining balances forgiven after 20 years. This more generous IBR plan took effect on July 1, 2014.

The Obama administration again expanded incomedriven repayment (IDR)plans by regulating the Pay as You Earn (PAYE) plan in 2012; and the Revised Pay as You Earn (REPAYE) plan in 2015. The Public Service Loan Forgiveness Program, created under the College Cost Reduction and Access Act of 2007, forgives Direct Loan balances after 10 years of qualified payments.

Income-Driven Repayment Plans

As shown in the table below, income-driven repayment for federal student loans is not one single program but a patchwork of complicated options. Indeed, the table highlights only some of the options available to students. Currently, the U.S. Department of Education offers 16 repayment plans, eight forgiveness programs, and 32 deferment and forbearance options. Each plan operates with its own guidelines and differs in important but nuanced ways.[3]

Overwhelmed by complicated information and complex choices, borrowers might go with the simplest option instead of one that is financially optimal. Or, paralyzed by an overload of information and choices, borrowers may do nothing at all and implicitly “choose” the standard 10-year, mortgage-style repayment plan. The myriad choices available make deliberation about enrollment a demanding financial decision. It is unlikely that borrowers in financial distress will be in a strong position to sort out the plans’ fine details.[4] The complexity likely harms the very students whom IDR seeks to benefit.

The application process for IDR can be just as daunting as sorting through all the options. Generally, borrowers can enroll in an IDR plan at any point in the repayment process. But to do so, they need to submit a 10-page application in paper form or online. They must verify their income with a tax return, pay stub, or certification of zero income, or authorize the Internal Revenue Service to share their tax return with their loan servicer—and repeat the process every year. Otherwise, they’ll have to start paying a fixed amortized amount—for example, to the standard 10-year plan—until they recertify their income or enroll in another IDR plan. And while a borrower’s monthly payment can be adjusted more often than once a year, doing so requires the borrower to submit proof of income each time. This complexity most likely leads to lower application rates among eligible borrowers.[5]

Advising Borrowers on IDR

Borrowers who choose to enroll in an IDR plan must apply through their loan servicer, a contractor for the U.S. Department of Education. Loan servicers initiate the loan payment process when a student enters repayment (generally six months after the student leaves school) and facilitate the processing of monthly payments over the lifetime of the loan. Servicers also support delinquent borrowers and provide counsel on available options. Unlike most repayment options, IDR enrollment cannot be finalized through borrowers’ accounts with their loan servicers. Instead, they must complete an online application on the Department of Education website or submit a paper copy.

As soon as a borrower falls behind on loan payments, the loan servicer contacts the borrower to discuss options, including IDR. Even prior to that, borrowers receive information about IDR, both in monthly statements and in communication before repayment begins. However, findings from the loan servicer Navient suggested that nine out of 10 borrowers who defaulted on their loans never responded to an outreach call by an agent.

Experiment: Introducing a Streamlined Electronic Process

Streamlining the application process would make it significantly more likely that students enroll in IDR, as an experiment with the loan servicer Navient demonstrates.[6] It compared borrowers who enrolled via a streamlined electronic process with those who enrolled via the current method. FFEL[7] borrowers were randomly assigned to each group. Borrowers in the treatment group were presented an electronic application that was pre-populated with salary and family information gathered by loan service agents over the phone. The only step required to complete the application was to provide an electronic signature using Adobe E-sign, which could be done on a smartphone, tablet, or computer. Indeed, borrowers could sign the application while on the phone with the agent, reducing the number of necessary follow-up steps. The new procedure also facilitated the application process for married borrowers by offering them jointly pre-populated applications. The study assumed that, in the absence of E-sign, both the control and treatment groups would enroll in IDR at similar rates after receiving only a phone call. This follows naturally from the fact that agents were randomly assigned to borrowers and only specific agents were authorized by Navient to offer the option of Adobe E-sign.

There were, on average, 28 previous contact attempts before a delinquent borrower enrolled in income-driven repayment. Only 27% of prequalified borrowers returned their applications using the standard paper forms, which require borrowers to complete 10 pages of personal income and family information. When surveyed on the reasons that they did not return their applications, a notable percentage of borrowers referred to the complexity of the application and the effort required to print, sign, and mail it.

