The Cost-of-Thriving Index: Reevaluating the Prosperity of the American Family

Photo: zoranm / iStock

A dramatic divergence between data and experience is confounding America’s policy debates. The data seem to show that households have attained unprecedented prosperity, and wages have (at worst) held their own against inflation, or (at best) risen much faster than prices. By conventional measures, material living standards everywhere in the income distribution are at all-time highs, and technological progress continues to improve them. Yet many jobs able to support a family in the past no longer do. Millennials are in worse financial shape than were those of Generation X at the same age, who themselves had fallen behind the baby boomers.[1] The stories appear irreconcilable.

The explanation is this: inflation does not measure affordability. Key assumptions built in to inflation indexes for the purpose of measuring the underlying, economy-wide upward pressure on prices are different from, and often counter to, the key assumptions necessary for assessing the economic choices and constraints faced by households. When analysts use inflation adjustments to compare household resources over time, they have chosen the wrong vantage point, and their view is obscured.

Economists and families see three things differently:

- Quality Adjustment. Products and services that rise substantially in price but in proportion to measured quality improvements can become unaffordable, while having no effect on inflation.

- Risk-Sharing. New products and services can increase costs for the entire population yet deliver benefits to only a very small share, while having no effect on inflation.

- Social Norms. Society-wide changes in behaviors and expectations can alter the value or necessity of a good or service, while having no effect on inflation.

As an alternative to inflation adjustment, this paper proposes the development of a “Cost-of-Thriving Index” (COTI) that tracks the cost of a basket of major items that a family of four would likely seek to buy. A comparison over time between the cost of that basket and a median weekly wage indicates whether economic trends are easing or compounding the challenge of making ends meet.

In 1985,[2] the COTI stood at 30—it would require 30 weeks of the median weekly wage to afford a three-bedroom house at the 40th percentile of a local market’s prices, a family health-insurance premium, a semester of public college, and the operation of a vehicle. By 2018, the COTI had increased to 53—a full-time job was insufficient to afford these items, let alone the others that a household needs.

Introduction: Making Ends Meet

It sounds like an absurd riddle, or perhaps a kindergarten-level math problem: the median male full-time worker earned $314 per week in 1979, while his counterpart at the median in 2018 earned $1,026;[3] who was better off? In fact, the question proves fiendishly difficult, even as its answer lies at the heart of understanding America’s economic progress and challenges.

The easiest answer is that $1,026 is 227% larger than $314, case closed. People lacking even rudimentary training in economics know that’s not right. Inflation reduces the value of money over time, so $1 in 2018 is not the same as $1 in 1979. But how much inflation has occurred?

Economists have numerous methodologies and indexes for estimating inflation and long-running battles over which are most appropriate in which circumstances. The most commonly used index, the Consumer Price Index (CPI), published by the Bureau of Labor Statistics (BLS), estimates that inflation has reduced a dollar’s value by 71% from 1979 to 2018.[4] Put another way, one 2018 dollar is worth 29 1979 cents. A different index preferred by the Federal Reserve and many economists, the Personal Consumption Expenditures Price Index (PCE), published by the Bureau of Economic Analysis (BEA), estimates that a dollar’s value has declined by 66%; so one 2018 dollar is worth 34 1979 cents.[5]

Unfortunately, not only are these estimates substantially different, but they produce opposite answers to the initial question. Using CPI, our 2018 worker’s $1,026 in 2018 earnings is worth $297 in 1979 dollars—or 6% less than the $314 in 1979 dollars earned by the 1979 worker. Using PCE, the 2018 earnings is worth $353 in 1979 dollars—a 13% gain.

Each index has its strengths and weaknesses, but they share a more serious problem: traditional measures of inflation are not intended to, and do not, describe all the forces acting on a household budget against which a changing wage might most reasonably be compared. On one hand, inflation, as Federal Reserve economist Michael Bryan has observed, “is a monetary phenomenon. It is caused by too much money chasing a limited number of things to buy with that money. As such, the control of inflation is rightfully the responsibility of the institution that has monopoly control over the supply of money—the central bank.”

On the other hand, Bryan continued, “the cost of living is a real concept, and changes in the cost of living will occur even in a world without money. It is a description of how difficult it is to buy a particular level of well-being. Indeed, to a first approximation, changes in the cost of living are beyond the ability of a central bank to control.” The cost of living might move in different directions in New York and Cleveland, he notes, or for older and younger households. But “it is inappropriate for us to think about inflation, the object of central bank control, as being different in New York than it is in Cleveland, or to think that inflation is somehow different for older citizens than it is for younger citizens. Inflation is common to all things valued by money.”[6]

To put rising nominal wages in context, inflation is not the right technical mechanism. Nor is it conceptually valid. What does it mean, after all, to say that a 2018 dollar is worth 29, or 34, 1979 cents? No currency-exchange counter exists at which one can be swapped for the other. Nor can our worker travel back in time to spend today’s earnings in a market of yore.

