Eliminate the Hidden Inflation Tax Why New York State Should Index Taxes to Inflation

Photo: d3sign / Moment via Getty Images

Executive Summary

New York State’s failure to index its personal income tax system to inflation exposes New York taxpayers—especially low- and middle-income earners—to hidden, compounding tax burdens. Unlike the federal government and many peer states, New York has not implemented automatic tax indexation since 2016. As a result, “bracket creep” and the erosion of the real value of deductions and credits increase tax liabilities without any legislative approval or any corresponding increase in public benefits.

This report evaluates the consequences of non-indexation in New York, demonstrating how inflation—through stagnant thresholds and deductions—results in higher effective tax rates and diminished purchasing power for residents. It draws comparisons with other states, like California, that have successfully implemented indexation and details federal practices that set a precedent. The analysis includes data models showing cumulative tax losses for different income brackets from 2016 to 2023 and how those losses disproportionately impact lower-income households.

The report highlights the political and fiscal feasibility of indexing: despite inflationary pressures, a $2.2 billion surplus in New York’s 2025 budget and past bipartisan support indicate that comprehensive indexation is both possible and prudent. Recommendations include indexing all bracket thresholds and deductions to regional Consumer Price Indexes (CPIs) to ensure equity, simplicity, and economic competitiveness. At the city level, reforms to New York City’s mansion tax and potential updates to city tax brackets are discussed, with an emphasis on geographic CPI application.

Ultimately, this report calls on lawmakers to restore tax fairness, fiscal responsibility, and democratic integrity by reintroducing tax indexation. Doing so would mitigate taxpayer flight, reduce regressive tax impacts, and align tax liabilities more accurately with real economic conditions.

Introduction

New York, like 40 other states, the District of Columbia, and the federal government, taxes personal income.[1] Taxpayers start with deductions, followed by income taxed at progressively higher rates set by explicit thresholds defined by law. The indexation of taxes incorporates automatic inflation adjustments into a tax code. In an indexed system, all dollar values—such as deductions or the threshold values for tax brackets and exemptions—rise with inflation. In other words, indexation automates a change in nominal values so there is never a change in real value. Importantly, real values describe dollar amounts in terms of their actual purchasing power, so indexation holds constant the true intention and impact of taxes.

Unindexed tax systems create a “hidden inflation tax,” burdening taxpayers in two ways. First, they erode the real value of deductions, reducing compensation for expenses such as childcare. This burden falls most heavily on low-income taxpayers, who receive the most deductions, such as the Child Tax Credit (CTC) (both state and federal). Second, unindexed tax systems can push taxpayers into higher tax brackets. This occurs because inflation increases nominal income, so taxpayers appear to be making more money.

However, prices have also increased, so taxpayers do not experience an increase in real purchasing power. Crucially, in a progressive tax system, higher nominal income (nominal income refers to income measured in current-year dollars, without adjustment for inflation) engenders a higher tax rate. In an unindexed tax regime, a common symptom of inflation is bracket creep.[2] In typical federal and state tax regimes, various tax rates are applied to various levels of income; there is no fixed rate. If incomes rise with inflation, then taxpayers are at risk of being pushed into higher tax brackets. This means that part of their earnings will be taxed at an increased rate, even though the real value of their wages has stayed the same.[3] Quite simply, this is a penalty.

Bracket creep impacts all taxpayers above the first bracket, except those already in the highest tax bracket. As the real value of bracket thresholds decreases, more and more of taxpayers’ income is taxed at a higher rate. Additionally, the compound effect makes even low wage inflation rates significant over time. In other words, so long as deductions and thresholds are not updated in one year, the next year will be two years behind in keeping pace with real value, and so on. Importantly, lawmakers do not vote on decreasing the real value of deductions or bracket thresholds, despite these effects changing the tax system. The erosion in value happens automatically, betraying the principle of democratic lawmaking in which voters have a say in tax rates through the election of their representatives. This effective tax increase occurs without any corresponding increase in the quality or quantity of public goods and services, exacerbating taxpayer dissatisfaction. This disconnect between rising tax burdens and stagnant benefits may also encourage fiscal evasion from lawmakers.

New York State Government’s Tax System

When it comes to indexation, New York’s tax code has remained largely unchanged since 2011, when Senate Bill (S.B.) S50002 indexed taxes.[4] In 2016, the New York State Legislature passed a budget proposal discontinuing tax indexation. Over the past few years, national inflation rates have surged, which can radically upset a taxpayer’s entire financial outlook. Eroding real value in an unindexed tax system is just another of inflation’s corrosive impacts. This flaw factors into why New York ranks 50th on the Tax Foundation’s State Tax Competitiveness Index.[5] While New York’s personal income tax brackets may have undergone minor adjustments since 2016, these changes have not kept pace with inflation and were not tied to any automatic indexation mechanism. As a result, taxpayers have experienced effective tax hikes through bracket creep, even without significant nominal changes to the tax code. Further, the threshold values of NYC’s personal income tax have not changed since 2010.[6] This issue is particularly pressing for New Yorkers because it is the city with the highest cost of living in the nation.[7]

The New York State Legislature recognizes this problem, and there have been attempts at adjustments at the margins. A new bill aims to index two homeowners’ exemptions, but this would only benefit the disabled and senior citizens.[8] And New York State politicians clearly recognize the importance of indexation as it relates to their career ambitions: they have not neglected to index the limits on political campaign contributions.[9] New York State should index its entire tax system to the NYC Metro CPI, prioritizing the personal income tax due to its widespread impact on taxpayers.[10] The inflation that occurred after the start of Covid-related recovery efforts shows the magnitude of the problem.

The CPI for the Northeast Region recorded that price levels had risen by 15.29% from December 2020 to December 2023, according to data from the U.S. Bureau of Labor Statistics (BLS). This drastic increase occurred after pandemic-related recovery efforts triggered the highest level of inflation in decades.[11] If the New York tax brackets had been indexed accordingly, threshold values would have risen in tandem—by 15.29%. Because they were not, taxpayers who belong in lower brackets are being pushed into higher ones. While the NYC Metro CPI is ideal for city-specific indexing, the Northeast Region CPI offers a broader and consistently available measure often used in economic analysis of state-level inflation trends. In this report, we demonstrate the detrimental effects of this unindexed tax system by estimating the answer to the following question: How much could taxpayers have saved if the New York tax system had been adequately indexed for inflation?

The Impact of Tax Indexation

Impact on New Yorkers

Assuming an average annual wage growth of approximately 5%—a figure aligned with recent trends in New York State—we can estimate the impact of bracket creep on taxpayers over the period from 2016 to 2023. Remember that bracket creep automatically triggers higher tax rates. For the average taxpayer and for the purpose of this report, we conceptualize the increased taxes due merely to nominal wage increases as “losses,” as purchasing power gets eroded by inflation confounded by taxes.

