A Blueprint for Sustainable Discretionary Spending Caps

Photo: Douglas Rissing/iStock

The recent enactment of statutory discretionary spending caps for FY 2024 and FY 2025 has revived the debate over the importance, efficacy, and design of discretionary spending caps. Within the next two years, Congress will debate whether to revise and extend those spending caps in order to address annual budget deficits that have doubled to nearly $1.5 trillion since 2018 and are projected to approach $3 trillion within a decade.[1] Discretionary spending, which has gradually fallen to 27% of total federal spending, is not the main driver of runaway deficits. But nonemergency discretionary appropriations have jumped by 23.4% in the past two years, adding $300 billion to current spending levels and raising the ten-year discretionary spending baseline by nearly $3 trillion.

The 2021 expiration of the discretionary spending caps of the Budget Control Act (BCA) has clearly led to a surge in “regular” (i.e., nonemergency) discretionary spending. However, even before expiring, BCA’s effectiveness was gradually weakened, as lawmakers repeatedly increased the caps. Additionally, the new 2024 and 2025 caps were accompanied by a concurrent bipartisan agreement to evade their spending levels in the later appropriations bills.[2] Therefore, future reimpositions of multiyear discretionary spending caps must be informed by the successes and failures of earlier caps.

History has shown that, paradoxically, overly ambitious discretionary spending caps that attempt to constrain spending too tightly will ultimately backfire and bring larger spending increases than less tight caps. Modest spending caps that accommodate realistic appropriations growth rates have sustainably reduced discretionary spending as a share of the economy. By contrast, caps requiring drastic cuts, or little to no annual spending growth, have typically been disregarded by Congress (or abused through loopholes) and replaced with appropriations hikes exceeding 10%. Because spending caps can be easily repealed at any time, they cannot force spending cuts beyond the political system’s capacity. They can only enforce an existing broad commitment to constrain spending.

Discretionary spending is not the lead driver of deficits, but it is typically the first place that Congress looks for deficit reduction. In fact, the six largest deficit-reduction laws since 1983 have cumulatively produced 53% of their savings from discretionary spending.[3] Preventing discretionary spending from growing faster than the economy is a necessary piece of the deficit-reduction puzzle. This report shows how Congress can best design sustainable caps on discretionary appropriations.

Discretionary Spending Background

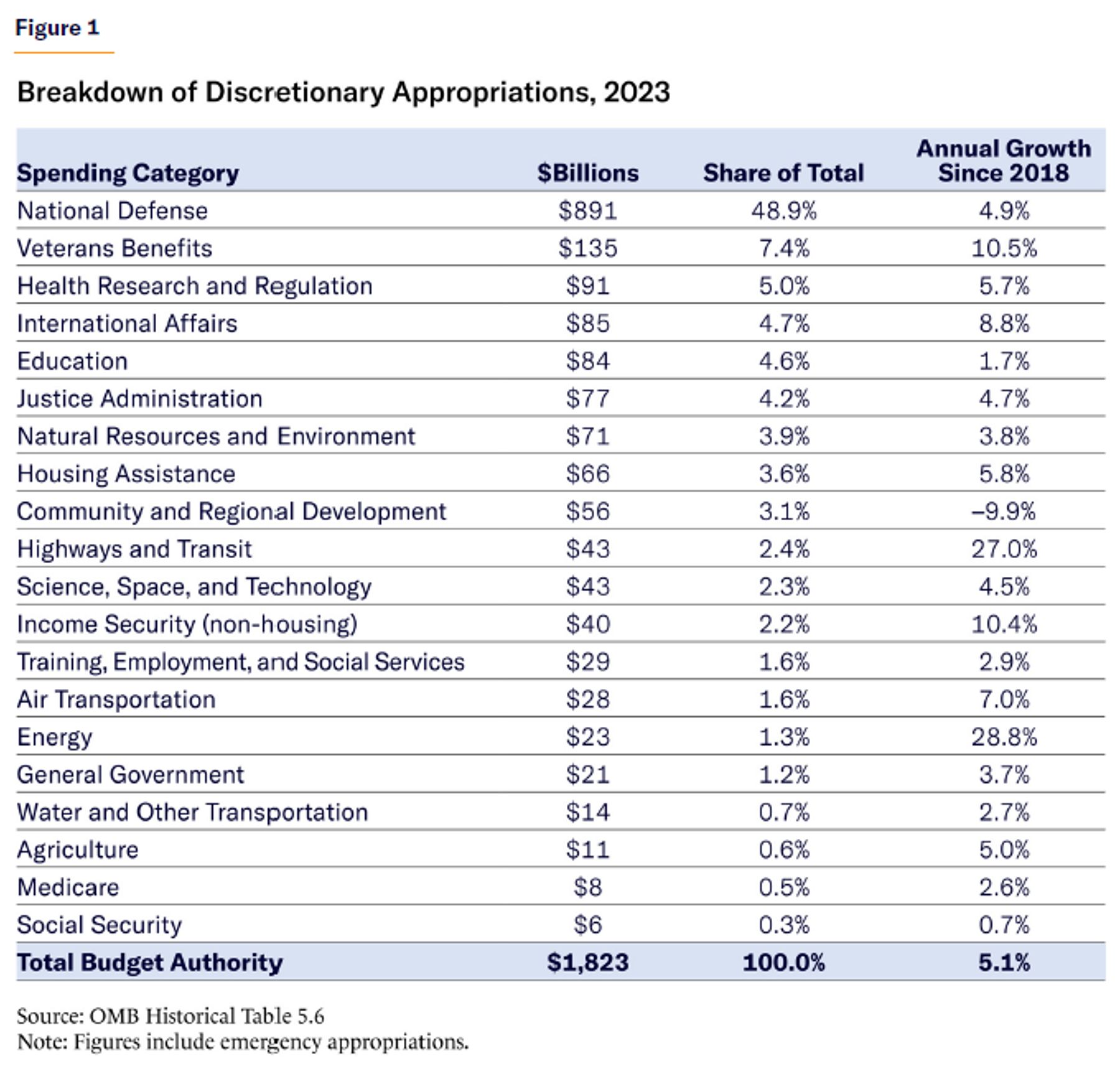

Virtually all federal spending programs are classified as either discretionary or mandatory. The spending levels for discretionary programs are set directly by Congress and the president through the annual appropriations process. Defense constitutes nearly half of discretionary spending, which also includes most spending on veterans’ health, K–12 education, health research, NASA, international assistance, and justice (Figure 1).

By contrast, spending levels for mandatory programs (mostly entitlement programs) are set by occasional authorizing legislation. For programs such as Social Security, Medicare, farm subsidies, and most antipoverty spending, Congress sets eligibility and benefit formulas, and then spending levels are determined by how many people enroll and where they fit into the benefit formula. Social Security, Medicare, and Medicaid have permanent authorizations, meaning that their underlying parameters never expire and are changed only when Congress and the president so desire, while other mandatory spending programs—as well as their eligibility and benefit formulas—are typically reauthorized by Congress on a schedule between two and seven years.

Because Congress does not set mandatory program spending levels (with a few minor exceptions),[4] these programs are often described as “uncontrollable” or “on autopilot.” Costs rise rapidly with program participation because of eligible population growth. At the same time, benefit formulas automatically rise each year; and occasionally, Congress passes legislation further expanding eligibility and benefit parameters. Because mandatory programs are not appropriated annually, Congress has little reason to provide oversight, address waste, or subject these programs to broader budget targets. Overall mandatory spending—excluding net interest costs on federal debt—has leaped from 5% to 15% of GDP since 1962.[5] And it is projected to continue rising indefinitely, driven entirely by escalating Social Security, Medicare, and Medicaid costs.

