Enhancing Medicare Advantage

Photo: Wavebreakmedia Ltd / Wavebreak Media / Getty Images Plus

Medicare funds health-care services for 60 million elderly and disabled Americans. Of these, 39 million receive coverage through a plan known as “Traditional Medicare” or “Medicare Fee-for-Service” (MFFS) that the federal government administers directly. Increasing numbers—21 million in 2019—enroll in Medicare Advantage (MA), choosing Medicare coverage from competing plans managed by private insurers.

Medicare’s Fee-for-Service payment system has hampered appropriate coordination of care and inflated costs by paying separately for each medical procedure or service delivered to beneficiaries, regardless of their value. As every detail of its operation is highly politicized and hard to reform, MFFS has an outdated benefit structure that leaves elderly and disabled enrollees exposed to potentially catastrophic out-of-pocket costs.

By contrast, MA plans have broad flexibility to upgrade operations. They are able to reduce costs and improve medical outcomes by making better use of primary care, negotiating discounts with preferred networks of providers, and managing chronic conditions to avoid expensive hospitalizations. This allows them to attract enrollees by reducing out-of-pocket costs and enhancing benefits.

Nevertheless, thanks to a few poorly designed rules, MA plans are currently operating below their full potential. This paper suggests potentially bipartisan reforms that could enhance the quality of MA plans for beneficiaries, while getting better value for taxpayers.

- MA covers the same health-care services as traditional Medicare, but at lower cost.

- By paying health-care plans in advance, MA provides an incentive for them to develop innovative care arrangements that keep beneficiaries healthy.

- The rules under which MA plans operate can be restructured so that more of the efficiency gains can be passed on to beneficiaries.

Introduction

Medicare began in 1965 as a federal entitlement to a comprehensive range of hospital and physician services for eligible beneficiaries. By 2017, 58.4 million elderly and disabled Americans were enrolled and federal spending on the program had grown to $710 billion from $8 billion in 1970—a 14-fold increase, after adjusting for inflation.[1] The Congressional Budget Office (CBO) estimates that over the next three decades, the cost of Medicare to federal taxpayers will increase from 3.5% to 6.8% of GDP. In the process, Medicare’s expense will surpass Social Security (which is expected to grow from 4.9% to 6.3% of GDP), making it the largest item on the federal budget—and the program most responsible for increasing the national debt from 78% to 152% of GDP.[2]

Although the retirement of the baby-boom generation contributes to this escalating cost, the main reason for it is structural: fee-for-service reimbursement provides an open-ended entitlement to whatever medical services are developed and delivered to beneficiaries, regardless of their quality or cost-effectiveness. This has led to constant inflation in the expense of the program, driving up health-care costs for those not even enrolled in Medicare—a problem that generations of reform attempts have failed to remedy.[3]

In practice, there remains little scrutiny of the adequacy or effectiveness of reimbursement claims made, and little incentive for physicians to be sparing in their use of diagnostic tests, office visits, and expensive procedures. Politicians like to boast that MFFS has low administrative costs by comparison with private health insurance, but this has engendered the costlier problem of fraudulent claims or improper payments. Private insurers usually review the merits of medical claims before and after payment; MFFS verifies the legitimacy of less than 0.3% of nearly 1.5 billion payments made by the program.[4] The U.S. Department of Health and Human Services has estimated that 8.1% of claims reimbursed by the Medicare program in 2018—$31.[6] billion—ought not to have been paid.[5] While some of these claims may have been legitimate, though improperly documented, many were not.

Medicare sets tens of thousands of prices for the services it covers. The program incurs new costs when expensive new drugs, devices, and surgical procedures become available, but reimbursement rates are rarely trimmed when new technologies reduce the time and expense needed to treat patients—so taxpayers enjoy few savings from innovation.[6] Thanks to fierce lobbying, Congress legislated 17 times between 1997 and 2015 to override scheduled cuts to physician fees, and 91% of hospitals receive add-ons to its standard payments rates or are exempt from them entirely.[7]

With every aspect of Medicare deeply politicized, many elements of MFFS remain frozen in time—reflecting idiosyncratic features and inefficiencies of health-insurance arrangements from the 1960s. For example, the program is poorly designed to compensate innovative care-coordination services that prevent hospitalizations and save money but do not fit neatly into existing payment silos. Open-network fee-for-service arrangements mean that new billing opportunities are likely to add to existing costs, rather than to reduce them. Congress is therefore reluctant to expand the delivery of care by telehealth (which could save money and time) because of concerns that it will increase costs by making it harder to police inappropriate claims.

Patients in the traditional Medicare program pay a $1,340 deductible for each continuous stay in a hospital under Part A and, for Part B, a separate $183 deductible, plus 20% coinsurance—without any cap for physician services and outpatient procedures. Given the cost of cutting-edge therapies (12 of 13 new cancer drugs approved in 2012 cost above $100,000), these patients may be liable for potentially ruinous out-of-pocket costs.[8]

Such out-of-pocket costs are experienced as an arbitrary and unpleasant surprise and do little to discourage overuse or encourage beneficiaries to shop for cost-effective care. If anything, they are upside-down insurance—protecting those enrolled from routine costs, while leaving them exposed to catastrophic expenditures.[9] As a result, most MFFS beneficiaries have some form of supplemental coverage to be well insured.