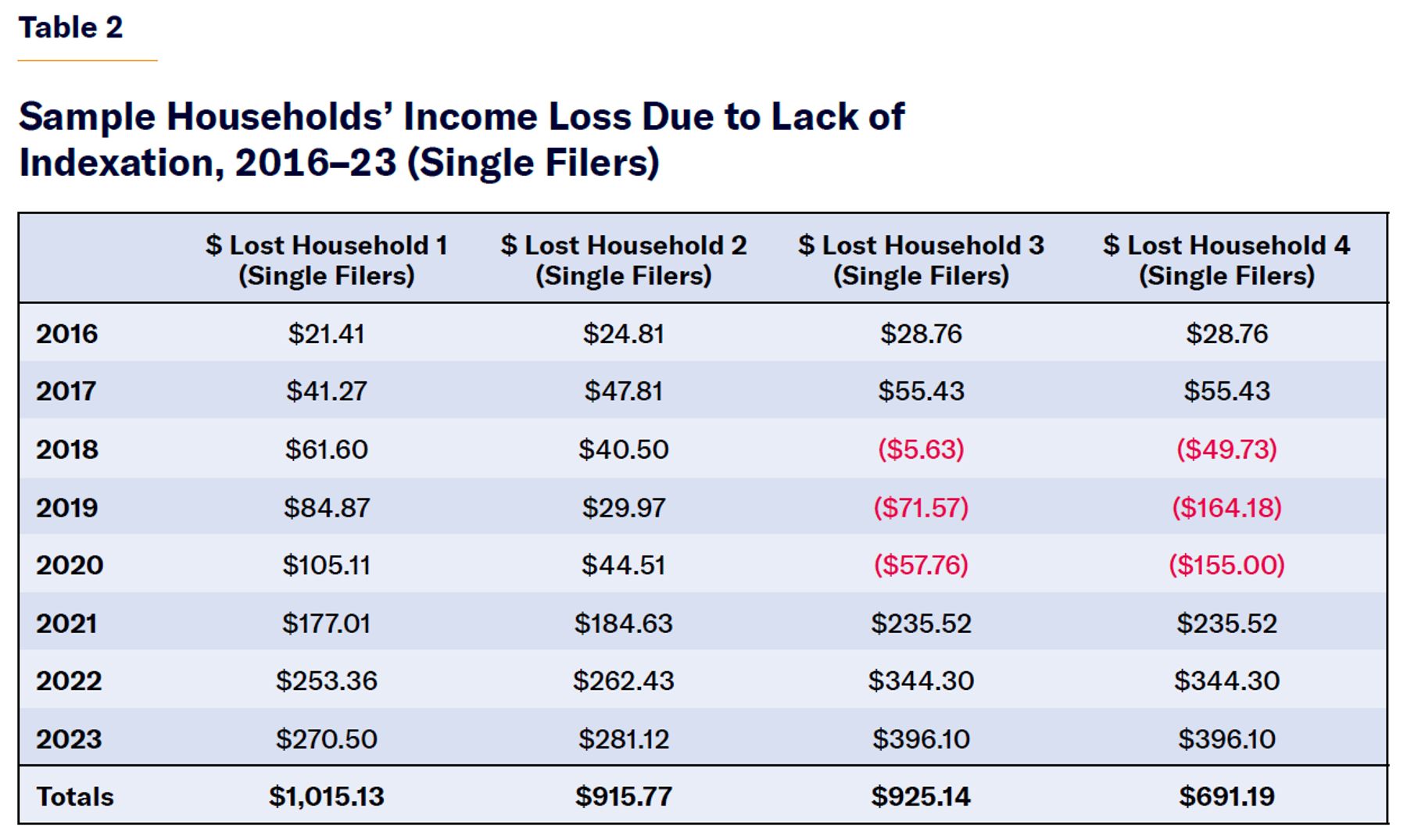

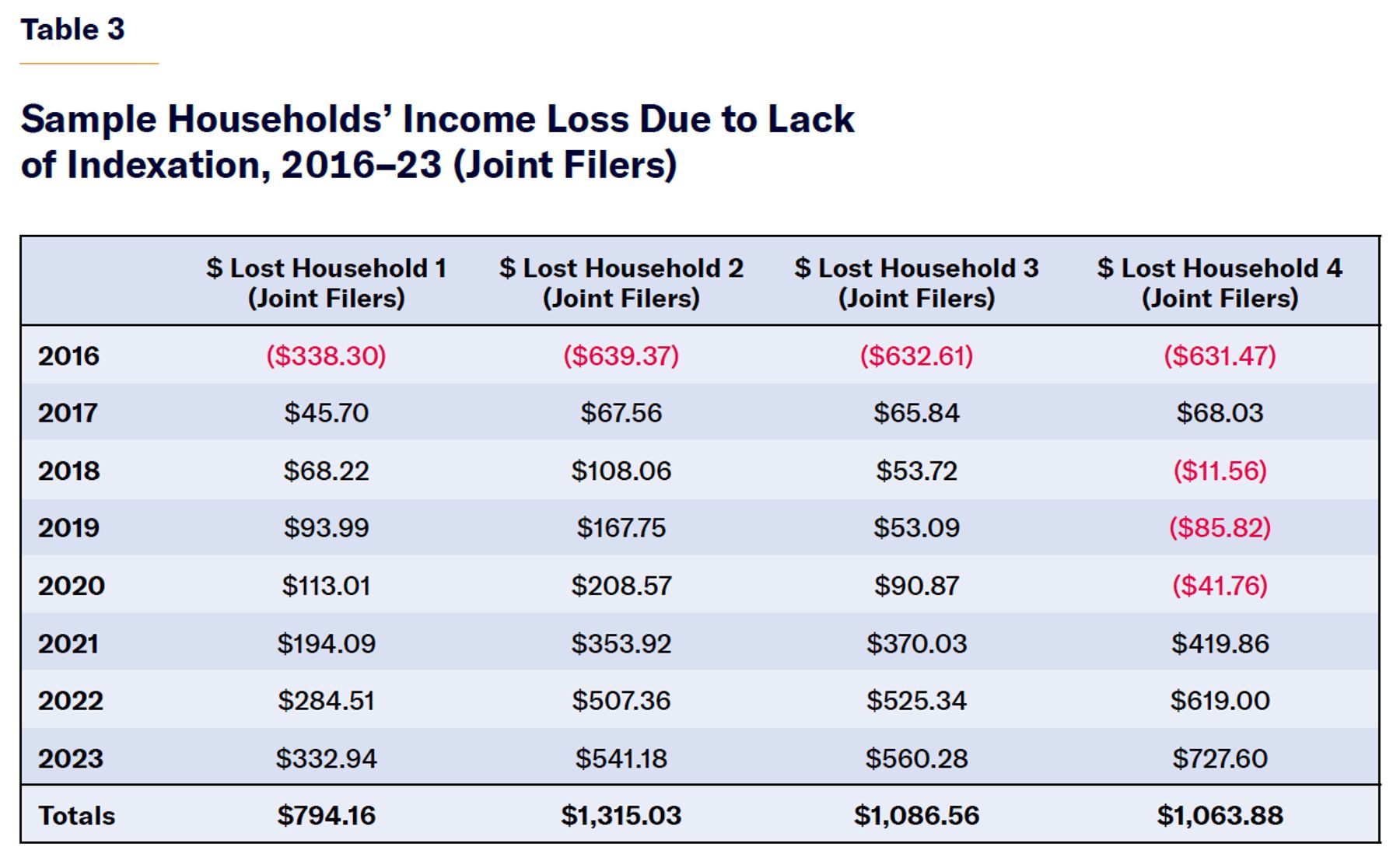

For example, joint filers who made $50,000 per year in 2016 would have seen $1,315 in cumulative losses by the end of 2023. A single filer making $25,000 in 2016 would have seen $1,015 in cumulative losses by the end of 2023. These losses add up, especially for New Yorkers with low disposable income.

Indexation also applies to the standard deduction; its current levels of $8,000 (single filers) and $16,050 (joint filers) would instead lie at $9,223 and $18,503, respectively. For low- and middle-income households, having an additional $1,000–$2,000 of untaxed income would make a significant impact on their budgets each year. It could also encourage residents to remain in the state.

New York has experienced a population loss of more than 500,000 since 2020.[12] Ensuring that New Yorkers do not face a hidden inflation tax hike can help keep residents from fleeing the state’s high cost of living. Indexation would provide savings to taxpayers, stimulating the larger economy through increased consumer spending and boosting sales tax revenue. Furthermore, indexation would offset the state’s high marginal tax rates, which discourage work and saving and thereby hinder economic growth. Through indexation, New York would become more economically competitive with states that have less burdensome tax rates, protect taxpayers from a hidden inflation tax, promote economic growth, and ensure a fairer and more predictable tax environment.

California’s Example

States like New York have recognized the need to index. New York’s income taxes resemble California’s in their high degree of progressivity. However, California indexed its taxes through a ballot proposition in 1982, right on the heels of the federal government’s decision to do so.[13] Forty-three years later, New York still has no such ballot proposition. California’s arguments in favor of indexation were twofold: protecting the purchasing power of all taxpayers’ income and shielding low-income taxpayers from rapid rate increases.[14] These issues apply today to New York as well.

First, bracket creep remains a reality. Second, like California, New York has many separate tax brackets at low levels of income. In combination with deductions that matter most for low-income taxpayers—and plummet in real value with inflation—it is the poorest taxpayers who face the highest percentage losses in income due to lack of indexation. Thus, New York should follow California’s lead in protecting the most vulnerable taxpayers from inflation-induced losses.

Implementing Indexation

The effect of leaving taxes unindexed worsens as inflation rises—particularly in a high inflation environment, generally understood as inflation exceeding 5%. While central banks such as the Federal Reserve target a 2% inflation rate, levels above 5%–10% are widely considered high and can significantly accelerate bracket creep. As such, the high inflation environment of the past few years intensifies the call to index.[15] With rates consistently higher than 2%, nominal incomes rise at a faster pace, pushing taxpayers into higher tax brackets faster than ever. Indeed, the Tax Foundation goes so far as to suggest that in high inflation environments, more than one annual adjustment or forward-looking estimate of inflation may be ideal to prevent taxpayers from overpaying. When inflation rates are high, adjusting the tax brackets in 2024, for example, to account for the inflation recorded in 2023 may still create fiscal drag.[16] Nevertheless, any indexation is better than none.

Even seemingly low rates of inflation have a compound effect over time. In other words, after one year’s inflation, higher prices are the starting point for the next year’s inflation rate calculation. As such, even though inflation rates fell in 2024, taxpayers are still paying for every year of inflation since 2016, stacked on top of one another.[17] The year 2016 was the last year in which New York changed its tax bracket thresholds, after its five-year stint of indexation to the Consumer Price Index for All Urban Consumers (CPI-U) through S.B. S50002.[18]

The impact of inflation is particularly evident in New York. Specifically, the New York–Newark–Jersey City Metropolitan Statistical Area has experienced the third highest inflation in the nation between June 2022 and June 2023 compared to other major urban areas.[19] High inflation directly undermines affordability for New Yorkers by reducing the purchasing power of their income. When inflation drives up the price of essential goods and services—housing, food, health care, and transportation—it diminishes the real value of wages. Without indexing, taxpayers not only face these higher everyday costs but also higher effective tax rates through bracket creep. Consequently, the failure to index tax brackets exacerbates affordability issues, disproportionately harming low- and middle-income households who already spend a larger share of their incomes on necessities. Only in Dallas, Texas, and Honolulu, Hawaii, was the share of this necessary spending higher. But unlike New York, Hawaii just took a major step to account for inflation in its tax system.[20] Hawaii Governor Josh Green, through the Green Affordability Plan II, recognized that Hawaii’s high cost of living was intensified by its income tax burden and bracket creep.