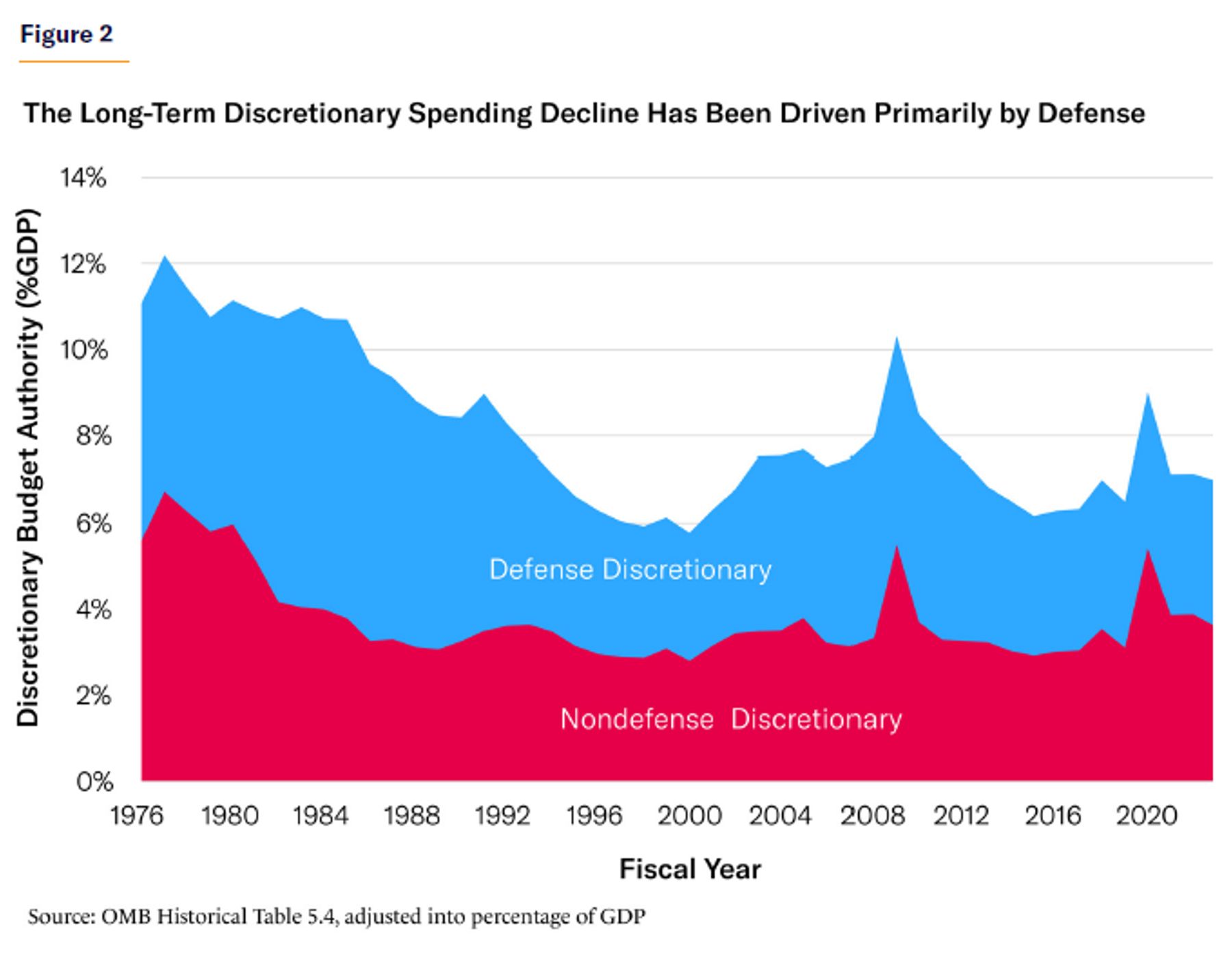

Discretionary spending levels, on the other hand, must be reappropriated annually and are subject to regular oversight when there is a spending target to meet. Increasingly crowded out by mandatory spending growth, discretionary spending has fallen from 67% to 27% of federal outlays since 1962.[6] During this period, discretionary outlays as a share of GDP decreased from 12.3% to 6.6%, bottoming out at 6.0% in 1999.[7]

The decline in discretionary spending has been driven by defense spending. Its share of the economy gradually fell from 9% in the early 1960s, to 3% shortly before the 9/11 attacks, which brought a rebound to 4.6% by 2010, before falling back to 3% by 2023 (Figure 2).

Nondefense discretionary spending levels have remained steadier, typically ranging between 3.0% and 4.5% of GDP, with a current level of 3.6% of GDP. Still, since 1990, nondefense discretionary spending (after inflation) has expanded by 154%, versus 35% for defense.[8]

Thus, while discretionary spending has not been the driver of rising long-term deficits—and cannot realistically be cut deeply enough to accommodate surging mandatory costs—Congress should still approach this spending with a “do no harm” principle, ensuring that it does not rise as a share of the economy and further deepen the surging baseline budget deficits.

The Modern History of Discretionary Spending Caps

Statutory discretionary spending caps were born from the failure of broader deficit-reduction targets. In 1985, rising deficits led Congress and President Ronald Reagan to enact the Balanced Budget and Emergency Deficit Control Act of 1985 (nicknamed “Gramm-Rudman-Hollings” [GRH], after its lead Senate authors). The law set declining annual deficit targets—enforced by automatic cuts of any overages, known as “sequestrations”—that aimed to eliminate the budget deficit by 1991. A Supreme Court decision forced Congress to rewrite the law in 1987, which pushed the target balanced-budget date to 1993.[9]

GRH modestly restrained spending and deficits. However, the law was also sabotaged by typical congressional and White House shenanigans: exempting certain policies, tweaking economic assumptions, and blocking enforcement of deficit targets. More damaging, however, was GRH’s lack of flexibility to accommodate temporary deficit increases brought on by non-legislative changes such as a recession.[10]

In late 1990, with a weakening economy pushing up deficits and threatening a large sequestration, President George H. W. Bush and congressional leaders replaced GRH with the Budget Enforcement Act (BEA), as well as new legislation to raise taxes and trim mandatory spending.[11] BEA imposed multiyear caps on discretionary appropriations and imposed Pay-as-You-Go (PAYGO) rules blocking, via sequestration, new mandatory spending or tax legislation that would collectively widen projected budget deficits.

BEA represented a different approach from GRH in two key ways. First, while GRH was designed to spur future legislation to reduce baseline deficits, BEA was intended to protect concurrent deficit-reducing legislation from future repeal. PAYGO would limit Congress’s ability to repeal the budget deal’s tax increases and mandatory spending savings (or hike deficits through other tax cuts or mandatory expansions). The five-year discretionary spending caps would codify the existing bipartisan commitment to pare back the growth of appropriations. In short, while GRH was offensive (motivating future deficit reforms), BEA was defensive (protecting past deficit reforms).

Second, by limiting only new deficit-expanding legislation—PAYGO applied only to newly legislated expansions—BEA did nothing to limit the automatic baseline growth of mandatory spending due to pre-1990 program rules. Nor did BEA impose any constraints on automatic deficit fluctuations resulting from booms, recessions, and the business cycle.

1991–2002 BEA Period

BEA capped discretionary budget authority for 1991 through 1995 at a growth rate averaging 1.3% per year (in nominal dollars).[12] Separate sub-caps were created for defense, international, and domestic appropriations for the first three years in order to provide predictability and prevent partisan raids of generally “Republican” defense spending and “Democratic” domestic spending. The caps were enforced by House and Senate points of order against legislation exceeding the targets, which, in the Senate, crucially required a three-fifths vote to defeat. And even if that waiver threshold was met and the caps were exceeded, the law mandated an automatic, year-end, across-the-board sequestration of any spending category with total enacted appropriations exceeding the cap (unless Congress passed a law raising the cap levels or canceling the sequestration, which could not be prevented without constitutional reforms).