Most of these flaws and shortcomings have been widely known for decades, but the voting clout of seniors and the concern they have for easy access to care make it easy for lobbyists for provider interests to scare politicians away from even incidentally threatening their incomes by challenging needless costs inherent in the status quo.[10]

The Objectives of Medicare Advantage

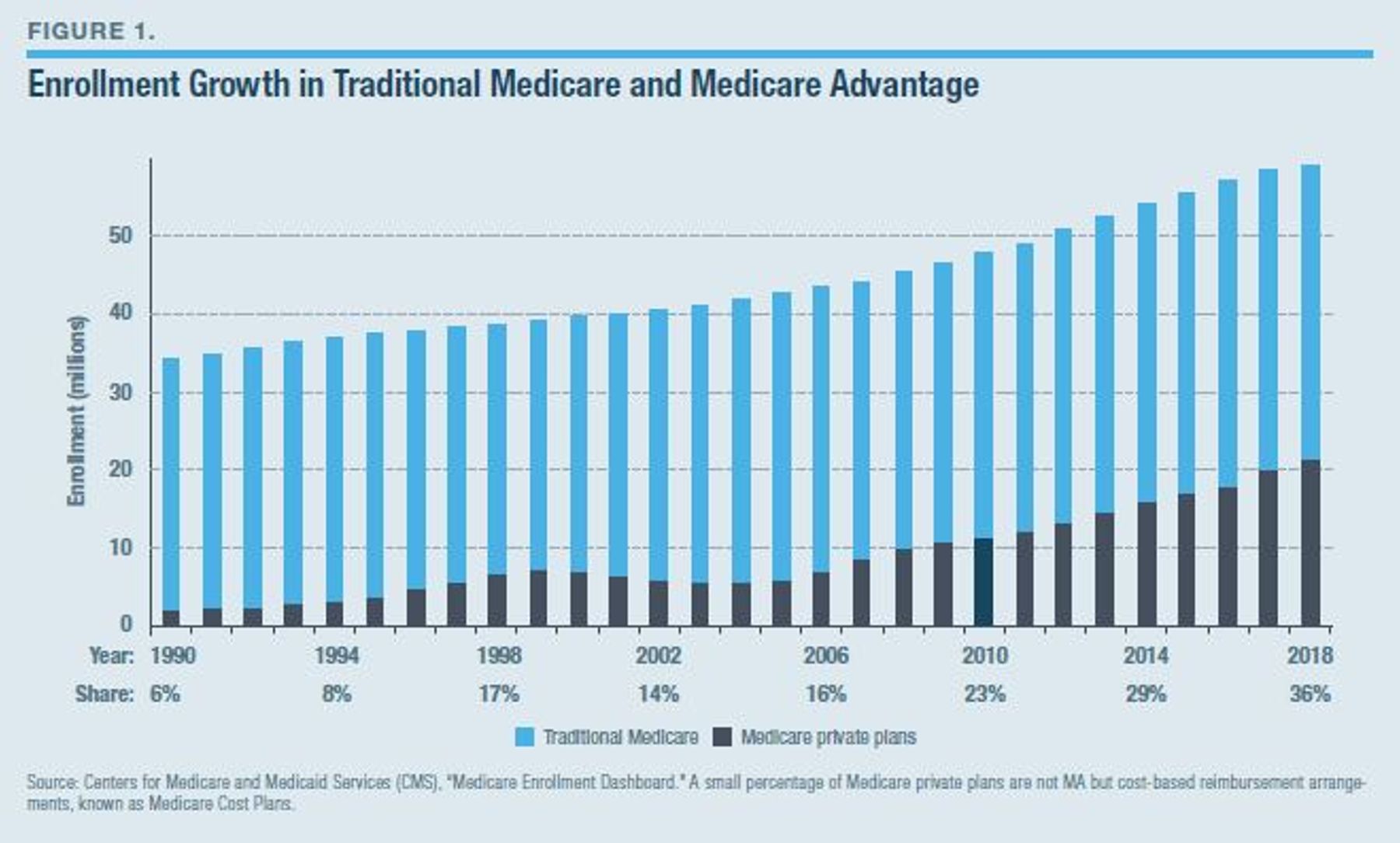

The most promising alternative to the escalating costs and fragmented delivery of care associated with the direct purchasing of care by the federal government is Medicare Advantage (MA)—government-funded but privately managed health-care insurance plans.[11] MA was initially established as Medicare Part C by the Tax Equity and Fiscal Responsibility Act of 1982, which sought to open Medicare to HMOs.[12] Enrollment grew slowly until the Balanced Budget Act of 1997, which allowed MA plans built on the PPO model (looser networks of preferred providers) to participate. Since the Medicare Modernization Act of 2003, the number and share of Medicare beneficiaries enrolled in MA plans has increased steadily (Figure 1).[13]

In 2018, 36% of Medicare beneficiaries were enrolled in private plans, with the proportion ranging from 1% in Alaska to 59% in Minnesota.[14] Some analysts expect that a majority nationwide will be enrolled in MA within a decade.[15]

Medicare gives insurers a single bundled payment based on each enrollee’s expected medical costs under MFFS. In return for this and the enrollee’s Part B premiums, MA plans must provide beneficiaries with Medicare’s full spectrum of Part A (hospital) and Part B (medical insurance) benefits—paying for at least the 76% share of medical costs that MFFS covers.

Within this framework, MA plans have great discretion in structuring their benefits and procuring covered medical services to deliver timely care in the most cost-effective way. They can establish networks, limit access to costlier providers, and review claims to eliminate needless costs. They can alter cost-sharing so that enrollees are deterred from using low-value services, while protecting them from catastrophic medical expenses that MFFS does not. Plans have the freedom to restructure payments to physicians to discourage unnecessary diagnostic tests and referrals. But they may also fund additional care-coordination services (such as assisting patients to manage their medications or their transitions from hospital to home care) that save money by avoiding costly hospitalizations and readmissions.

MA plans can offer a variety of additional benefits. Some use the savings generated by their greater efficiency to reduce premiums, deductibles, or coinsurance. Many plans will pay for dental and eye care, or for hearing aids. Most MA plans include drug coverage (Medicare Part D) with a zero premium. Plans may also reduce the cost-sharing provisions in MFFS.

Proposals to address Medicare’s solvency by shifting the program to a “premium support” arrangement are unlikely to be politically feasible to the extent that they would force people out of existing plan arrangements or cut benefit commitments that they already enjoy through MFFS.[16] But the shift of Medicare beneficiaries into MA potentially makes it far easier to define and adhere to a deliberate spending growth rate over the long term, as MA plans operate on a defined-contribution basis. That would effectively realize the objectives of premium support—but through beneficiaries gladly embracing better benefits, rather than the impossible struggle of forcing them to relinquish existing ones.