Hawaii witnessed firsthand the recent trend across the U.S. where residents are relocating to states that do not impose income taxes, such as Florida, Texas, or Tennessee. The Tax Foundation thus suggested that Hawaii index portions of its tax code, such as the standard deduction and bracket thresholds, to counteract migration toward lighter tax environments.[21]

Due to the laws and economic policies in place, the political environment across the U.S. is ripe to implement tax indexation. For instance, earlier this year, Connecticut indexed the taxable wage base for its unemployment insurance tax.[22] The legislature has considered indexing its income tax to inflation, especially considering that the state spending cap rises with inflation.[23] If the state government acknowledges the impact of inflation on spending, it is a contradiction not to acknowledge its impact on taxes.

The Georgia state legislature similarly signaled that the state should prevent inflation from creating unreasonably high taxes.[24] Rising home values were rapidly causing property taxes to increase, so last April the legislature passed, nearly unanimously, a constitutional amendment to cap the increases in property value assessments to be no higher than the rate of inflation.[25] Although Georgia has a flat income tax rate, the legislature should capitalize on the current recognition of inflation’s impact on the tax burden by proposing broader indexation, such as of the standard deduction.

Harms to Taxpayers

Dylan Grundman O’Neill of the Institute on Taxation and Economic Policy identifies the aggregate impact of the unindexed tax penalty over time, showing how an “inflationary tax hike” could result in almost $200 more in taxes for an individual earning (inflation-adjusted) $19,500 a year.[26] Our model corroborates this result. A hypothetical single filer earning $25,000 in 2016 would have lost a cumulative total of $270.50 between 2016 and 2023 due to bracket creep. This figure might not seem like much, but losses add up over time.

Hypothetical Households

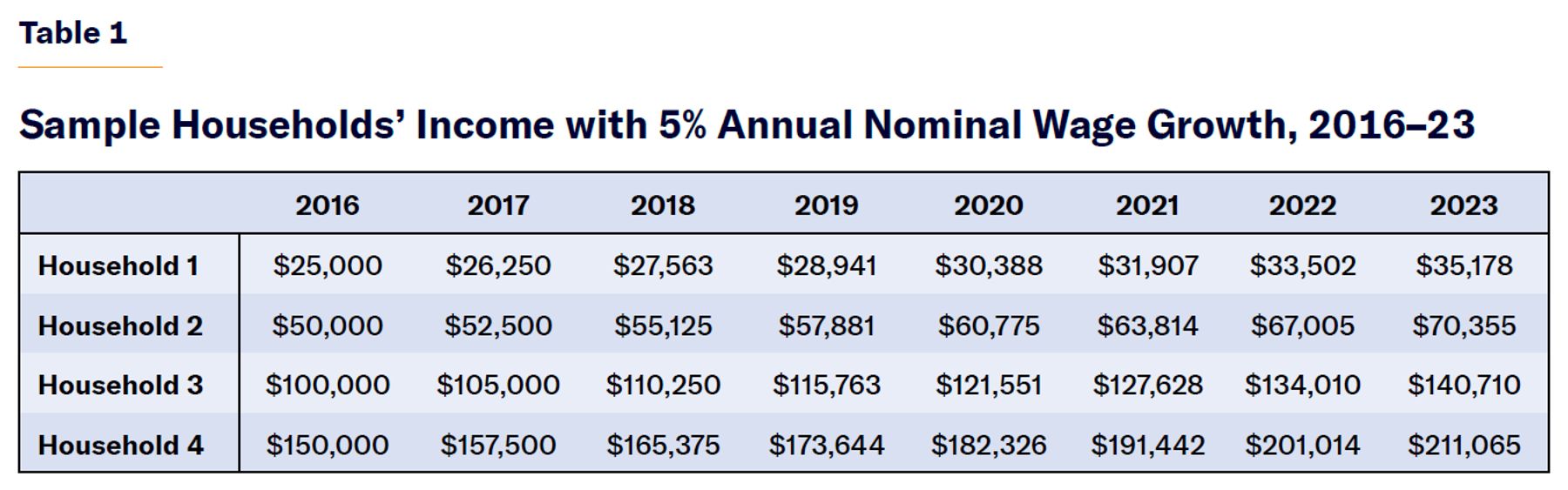

Table 1 shows four sample households with starting incomes of $25,000, $50,000, $100,000, and $150,000 from 2016 to 2023. Those incomes were chosen to demonstrate an incremental effect of nominal wage increases between different salary expectations to demonstrate the losses for lack of indexing. We applied a generous 5% annual nominal wage growth—above the regional average of 3%–4%—to emphasize the impact of non-indexed tax brackets even when wages are rising.[27]

