The Overextended Retirement State

Photo: Willowpix / E+ via Getty Images

Executive Summary

The welfare state is supposed to redistribute funds from times of plenty to times of need, as well as from rich to poor. That is why the nation’s most generous publicly financed benefits are reserved for seniors, who have less capacity to earn money and who face higher health-care costs, while taxes are concentrated on working-age households.

But working-age Americans, despite typically earning more income than seniors, also bear substantial child-rearing costs, have rarely paid off their mortgages, and must spend more to live near good jobs and schools. As a result, this group now has lower material standards of living than retirees: they have less living space, are more likely to go without meals or health care, are less able to pay utility bills, are more likely to live in pest-infested houses, and are more likely to live where they feel threatened by crime. This also means that families have less money to invest in their children.

The U.S.’s increasingly costly entitlements for middle-class retirees result in substantial redistribution away from young workers. If this system is not reformed soon, major tax increases on workers at all income levels will be required, which will only exacerbate redistribution away from age groups who are worst off.

Why Redistribute to the Elderly?

Economist Nicholas Barr has argued that the welfare state serves two main functions: First, as a “Robin Hood”, redistributing from the rich to the poor; second as a “piggy bank,” redistributing income from times of plenty to times of need over the life cycle.[1] The second function is necessary, Barr argues, because “even if all poverty and social exclusion could be eliminated, so that the entire population were middle class, there would still be a need for institutions to enable people to insure themselves and to redistribute over the life cycle.” He acknowledges that while “private institutions are often effective” at fulfilling this purpose, they “face predictable problems, which require government intervention.”[2] The most predictable and long-lasting of these problems is old age.

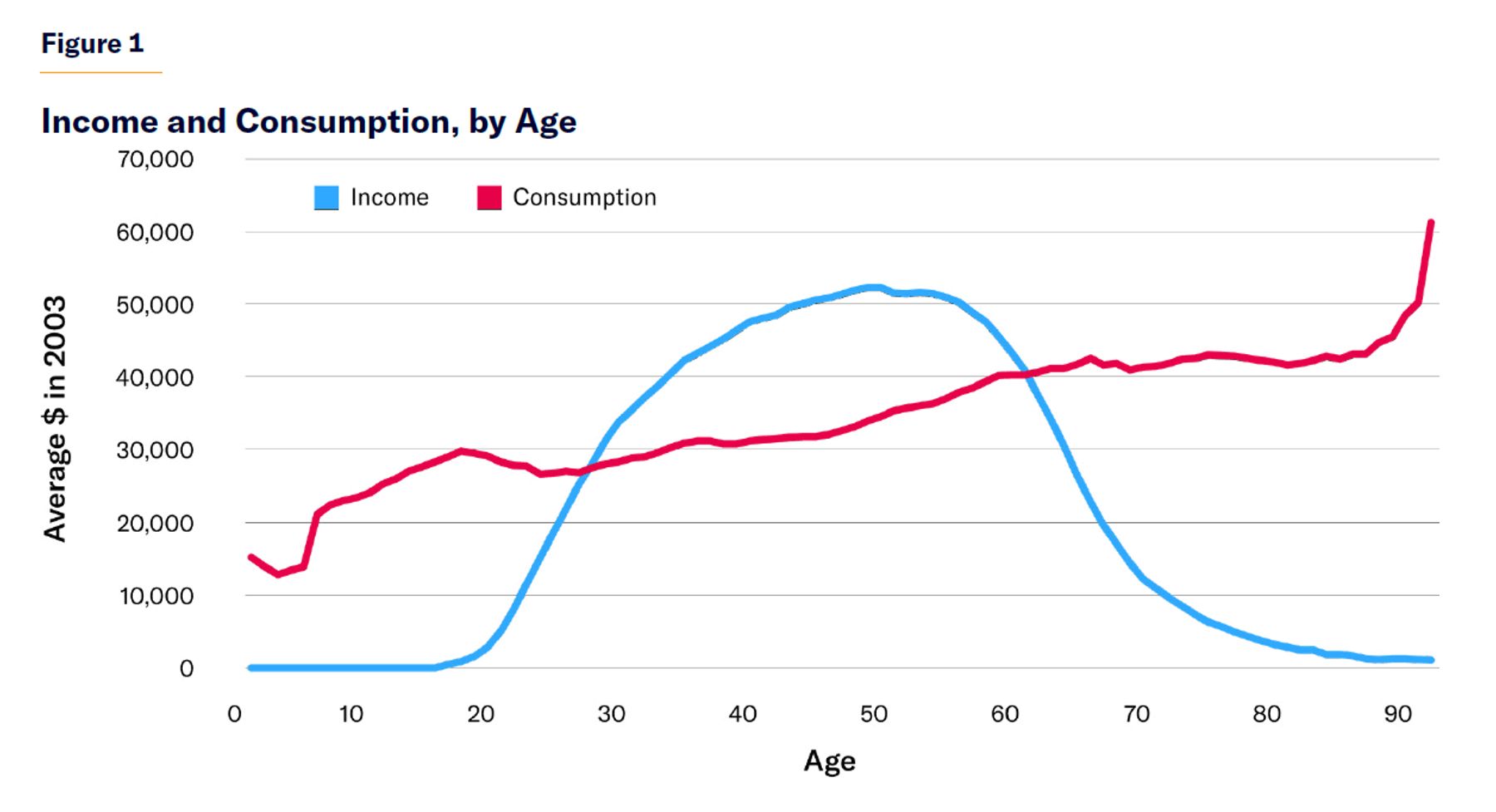

Although consumption increases gradually over the life cycle, personal income rises rapidly as individuals’ careers get going—before falling sharply as they retire from employment (Figure 1). On average, hourly wages of full-time workers increase steadily up to age 40, at which point they reach a plateau. But as individuals age, their ability to work declines. Labor-force participation begins to decrease from age 50 and does so rapidly after the age of 60.[3]

Urbanization in the late 19th century meant that the elderly could no longer simply be cared for by relatives on family farms but needed to pay rent and other bills to live independently.[4] At the same time, longevity was increasing past the period of active work, which expanded the number of seniors living in poverty.

To remedy this problem, Progressive Era reformers called for the establishment of public pension systems. They argued that households would fail to set aside adequate funds for retirement because of the pressure of more immediate concerns and because of uncertainty about the duration of their longevity into old age. The reformers suggested that this uncertainty also made it difficult for private financial institutions to sell annuities at prices that would be attractive to those with both short and long prospects of longevity into retirement. Furthermore, they suggested that household savings needed to be protected from scams and the risk of failed investments.[5]

The Great Depression provided additional justifications for publicly funded retirement systems, including a desire to clear the workforce of less productive older workers and the hope that bolstering the purchasing power of the elderly would help pull the economy out of the slump.[6] Legislators believed that the establishment of federal pensions would help relieve states of the need to fund aid for the elderly poor, most of whom, at the time, did not receive pensions from previous employers and had not accumulated substantial assets for retirement.