The Advantages of Medicare Advantage

Cost-effective medicine

To compare the cost and quality of MA with MFFS, it is necessary to adjust for differences in the relative health of enrollees in each option. The medical costs of MA enrollees are 25% lower than those of MFFS enrollees in the same county with the same medical risk score—and are still 10% lower than MFFS levels after using disparities in mortality to control for unobserved differences in health status (a method that would underestimate the savings if MA reduces mortality).[17] Individuals who switch from MFFS to MA also had racked up lower costs—with reductions concentrated in Part A inpatient spending.[18]

Strict regulations stipulate the minimum number of physicians and hospitals in each local area that MA plans must include in their networks. But plans can use the requirement that Medicare-participating hospitals accept payment at MFFS rates for out-of-network care to negotiate affordable rates at most facilities. Physicians, including those providing emergency services, are similarly constrained in their ability to charge more than Medicare rates to out-of-network MA patients: MA plans pay physicians, on average, 3% less than MFFS for equivalent procedures.[19] They are able to get even better rates at their in-network facilities: MA carriers paid 8% less per equivalent hospital admission than MFFS—even though those admitted were likely to be relatively sicker, given that MA plans try to keep healthier patients out of the hospital.[20]

Although MA plan premiums are little correlated with the breadth of their hospital networks, the mean beneficiary premium for MA plans with narrow physician networks (those with fewer than 30% of MFFS-participating physicians) was $60 per month lower than that for broad-network MA plans (those including over 70% of MFFS-participating physicians).[21] MA plans also have the flexibility to correct inefficiencies in MFFS: the commercial rates at which MA plans purchased durable medical equipment and diagnostic tests were around 30% lower than MFFS.[22]

Avoiding hospitalizations

Savings in the cost of delivering care under MA largely result from constraints that a plan puts on patients using high-cost services and by directing patients toward cheaper sources of care. MA patients with equivalent medical needs make 22% fewer visits to specialists, but only 3% fewer visits to primary-care physicians. MA enrollees are 7% less likely to undergo surgery on an inpatient basis and 25% more likely to receive outpatient surgery.[23] Seniors who choose MA HMOs (65% of all MA enrollees) are 60% less likely to be hospitalized, have hospital stays that are 44% shorter, but are 14% more likely to see a physician at least once during the year after controlling for differences in medical risks.[24]

According to one study, seniors forced to quit MA and return to traditional Medicare when their plans exited local markets experienced a 60% increase in hospital utilization (an increase of 27% for emergency care and 151% for elective care). They had longer lengths of stay and received more medical procedures but tended to be treated closer to home at hospitals of slightly lower Medicare quality ratings. The study found that much of this effect was instantaneous, but that its magnitude grows over six months. This suggests indirect effects (possibly from getting accustomed to using closer hospitals, visiting the ER rather than a primary care doctor, and seeking procedures without waiting for prior authorization) that persisted over time.[25]

Compared with MFFS patients, MA patients matched by geographic location and demographics, and adjusted by disparities in health status, had 20%–25% fewer inpatient hospitalizations and made 25%–35% fewer emergency-care visits. Although there was less disparity in the use of ambulatory procedures, MA HMO patients were more likely to be treated in primary-care settings than by costlier specialist physicians. Heart patients enrolled in such MA plans were more likely than those in MFFS to receive coronary bypass surgery than percutaneous coronary intervention—reducing the risk of requiring a repeat procedure.[26]

The readmission of patients within 30 days of a hospital stay cost Medicare $24 billion in 2011—11% of its total spending on hospital care.[27] While hospitals treating traditional Medicare patients stand to receive more revenue when their patients are readmitted, those treating MA patients may risk being left out of networks if they fail to pay appropriate attention to reducing readmissions. Indeed, MA patients with equivalent diagnoses had 30-day readmission rates that were 13%–20% lower than those of traditional Medicare patients.[28]

Managing chronic conditions

While 21% of Medicare beneficiaries have five or more chronic conditions, they account for 58% of the program’s spending.[29] As most individuals tend to remain enrolled in the same MA plans from year to year, insurers know that they are likely to be responsible for their medical costs as they develop major illnesses in subsequent years, and therefore have an incentive to invest in preventive care.[30]

Enrollees of MA HMOs at risk of breast cancer, diabetes, and cardiovascular disease were consistently 5%–20% more likely than traditional Medicare patients to receive appropriate tests.[31] Medicare enrollees in privately managed care plans were also 22% more likely than those in traditional Medicare to receive flu shots and pneumococcal vaccinations.[32] Disabled Medicare beneficiaries enrolled in MA with breast cancer were diagnosed earlier and had higher survival rates than traditional Medicare, but there was no similar relationship between benefit choice and outcomes for lung cancer.[33]

Clinical risk factors alone would predict MA patients to be 14% less likely than MFFS patients to die in any particular year, but the mortality rate of MA enrollees is actually 33% less. This suggests that MA’s lower mortality rate may be due more to improved care than simply to having healthier patients enrolled. The disparity increased with the intensity of managed care, being greatest for HMOs but weakest for MA fee-for-service plans.[34] Using a disparity in payments to plans to identify the impact of enrollment in MA (plans serving metropolitan statistical areas with populations above 250,000 receive higher subsidies, which allows them to be sold on more attractive terms), one study found areas just above the higher payment cutoff that have higher MA enrollment, lower hospital use, and lower mortality.[35]

MA plans generate the most savings on diseases amenable to management by primary care, such as diabetes, chronic heart failure, or COPD, which allows them to cut out needless consultations with expensive specialists.[36] Diabetics enrolled in an MA Special Needs Plan that does preventive house calls, medication assistance, and care transition coordination visited physicians 7% more than MFFS patients with similar risk levels, but spent 19% fewer days in hospital.[37]

In 2014, MFFS spent $59 billion on post-acute care—about 10% of its total spending. MA patients discharged from the same hospitals with equivalent conditions received less costly post-acute care but had better medical outcomes: they had lower rates of hospital readmission and were more likely to be able to return to their own homes. As a result, post-acute care costs after joint replacements, strokes, and heart failure were 16% lower for MA patients.[38]