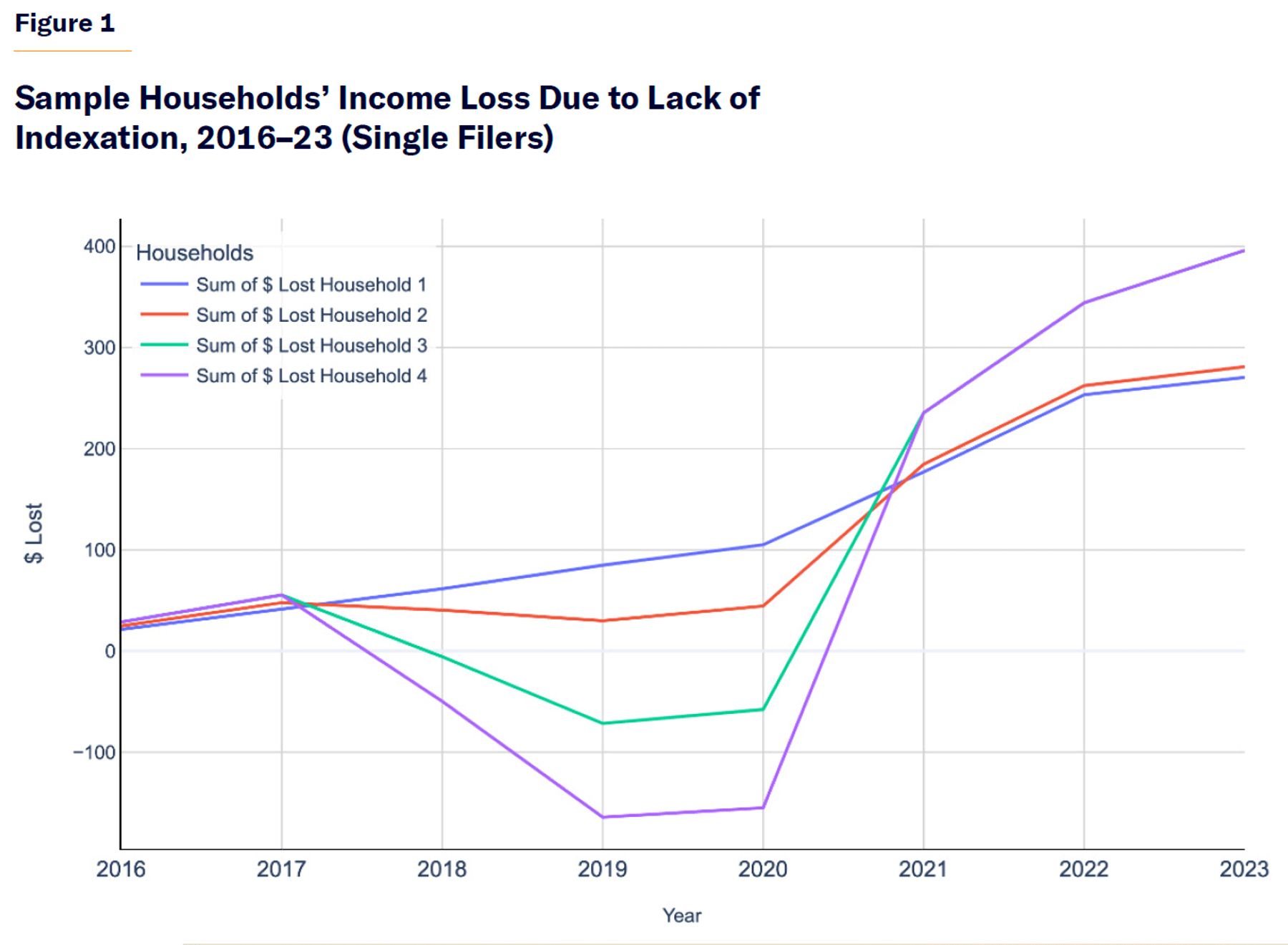

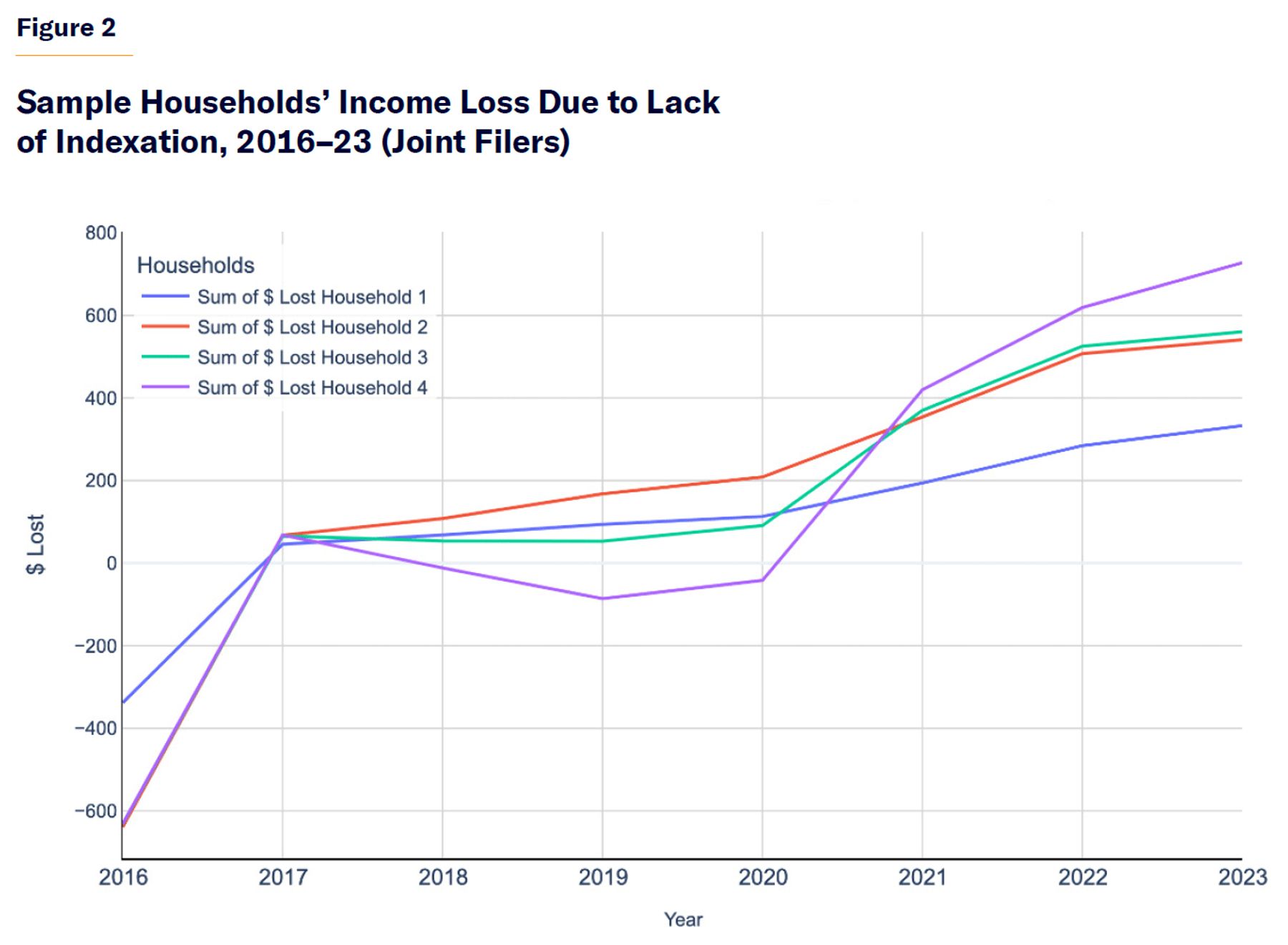

Table 2 takes those same households and demonstrates that lower-income single filers (e.g., those earning $25,000) lose proportionally more income due to the lack of tax indexation compared to higher-income single filers (e.g., those earning $150,000). From our calculations, lower-income households are disproportionally affected by the lack of tax indexing, generating the biggest losses in income from 2016 to 2023. Over this time period, the difference in lost income between the lowest-income group (Household 1) and the highest-income group (Household 4) is approximately $323.94. Figure 1 shows the same information in graphic form.

For joint filers, the pattern is less straightforward. Table 3 and Figure 2 reveal that while the lowest-income joint-filing household experiences the smallest loss, the second-lowest-income group (Household 2) suffers the greatest loss. This suggests that middle-income joint filers are most negatively affected by the absence of indexation, rather than the highest-income earners.

Inflationary Impacts on the Tax System

Inflationary impacts do not harm only those who straddle the borders between brackets. A major threat of inflation generally is its ability to create small impacts that inevitably add up.[28] This is true for consumers, for example, who face the rising prices of goods, services, and borrowing while simultaneously dealing with the decreasing real value of their savings. The same is true for taxation. Inflation impacts the elements of a tax system that provide assistance to those earning lower income, including credits, deductions, exemptions, and more.[29] There is no question that such tax benefits are important. This is why the IRS indexes many of them and assesses them annually: to protect taxpayers from losing their value.[30] This approach helps maintain the real value of these benefits over time and prevents unintended tax increases due to nominal income growth. When these benefits are not adjusted, inflation erodes their real value year after year.

Again, while the immediate impact of a few dollars year-over-year might seem miniscule, a few historical examples reflect the magnitude and importance of compounding. O’Neill cites the Illinois income tax personal exemption as a relevant case. The exemption, originally set at $1,000, remained the same for nearly 30 years, and was indexed to inflation in 2012 only after being raised by $1,000 in 1998.[31] Today, the exemption is $2,175. Had the exemption been indexed from inception, today’s credit would be more than $6,000. This differential means that failure to index even just this one exemption has cost working people thousands of dollars a year in effective tax hikes.

Another example is the unindexed CTC, which lost 25% of its real value from 2003 to 2017, according to the Tax Foundation and based on a previous report from the Niskanen Center.[32] In 2024, the Wyden-Smith bipartisan tax plan proposed indexing the CTC.[33] It is likely to be indexed with bipartisan approval because (like any deduction) its real value has eroded over time, making it less and less able to cover the true cost of childcare. The plan passed the House and is currently under consideration in the Senate.[34]

Inflation and the Covid Years

Bouts of high inflation can radically disrupt a taxpayer’s entire financial situation, and failing to index taxes is another way one can be exposed to inflation’s corrosive impacts. In the years during and after the Covid-19 pandemic, inflation hit record highs of 9% in 2022. Today, inflation is still well above the Federal Reserve’s 2% target.[35] Americans have felt the impact of such a bout. Higher interest rates have raised borrowing costs, which research suggests have caused a threefold increase in interest payments on newly originated 30-year mortgages.[36] Inflation for popular services is also still high. For example, in June 2024, the price of energy services was up 4.3% year-over-year.[37] Returning to the example of the CTC, it again illustrates how unindexed taxes amplify the burden of inflation and reveal the consequences of volatile inflationary pressures. While the CTC might have lost 25% of its real value from 2003 to 2017, from 2018 to February 2023 it lost 15% of its real value.[38]

Bracket creep assumes that as nominal incomes rise, real wages at least stay flat. But that’s not always the case.[39] From mid-2021 to mid-2023, real wages fell even though nominal wages rose—thanks to post-pandemic inflation.[40] According to Manhattan Institute fellow Stephen Miran, by fall 2023, real wages had dropped to 2015 levels.[41] This left taxpayers squeezed: inflation ate away their purchasing power while tax brackets, deductions, and credits didn’t adjust quickly enough—eroding the real value of those benefits. It was a classic case of a candle burning at both ends. More recently, however, the dynamic has improved. As of June 2024, nominal wages rose 4.2% while inflation was 3.3%, leading to a 0.9% gain in real wages.[42] While that helps taxpayers keep up with higher prices, it also means they may hit higher tax brackets faster.

The burden from inflation particularly affects lower-income Americans. These Americans are often burdened with high household debt, which surged nationally by $3.7 trillion by the end of 2019.[43] In particular, credit card debt grew by 16.6% and mortgage debt by 4% from 2022 to 2023.[44] This added debt means that the already limited household budgets of low-income taxpayers are currently stretched to a breaking point. In 2023, the bottom 20% of households had a debt-to-income ratio exceeding 150%, according to Federal Reserve data—significantly higher than pre-pandemic levels. Since the marginal value of income is much greater for these households, even modest increases in debt or inflation can substantially reduce their financial stability.