As seniors already have much less capacity for employment, providing cash benefits to them does more to reduce poverty and less to crowd out work than it does for other age groups. Since even affluent retirees have low earnings, limiting eligibility for public old-age pensions with income tests would save little money. Similarly, asset tests save little, as they can be evaded by forgoing savings, spending down assets, or diverting investments abroad.[7]

When Social Security was first established, there was a close link between each generation’s old-age-insurance benefits and their previous payroll tax contributions. But after this link was destroyed by rapid wartime inflation, Social Security was repackaged as a scheme promising a return on investment that no honestly managed private business could match.[8] So long as wages and population grew faster than interest rates, economist Paul Samuelson assured policymakers, a pay-as-you-go pension system would be able to provide each successive generation with benefits that were larger than what they had previously contributed in payroll taxes.[9]

The shift to full pay-as-you-go financing allowed funds to be redistributed from birth cohorts whose peak earning years were blessed with favorable rates of demographic and economic growth to those who were less fortunate—as well as from wealthier generations to their poorer predecessors.[10] Furthermore, pay-as-you-go pension systems have been popular with workers (who typically have their own children to raise), as they spread out the burden of supporting parents who live longest into old age—thereby providing personal freedom and independence to both generations.[11]

After World War II, reformers began to focus on rising health-care costs. As medical capabilities and hospital expenses surged, the tax-preferred expansion of employer-sponsored benefits brought health-insurance coverage to the bulk of U.S. workers. But this meant that retirees were left behind—even though the elderly faced higher medical bills and had lower incomes with which to pay them. Hospitals struggled to finance treatment for uninsured seniors, and business- or family-purchased plans were unable to fill the gap. Congress therefore established Medicare to cover the bulk of medical costs incurred by seniors.

As people age, they become increasingly likely to be widowed and more likely to need assistance with basic daily living chores, such as bathing, dressing, and preparing meals. The federal government has therefore steadily expanded Medicaid funding for nursing homes and long-term services to help frail elderly Americans live in their own homes.

The Redistribution Balance Sheet

Despite its supposed purpose of redistributing from the better-off to worse-off, the American welfare state redistributes much more to middle-class retirees than it does to the poor.

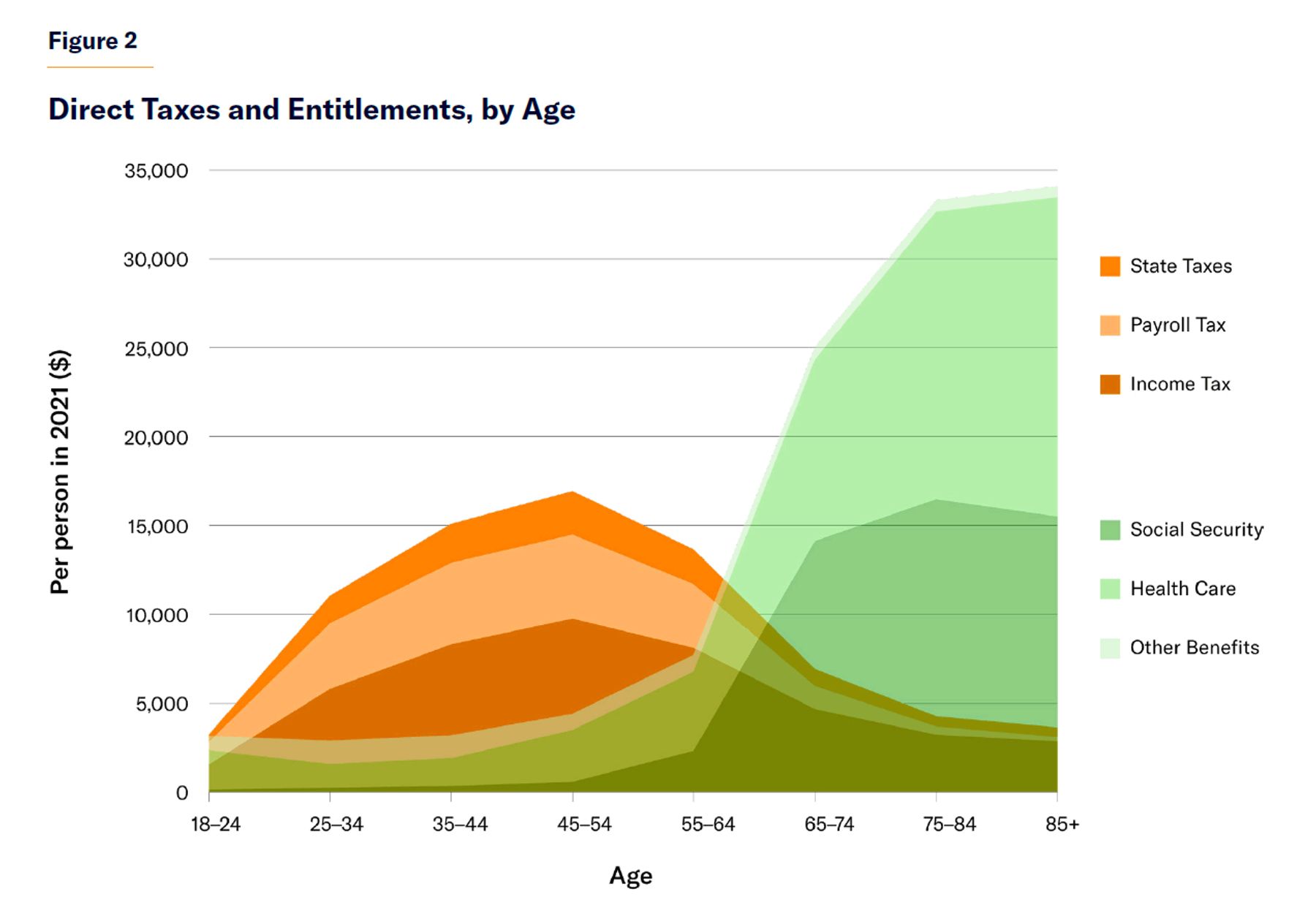

In 2022, 66% of U.S. entitlement spending went to the 17% of the population aged 65 and older. That age cohort contributed only 11% of U.S. direct tax revenues (Figure 2).[12]

Social Security and Medicare expenditures on the elderly dwarf all other publicly funded welfare benefits (Table 1). This is partly because Social Security and Medicare beneficiaries each receive substantially more aid than recipients of other benefits. But it is primarily because 88% of seniors are eligible for Social Security and Medicare, whereas only 4% of working-age Americans are eligible for these programs (due to disability).[13]

Table 1

Benefits Received per Person in Age Cohort, 2021–22 ($)

| 18–24 | 25–34 | 35–44 | 45–54 | 55–64 | 65–74 | 75–84 | 85+ | |

| Social Security | 131 | 236 | 356 | 587 | 2,313 | 14,128 | 16,480 | 15,506 |

| Medicare | 59 | 127 | 328 | 898 | 2,037 | 7,215 | 11,479 | 11,505 |

| Medicaid | 2,146 | 1,175 | 1,184 | 1,881 | 2,325 | 2,920 | 4,511 | 6,270 |

| Food Stamps | 288 | 341 | 263 | 185 | 216 | 220 | 222 | 216 |

| Housing | 271 | 187 | 182 | 136 | 144 | 171 | 218 | 193 |

| SSI | 91 | 120 | 134 | 220 | 418 | 235 | 156 | 187 |

| EITC | 78 | 306 | 324 | 186 | 61 | 17 | 5 | 4 |

| Unempl. Comp. | 16 | 58 | 83 | 89 | 71 | 44 | 7 | 11 |

| Pub. Assistance | 22 | 66 | 29 | 21 | 27 | 21 | 26 | 16 |

| Refundable CTC | 41 | 222 | 234 | 87 | 18 | 6 | 3 | 2 |

Source: U.S. Census Bureau, ASEC; U.S. Dept. of Health and Human Services (HHS), Medical Expenditure Panel Survey Household Component Overview

Medicaid LTC costs imputed from Centers for Disease Control and Prevention (CDC), National Post-Acute and Long-Term Care Study (NPALS), Study Publications and Products, table 4; and Zoe Caplan, “2020 Census: 1 in 6 People in the United States Were 65 and Over,” U.S. Census Bureau, May 25, 2023; for food stamps, spending is apportioned to individuals according to their share of household income.