Because they are paid lump sums to cover enrollees, MA plans have no incentive to inflate the number of costly medical procedures that fail to improve the quality of life for the terminally ill. Medicare beneficiaries were 43% less likely to die in a hospital (an expensive and unwanted setting) rather than elsewhere (such as home, long-term care, or hospice) if they were continuously enrolled in MA rather than in traditional Medicare.[39] In their last six months of life, beneficiaries were 15%–31% percent more likely to use hospice if they were enrolled in MA HMOs, 11%–13% less likely to be admitted to hospital, and 42%–54% less likely to use emergency-department services, than comparable traditional Medicare patients in the same local area. They had similar levels of outpatient visits.[40]

Spillover benefits

MA plans’ scrutiny of expensive therapies has had a spillover impact on the rest of health care by altering practice styles and the cost-effectiveness of care delivery. An increase in payments to MA plans causing an increase in MA penetration from 35% to 40% is associated with a reduction of overall hospital costs by 2%—including for individuals remaining in MFFS and those outside of Medicare altogether. Spillover effects consist of reduced costs per admission and average lengths of stay but no difference in the overall number of hospitalizations.[41]

A one-percentage-point increase in the share of Medicare beneficiaries enrolled in MA was associated with a 1.7% reduction in MFFS spending—driven by reduced inpatient stays, fewer imaging events, and reduced post-acute care.[42] Costs were reduced the most by the growth of MA in counties where the base level of MA penetration was highest.[43]

Returning savings to enrollees

MA plans can use savings generated in delivering standard Part A and Part B services to attract enrollees (and help them achieve better health) by reducing their costs or expanding their benefits.

As adherence to prescribed courses of medications helps avoid expensive hospitalizations, the most common way for them to do this is by reducing beneficiaries’ costs associated with the Part D prescription drug benefit, whose premiums paid by traditional Medicare enrollees averaged $492 per year in 2018.[44]

Across the country, 84% of Medicare beneficiaries have access to an MA plan including prescription drug coverage without any such premium at all—and the majority of MA beneficiaries enroll in these zero-premium plans.[45] Annual deductibles for Part D are also substantially lower: averaging $131 for those in MA rather than $400 for those in MFFS.[46] MA enrollees pay an average of 5%–7% less out-of-pocket for identical drugs than do traditional Medicare patients purchasing Part D. The largest differences were concentrated among drugs to treat chronic conditions like asthma, diabetes, and high cholesterol.[47] The most innovative MA plans incorporate clinical nuance to eliminate cost-sharing altogether for medications that are most important to managing chronic conditions.[48]

MA plans incorporate other cost-saving features for patients. There is no limit on total out-of-pocket expenditures for those in MFFS. MA plans must limit enrollees’ out-of-pocket costs to no more than $6,700 per year, and on average they limit them to $5,219.[49]

MA plans can also use the savings they generate to provide benefits that are not available to MFFS patients. Thus 77% of MA beneficiaries are in plans that cover eye exams, 58% receive some dental coverage, and 46% have coverage of hearing aids. Many plans also provide access to 24-hour nursing hotlines, telemonitoring, and nonemergency transportation.[50] Recent bipartisan legislation has made it easier for MA plans to offer additional nonmedical benefits tailored to the broader needs of specific beneficiaries with chronic conditions like diabetes, Alzheimer’s, Parkinson’s disease, heart failure, arthritis, and cancer.[51]

MA and the future of Medicare

By giving plans the responsibility for controlling aggregate medical costs, MA establishes a structure that can help to ensure Medicare’s long-term solvency. MA plans can tighten networks, reform payments to providers, increase cost-sharing, or adjust premiums automatically in response to rising costs. As particular hospital or physician costs increase, plans can substitute cheaper alternative care-delivery arrangements. Between 2009 and 2017, after the Affordable Care Act had reduced payments to MA plans by 12%, MA plans managed to absorb the hit while raising average monthly premiums by only $8.[52]

This contrasts starkly with failed attempts to trim MFFS costs. In 1997, Congress established a Sustainable Growth Rate limit for spending on physician services, but within five years enacted bipartisan legislation to override the mechanism that was supposed to constrain costs, even though this would have reduced spending by only 5%.[53] After overriding SGR cuts 16 more times, Congress in 2015 repealed the SGR mechanism altogether—increasing the projected cost of Medicare by $175 billion over the following decade.[54]

Any sweeping “premium support” reform to make Medicare fiscally sustainable with a single legislative enactment is unlikely to be politically feasible, nor is it necessary.[55] Rather than battling fruitlessly to turn Medicare’s open-ended entitlement into one that functions on a budget, by cutting payment rates and benefits, policymakers should instead encourage beneficiaries to move to MA, where they would immediately share in the benefits from more cost-effective plan arrangements.

Proposed Reforms

Since MA plans can improve medical care, reduce costs to patients and the government, and offer benefits unavailable under MFFS, why haven’t more Medicare beneficiaries chosen to enroll in them?

Aside from inertia, it is because various regulations have hobbled their competitiveness and impeded them from returning savings to enrollees. Several specific reforms could therefore enhance MA, so that more beneficiaries could enjoy its reduced costs and greater quality of care.

- Eliminate the “tax” on MA rebates

The structure of rebates to plans means that the efficiency benefits of MA are not being fully passed on to enrollees.

Every year, CMS sets a payment benchmark for every MA plan based primarily on the level of traditional Medicare spending in that local area.[56] Insurers must submit bids of what they expect it will cost to deliver the standard Medicare benefit package to an enrollee of average risk. Expenses associated with the standard Part A or B benefits, including reasonable profits and advertising, can be included in the bid.

If this bid is equal to the benchmark, the plan receives that amount per enrollee, adjusted by his or her expected medical needs. If the bid is greater than the benchmark, the plan must charge enrollees a supplemental premium to make up the difference. If the bid is below the benchmark, plans can receive 50%–70% of the difference as “rebates,” with the proportion depending on a variety of regulatory performance metrics.[57] They can use these rebates to attract enrollees by further reducing their out-of-pocket costs or providing supplemental benefits.