Some flexibility was allowed. According to the Congressional Research Service (CRS), “the discretionary spending limits could be adjusted to take into account changes in budgetary concepts and definitions, changes in inflation (for FY1993 and FY1994), changes in estimates of credit subsidy costs to allow for specified allowances, such as emergency appropriations, IRS tax compliance funding, and debt forgiveness for Egypt and Poland.”[13]

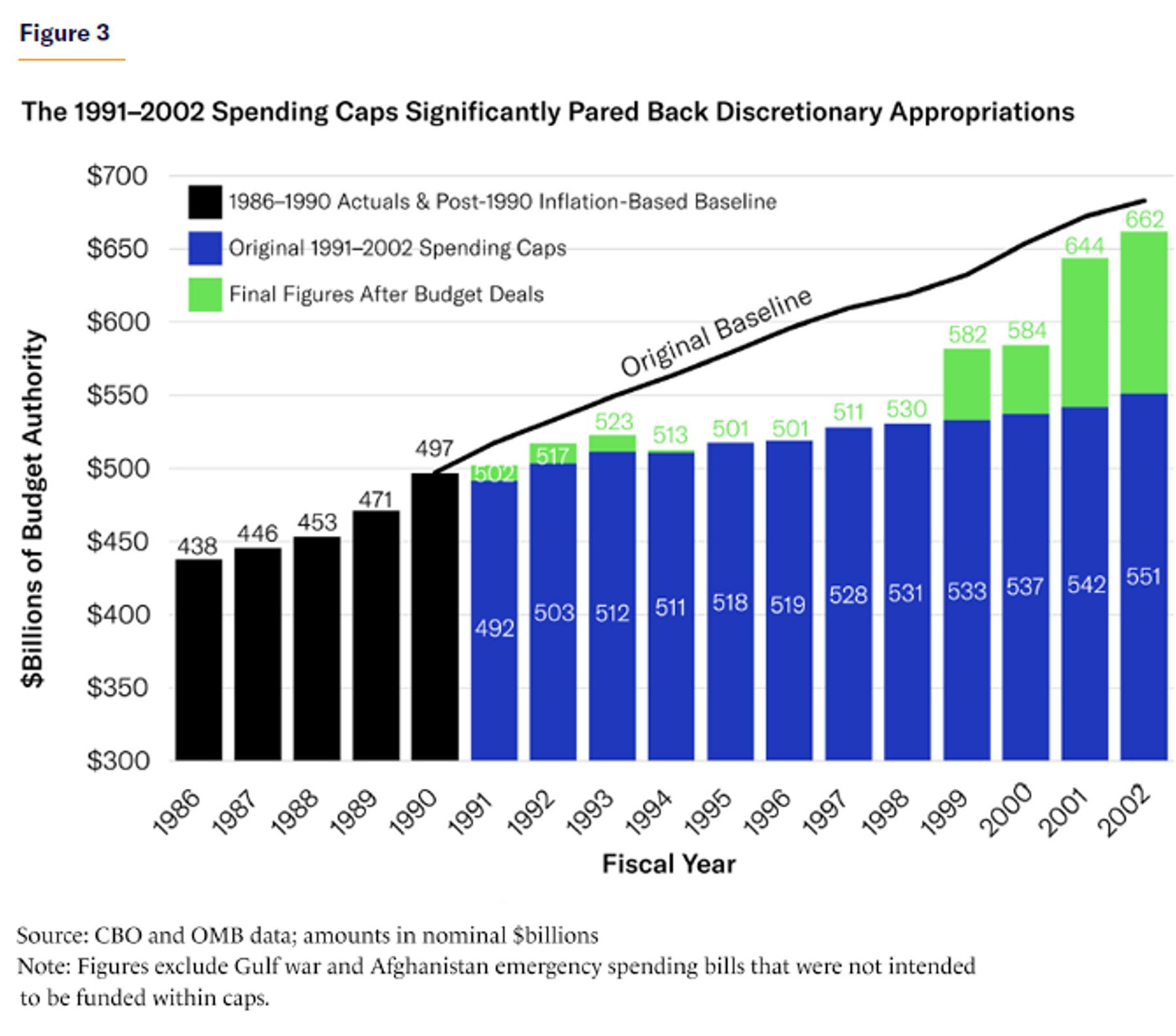

BEA caps were originally intended to limit spending from 1991 through 1995. However, Congress and President Bill Clinton extended them in 1993 (through 1998), and again in 1997 (through 2002), with evolving sub-caps for defense, nondefense, violent-crime reduction, conservation, highways, and mass transit. Over 12 years, the cap levels allowed for average spending growth of 1% annually, during a period in which yearly inflation was forecast to top 3%. Defense appropriations were capped at a slower growth rate than nondefense appropriations in response to the collapsing Soviet empire.

Generally, the caps succeeded from 1991 through 1998. During those eight years, lawmakers exceeded the cumulative $4,113 billion in capped spending by just $132 billion, or 3%. Of that overage, $59 billion went for early 1990s Gulf War emergency spending, $39 billion went toward other emergencies, and the rest consisted of allowable cap adjustments for aforementioned items such as credit reestimates and IRS funding.[14]

Emergency spending was a major issue for the designers of BEA. The earlier GRH law had induced the Office of Management and Budget (OMB) to impose a near-“zero-tolerance” policy on emergency spending requests.[15] Republicans were able to secure Democratic support for BEA in part by promising that emergency spending would be automatically exempt from all budget caps and sequestrations and that the emergency designation would be applied when necessary. Still, both the president and Congress would have to certify the emergency designation.[16] Economists Veronique de Rugy and Allison Kasic note that, in 1991, OMB tried to define “emergency” spending as meeting all of five criteria: necessary, sudden, urgent, unforeseen, and temporary. However, no such definition has ever been statutorily or administratively implemented.[17]

That said, Congress and the White House—under presidents of both parties—were careful not to abuse the emergency designation. Of the $138 billion in emergency supplemental appropriations enacted during the 1990s, $52 billion was immediately offset by rescinding other spending.[18] Excluding Gulf War emergency appropriations, the majority of 1990s emergency spending was offset, at times with rescission provisions even larger than the accompanying emergency expenditure—although some of these rescissions were of budget authority that was never going to be spent. Even without strong statutory limitations, a culture of restraint prevented abuse of the emergency loophole.

For those first eight years of discretionary caps, total appropriations expanded by an average of less than 1% annually. This progress stalled beginning in 1999, after the unanticipated balanced budget removed the urgency for spending restraint. In 1999 and 2000, Congress abused the emergency spending rules by using loopholes such as “advance appropriations, obligation and payment delays, and specific legislative direction for scorekeeping”[19] to exceed the caps by 9%.[20] Congress and the White House even went so far as to claim funding for the 2000 census to be an unforeseen emergency—despite the decennial census being a predictable (and constitutionally mandated) constant every 10 years since 1790.[21]

Eventually, Congress dropped the charade and simply voted to bust the caps by 18% in 2001 and then 24% in 2002.[22] The caps were ultimately cast aside due to a balanced budget, spending restraint fatigue, and—as a result—simply being too tight for the evolving political moment. After mercifully allowing the now-irrelevant caps to expire at the end of 2002, President George W. Bush and Congress continued the discretionary spending spree with annual growth rates as high as 15%.

Despite their eventual abandonment, the 1991–2002 discretionary caps were largely successful (Figure 3). During a 12-year period in which merely limiting discretionary spending growth to the inflation rate (which is the CBO baseline growth rate) would have produced a cumulative $7,208 billion in discretionary appropriations, the actual total (even with emergency spending) came in at $6,721 billion. That is $487 billion in savings relative to the baseline (which equates to $1.5 trillion in today’s GDP).

The main failure was that—after annual spending fell as low as $98 billion below the original inflationary-growth baseline—the post-1998 spending spree pushed the final 2002 appropriations $52 billion above that baseline ($5 billion, excluding 9/11 emergency funding). Still, total discretionary appropriations between 1990 and 2002 fell from 8.4% to 6.8% of GDP, bottoming out at a post–World War II low of 5.8% of GDP along the way.