Most means-tested benefits have very narrow eligibility, often limited to those with disabilities or young children. Fewer than 3% of Americans receive Section 8 Housing vouchers, Unemployment Compensation, or Temporary Assistance for Needy Families.[14] Although most seniors receive health-care benefits from Medicare, Medicaid also funds dental, long-term care, and out-of-pocket medical expenses for low-income seniors. Even though 20% of the population across age groups is eligible for Medicaid, the program still spends more on each senior enrolled because of their much greater utilization of medical and long-term-care services.

Conversely, direct taxes are concentrated on the young (Table 2). This is especially true of payroll taxes, which are deliberately designed to redistribute from workers to retirees. But it is also true for income taxes, which increase with earnings and therefore weigh little on older age cohorts, who are out of the labor force and finance consumption from assets or pension income. Furthermore, the standard exemption from federal taxes is higher for seniors, while most Social Security benefits are exempt from federal and state income taxes. Many states also have dedicated tax exemptions for seniors’ pension income.[15]

Table 2

Direct Taxes Paid per Person in Age Cohort, 2022 ($)

| 18–24 | 25–34 | 35–44 | 45–54 | 55–64 | 65–74 | 75–84 | 85+ | |

| Income | 1,545 | 5,820 | 8,328 | 9,752 | 8,113 | 4,671 | 3,237 | 2,873 |

| Payroll | 1,290 | 3,662 | 4,595 | 4,750 | 3,601 | 1,312 | 448 | 214 |

| State | 377 | 1,556 | 2,186 | 2,440 | 1,924 | 940 | 582 | 550 |

Source: U.S. Census Bureau, ASEC

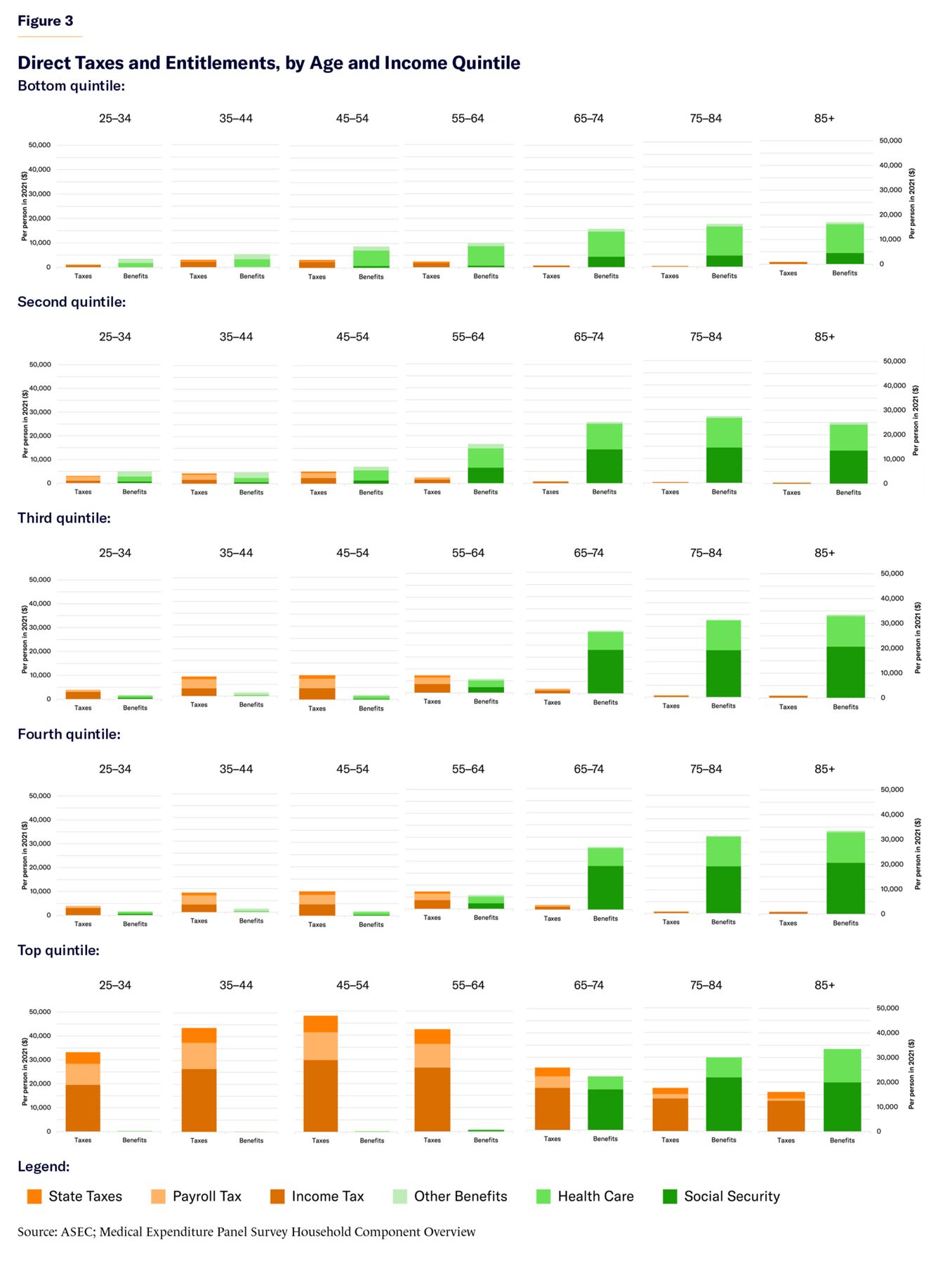

Figure 3 shows how the tax burden, which is distributed unevenly because of progressive income taxes, redistributes money among age cohorts.

Seniors from all income quintiles receive more in benefits than they pay in direct taxes. In fact, because of the structure of Social Security benefits, seniors with incomes above the median receive significantly greater benefits than those with incomes below the median. Only the highest-income quintile of seniors sees its benefits significantly offset by direct taxation.

Among working-age Americans, the welfare state is more progressively structured, with benefits largely reserved for those with incomes below the median. Yet workers at all income levels are burdened by substantial direct taxes. Only for the lowest-income quintile of working-age Americans did benefits significantly exceed direct taxes—and, even then, by an average of less than $2,500 per year for individuals under 45. In fact, since eligibility for federal benefits is concentrated among less than 5% of the working-age population, most of the bottom quintile of working-age adults comprises net losers from redistribution. By contrast, seniors from the lowest-income quintile received net benefits averaging over $16,000 per year.

The highest-income quintile of workers pays much more in taxes than the highest-income quintile of retirees receives in net benefits. But the opposite is true for every other income quintile. For instance, middle-income seniors aged 75–84 receive an average of $32,000 in net benefits, while the middle-income quintile of those in peak earning years (45–54) contribute only $8,000 in net taxes.

While it is true that employment has a longer average duration than retirement—and there is mobility between income quintiles over the course of one’s career—it is clear that the most substantial redistribution accomplished by the U.S. welfare state is from high-income workers to middle-income seniors. It reflects Social Security’s peculiar benefit structure, whereby middle-earners receive much greater benefits in retirement than low-earners, but high-earners do not receive substantial additional benefits beyond that.

Analyzing transfers within a single year nonetheless greatly understates the regressive nature of redistribution to the elderly because of disparities in longevity. The wealthiest quintile lives 13 years longer than the poorest and thus collects Medicare and Social Security benefits for more than twice as long, as a result.[16]

In the coming years, redistributive federal spending is projected to skew even further in the direction of the elderly. The Congressional Budget Office estimates that Social Security and Medicare spending will increase from 8.4% to 11.3% of GDP from 2024 to 2054, while other entitlement spending is projected to decrease from 5.5% to 4.8% of GDP.[17]

Taking Too Much from the Young

Redistribution to the elderly has gone beyond the level necessary to smooth resources over the life cycle; indeed, it now shifts funds from times of need to times of plenty.