Implicitly, this payment structure imposes a 30%–50% tax on rebates to be gained from bidding below the benchmark. Below the benchmark, plans can claim $1 for every $1 they associate with Part A or B benefits, but only $0.50–$0.70 for every $1 they spend on reducing out-of-pocket costs or supplemental benefits. As a result, plans have been deterred from reducing the “cost” of the standard Part A and B benefit, in order to increase rebates and the associated benefits for enrollees.

Indeed, as a result of these incentives, MA plans are failing to pass through the full value of the benchmark to enrollees as supplemental benefits.

A study using variation in the rebasing of plan payment benchmarks from 2007 to 2009 found only 49% of increases in payments to plans being passed through to enrollees in extra benefits or reduced cost-sharing.[58] Using the disparity in payments to MA plans serving metro areas, a study of legislation from 2000 found 45% of increased payments serving to reduce premiums and 9% going to increased benefits.[59] A third study of a payment change from 2007 to 2011 found that only an eighth of payment increases were passed through to beneficiaries, with substantially more spending on advertising and higher profits being enjoyed by plans in areas with higher payments.[60] A fourth study, examining variation in benchmark increases between plans, found a pass-through rate of 39%, with rebates primarily being used to reduce supplemental premiums, except for zero-premium plans, in which case they tended to be used to expand supplemental benefits.[61]

Whereas efficiency gains can be used to directly reduce any supplemental premiums for plans that bid above the benchmark, below the benchmark any savings returned to beneficiaries as reductions to Medicare Part B premiums would be subject to the implicit 30%–50% tax. It ought therefore to be no surprise that for every $1 in payment increases to plans, those bidding above the benchmark passed through $0.70 more to beneficiaries than those at the benchmark.[62]

In counties with more than 10 beneficiaries enrolled in MA, an average of four insurers are offering plans. Pass-through rates increase from 13% in the least competitive markets to 74% in the markets with the most competing insurers—suggesting that the disincentive to avoid bidding below the benchmark is overcome in the more competitive markets.[63] Immediately above the payment bump for metro areas, which encourages more individuals to enroll in MA, there are 1.8 more insurers offering plans.[64] (This also demonstrates the weakness of MFFS as an appealing alternative to MA and as a competitive discipline on the plans within it.)

The disincentive to increase efficiency and pass on the savings to attract enrollees can easily be remedied by reforming payments to MA plans from a complex bidding structure to a system by which they are simply paid the benchmark as a lump sum and allowed to pass on all efficiency savings to enrollees. This would effectively remove the tax on rebates and could be funded by legislation that is budget-neutral through a proportionate reduction of the benchmark (Figure 2).[65]

The disincentive to increase efficiency and pass on the savings to attract enrollees can easily be remedied by reforming payments to MA plans from a complex bidding structure to a system by which they are simply paid the benchmark as a lump sum and allowed to pass on all efficiency savings to enrollees. This would effectively remove the tax on rebates and could be funded by legislation that is budget-neutral through a proportionate reduction of the benchmark (Figure 2).[65]

Beneficiaries would see immediate gains from such a reform, in terms of reduced out-of-pocket costs and increased availability of dental benefits. Such a reform would also help depoliticize and reduce uncertainty surrounding MA benchmarks and clarify the relative subsidies provided to various MA plans relative to MFFS. It may establish a virtuous cycle, whereby more benefits passed through to MA enrollees attracts more competing insurers into the market, which, in turn, increases the share of benefits passed through and the number of beneficiaries enrolling in MA.