Nearly freezing discretionary appropriations for most of a decade represented a rare achievement for fiscal restraint. Ultimately, lawmakers were aided by drastic defense savings brought on by the collapse of the Soviet Union and the end of the Cold War. Between 1990 and 2002, nondefense discretionary appropriations expanded from $402 billion to $609 billion (adjusted for inflation), remaining close to 3.2% of GDP. By contrast, inflation-adjusted defense appropriations collapsed from $633 billion to $472 billion between 1990 and 1997, before rebounding to $588 billion in 2002 after the 9/11 attacks. Overall defense spending as a share of the economy—which had already fallen from 6.9% to 5.2% between 1983 and 1990—collapsed further, to 3.0% by 2000, before nudging upward to 3.3% after the 9/11 attacks.

Budget Control Act: 2012–21

The 2002 expiration of discretionary spending caps brought an unrestrained spending spree. Between 2003 and 2011, Congress hiked discretionary spending by an average of 5.9% annually.[23] This pushed total discretionary appropriations up to 8.5% of GDP by 2010—exceeding the 1990 level that motivated the earlier round of spending caps.

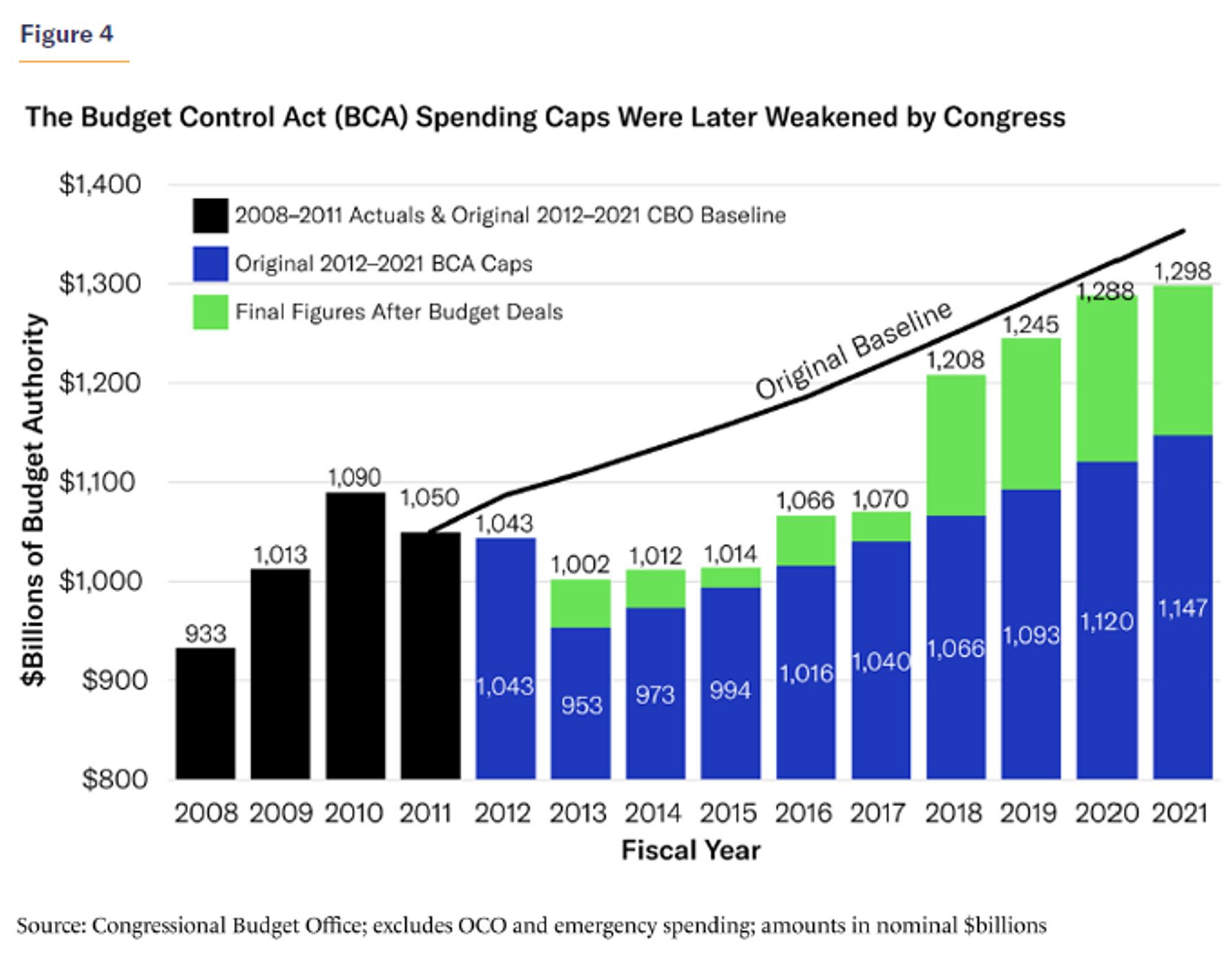

In response to surging spending and deficits, President Barack Obama and Congress in August 2011 enacted the bipartisan Budget Control Act (BCA). BCA imposed spending caps that were much more straightforward than the law’s predecessors. Rather than cap spending for three to five years at a time with modest flexibility for automatic readjustments, BCA set specific cap levels covering 2012–21. Sub-caps were set for security and non-security spending. As in the 1990s, the new caps would be enforced by a congressional point of order, and any enacted overages would trigger an automatic sequestration returning appropriations to their capped levels.

Cap levels were initially intended to reduce discretionary spending by $841 billion over the decade, relative to a baseline of growth at the rate of inflation. However, BCA also created a Joint Select Committee on Deficit Reduction (“Super Committee”) to identify and recommend an additional $1.2 trillion in 10-year savings across the government. The deadlock of the Super Committee automatically triggered an additional $815 billion in spending cap reductions over the decade (plus some mandatory program savings).[24]

BCA’s spending targets were ambitious. The caps mandated an immediate 8.6% (or $90 billion) reduction in 2013 appropriations from the previous year’s level. From there, the cap levels would grow by roughly 2.3% annually (close to the expected inflation rate) through 2021. Overall, the caps envisioned a reduction in 10-year discretionary spending by $1,656 billion (or 13.7%) relative to the baseline level.[25]