As O’Neill notes, low-income households stand to benefit the most from tax relief (credits, exemptions, and deductions) and thus suffer the most when these items are not indexed.[45] Lower-income Americans, according to economist Parker Sheppard, are also subject to greater inflation penalties than wealthier Americans.[46] Their assets, mainly cash, do not accrue value because of inflation, unlike assets such as equities, precious metals, cryptocurrency, or real estate.[47] Lower-income earners also spend a greater portion of their income on goods and services that are the most impacted by inflation.[48] Wage inflation can push low-income earners out of range for public assistance and, in the same vein, push them over the threshold for the tax breaks meant to protect them.

In a world where taxpayers cannot control prices, the value of their wages, or the cost of borrowing, tax indexing is a simple and effective remedy that alleviates one of the burdens of inflation.

New York State

Political Environment

New York State has a precedent for an indexed income tax. From late 2011 to 2016, state income tax was indexed to the CPI-U through S.B. S50002.[49] Governor Andrew Cuomo described signing this bill in his 2012 State of the State address as reforming an unfair tax code.[50] When the indexation bill was passed in 2011, the State Senate had a slim Republican majority, while the Assembly had a Democratic supermajority.[51] Despite the Republicans’ narrow two-seat advantage in the Senate, the passage of income tax indexation was bipartisan and overwhelmingly supported by Democrats, including Governor Cuomo. S.B. S50002 passed both chambers with significant majorities: the Senate at 55–0 and the Assembly at 132–8.[52] Ultimately, the indexation provision expired and was not renewed in 2016, still under the Cuomo administration.

Another recent precedent for indexation in New York State includes proposed S.B. S2960A.[53] This bill seeks to amend real property tax law to adjust the income thresholds for eligibility of Senior Citizen Rent Increase Exemption (SCRIE) and Disability Rent Increase Exemption (DRIE) programs, as well as the respective homeowners’ programs, the Senior Citizen Homeowners’ Exemption (SCHE) and the Disabled Homeowners’ Exemption (DHE). In NYC and Dutchess, Nassau, Orange, Putnam, Rockland, Suffolk, and Westchester counties, thresholds would be adjusted annually based on the CPI-U for the New York–Newark–Jersey City area.[54] For other municipalities, the Northeast Region CPI would be used for adjustments. So far, this legislation has passed in both the Senate Aging Committee (7–0) and Finance Committee (20–0).[55] It has been referred to the Senate Rules Committee and will likely pass through the Democratic supermajorities in both chambers and reach Governor Kathy Hochul’s desk.

The current political environment in New York State suggests that the indexation of income tax for inflation has a good chance of being reinstated under a comprehensive tax reform bill. Indexation may reduce state revenues relative to a scenario without indexation, potentially impacting budget forecasts—though whether it results in a true budget shortfall would depend on a range of economic and behavioral factors, including potential offsets from increased consumer spending and migration retention. This, in turn, would stimulate the state economy and boost county revenues through the shared sales tax revenue system in New York State. Overall, recent indexation efforts in the State Senate, high inflation since the pandemic, one of the highest tax burdens in the nation, and record out-of-state migration combine to make reintroducing indexation appealing to lawmakers.[56]

Recommendations for New York State

New York should modify its personal income tax to incorporate indexation. These modifications include indexing both the values of deductions and the income tax bracket thresholds. Itemized deductions needn’t be indexed, because either they are fully subtracted or a percentage of the expense is subtracted from the value owed.[57] The Earned Income Tax Credit also needn’t be indexed, as it is calculated as 30% of the federal EITC, which is indexed to inflation.[58] However, at least four deductions are unindexed to inflation and need to be addressed:

1. Standard Deduction

As mentioned, New York State’s standard deduction is $8,000 for single filers and $16,050 for joint filers.[59] Although the legislature has occasionally updated its value, the revisions do not keep up with inflation because the deduction is not automatically indexed.[60]

2. Household Tax Credit

The Household Tax Credit can be applied under income limits of $28,000 for single filers and $32,000 for joint filers. Its value is up to $75 for single filers and up to $90 plus a dollar amount determined by the number of dependents for joint filers.[61] Neither the income limits nor the dollar values of the credit have been changed since 1986, meaning its value today is close to negligible.[62]

3. Child and Dependent Care Tax Credit (CDCTC)

The state-level CDCTC is claimed as a percentage of the value of the federal credit.[63] Because the federal credit is not indexed to inflation, the values of both the federal and New York State credits have eroded over time. For example, at an income level of $25,000 or under, the state credit is 110% of the federal credit. At income levels from $40,000 to $50,000, the state credit is 100% of the federal credit.[64]

Federal guidelines stipulate that filers can claim up to $3,000 for the care of one dependent and up to $6,000 for the care of two or more, then be reimbursed for up to 50% of that claim.[65] The maximum claim values were last updated in 2000. If adjusted for inflation since 2001, the current federal values would be $5,284 and $10,568, respectively. With these adjustments, the maximum total credit for New Yorkers would be $3,699, rather than today’s $2,100.[66] Because the federal government has failed to index the CDCTC, New York State must divorce its credit from the federal one and index it to inflation.

4. College Tuition Tax Credit

The College Tuition Tax Credit is calculated as 4% of college tuition, but the maximum value of allowable college tuition is not indexed. The maximum allowable tuition was set at $10,000 in 2001 and has not changed.[67] Whatever the merits or demerits of this specific tax credit, the credit has not kept up with the inflating cost of college tuition.[68]

A Closer Look at the Standard Deduction

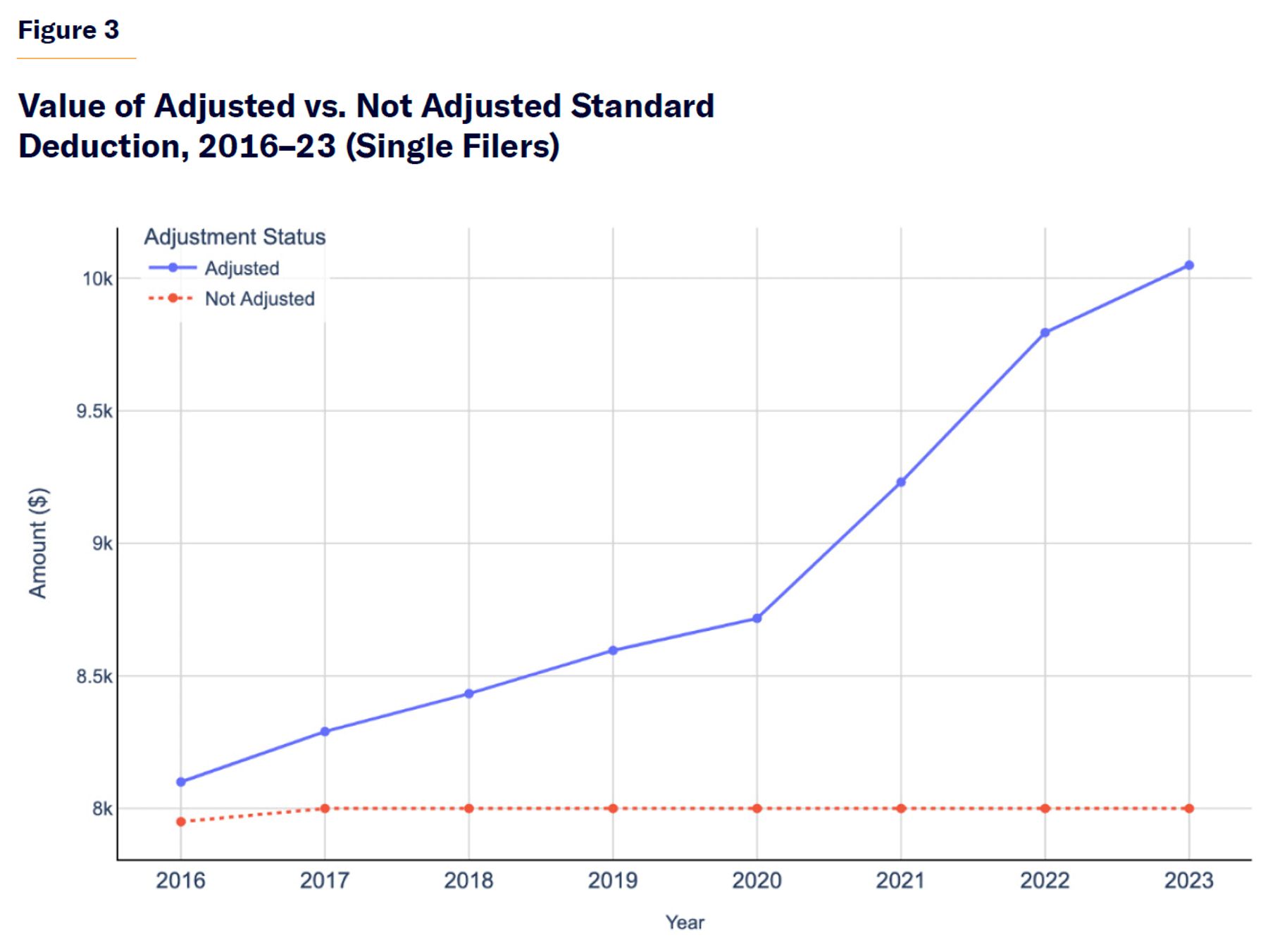

Figure 3 compares the actual standard deduction New York taxpayers received from 2016 to 2023 with the deductions that would have been available to single filers if adjusted for inflation. Over the eight-year period, single filers received cumulative savings of about $63,950. In contrast, if the deductions had been adjusted for inflation, the cumulative savings would have been roughly $71,211—indicating a loss of approximately $7,261 due to the lack of indexation.