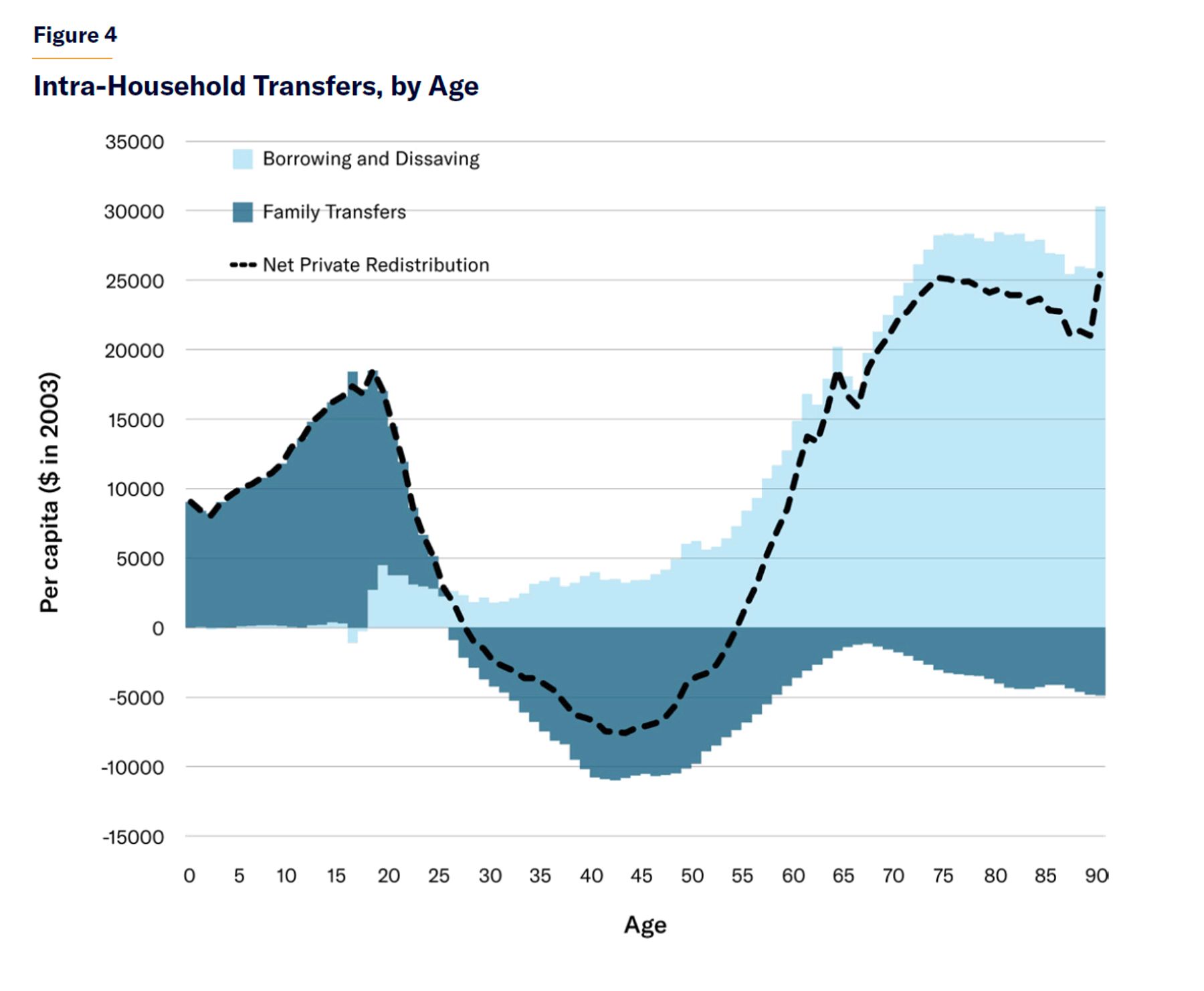

Although the poorest households are often unable to set aside funds for retirement, middle-class Americans can and do transfer substantial resources from their peak earning years to provide for their old age through private arrangements (Figure 4).

Due to a combination of Social Security payments, defined-benefit pensions, and investments, the median income of seniors is only slightly less than that of working adults under the age of 35. But net worth, by contrast, tends to increase steadily with age.

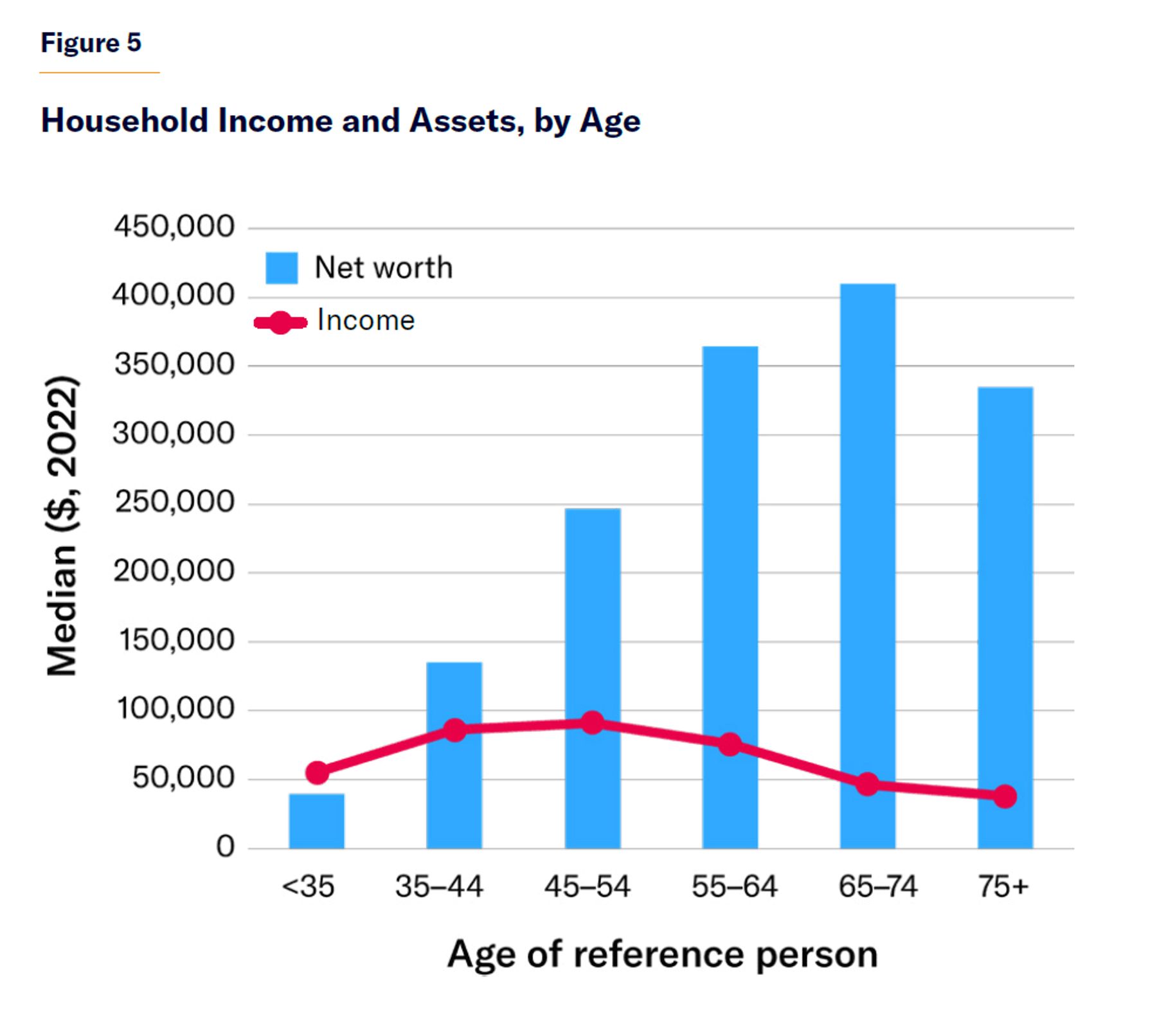

The median household headed by an adult under the age of 35 had a net worth of $39,040 in 2022, compared with a $410,000 median household net worth for those aged 65–74 (Figure 5).[18] Among those aged 65–74, 51% have retirement accounts (with a median balance of $200,000).