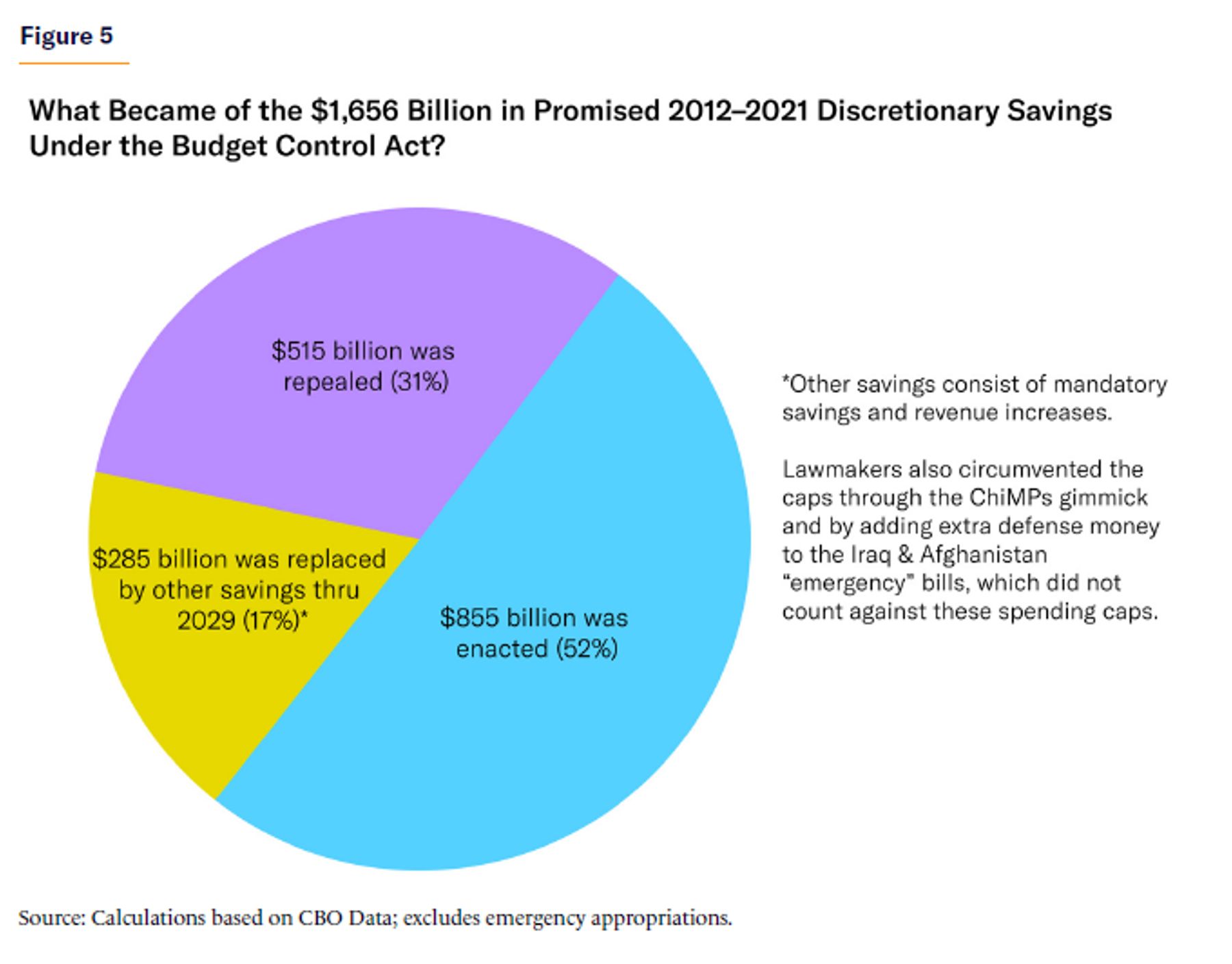

On the surface, the caps were modestly successful. Regular discretionary appropriations between 2012 and 2021 came in $855 billion below the inflation-growth baseline—or roughly half the promised savings. However, as shown in Figure 4, Congress never came close to meeting the caps in any year after 2012. The promised $90 billion spending cut for 2013 was quickly halved. Later bipartisan budget deals added between $19 billion and $50 billion to annual 2014–17 cap levels. By 2018, lawmakers essentially had given up on BCA: they hiked the caps by $143 billion (13%), and then renewed (and further hiked) these inflated levels for the final three years. Altogether, Congress hiked the spending caps by $801 billion over the life of BCA (of which $285 billion was offset with new mandatory program savings scheduled to occur through 2029).[26]

While BCA’s ambition was laudable, its targeted spending levels were never realistic (Figure 5). The requirement of an initial 8.6% cut in discretionary appropriations, affecting areas such as K–12 education, health research, and veterans’ health care, was never going to survive the full appropriations process. And busting the first-year cap all but guaranteed that each subsequent year’s cap would also be raised to avert a sharp ratchet down of spending to BCA’s now-abandoned original path.

The limited savings that BCA would have produced were further negated by the enactment of $2 trillion in emergency and other cap-exempt spending during these 10 years. The largest portion of this spending, $880 billion, was for Overseas Contingency Operations (OCO), primarily related to Iraq and Afghanistan. Granted, OCO had been consistently funded on a separate emergency basis since 2001, and BCA cap levels were never intended to accommodate OCO’s approximately $100 billion annual cost. However, deliberately exempting OCO from BCA caps shielded these costs from budget discipline, and eventually turned OCO into a slush fund allowing Congress to move regular defense costs outside the budget caps, which, in turn, created space for more domestic spending.[27] A more responsible approach would have been to set higher BCA cap levels and require them to accommodate OCO.

Another gimmick—Changes in Mandatory Programs, or “ChiMPs”—served as a loophole to circumvent the budget caps. ChiMPs allowed Congress to cut mandatory spending and then apply those savings to additional discretionary appropriations. While conceptually fair, two aspects of the rules turned them into a gimmick. First, the mandatory “cuts” were often rescissions of budget authority that would never have been spent anyway, such as expired funding or disaster assistance that was no longer needed. Second, merely delaying—not canceling—a single-year mandatory expenditure indefinitely allows Congress to hike discretionary spending repeatedly for as long as the delay is in force. For example, delaying a one-time $5 billion mandatory expenditure for a decade would allow $5 billion in additional discretionary spending every year for that decade, for a total expenditure of $50 billion (plus the eventual mandatory expenditure). During the 2010s, ChiMPs typically allowed $20 billion in extra discretionary appropriations per year without producing legitimate mandatory spending offsets.[28]

Other emergency appropriations included pandemic-related costs ($686 billion), traditional emergency and disaster relief costs ($339 billion), and—once again—the 2020 decennial census ($2.5 billion), which was anything but an unanticipated emergency.[29] While much of this supplemental spending was justified, the emergency and disaster relief costs far exceeded 1990s levels and were often abused as a slush fund to evade spending caps. The 1990s culture of minimizing and even offsetting emergency spending became a distant memory.

Despite widely missing their statutory targets, BCA caps successfully trimmed discretionary appropriations as a share of GDP from 7.9% in 2011 to 6.3% in 2021 (excluding short-term emergency pandemic spending). The $855 billion savings (relative to the inflation-growth baseline) must be adjusted to account for “emergency” spending abuses. Yet compared with annual discretionary hikes averaging 5.9% during the uncapped 2003–11 period, the 1.8% average annual increase between 2012 and 2021 represented significant progress.[30]

As soon as BCA officially expired, however, Congress quickly hiked “regular” discretionary appropriations by 13% in 2022 and by 9% in 2023. This prompted the 2023 Fiscal Responsibility Act, which is expected to roughly freeze or slightly increase nonemergency appropriations in 2024 and 2025.[31]

