For over a decade, the Bernanke- and Yellen-led Federal Reserve have talked incessantly about conducting monetary policy to achieve the Fed’s dual mandate. The unemployment rate is now 4.7%, at the Fed’s estimate of full employment. When inflation rises to 2% by year-end, the Fed’s dual mandate will be fully achieved. But the Fed has tilted decidedly against normalizing interest rates and convinced itself and markets that doing so would be harmful. How will it respond?

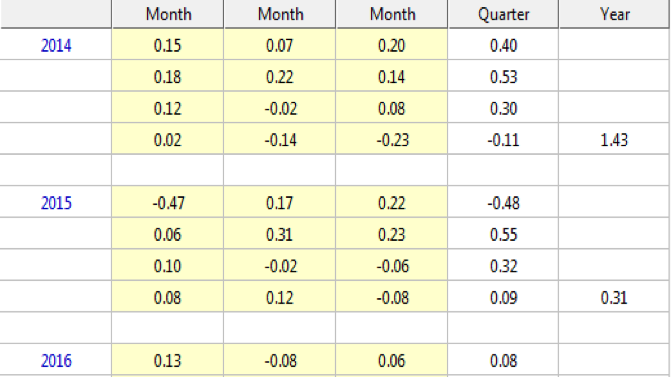

Prior to the sharp decline in oil prices in mid-2014, inflation measured by both the PCE deflator and core PCE deflator were roughly 1.6% year-over-year (see Chart 1). The declines in crude oil prices through mid-February 2016 have suppressed headline inflation and weighed modestly on core inflation measures.

Chart 1. Core and Headline PCE Deflator

PCE Deflator: Month-over-month percent changes

Source: Bureau of Economic Analysis / Haver Analytics

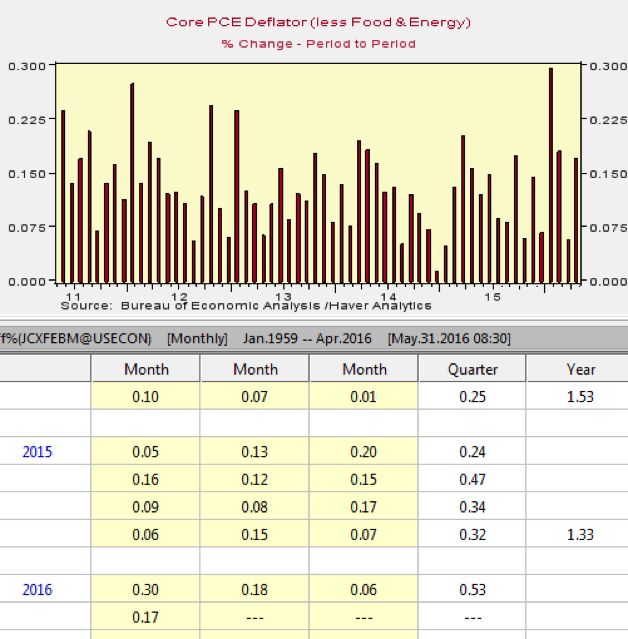

If the significant rise in crude oil prices since February 2016 is maintained and there is no material change in the trajectory of prices of non-energy goods and services, increases in retail energy prices will lift the year-over-year measure of PCE deflator inflation to approximately 2.2% in 2016Q4. Moreover, the core PCE deflator (excluding food and energy), up 1.6% year-over-year through April 2016, is estimated to rise to 1.9%-2.0% by year-end. This estimate is based on the low increases in the second half of 2015 when they averaged 0.1% per month (see Chart 2).

Chart 2. Core PCE Deflator

Source: Bureau of Economic Analysis / Haver Analytics

If so, later this year, the Fed’s dual mandate for employment and inflation as established in its official Longer-Run Goals and Monetary Policy Strategy will have been achieved. The Fed has repeatedly expressed its comfort that inflation would rise to its official 2% longer-run target. Actually realizing that goal at the same time the unemployment rate is at—or below—the Fed’s estimate of the longer-run natural rate of unemployment should be considered important.

The Fed’s dual mandate will be achieved when monetary policy is very accommodative, with the Federal funds rate negative in real terms and the Fed’s balance sheet bloated from massive asset purchasing programs that has created over $2.5 trillion in excess reserves in the banking system.

The Fed’s response to this situation will reveal a lot about how it perceives its objectives and its policymaking role. Will it quicken the path of interest rate normalization when its stated dual mandate is fulfilled, or once again delay increasing rates, as it is has done so frequently in recent years?

History and the thrust of the current Federal Reserve suggest that the achievement of the dual mandate will have little effect on the Fed’s conduct of monetary policy.