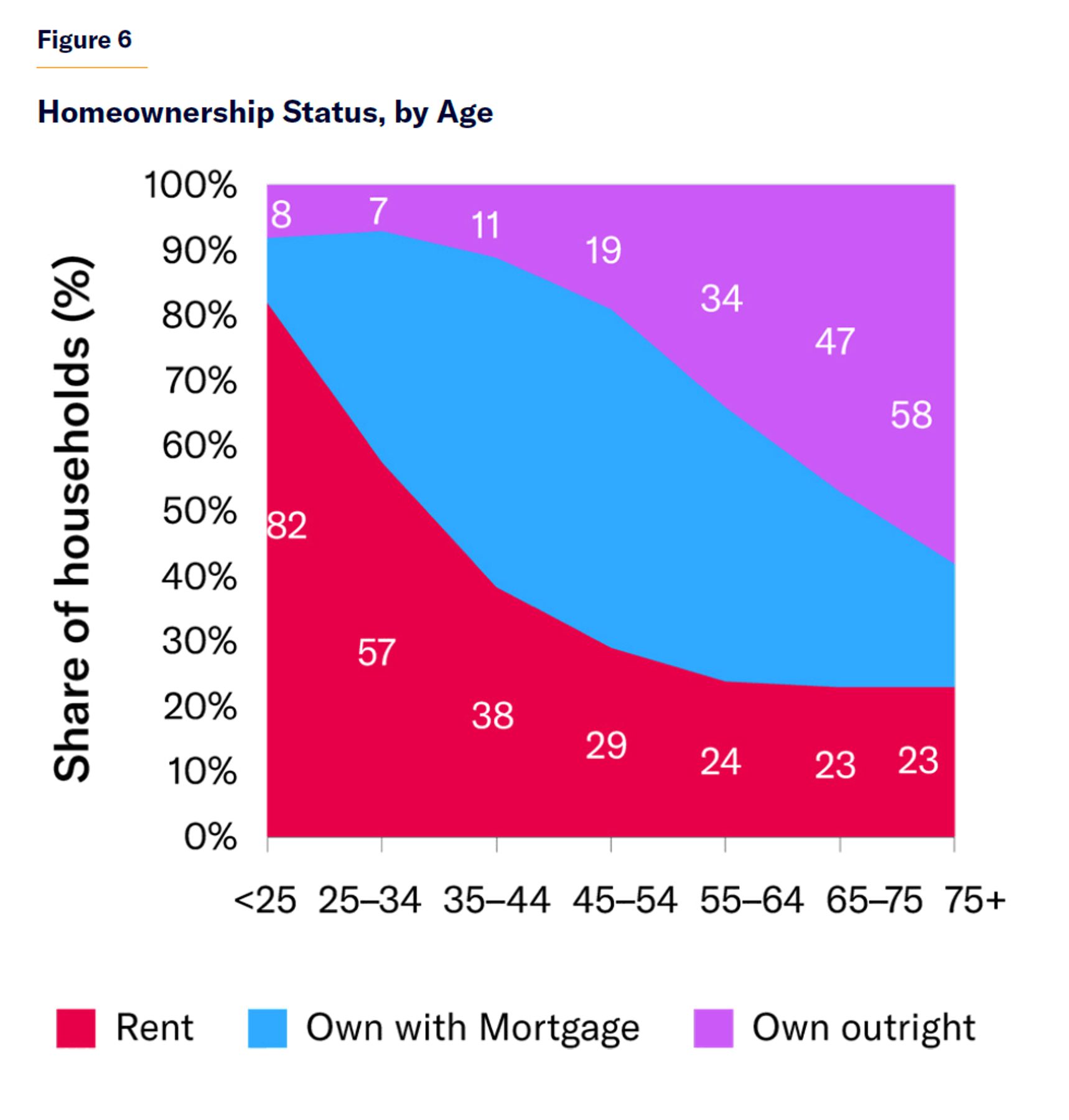

Americans make the bulk of their investment for later in life in the form of home equity. By obviating the need to make monthly rent payments, this eliminates the largest source of financial risk associated with longevity. From early adulthood to retirement, homeownership rates increase from 18% to 77%, and the share that own their homes outright increases from 8% to 58% (Figure 6). Workers are substantially more at risk from income fluctuations than retirees, and their ability to absorb these shocks by borrowing against home equity is also much less.

Intra-family transfers also help to redress life-cycle consumption imbalances.[19] Young parents typically bear more of the burden of supporting others. Whereas households headed by those aged 35–44 have an average of 3.4 members, those headed by Americans 65 and older had only 1.7.[20]