Lessons from Past Spending Caps

Discretionary Caps Have Successfully Constrained Spending

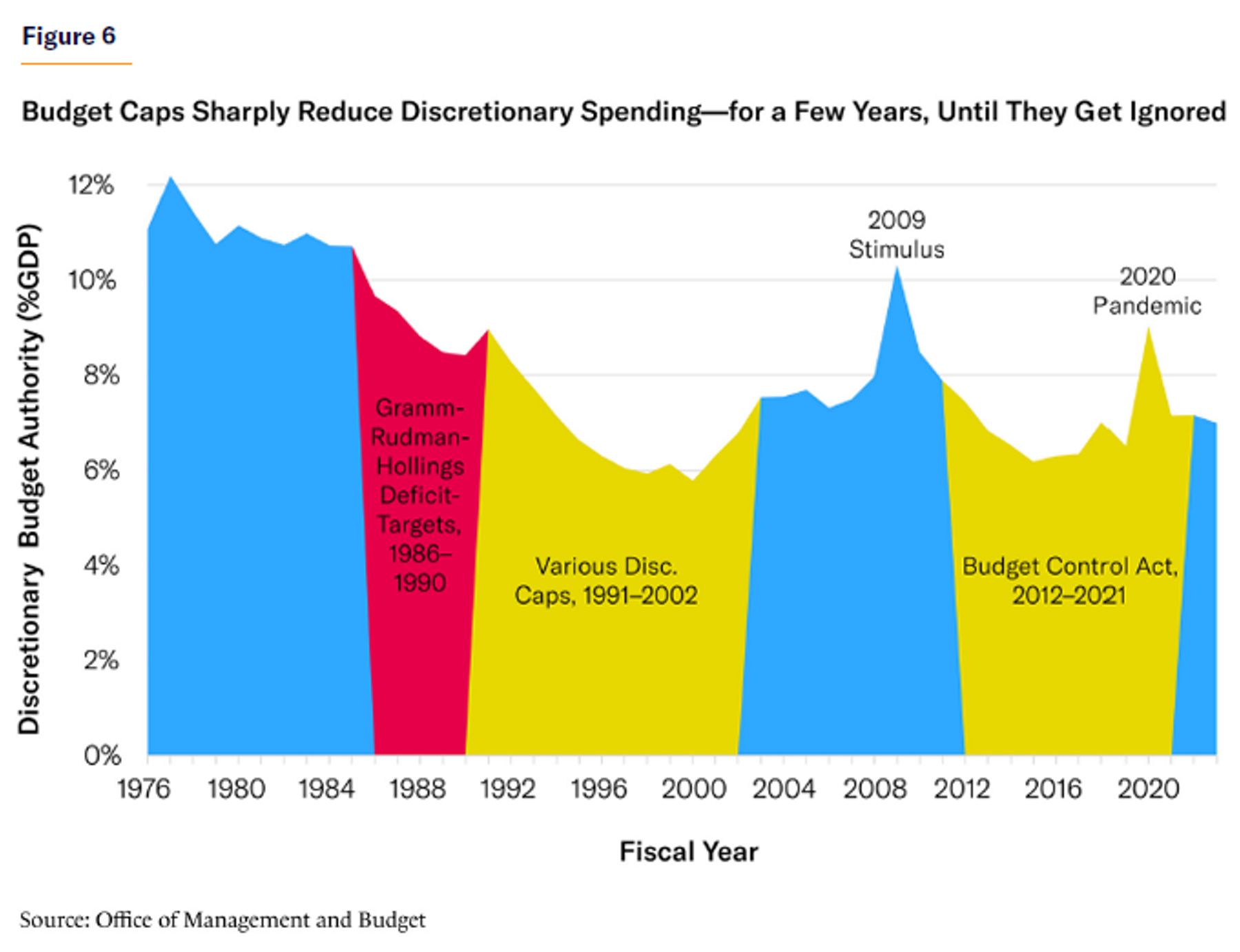

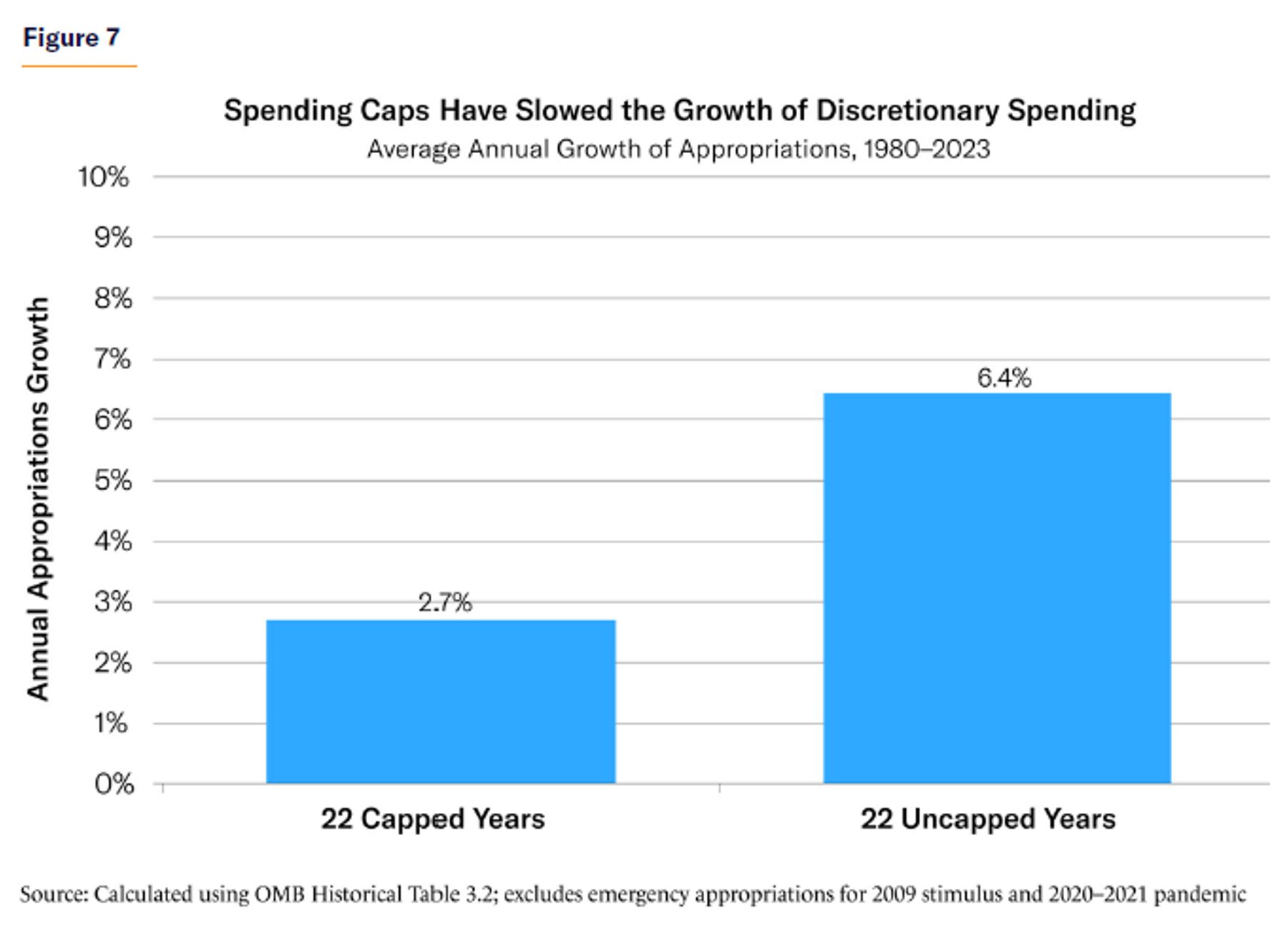

In the 44 years between 1980 and 2023, discretionary spending was statutorily capped for 22 years and uncapped for 22 years (Figure 6). Capped years saw appropriations expand by an average of 2.7%, versus 6.4% in uncapped years. Total discretionary appropriations averaged 6.7% of GDP in capped years and 8.8% of GDP in uncapped years[32] (Figure 7).

Spending Caps Should Be Realigned Every Few Years

The 1990 spending caps were rewritten and extended in 1993 and again in 1997. Relatively frequent adjustments meant that the caps had always been recently enacted, which gave them credibility and ensured that they matched the political moment. These caps also contained occasional flexibility to adjust for swings in inflation or congressional scoring reestimates, allowing them to adapt to changing conditions that could otherwise motivate a full breach. By contrast, the 2011 BCA imposed tight spending caps for a full decade and allowed less flexibility than earlier caps. Those cap levels soon became unrealistic and, over time, were largely discarded.

Bipartisanship Requires Defense and Nondefense Sub-Caps

In an ideal world, each year’s discretionary appropriations would be subject to a single cap, giving lawmakers maximum flexibility to meet that target. But in reality, defense and nondefense sub-caps have proved vital to assure both parties that their priorities will be protected and not easily raided by the other party down the road. Additionally, annual partisan brawls over defense and nondefense levels would delay the appropriations process and would put pressure on lawmakers to lift the caps in order to solve these distributional fights.

Less useful were past sub-caps covering spending on international spending, veterans, highways, and the opioid crisis. Splitting out those categories needlessly micromanages Congress and limits its ability to trade off competing priorities. Those categories also lack the natural partisan split that necessitates a long-term pre-negotiation to maintain bipartisan credibility.

More broadly, multiyear spending caps must be designed with bipartisan input if they are to be sustained across different Congresses and presidential administrations. The cap levels of the 1990s and BCA were broadly bipartisan, which prevented Senate filibusters and a repeal of the caps resulting from changes in party control.

Caps Should Be Flexible but (Relatively) Unbreakable

Cap enforcement is a challenging needle to thread. If caps are too tight and rigid, they will be repealed. If they are too loose and have countless off-ramps, they will cease to limit spending. The optimal solution is a bend-but-not-break approach that keeps caps realistic and flexible yet difficult to evade entirely. This means imposing caps that cover as many discretionary appropriations as possible (including OCO spending and average levels of disaster aid) and banning fake offsets such as ChiMPs and rescissions that do not save money. It also obviously requires not repeating the handshake agreement to evade the 2024 and 2025 caps for additional regular spending.