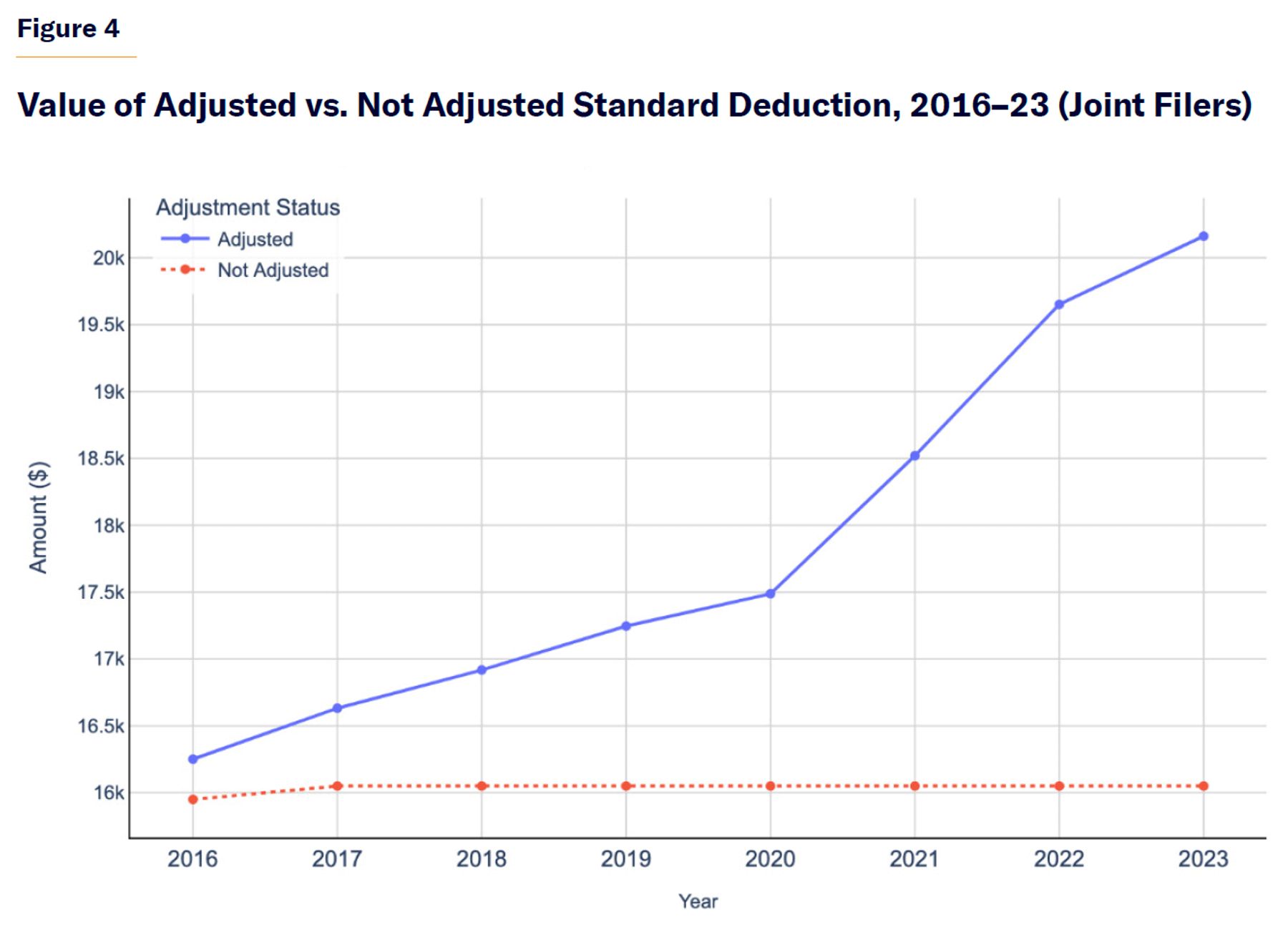

Figure 4 highlights that the standard deduction for joint filers increased only once—from $15,950 in 2016 to $16,050 in 2017—and then remained flat for seven years. Consequently, joint filers accrued $128,300 in savings without inflation adjustment compared to an inflation-adjusted total of about $142,869. This discrepancy reflects a loss of $14,569 in potential savings for joint filers over the eight-year period.

Implementing Indexation Through Regional CPIs

Currently, the state legislature must manually raise the tax bracket income thresholds. The last time those thresholds were amended was more than a decade ago, in 2014.

S.B. S2960A,[69] which was introduced in January 2023, would index to inflation four sections of property tax law: SCRIE, DRIE, SCHE, and DHE. This bill can shed light on a possible methodology for New York State tax indexation for both deductions and thresholds.

One important step the bill takes is to index upstate and downstate to two different CPIs to more accurately represent the differing effects of inflation within the state. NYC and Dutchess, Nassau, Orange, Putnam, Rockland, Suffolk, and Westchester counties would be indexed to the New York–Newark–Jersey City, NY-NJ-PA CPI-U, while other municipalities would be indexed to the Northeast Region CPI-U.[70]

This distinction is a good idea because it ensures that neither upstate nor downstate residents face bracket creep due to one CPI’s understatement of their region’s inflation. It makes the policy maximally fair and financially feasible, creating an important distinction to consider including in the indexation of the income tax.

While it is not common practice among other states to index different counties to different CPIs, it is common for states to use a regional CPI rather than the national one. California indexes based on the percentage change in the California CPI for all items.[71] California’s inflation adjustment factor ensures that its income tax brackets have the exact same percentage change as California’s CPI, rounding to a factor of $1.

Allowing tax brackets to diverge based on county across New York State may overcomplicate state tax policy. However, the state legislature has recognized that it is worth accounting for the difference in inflation by region in the tax code. One possibility to accomplish this goal is through the indexation of the standard deduction. At the state level, indexing the standard deduction or personal exemption is crucial, as acknowledged by states such as Illinois.[72]

Accounting for spatial variation in inflation incidence is critical for equitable tax policy. Theoretically, the burden of inflation differs across regions due to factors such as housing market dynamics, transportation reliance, health care costs, and distinct consumption patterns. For example, urban areas like NYC face higher housing and service costs, while rural or upstate regions may experience different inflation drivers, such as energy or transportation expenses.

Empirical data support this divergence. According to the BLS, the CPI for the New York–Newark–Jersey City metro area rose by 13.81% between 2020 and 2023, compared to 15.39% in the broader Northeast Region and 17.76% nationally. This gap underscores why applying a single CPI across all New York State municipalities risks misrepresenting the real tax burden faced by different communities. By tailoring indexation—such as through geographically adjusted standard deductions—New York can more accurately reflect local economic conditions while preserving policy fairness.

There is a trade-off between using a regional CPI and using a chained CPI, because the BLS only calculates the chained CPI at the national level. Chained CPI better takes into account substitution of goods, but requires multiple months of revisions. On the other hand, using a traditional, regional CPI in indexing ensures that taxpayers will not be over- or underprotected from inflation-induced tax hikes merely because of New York’s divergence from national inflation trends. Indeed, most other states that index use a regional CPI.

The takeaway from New York’s bill and California’s tax codes is that inflation adjustment should occur based on a regional CPI—one that zeroes in on the inflation that state residents experience every day. New York State should thus index all income tax bracket thresholds to either the NY-NJ-PA CPI-U or the Northeast Region CPI, so as not to overcomplicate the tax code. However, the legislature should consider the option of including intrastate differences in inflation elsewhere in the tax code, such as through the standard deduction.

Accounting for Decrease in New York State Tax Revenue

While tax indexation typically leads to reduced income tax revenue for the state, it may also influence taxpayer behavior in ways that partially offset these losses. For example, increased disposable income could lead to greater consumer spending, which in turn may boost sales tax collections and local economic activity. Governor Hochul’s 2025 $237 billion state budget includes both tax breaks and significant spending, such as a break for real estate developers to stimulate New York’s stagnant housing market. New spending includes $2.4 billion on caring for migrants in NYC.[73] Nevertheless, New York does have room in the budget for a decrease in revenue from the personal income tax: the proposed 2025 budget has a $2.2 billion surplus.[74] As such, indexation would not send the state into debt.