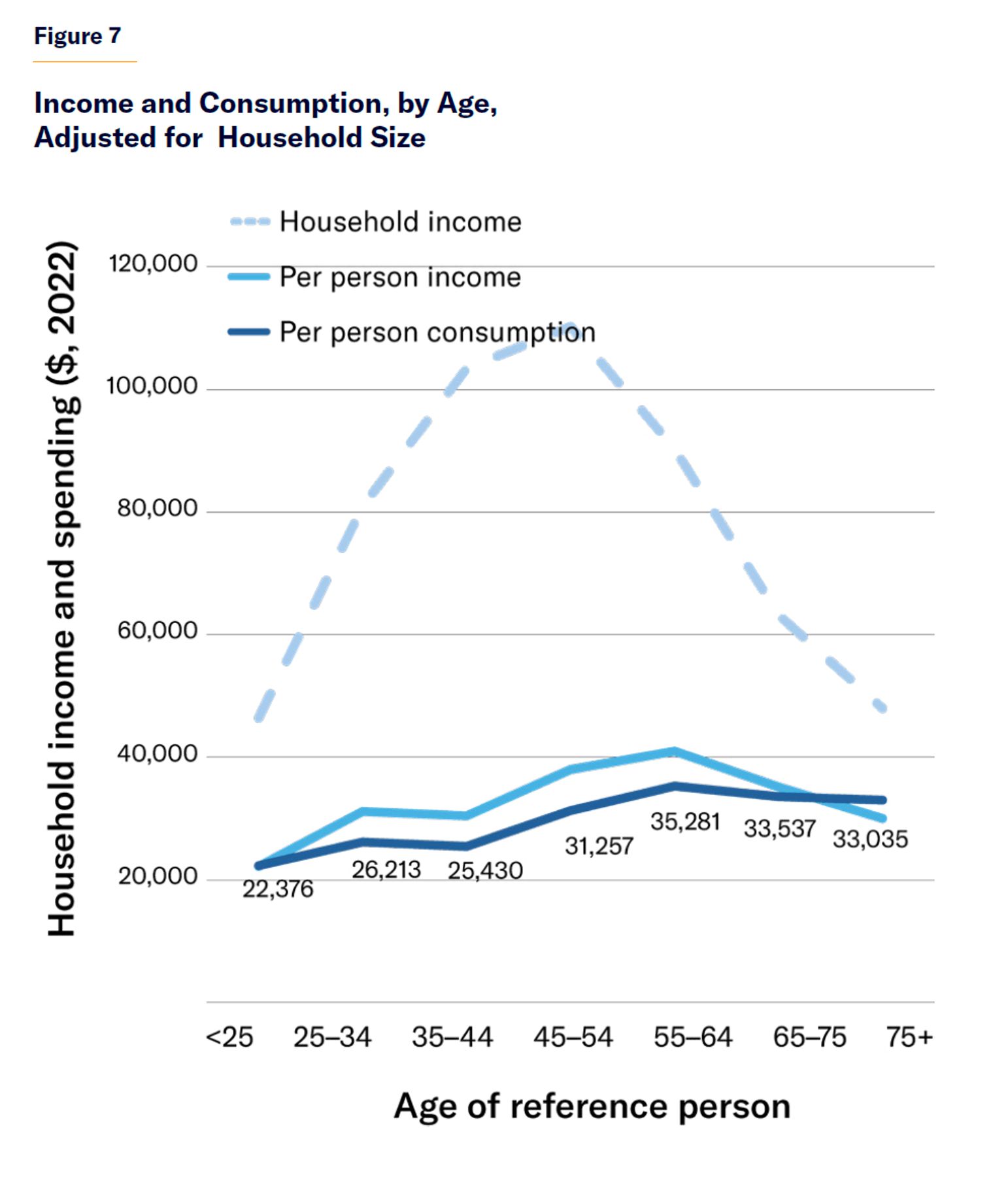

Although retirees, on average, earn substantially less income than workers in their forties, their personal levels of consumption of most goods of services are not lower. In fact, adjusted for the number of people in a household, the median senior spends a similar amount as those at the end of their careers—and more than any other age group (Figure 7). In addition to child-rearing costs, current workers also typically bear substantial commuting expenses.

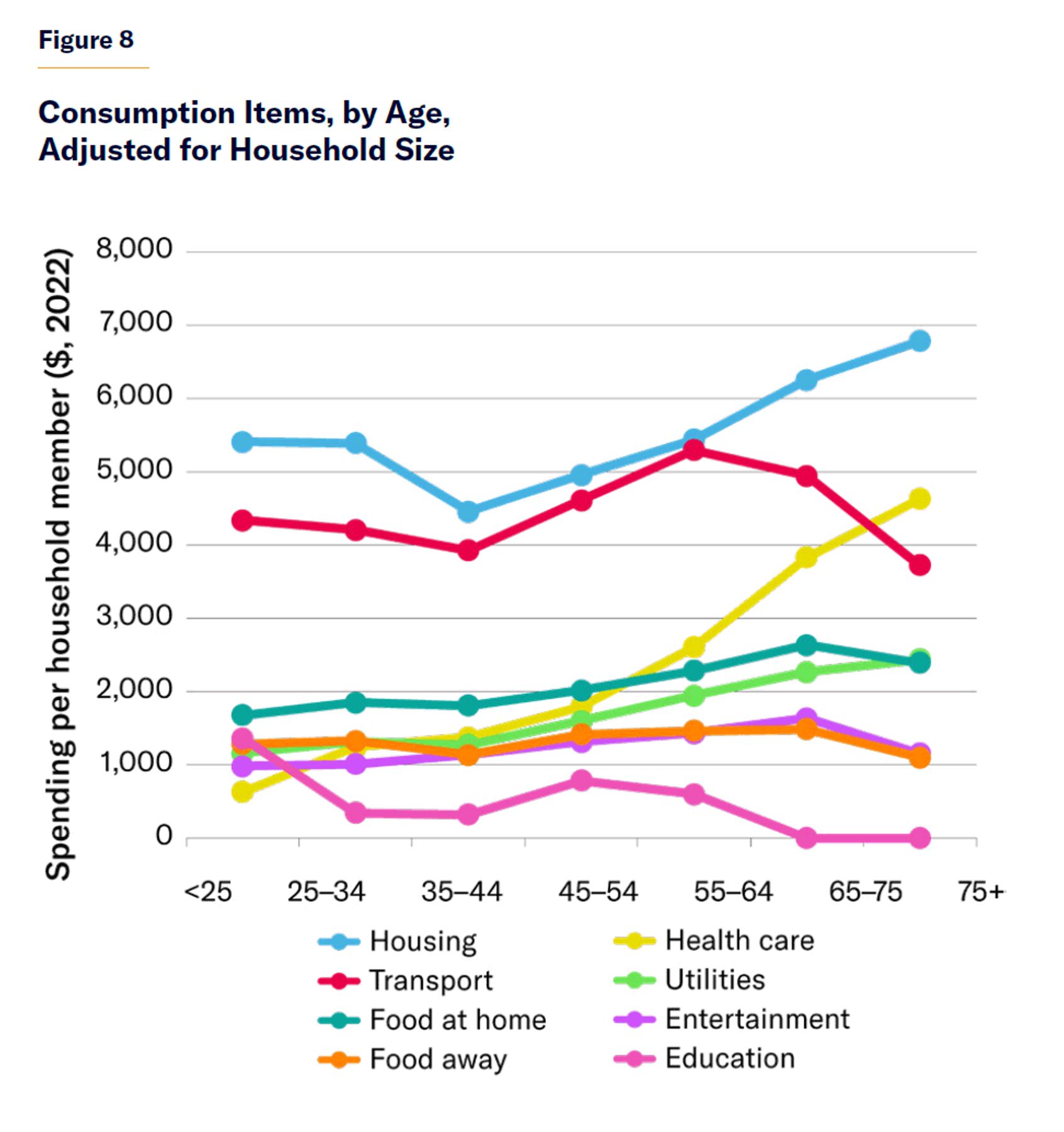

Even though seniors are much more likely to own their homes outright, they spend more on housing and utilities than any other age group (Figure 8). This is because they consume more living space. The median living space per capita increases only gradually from 500 square feet for households headed by adults aged 18–24, to 625 square feet for those aged 45–54. But as children move out and households shrink, people don’t proportionately downsize their housing. The homes of Americans aged 65–74 average 932 square feet per person and, for those aged 75 and older, 1,000 sq ft.[21]

Younger seniors aged 65–74 consume more food away from home, transportation, and entertainment than other age groups. But seniors aged 75 and older, who are often less mobile, have lower levels of consumption, more in line with younger workers.