Results: E-Sign Doubles Application Rate

Loan service agents began contacting students in both the treatment and control groups by phone to inform them about IDR plans. In March, there were similar levels of participation among both groups. In June and July of 2017, those in the treatment group received the streamlined electronic application. By August, enrollment rates for those who received the online application had significantly increased. More than 60% of those in the treatment group were enrolled by August, compared with only 24% in the control group.

Approximately 70% of borrowers returned the prefilled and signed electronic application to their loan servicer—and two out of three of those borrowers ultimately enrolled in IDR. The remaining 5% were deemed ineligible. These numbers contrast sharply with the approximately 25% of prequalified borrowers from the control group who returned their 10-page application. The results demonstrate a large and immediate effect on borrower enrollment in IDR when a prefilled electronic application form is presented as an option.

Perhaps even more significant than the simple boost in enrollment is the effect on average monthly payments and delinquency. Those who enrolled saw monthly payments drop by $355, on average, and had a 7% reduction in delinquency.

Simplifying the application process by offering a pre-populated electronic application with Adobe E-sign has the potential to substantially increase enrollment in IDR plans. And this can be done without changing any other parameter of IDR. This finding reinforces feedback from prequalified borrowers who cited the complex, time-consuming process as a major deterrent. This experiment shows that when these impediments are removed, enrollment in IDR is likely to increase—and quite substantially.[8]

Conclusion

What does this mean for policymakers? Most notably, complexity is a serious issue for students who are navigating the landscape of student loan repayment. But this complexity can be addressed, in part, with a relatively easy solution. Simply making the application process less onerous is a low-cost way to increase participation in this federal program, if this is desired by policymakers.

That said, the extent to which policymakers ought to desire increased use of IDR plans remains unanswered. It is possible that the expanded use of IDR will cost taxpayers money. The budgetary effects of IDR plans are not obvious, as there are two countervailing effects: on the one hand, borrowers are typically making smaller payments; on the other hand, maturity is extended, and borrowers are repaying over a longer period of time. If we accept GAO estimates, the federal government will lose approximately 25 cents on every dollar of balances enrolled in IDR.

In many cases, the benefits of IDR for borrowers outweigh the costs. But these costs warrant attention. Interest accrues while a borrower is enrolled in an IDR plan, and it might be capitalized, according to the specific terms of each repayment plan. Participation in IDR is likely to result in longer repayment periods and a higher total repayment amount. These issues warrant further investigation.

The complexity of IDR is a significant obstacle to enrollment, but it can be overcome. If policymakers determine that the current participation rates in IDR are suboptimal, these findings offer powerful evidence in favor of an effective and extremely low-cost way to achieve increased participation. Simplifying paperwork to streamline enrollment in IDR might be effective. But policymakers need to ascertain whether this approach serves the overarching goal of optimal student credit arrangements: to ensure that investing in higher education pays off without strapping students as well as taxpayers with burdensome debt.

Acknowledgements

We are grateful to Beth Akers and participants at the Manhattan Institute’s “Reimagining Higher Education Finance: Solutions Beyond the Beltway” working group.

Endnotes

About the Authors

Katerina Nikalexi is an analyst at the Fiscal Policies Division of the European Central Bank. Previously, she worked at the University of Chicago Booth School of Business as a research professional, where her work focused on public finance and human capital. She holds an undergraduate degree in philosophy, politics, and economics and a master’s degree in economics from University College London.

Constantine Yannelis joined Chicago Booth as an Assistant Professor of Finance in 2018. He conducts research in finance and applied microeconomics. His research focuses on household finance, public finance, human capital and student loans. His recent research primarily explores repayment, information asymmetries and strategic behavior in the student loan market. Yannelis’ academic research has been featured in the Wall Street Journal, Financial Times, New York Times, Washington Post, The Economist, Bloomberg, Forbes and other media outlets and has been published in leading academic journals. Before joining Booth, Yannelis was an assistant professor of finance at New York University Stern School of Business. Prior to his time at NYU Stern, he worked at the United States Department of the Treasury, the Organization for Economic Cooperation and Development, the United Nations and the Federal Reserve Bank of Chicago as an associate economist. Yannelis earned a BA in economics and history from the University of Illinois at Urbana-Champaign and an MA in applied mathematics from Université de Paris I: Panthéon-Sorbonne. He holds a PhD in economics from Stanford University.

This report was written as a part of MI's Solutions from Beyond the Beltway series

Photo: Tero Vesalainen / iStock / Getty Images Plus

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).