Indexing taxes may also prevent migration out of New York, which will stop a decrease in tax revenue. For example, Comptroller Thomas DiNapoli found that in 2019, the revenue loss due to taxpayers moving out of state amounted to $360 million.[75] The year 2019 was before out-migration became particularly enticing due to the pandemic. In 2021, the net number of taxpayers who moved out of New York was more than 10,000 higher than the annual average of 28,700 from 2015 to 2019. Specifically, almost three times the number of millionaires who left in 2019 migrated out of state in 2021. Unsurprisingly, Comptroller DiNapoli warned that this trend will harm personal income tax collections.[76]

Once a taxpayer reaches the highest tax bracket, all other income becomes subject to that tax rate, too, amounting to an additional penalty of $22,000.[77] This provision makes it illogical for higher earners to remain in New York. While indexation will not eliminate this problem, preventing taxpayers from drifting upward into a higher tax bracket—and thus subject to a higher tax rate—will disincentivize migration out of New York and have the potential to increase New York’s overall tax revenue.

New York City

Political Environment

NYC is far less likely to implement changes to its income tax code than New York State. In recent years, the predominantly progressive City Council has focused on providing targeted relief to low-income households through tax credits, rather than offering broad relief to all taxpayers who have been deeply affected by inflation. This approach is exemplified by the 2022 expansion of the EITC, which increased the credit percentage for eligible low-income taxpayers.[78] However, substantial changes to the city’s income tax code have been on the back burner for years, with the last major structural adjustments occurring in 2006 under the Bloomberg administration. During that period, temporary tax brackets and rates introduced in the early 2000s expired, leading to the current four-bracket system with rates ranging from 2.907% to 3.876%. Given the current political landscape—with 45 Democrats and only 6 Republicans on the City Council, alongside Democratic control of the mayor’s office—significant changes to the city’s income tax are highly unlikely.

Another critical factor is the severe fiscal stress NYC is currently experiencing. City Hall’s projections for asylum seeker costs have fluctuated dramatically. Initially budgeted at $2.91 billion for FY 2024 and $1.00 billion for FY 2025, these costs were revised upward by $6.91 billion in August, bringing the total to $10.82 billion—a staggering 177% increase.[79] In response, Mayor Eric Adams mandated that city agencies identify 5% savings in each of the next three financial plans, amounting to nearly 15% in total, to offset the additional asylum seeker costs. Furthermore, the Office of Management and Budget (OMB) has implemented a hiring and spending freeze. While OMB projects a balanced budget for FY 2025, the Comptroller’s Office anticipates a $3.30 billion gap in FY 2025, which could grow to $10.54 billion in FY 2026 and $13.50 billion in FY 2028 when including the costs of asylum seekers and mandated class-size reductions. Under these circumstances, introducing income tax indexation—despite its potential benefits to taxpayers and the likelihood of increased sales tax revenue and mitigation of out-migration—would likely exacerbate these budget gaps.

Unlike other policies, the city’s mansion tax may be easier to reform. NYC is one of just a few jurisdictions—including six states and D.C.—that impose this real estate transfer tax on properties over $1 million.[80] It contributes to the city’s already high home-buying costs.

Today, the mansion tax no longer serves its purpose because of inflation in real estate prices. Lack of indexation means that today, the mansion tax targets the average homebuyer, not the wealthy one. When the mansion tax was first introduced in 1989, $1 million may have been an effective threshold to target, well, mansions. Today, the median price of a home sold in NYC is $776,000, and 41% of all listings are above $1 million.[81] That’s hardly the top 1%. The mansion tax is thus an example of rampant bracket creep.

In response to the high price of homeownership in NYC, recent city property tax reform proposals were presented to the 2018 and 2022 City Charter Revision Commissions (CRCs).[82] The 2018 proposal suggested that Class 1 properties, which include one-, two-, and three-family homes, should receive preferential tax treatment to encourage homeownership. Despite their owner-occupied status, cooperative and condominium units are classified as Class 2, which the proposal argued should bear progressively higher effective tax rates compared to Class 1. Although these proposals did not address the mansion tax directly, they highlight the political will for property tax reform in NYC.

Affordable housing remains a major challenge. Homeownership is just 30% in the city—far below the national average of 66%.[83] As average home prices approach the $1 million mansion tax threshold, this added cost risks further driving up prices and pushing homeownership out of reach for many. In turn, demand for affordable housing may grow, increasing pressure on the city to expand support for middle-income residents.

In summary, the current political environment in NYC suggests that while the indexation of the city income tax is unlikely due to a lack of political will, budgetary constraints, and the city’s legislative priorities, some degree of reform to the mansion tax appears more feasible. The potential for mansion tax reform is supported by recent CRC proposals and its implications for affordable housing and homeownership across the city.

Recommendations for NYC

Proposed reforms will make NYC’s personal income tax more progressive than ever. In 2023, Comptroller Brad Lander recommended reforms to make the personal income tax even more progressive by adding one to three more tax brackets. Currently, the top rate kicks in at $50,000 for singles and $90,000 for joint filers. Lander recommends that a new bracket be added with a higher rate at $500,000 for singles and $750,000 for joint filers, an attempt to target the wealthiest New Yorkers.[84]

New York has the second highest city income tax rate in the country, and research shows that has led to decreases in employment.[85] For example, NYC lost an estimated 331,000 jobs from 1971 to 2001 because of local income tax increases. Importantly, overall migration (both in and out of the city) has risen in recent years, especially among high-income earners who would see a higher tax rate under Lander’s proposal.

Measured in the difference in adjusted gross income (AGI) between incoming and outgoing taxpayers, the city lost 1% of AGI in 2012. The loss increased to 6.5% of AGI in 2021.[86] Migration of high earners results in a loss of both tax revenue and economic activity for the city. Without indexation, inflation can push taxpayers into higher tax brackets than those originally intended by lawmakers, effectively increasing their tax burden without legislative action. This can intensify out-migration pressures. By indexing the personal income tax, the state can preserve the integrity of its original tax structure and avoid exacerbating taxpayer flight driven by unintended bracket creep.

Adding progressive thresholds to the city’s already high income tax only intensifies the need to index it. The more tax brackets a system holds, the greater the potential for bracket creep. Each new threshold is another value that will become outdated should it not automatically rise with inflation. NYC needs indexation because the City Council has shown that it will not raise bracket values to keep up with inflation. Currently, the thresholds have not been changed since 2010, and neither has the NYC School Tax Credit.[87]