- Establish a baseline MA provider contract

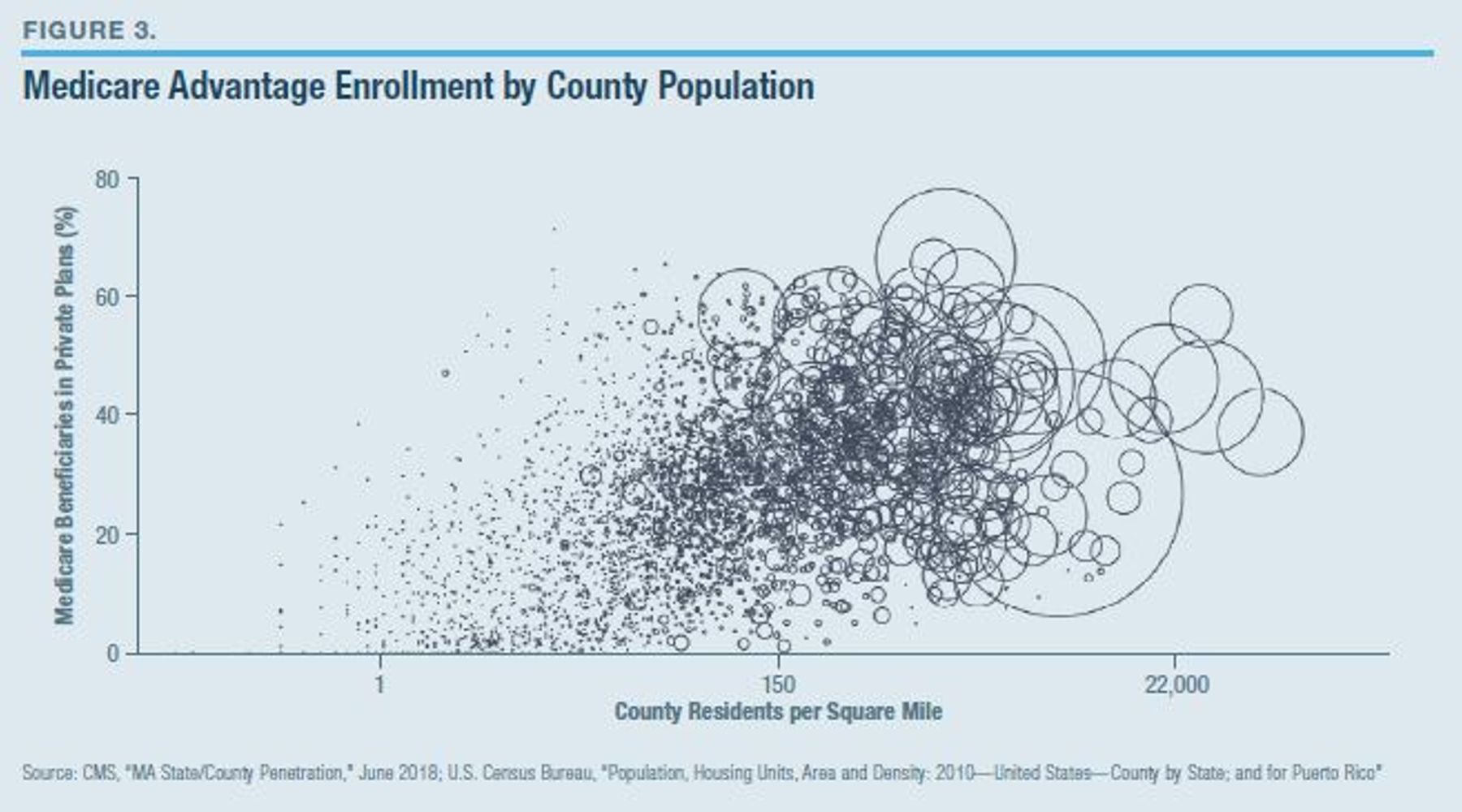

Enrollment in MA is significantly higher in urban than rural areas (Figure 3). In 2017, while the absence of insurers from the exchange in seven counties across the U.S. made headline news, MA plans were unavailable in 147 counties—even though total insurer revenues from MA are twice as great as those from the individual market.[66]

While MA plans in urban areas receive higher benchmark payments, it has also traditionally been easier for HMOs to form networks and gain acceptance of managed-care methods in areas where there are larger numbers of potential providers. In rural areas, by contrast, MA plans are often unable to persuade providers to accept their reimbursement rates and terms.

In 1997, to protect rural hospitals from insolvency, Congress designated a third of Medicare participating hospitals as Critical Access Hospitals, exempting them from the program’s standard fee schedules and reimbursing them according to whatever costs they incur. This is designed to be a very lucrative arrangement for rural hospitals, which cater to populations with low rates of employer-sponsored insurance and make Medicare revenues their main cash cow.

In rural counties where few Medicare beneficiaries are yet enrolled in MA, Critical Access Hospitals have little incentive to offer generous contract terms to MA plans that would try to reduce spending on hospital admissions.[67] MA plans can therefore find it difficult to gain a foothold in states dominated by these facilities. And so 44% of Medicare beneficiaries in Rhode Island are in MA plans while only 4% of those in Wyoming and 1% in Alaska are enrolled.[68]

CMS requires MA plans to contract with hospital and physician networks such that 90% of enrollees within a county can access care within specific travel limits. It also requires MA plans to have a minimum number of providers across a range of specialties to serve beneficiaries in the county. Regional PPOs, a subset of MA plans whose benchmarks are set on a regional basis, can apply to CMS to have non-contracting hospitals “deemed” in-network for the sake of meeting Medicare’s network adequacy criteria, subject to in-network cost-sharing limits.[69]

Such deeming rights should be extended to all MA plans, but this alone is unlikely to make MA viable in rural areas. While Private Fee for Service (PFFS) plans, a small subset of MA plans without networks, had the right to “deem” providers retrospectively and to compensate them at MFFS rates for care that was delivered, they were nevertheless often unable to entice sufficient numbers of rural providers to accept MA PFFS patients.[70] Many providers may refuse to accept reasonable terms and conditions of payment from MA plans out of good faith, seeking to avoid complex cost-sharing or documentation requirements associated with reimbursement from MA plans that have few enrollees. But others seek to avoid scrutiny of the tests and services that MA will authorize reimbursement for.[71]

A baseline MA provider contract should therefore be established, with payment rates aligned with MFFS, standardized documentation and prior authorization requirements by specialty, and out-of-network cost-sharing collected by the plan. Acceptance by providers of this contract should be a condition of billing Medicare. This would allow MA plans a fair chance to compete in rural areas, greatly reduce the documentary burden on providers who participate in an MA plan, and protect providers from the risk of substantial unpaid cost-sharing—while allowing MA to generate savings for beneficiaries.