The Fed has clearly evolved from conducting monetary policy guided by sound principles to policy actions that are fully discretionary in nature. The Volcker and Greenspan-led Fed acknowledged that monetary policy is incapable of generating permanent job gains or productivity advances, and so emphasized that maintaining stable low inflation was the Fed’s greatest contribution to achieving its dual mandate.

In the early 2000s the Fed began altering its reaction function in several ways. In response to fears that inflation was too low—and deflation posed a low probability but high cost outcome—the Fed kept its policy rate too low relative to economic and inflation conditions. Additionally, in response to fears that raising rates would result in harmful increases in bond yields, the Fed began to explicitly manage market expectations.

In response to the 2008-2009 financial crisis, which stemmed from the unsustainable debt and a housing bubble that its earlier monetary policies facilitated if not contributed to, the Fed launched emergency monetary policy measures that clearly helped the economy and the financial sector escape from crisis.

Since then, as the economy has expanded at a moderate but disappointing pace and the financial crisis has ebbed into history, yet inflation remained below 2%, the Fed’s behavior has been fully discretionary. The path of normalizing rates has become a moving target of frequently changed unemployment rate objectives, labor market measures it deems important and policy adjustments to random international and financial conditions. Most glaringly, the Fed has readily shifted its economic assessment with each Employment Report, despite the large month-to-month swings in reported jobs, occasionally large revisions and the Bureau of Labor Statistics’ large estimated standard error in its survey results.

In reality, the Fed is just as fickle as market participants in its assessment of the economy. The Fed gives the clear impression that monetary policy directly influences specific labor market conditions that historically have been considered way beyond its scope, and conducts policy as if the historic lags between monetary policy and the economy have disappeared.

If there has been any guideline to the Fed’s behavior that has been fairly consistent in recent years, it can be described as a reaction function of “maximizing employment subject to the Fed’s 2% targeted inflation constraint.” By year-end, the Fed is expected to be bumping up against that constraint.

The Fed, fearing that financial markets may react poorly to raising rates, may be laying the groundwork for how it will respond to this situation. First, it argues that the natural rate of interest—that unobservable real rate that is consistent with the real economy growing along its potential path—has receded significantly. The Fed estimates potential growth to be 2%, a dramatic decline from its 2007 estimate of 2.7%. A lower natural rate implies that the current negative real Federal funds rate is not nearly as stimulative as history would suggest.

Secondly, some Fed members argue that the Fed’s 2% inflation target is a longer-run average, suggesting they would be comfortable with inflation rising temporarily above 2%. While they emphasize that the Fed is targeting inflation and not the general price level (which would allow for a sizeable increase in inflation), the Fed obviously uses the fact that inflation has been below 2% to suggest that it would be comfortable if inflation rises above 2%.

Two general arguments suggest this line of thinking should not inhibit the Fed from raising rates. First, although the natural rate of interest seemingly has fallen, it is not negative. That is, consistent with 2% potential growth, the expected rate of return on capital is not negative. Maintaining a negative real Federal funds rate at full employment and 2% inflation is excessively accommodative. The Fed’s deliberations about whether to raise rates would be more rational if currently the funds rate were close to inflation. Unfortunately, it is not.

Secondly, the Fed favors higher inflation because the Fed perceived that inflation is generated by stronger real economic growth and lower unemployment, and ongoing excessive monetary accommodation will stimulate stronger aggregate demand. Reality check: persistently weak economic growth and capital spending suggest clearly that the Fed’s monetary accommodation and very low real costs of capital are not stimulating. There’s a reason for this stubbornly low growth that the Fed finally seems to be acknowledging: an array of non-monetary factors are constraining economic activity. Among these factors, higher taxes (state and local as well as Federal), a growing web of government regulations and rising government-mandated expenses are generating inefficiencies and constraining actual and potential growth (see Rethinking Fed Policy amid Supply Constraints, April 29, 2016). The Fed is incapable of offsetting these constraining factors, and its efforts to stimulate simply result in mounting distortions.

These counter arguments to the Fed’s tilt against proceeding to normalize rates carry little weight within the very dovish Fed.

As a result, the Fed is expected to not materially adjust monetary policy when its dual mandate is fully achieved, and proceed to raise rates very slowly. We expect two rate increases by year-end 2016, which would leave the real Federal funds rate significantly negative at the same time the Fed’s dual mandate will have been achieved.

Mickey Levy is Chief Economist for the Americas and Asia, Berenberg Capital Markets, LLC and member, Shadow Open Market Committee.

Interested in real economic insights? Want to stay ahead of the competition? Each weekday morning, e21 delivers a short email that includes e21 exclusive commentaries and the latest market news and updates from Washington. Sign up for the e21 Morning Ebrief.