Digging into the NYC School Tax Credit

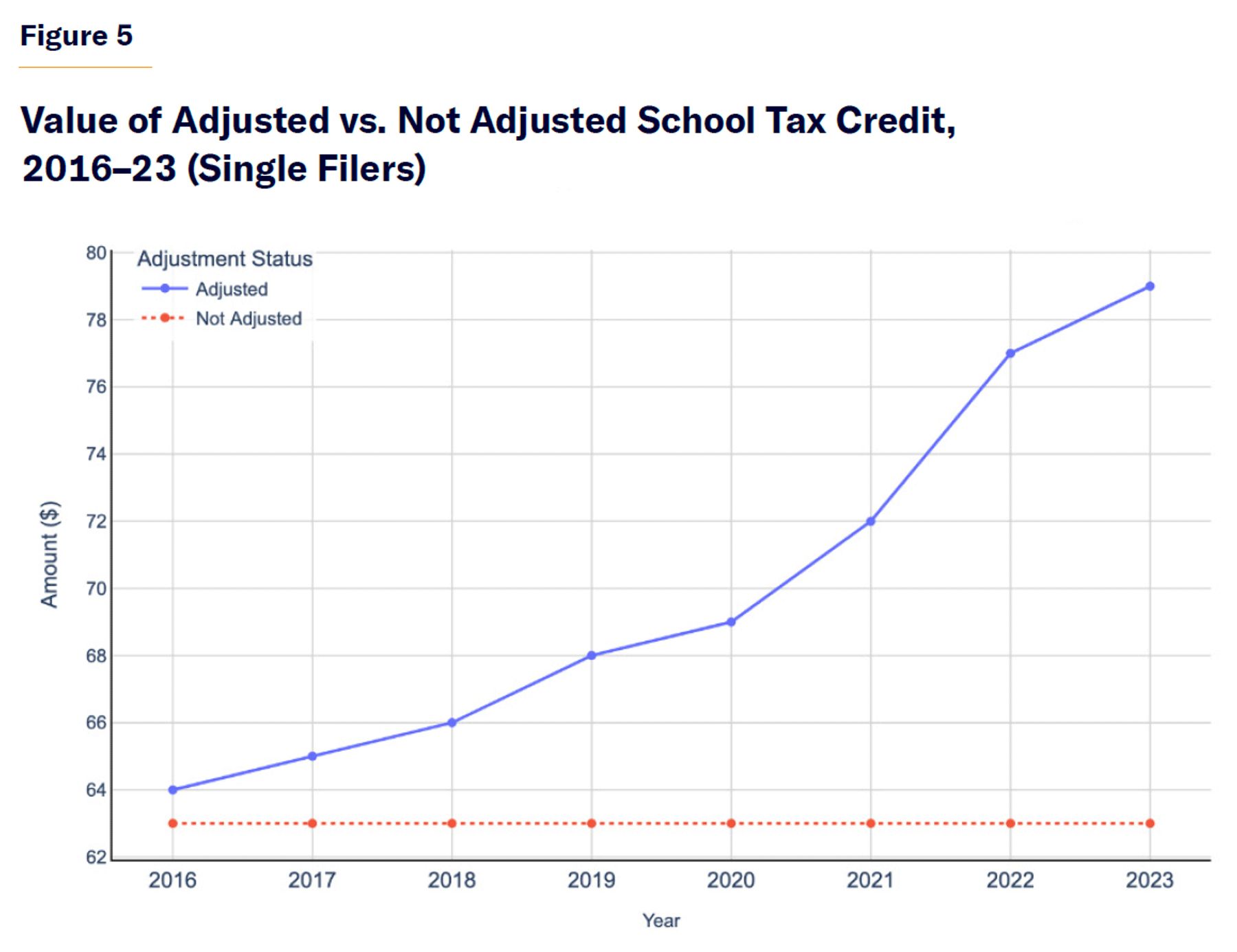

Figure 5 depicts the difference between the actual School Tax Credits received for single filers and the credits that would have been available if they had been adjusted for inflation in the NYC metro area. Single filers received cumulative credits of approximately $504 without adjustment, versus an inflation-adjusted total of around $560. This difference means that single filers effectively lost a total of $56 in potential savings due to the lack of indexation.

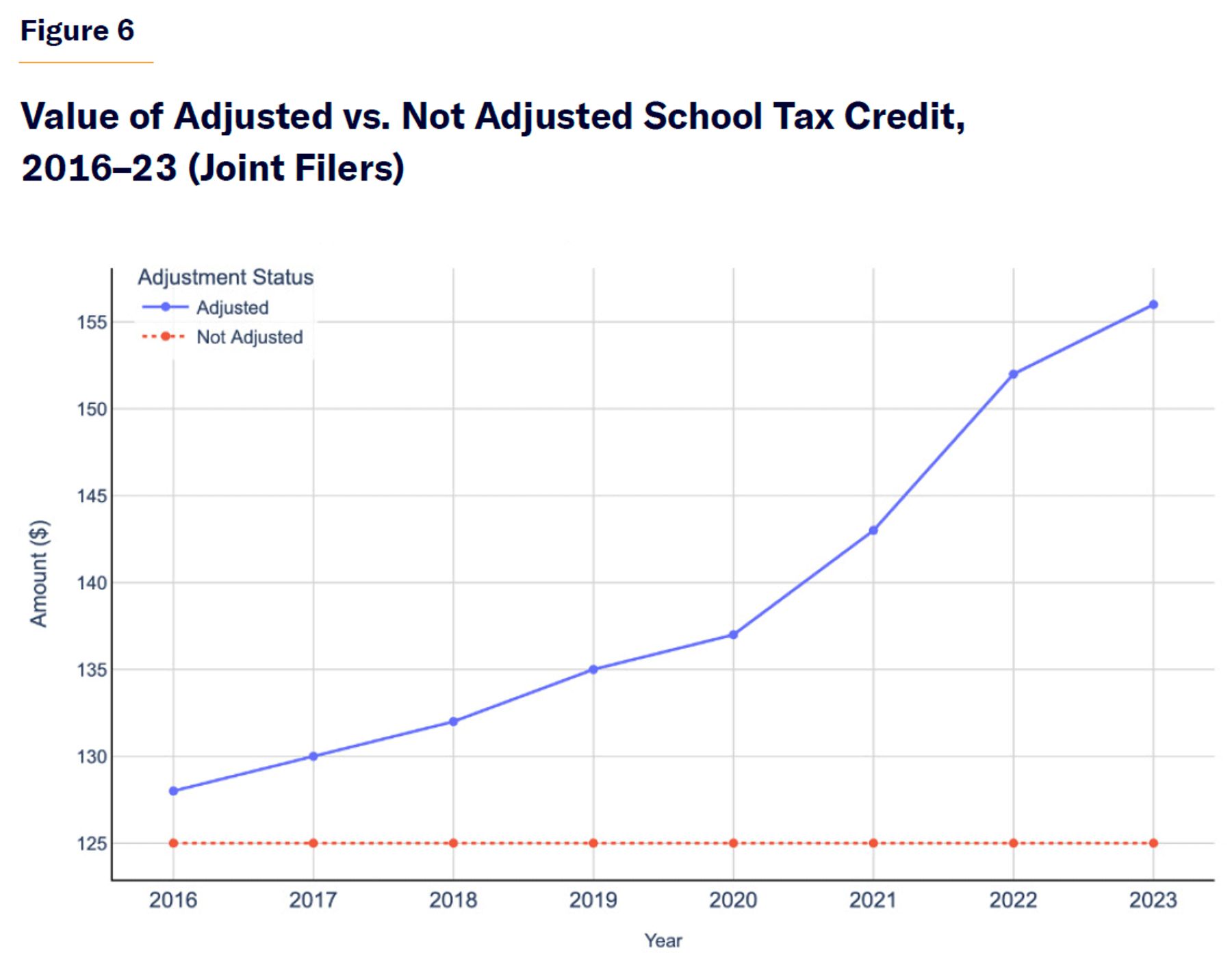

For joint filers (Figure 6), the School Tax Credit remained unchanged. Over the eight years, joint filers accumulated $1,000 in credits without indexation compared to an adjusted total of roughly $1,113. This results in a loss of about $113 in potential savings because the tax credit was not adjusted for inflation.

Additional Reforms

Lawmakers should consider indexing the NYC income tax to the city’s metro area CPI (New York–Newark–Jersey City), which zeroes in on city-specific inflation.[88] Because the most recent change in tax bracket threshold values was in 2010, the city should consider adjusting current thresholds to reflect the cumulative inflation that has occurred since then. This would mean indexing from 2010 forward.[89] While this would not necessarily involve retroactive tax refunds, it would reset the brackets to where they would be had indexation been applied annually, ensuring that current taxpayers are not overburdened by outdated thresholds, especially in light of pandemic-era inflation.

Last, the mansion tax must be indexed to inflation, and policymakers should consider raising the threshold immediately to account for the inflation of the past three decades. If indexation had been included in the initial policy, the threshold for the mansion tax would today be more than double its current value: $2.6 million.[90] For this reason, the Center on Budget and Policy Priorities recommends that all mansion taxes be indexed to inflation to ensure that the tax truly remains focused on the same percentage of high-value homes.[91]

Conclusion

Indexing New York State’s taxes will ensure that the system reflects the real value of money and stop taxpayers from being shortchanged by the falling purchasing power that inflation creates. Indexation would prevent the erosion of the real value of the standard deduction, the Household Tax Credit, the Child and Dependent Care Tax Credit, and the College Tuition Tax Credit—four deductions outlined in nominal terms. Indexation would also prevent bracket creep, which occurs when rising nominal incomes push taxpayers into higher tax brackets with no correlated increase in purchasing power.

Tax indexation is not a controversial policy; not only does the federal government index taxes, but its economic logic is also indisputable. Economic wisdom and common sense hold that nominal values must be adjusted for inflation to retain the same purchasing power; indexation simply applies this principle to taxes. Although indexation will give consumers additional spending money to stimulate the economy, the most compelling reason for indexation is not the economy; it is fairness. In a democracy, we agree that all changes to taxes must be passed through a legislative process. Therefore, we must update the system that allows tax benefits to decrease in value automatically—without any deliberate action from lawmakers or voters.

About the Authors

Paul Dreyer is a Cities Policy Analyst at the Manhattan Institute, where he focuses on urban policy issues affecting New York City and State. His research encompasses state constitutional amendments, governance, public safety, and infrastructure development, with a particular interest in state politics and its impact on local policymaking.

A lifelong Long Islander, Dreyer served as a legislative aide in the New York State Senate, advising on policy matters related to mental health, the judiciary, and criminal justice. He also worked as assistant to Brookhaven Town Supervisor Ed Romaine, contributing to local policy initiatives and community relations. Dreyer started his career in the office of Congressman Lee Zeldin, focusing on policy research and constituent services.

Dreyer’s analyses have been featured in publications such as RealClearPolicy, the New York Post, and City Journal, covering a variety of topics. He holds a B.A. in political science from Stony Brook University, where he graduated summa cum laude.

Victoria Freeman was a Collegiate Associate at the Manhattan Institute. She is a senior at Georgetown University majoring in economics and government. She currently works at Brinen & Associates as a law clerk.

Matias Ahrensdorf is a junior web developer at the Manhattan Institute, where he supports scholars with data analysis across a range of research projects and helps manage the organization’s suite of digital platforms. His writing and analyses have appeared in RealClear and City Journal, among others. Ahrensdorf holds a B.S.B.A. in finance from Elon University.

Acknowledgments

Thanks to Manhattan Institute policy analyst Santiago Vidal Calvo for his research and contributions to this report.

Endnotes

Photo: d3sign / Moment via Getty Images

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).