- Phase out Medicare supplemental insurance plans

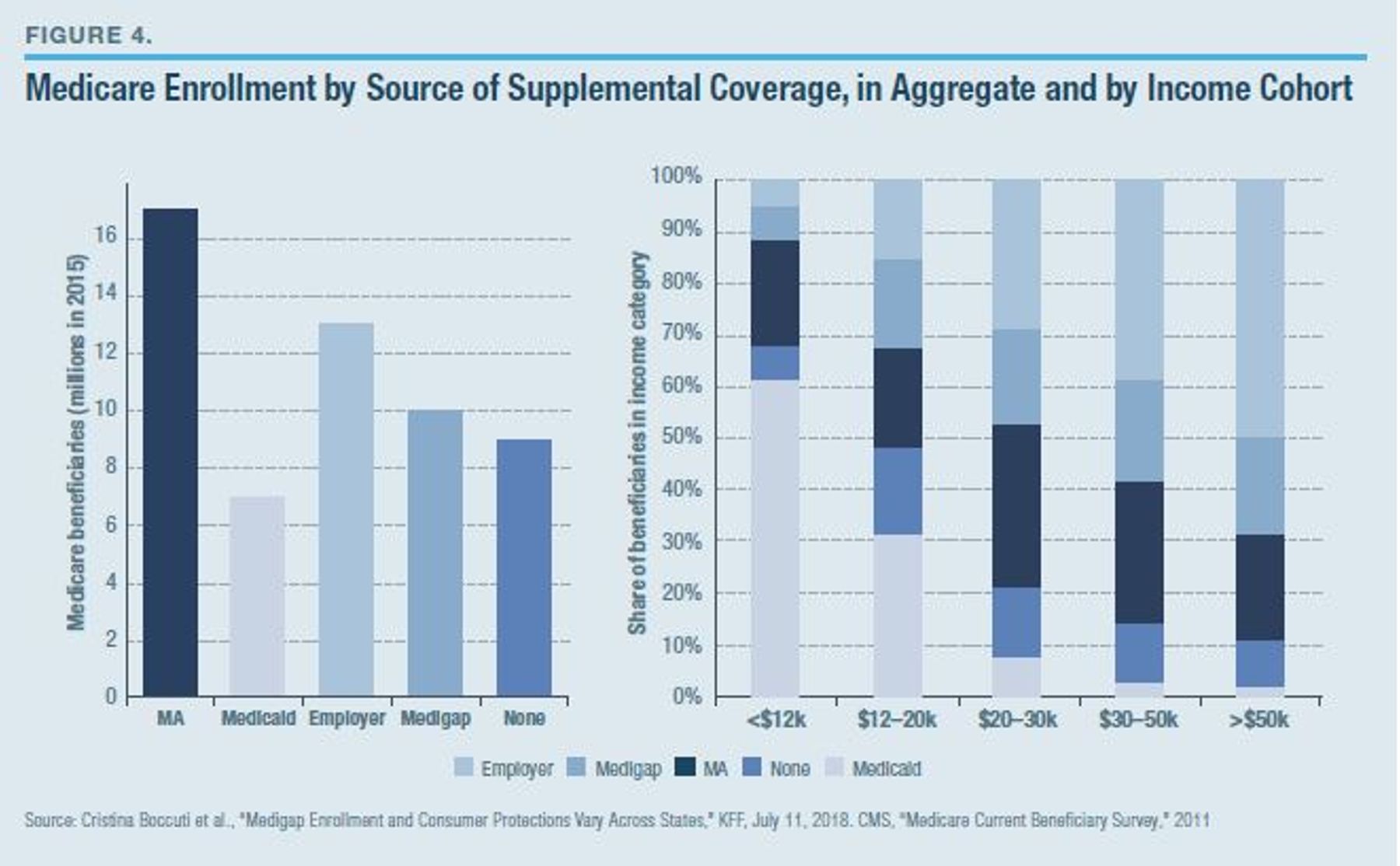

MA is often spoken of as a competitor to traditional Medicare, but only 23% of traditional Medicare beneficiaries in 2015 experienced unadorned Part A and Part B benefit structures.[72] The rest have some form or another of supplemental, or “wraparound,” insurance—from the government in the form of Medicaid, from previous employers’ retiree health benefits, or by individually purchasing Medicare supplemental insurance, called Medigap. MA’s competition is therefore as much supplemental coverage to traditional Medicare as it is MFFS itself.

Medicare supplemental coverage is highly fragmented by income (Figure 4):

Medicaid: In 2011, 7 million low-income “dual eligible” Medicare beneficiaries who also qualify for Medicaid had their cost-sharing and Part B premiums paid by “Medicare Savings Programs” and may qualify for supplemental benefits such as dental coverage.[73]

Employer-sponsored: 13 million mostly higher-income traditional Medicare patients received supplemental coverage from previous employers.[74] And 74% of employer supplemental benefits were organized around MFFS.[75]

Medigap: 10 million middle- and upper-income MFFS enrollees purchased Medigap policies to cap, reduce, and often eliminate their out-of-pocket costs.

Medigap premiums averaged $2,196 per year in 2010, with the most popular plans eliminating beneficiaries’ exposure to cost-sharing altogether.[76]