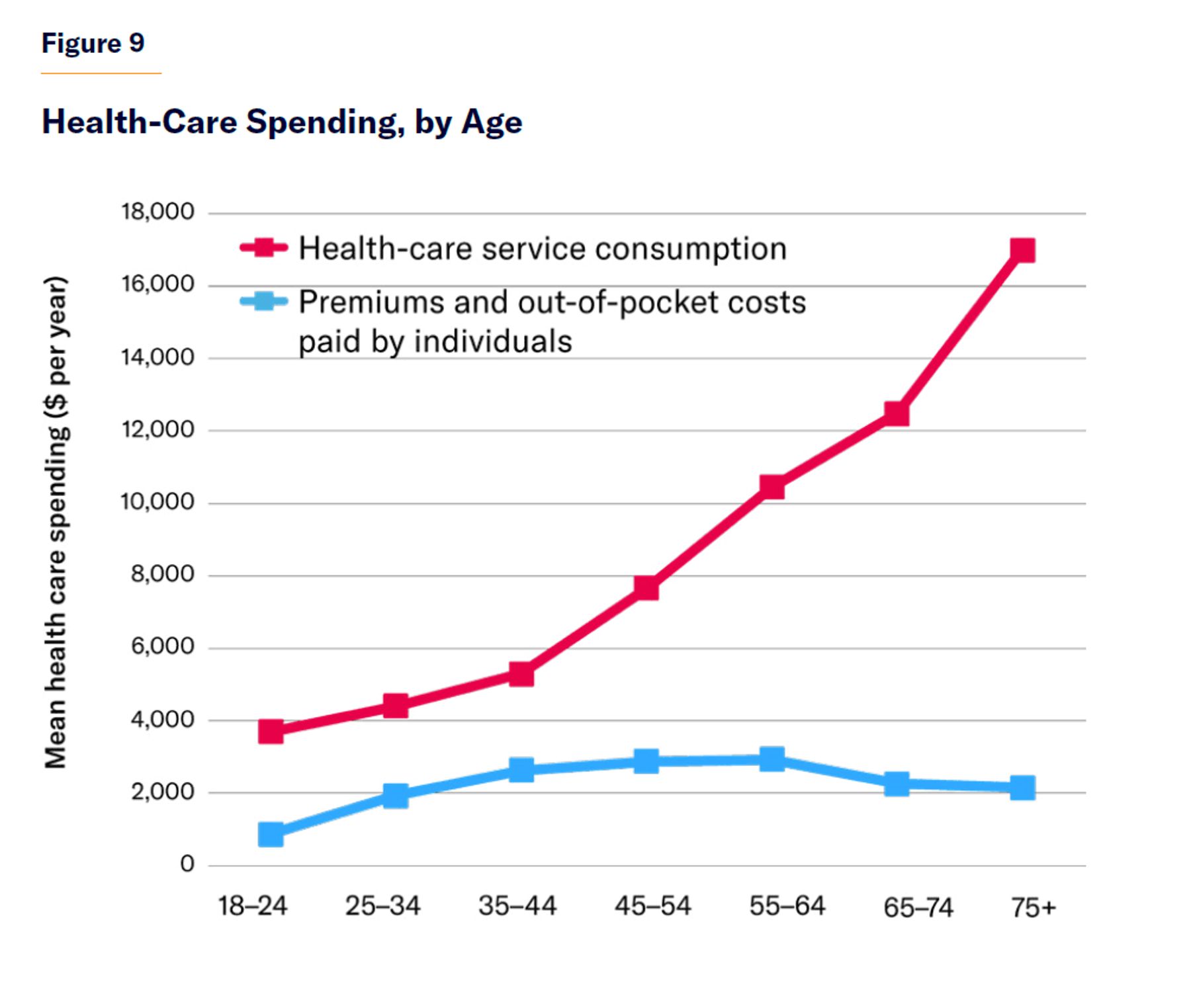

Americans consume steadily more health care as they age, but the bulk of these costs is covered by employers or taxpayers. Due to Medicare and Medicaid, seniors spend less on health-care premiums and out-of-pocket costs than their fellow citizens in their thirties, despite consuming services that are more than three times as costly (Figure 9).

Most of today’s seniors previously made net tax contributions to earlier generations’ Medicare and Medicaid benefits. But with medical capabilities and life spans expanding, today’s middle-income retirees now cost the programs much more than they have previously contributed.[22]

The only major category of expenditure for which the elderly consume substantially less than the young is education. Tuition fees and student loans are generally paid off before individuals reach old age; while the sensitivity of seniors to property taxes means that they avoid much of the burden of financing public education despite having the most home equity. Moreover, property tax assessments are often frozen during the tenure of homeowners, favoring older residents, and many states grant special age-based exemptions from local property taxes.[23] On average, 75-year-olds live in houses worth the same as those of 40-year-olds but pay 15% less in property taxes.[24]

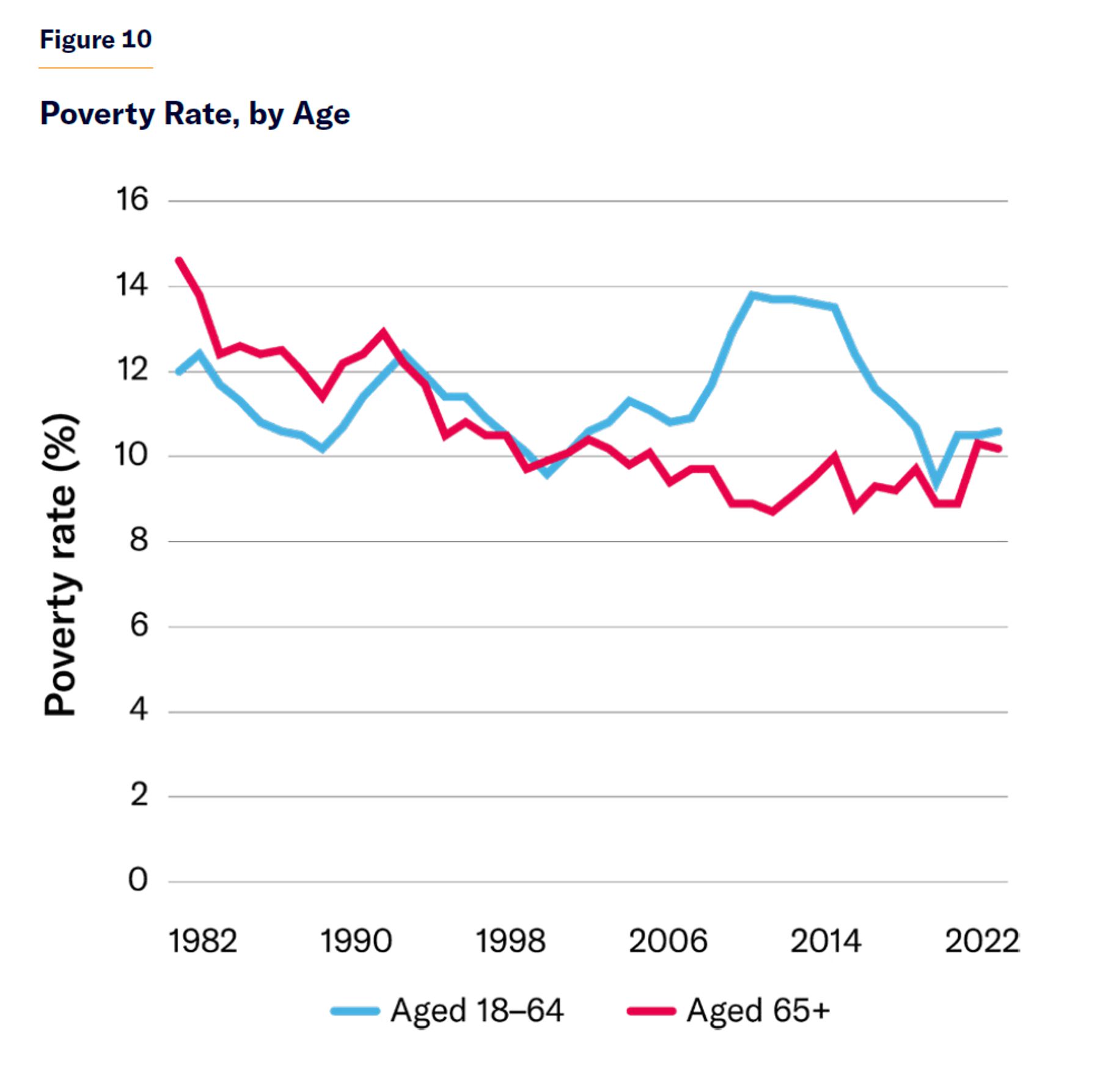

The share of seniors with incomes below the federal poverty level in 2022 was similar to the share among the working-age population. But whereas the poverty rate among working-age households swelled in the years following the 2008 recession, it remained flat among seniors (Figure 10). Not only does the guaranteed income from Supplemental Security Income and Social Security keep seniors relatively better off during business-cycle downturns; it also lessens the need to set aside as much of their income during economic good times to hedge against the risk of unemployment.

The similarity of income poverty rates by age obscures the great difference in the ability of seniors and non-seniors to draw upon accumulated assets to make ends meet.