At the same time, caps should be set at reasonable levels and should include 1990s-style provisions incorporating automatic cap adjustments for major changes to inflation, scoring reestimates, and possibly even recessions. These changes will accommodate lawmaker pressure to respond to temporarily expensive events without completely busting the caps and passing even larger spending expansions.

Weak Emergency Limits Can Be a Massive Loophole

Lawmakers must be able to flexibly respond to emergencies without creating a clear loophole to evade budget caps for regular spending. While no reforms are foolproof, Congress should codify the definition of emergency spending, which requires meeting all five criteria of necessary, sudden, urgent, unforeseen, and temporary.

Building on past reforms, Congress could require a simple majority vote for annual disaster assistance not exceeding the average level of the past 10 years (disregarding the highest and lowest year), with the additional option of pre-funding a discretionary emergency fund (within capped appropriations) that can roll over into future years. Any additional emergency or disaster funding that is not offset should be subject to a point of order that requires a two-thirds House and Senate vote to waive. This bar is higher than the common three-fifths point-of-order thresholds, although legitimate emergencies—that meet all five criteria—should be able to clear even this hurdle, especially if the caps already allow for modest automatic readjustments to inflation and even recessions. The alternative of essentially trusting lawmakers not to abuse an easier emergency designation has proved ineffective.

Successful Spending Caps Should Be Uncomfortable but Not Painful

This lesson can be broken into three sequential parts:

- Overly tight caps will be easily discarded. Because enforcement mechanisms are so weak, spending caps can be only as effective as they are credible and realistic. Caps cannot force Congress to commit political suicide or impose wildly unpopular spending cuts. Cap levels that no longer reflect the political moment have been easily adjusted or repealed in any future spending bill. In short, caps can enforce Congress’s will to constrain spending, but they cannot impose discipline on a Congress that lacks any such will.

Realistic spending caps should provide a plausible framework that helps lawmakers balance competing spending priorities. They are most effective at keeping the growth of appropriations at a steady yet modest rate, which requires mild discomfort from both sides.

There are two ways in which spending caps can be unsustainably tight. First, deep and immediate first-year reductions are typically pared back, which, in turn, forces up the cap levels for all subsequent years to avoid a downward ratchet. Second, caps can also lead to an unsustainably low absolute level of spending: the most dramatic cap rewrites since 1990 have taken place shortly after discretionary appropriations fell below 6.3% of GDP. Which relates to the second part of this lesson: As the caps lose their efficacy… - Expiring or discarding of spending caps brings mammoth spending binges. Building on the lesson above, unrealistically tight spending caps are self-defeating because their inevitable abandonment often induces Congress to go all in, with appropriations expansions exceeding 10%. When Congress finally gave up on the 1991–2002 spending caps, it raised the cap levels by 18% in 2001 and 24% in 2002. When the caps officially expired in 2003, Congress immediately hiked appropriations by 16%. Similarly, when Congress gave up on BCA in 2018, it hiked the caps 13% over their original level, and when the caps officially expired in 2022, “regular” appropriations immediately jumped by another 13%.

In these situations, Congress should have opted for looser spending caps that matched the political moment, rather than disregard tight caps and pass double-digit expansions. After all, even capping appropriations expansions as high as nearly 4% can still stabilize or reduce discretionary spending as a share of the economy. The only capped periods in which appropriations rose as a share of the economy were 1991 (due to Gulf War emergency appropriations), the final four years of the 1991–2002 period (after the deficit vanished), and the final four years of the 2012–21 period (when tighter caps finally became unbearable for Congress and the White House).[33] The effect of those few mammoth increases is that… - A small number of spending-binge years account for most of the long-term spending increases. From 1990 through 2023, annual discretionary appropriations increased by $788 billion (adjusted for inflation). More than 80% of that long-term increase—$637 billion in total—took place in just three years: 2003, 2022 (the first years after statutory caps expired), and 2018 (when BCA caps finally proved too tight even for smaller tweaks). Appropriations in the other 31 years fluctuated (due largely to more variable emergency and OCO costs) but averaged an inflation-adjusted annual growth of just $5 billion.

This experience suggests that budget discipline is endangered less by loose cap levels than by the resulting spending binges after Congress frees itself from caps completely. Even a one-year $50 billion discretionary spending hike pushes up the baseline spending level for all future years by $50 billion (plus inflation). And since Congress is very rarely able to reduce appropriations levels, the most effective way to constrain appropriations is to avoid large expansions in the first place.

Threading the Needle: Designing Caps Moving Forward

The 2025 expiration of the new two-year caps will likely bring a debate to extend multi-year caps.Lawmakers will have an opportunity to design the next round of spending caps using the lessons from the past. Ambitious longer-term spending caps are ultimately meaningless to the extent that their promised savings exceed the amount that current and future Congresses can reasonably deliver. In fact, ambitious spending caps have proved to backfire when canceled by a future Congress that subsequently hikes appropriations by 10% or more. Fiscal sustainability is better served by Congress holding itself to caps allowing 3% annual growth rather than canceling caps requiring 1% growth.

Since the fall of the Soviet empire (which significantly brought down defense spending), discretionary appropriations have generally fluctuated between 6% and 9% of GDP, with a relatively even split between defense and nondefense appropriations. The current level of appropriations is 6.6% of GDP. Given that mandatory spending as a share of the economy will continue to rise substantially, it is reasonable to keep discretionary appropriations limited to their current share or even decrease them closer to 6% over the long term.