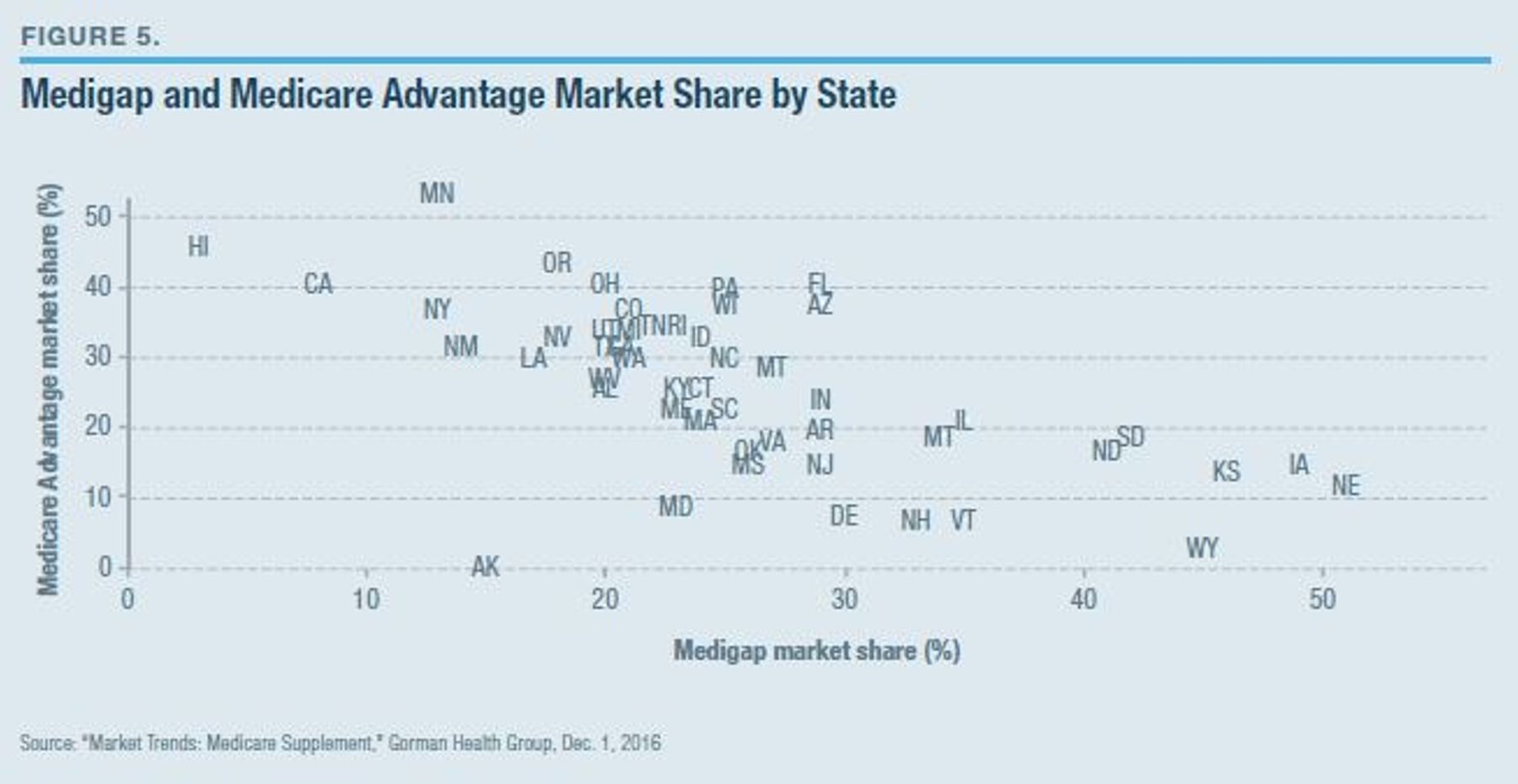

Because MFFS plus Medigap is a close substitute for MA, there is a strong negative correlation in enrollment between them. As Medigap premiums in particular regions increase, so does enrollment in MA, regardless of the availability of zero-premium MA plans in the area (Figure 5).[77]

Given that it caps cost-sharing and provides supplemental benefits without supplemental premiums, MA is more attractive to price-sensitive lower-income and urban-residing beneficiaries.[78] In 2011, 17% of white Medicare beneficiaries purchased Medigap plans, while 26% enrolled in MA; 3% of black beneficiaries purchased Medigap, while 29% enrolled in MA; 4% of Hispanic beneficiaries purchased Medigap, while 45% enrolled in MA.[79]

Why might wealthier beneficiaries seeking coverage without any network restrictions or out-of-pocket costs tend to purchase Medigap rather than Private Fee-for-Service plans under MA? Because under MA, they would bear the full incremental cost of receiving these additional benefits, whereas with Medigap they don’t.

A 2014 study commissioned by MedPAC, the federal agency established by Congress to advise it on Medicare payment policy, found that, after controlling for differences in demographics and health status, elderly beneficiaries’ enrollment in Medigap increased Medicare costs borne by taxpayers by 27% (by 13% in Part A and 45% in Part B), while the provision of employer-sponsored wraparound coverage for MFFS increased Medicare costs by 14% (by 4% in Part A and 28% in Part B).[80] The induced increase in spending was larger in absolute terms for the sick but greater in proportionate terms for healthier individuals.[81] That report’s findings align with those from a research literature stretching over three decades, including a 2017 study that used disparities in Medigap premiums arising from state boundaries crossing Hospital Service Areas to estimate that Medigap enrollment increased Medicare costs by 22%.[82] CBO has endorsed the findings of this research and consequently included savings from Medigap reform in its compendium of proposed policy options.[83]

MedPAC has repeatedly argued in favor of parity of federal subsidies between MA and MFFS, even though MA plans generate spillover benefits by improving the efficiency of medical care.[84] In fact, accounting for differences in enrollee health risks, disparities in the documentation of similar medical diagnoses, and flaws in the calculation of MA benchmarks, per-beneficiary payments to MA and MFFS are currently close to parity.[85] But MFFS ought not to be considered as a single benefit design for the purposes of assessing payment parity; instead, MFFS consists of four different programs, depending on the source of supplemental coverage.

The budgetary implications of Medicare supplemental plans are well understood on both sides of the political aisle. In his 2014 budget proposal, President Obama advocated a 15% tax on first-dollar Medigap plans.[86] The following year, Congress took a different approach to the same objective—enacting legislation that prevents newly eligible Medicare beneficiaries in 2020 from enrolling in Medigap plans that covered the Part B deductible.[87]

Both initiatives point in the right direction, but neither goes far enough. If taxes were imposed on MFFS supplemental insurance in proportion to the fiscal externality they impose on the federal budget, as average Medicare spending per enrollee was $13,087 in 2017, the efficient tax would be up to $3,271 (27%) for individuals purchasing Medigap and $1,832 (14%) for those in employer-sponsored supplemental coverage.[88] In other words, the taxes on the plans would exceed the premiums that individuals and employers currently pay for them. While neither magnitude of tax is politically likely to be implemented in full in the near future, they give a sense of the degree to which public policy has implicitly subsidized MFFS wraparound policies.

Given that a subsidy is transparently and equitably made to PFFS MA plans for those who seek to pay extra to purchase open-network coverage with minimal cost-sharing, and that employers can contribute to retiree health care in Medicare Advantage (through Employer Group Waiver Plans [EGWP]), there is no inherent public-interest justification for the continued and separate existence of Medigap plans and employer-sponsored MFFS wraparounds. Although there will undoubtedly be a need for them to be tolerated to some extent for political reasons, policymakers should embrace every incremental opportunity to tax, nudge, and regulate them out of existence—only allowing current arrangements for existing cohorts on a grandfathered basis, as with the recently enacted restrictions on Medigap coverage of the Part B deductible.

Conclusion

Medicare Advantage has demonstrated that it can provide better quality care at lower cost than Medicare’s traditional fee-for-service reimbursement model. It reduces hospitalizations, shields patients from catastrophic medical bills, and makes possible innovative integrated-care services. MA plans also provide access to prescription drug coverage at substantially less cost on average than stand-alone Part D individual plans, and help pay for dental, vision, and hearing services that are not part of the standard Medicare benefit. Upward of a third of all senior citizens have chosen MA—and with some modest budget-neutral reforms, many more could similarly benefit.

Endnotes

Photo: Wavebreakmedia Ltd / Wavebreak Media / Getty Images Plus

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).