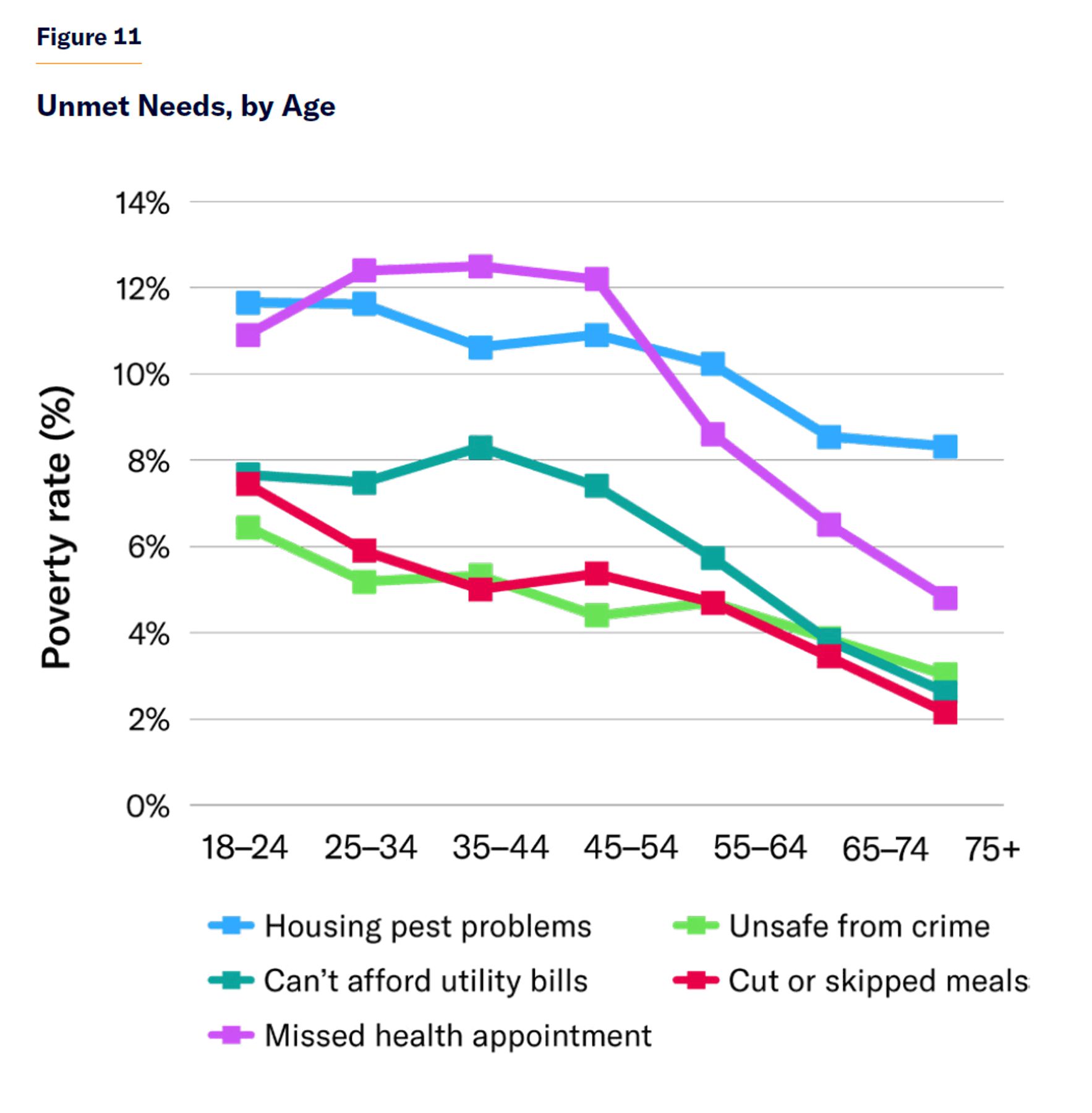

As individuals age, they are less likely to be unable to afford utility bills, less likely to skip meals due to cost, and less likely to fail to visit a doctor when they need to. Because seniors have higher rates of homeownership and need not pay premium amounts for proximity to employment in cities, they are least likely to reside in poor-quality housing that suffers from pest problems, or to live in neighborhoods where they report feeling unsafe from crime (Figure 11).

The magnitude of publicly funded entitlements for the elderly can no longer be justified by a desire to even out resources for people from the time of their highest earnings capacity to the lowest. On average, American seniors now enjoy a higher material standard of living than those in their working careers.

Redressing Life-Cycle Redistribution

If America’s increasingly costly entitlements for seniors are not reformed, major additional tax increases on workers of all income levels will soon be required.[25]

The assumption that economic and population growth could finance ever-rising pension benefits for retirees has proved to be flawed, as economic growth has slowed and the ratio of retirees to workers has increased. Meanwhile, the cost of funding medical and long-term care for seniors is escalating steadily because of improvements in medical capabilities and increases in life expectancy. The bulk of entitlement spending for the elderly goes to middle-income Americans, and therefore serves mostly to crowd out private financing, rather than to diminish poverty or ill health.[26] That can leave programs short of funds as demographics shift, while also slowing economic growth by reducing capital accumulation and encouraging early retirement.

Noting that the welfare state subjects “a third or more of lifetime earnings for redistribution by a political process over which [people] exercise minimal control,” historian David Thomson argued that “certain generations have been able to ‘capture’ the welfare state for their own aging priorities.”[27] He suggested that whereas everyone “over the age of about 40 has a clear interest in maintaining or enhancing the pensions and services of the aged,” the young “who will want a low-interest first-home loan a few years hence are currently still at school, without a vote, and not thinking of themselves as potential mortgage seekers.”[28]

Although the political challenge to reforming entitlements for the elderly is substantial, it is not insurmountable. The first step is to recognize that tomorrow’s old are today’s young, who will benefit from a more appropriate allocation of resources over their life cycle and less leakage of resources through the process of redistribution.[29] Furthermore, leaving more resources to young families increases their capacity to fruitfully invest in the future.[30]

It is important for the federal government to finance a safety net of cash and health-care benefits to prevent poverty among the elderly. But workers should not be made to pay for additional benefits to maintain the living standards of more affluent households in retirement; that should be a private responsibility.

To redress the impact of federal entitlement expenditures so that they do not redistribute excessively from the young to the old:

- Social Security beneficiaries should be allowed to opt for a uniform basic income in retirement, in return for a lower payroll tax for the remainder of their careers.[31]

- Medicare should no longer be expanded automatically through the addition of medical services to the standard benefit package, without attention to their cost or effectiveness.[32]

- Medicaid’s long-term-care benefit should be subject to tighter asset tests, so that affluent households have an incentive to purchase private long-term-care insurance.[33]

- Income taxes should be reformed to eliminate special exemptions for affluent seniors and to expand credits for families raising children.

- Working-age households should be permitted to borrow from their recent Social Security contributions to finance living expenses during times of unemployment.[34]

These reforms would each reduce the cost and improve the effectiveness of federal entitlement programs, by reorienting their resources to working-age households that need them more than already-well-off seniors.

About the Author

Chris Pope is a senior fellow at the Manhattan Institute. Previously, he was director of policy research at West Health, a nonprofit medical research organization; health-policy fellow at the U.S. House Committee on Energy and Commerce; and research manager at the American Enterprise Institute. Pope’s research focuses on health-care payment policy, and he has recently published reports on hospital-market regulation, entitlement design, and insurance-market reform. His work has appeared in, among others, the Wall Street Journal, HealthAffairs, U.S. News & World Report, and Politico.

Pope holds a BSc in government and economics from the London School of Economics and an MA and PhD in political science from Washington University in St. Louis.

Endnotes

Photo: Willowpix / E+ via Getty Images

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).