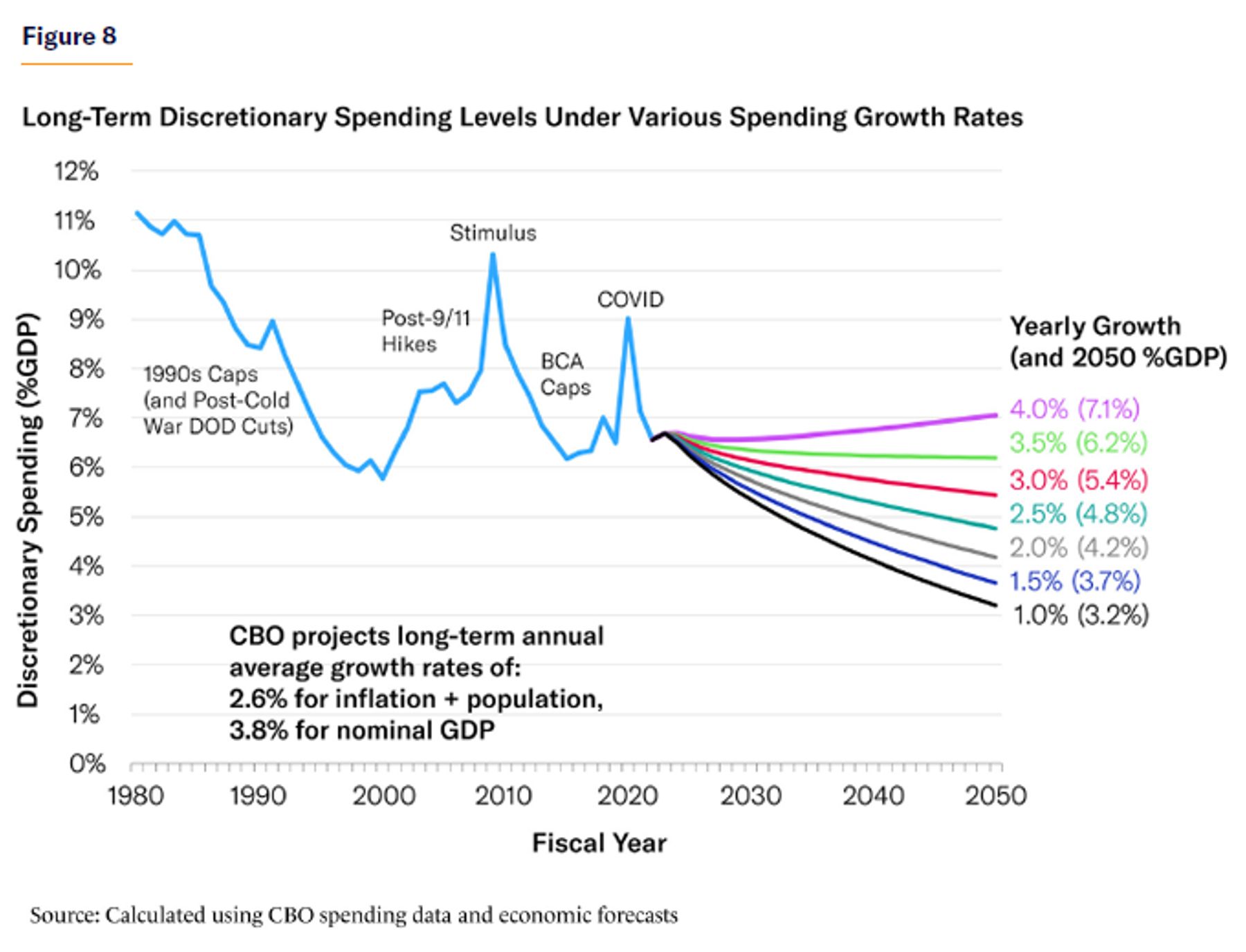

The encouraging news is that, as shown in Figure 8, such a target does not require overhauling government operations. Discretionary spending as a share of GDP will decline indefinitely as long as it grows slower than the nominal GDP—which is forecast to grow annually by 4.1% over the next decade and 3.8% over the next three decades.[34] Thus, even caps allowing 3.5% annual growth—if followed by Congress—would gradually reduce discretionary appropriations to 6.2% of GDP by 2050. More ambitious caps allowing 2.5% annual growth would push discretionary appropriations down to 5.7% of GDP within a decade and 4.8% by 2050.

History suggests that discretionary appropriations may not be sustained below 6% of GDP. Defense appropriations have not fallen below 3% of GDP in the post–World War II era, and the few nondefense dips below that threshold were quickly reversed. Nondefense appropriations will continue to face substantial upward pressure from veterans’ health costs, which have expanded 10% annually since 2018 and constitute the largest portion of the nondefense category. Nor are future lawmakers likely to dramatically slash funding for popular spending such as K–12 education, health research, highways, disaster aid, national parks, environmental remediation, and housing. A more realistic long-term path would entail Congress limiting appropriations to the inflation rate plus population growth—which is estimated around 3% annually over the long term—perhaps by balancing larger expansions for veterans’ health with more oversight and reform of remaining programs. Even that outcome would reduce discretionary appropriations to 6.0% of GDP in a decade and to 5.4% by 2050.

These projections reenforce the earlier point that—at least to a reasonable degree—the specific cap level is less important than ensuring that Congress holds to those caps and avoids an uncapped spending binge. Even occasional short-term appropriations spikes in the wake of major emergencies can be accommodated as long as they prove temporary and spending caps continue to push the long-term appropriations path in a responsible direction.

Thus, long-term discretionary caps set at annual growth rates of perhaps 3.0%–3.5% may thread the needle of political sustainability and long-term modest reductions in appropriations as a share of the economy.

Beyond the specific cap levels, successful appropriations caps should:

- Require legislative renewal every three to five years. Cap levels must reflect current political and economic realities. Past caps that were enacted more than five years earlier and that no longer reflected the current challenges were easily disregarded by Congress. Lawmakers should follow the 1990s model by rewriting the caps every few years.

- Allow automatic cap adjustments for significant inflation, scoring reestimates, and allowances. At various times in the 1990s, caps were automatically adjusted for major changes to inflation, scoring conventions, and other factors such as IRS funding that bring in significant new tax revenues. Renewing such flexibility would protect the caps from being canceled completely. Lawmakers could automatically hike caps if the inflation rate significantly exceeds the rates assumed at the time that the cap levels were set. Caps could also temporarily rise if the economy is declared to be in a recession (which would likely require relief spending).[35]

- Include defense and nondefense sub-caps. Bipartisan credibility requires assuring both Republicans and Democrats that their priority spending category will not be raided by the other party down the road to meet the caps. Sub-caps have encouraged a smoother appropriations process and avoided the defense-versus-nondefense impasses that could doom the caps altogether. At the same time, however, sub-caps for other narrow spending categories are not necessary to maintain cross-partisan cooperation and should be avoided to maintain flexibility.

- Enforce cap levels better. Lawmakers could create a point of order against legislative language that appropriates above the spending cap, raises the cap level itself, or cancels the automatic sequestration of an appropriations breach. Requiring a two-thirds vote in the House and Senate to waive this point of order would be ideal, although three-fifths requirements are more common in the Senate, and the House typically (and pointlessly) requires only a bare majority to waive a point of order. The House Rules Committee’s regular practice of waiving points of order before they can even be brought on the House floor could also be banned with respect to spending cap enforcement.

- Ban ChiMPs. This gimmick allows lawmakers to appropriate above the budget caps by claiming offsetting mandatory spending cuts that are usually fake. Congress should ban ChiMPs, or, at minimum, require that they arise from real, CBO-scored, mandatory outlay reductions (rather than mere delays).

- Address emergency spending better. Per the recommendations in the previous section, Congress should codify the definition of emergency spending and require a strong supermajority vote to override a point of order against non-offset emergency spending that exceeds regular disaster funding levels and exhausts any additional discretionary emergency fund.

Conclusion: Caps Are Important for Spending Restraint

Discretionary spending is not the lead driver of annual budget deficits, which are projected to surge past 10% of GDP in the coming decades. However, in the absence of statutory caps, Congress has regularly expanded discretionary appropriations at rapid rates that threaten to significantly deepen the long-term fiscal gap. Successful discretionary caps are less about reducing appropriations than preventing unaffordably large appropriations expansions.

Statutory caps in place during 1991–2002 and again during 2012–21 successfully reduced discretionary appropriations as a share of the economy. However, as the political environment evolved, tighter long-term caps were easily discarded by Congress and replaced with double-digit expansions. Additionally, lawmakers have already pledged to evade recently enacted caps for 2024 and 2025. The important lesson for policymakers is that spending caps can enforce Congress’s will for spending restraint—but they cannot force huge spending cuts where no congressional will exists.

Moving forward to the 2025 caps debate, successful statutory caps should be reasonably short- or medium-term, flexible to economic conditions, and modestly uncomfortable without being too tight. At the same time, caps should contain significant enforcement mechanisms to protect their integrity. The good news for lawmakers is that even caps allowing appropriations to rise as much as 3.5% annually would still gradually reduce long-term discretionary spending as a share of the economy, while providing a framework for lawmakers to trade off competing spending priorities. As long as they are not unrealistically ambitious, discretionary caps can be a vital component of long-term deficit reduction.

About the Author

Brian Riedl is a senior fellow at the Manhattan Institute, focusing on budget, tax, and economic policy. Previously, he worked for six years as chief economist to Senator Rob Portman (R-OH) and as staff director of the Senate Finance Subcommittee on Fiscal Responsibility and Economic Growth. Riedl also served as a director of budget and spending policy for Marco Rubio’s presidential campaign and was the lead architect of the 10-year deficit-reduction plan for Mitt Romney’s presidential campaign.

During 2001–11, Riedl served as the Heritage Foundation’s lead research fellow on federal budget and spending policy. In that position, he helped lay the groundwork for Congress to cap soaring federal spending, rein in farm subsidies, and ban pork-barrel earmarks. Riedl’s writing and research have been featured in the New York Times, Wall Street Journal, Washington Post, Los Angeles Times, and National Review; he is a frequent guest on NBC, CBS, PBS, CNN, Fox News, MSNBC, and C-SPAN.

Riedl holds a bachelor’s degree in economics and political science from the University of Wisconsin and a master’s degree in public affairs from Princeton University.

Endnotes

Photo: Douglas Rissing/iStock

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).