If inflation does not track the cost of living, then what would? The concept of “cost of living” is itself contested, with many economists arguing that inflation actually overstates cost-of-living increases because it fails to account for the savings that consumers can enjoy by switching to newer and lower-cost products or sales channels, or the constant but subtle improvements in the things they buy.[7] If inflation measures the increased price of buying the exact same set of things as in the past, any new opportunities that emerge for consumers to substitute new and different things must hold them harmless or leave them better off. The price of replicating one’s 1979 level of well-being in 2018 could not possibly have risen as much as inflation says it has.

Such a framework makes one major, unrealistic assumption: that having the exact same set of things in 2018 as in 1979 would lead to the exact same level of well-being. That’s not how life works. To use one obvious example: suppose the car was invented and widely adopted during that period. A new invention has no effect on inflation, and advancements in manufacturing that bring its price down would appear as deflation. A new invention cannot increase the cost of living as defined above. If households find that shifting their consumption to it improves their well-being, they can do so; if not, they can stand pat with their horses and buggies. Yet from the household’s perspective, the level of “well-being” achieved in 1979 with no car may now require a car, whether to access retail establishments that have moved to the town’s periphery, to get to work, or to socialize with friends—in short, to remain full participants in the society. They might also face the problem that horses and buggies are no longer for sale.

Alongside formal “inflation” and a technical “cost-of-living” measure that aims to hold constant absolute material consumption, an accurate depiction of economic trends would track a more dynamic basket of the things that a family would need to retain the financial security and social engagement typical of a flourishing middle class. Call it the “cost of thriving.” Much work could be done in constructing the most accurate possible measure or, more likely, a series of measures that accounts for regional and demographic differences. As a starting point and proof of concept, this paper offers a Cost-of-Thriving Index (COTI) that tracks how many weeks of the median male wage would be required in a given year to pay for a three-bedroom house, a health-insurance premium, a semester of public college, and the operation of a vehicle.

Any number of objections might be raised to these particular parameters: Why focus on male wages, when most women work, too? Why count a health-insurance premium’s total cost, when employers often cover a substantial share? A detailed discussion of each of these choices is presented in the description of methodology below (III.A. Index Components). But broadly, the choice of parameters flows from the question to be answered. Here, the question is how well the typical male worker can provide for a family.

This report shows that his ability to do so has degraded dramatically. A generation ago, he could be confident in his ability to provide for his family not only the basics of food, clothing, and shelter but also the middle-class essentials of a comfortable house, a car, health care, and education. Now he cannot. Public programs may provide those things for him, a second earner may work as well, his family may do without, although his television may be larger than ever. The implications of each is surely worth pondering. But the fact that he can no longer provide middle-class security to a family is an unavoidable economic reality of the modern era.

I. What Can Inflation Tell Us?

Before turning to the development of new measures, a review of those already available may be instructive. Existing inflation indexes attempt to quantify, to varying degrees, underlying macroeconomic inflation and increases in the cost of living. Recognizing their limitations is crucial to using them responsibly when they are the best available data and to understanding how and why a cost-of-thriving index should differ.

American economists and policymakers rely on two standard measures of inflation. Best known is the Consumer Price Index (CPI), calculated by the Bureau of Labor Statistics (BLS). To calculate CPI, BLS uses its Consumer Expenditure Survey (CEX) to estimate the “basket” of goods and services consumed on average by a household.[8] It then gathers detailed information on market prices for each item in the basket. Changes in the prices of those items, weighted by the share of spending that each item accounts for, yield CPI’s overall inflation estimate.

A second measure, the Personal Consumption Expenditures Price Index (PCE), is calculated by the Bureau of Economic Analysis (BEA). To calculate PCE, BEA relies mostly on CPI’s price estimates but uses other sources for some categories.[9] BEA then weights those price changes using a different basket calculated from its own tabulation of personal consumption expenditures, as reported by the producers who sell those goods and services, in its National Income and Product Accounts.[10] The result is PCE’s overall inflation estimate. By considering everything sold by producers, PCE achieves a broader “scope” of coverage than CPI—for instance, it captures health-care expenditures made by government programs and employer-sponsored insurance plans on behalf of consumers, whereas CPI would count only what consumers had paid out of pocket.

Historically, the federal government has regarded CPI as the official inflation measure. Government statistics presented in “constant” dollars are usually adjusted using CPI. Formulas “indexed to inflation,” including Social Security’s Cost of Living Adjustments (COLA) and the wage rates in many collective bargaining agreements, use CPI for that purpose. However, in 2000, the Federal Reserve switched to using PCE to assess price stability; and the Fed’s Open Market Committee’s target of 2% annual inflation refers to PCE.[11]

PCE generally yields lower estimates of inflation than CPI, so adjusting measures of personal income using PCE makes “real” gains appear larger—if prices have gone up less, more of the wage gain represents real purchasing power. CPI estimates that prices have risen by 252% over the past 40 years[12] while PCE estimates a rise of 194%.[13] Men’s median weekly earnings have increased by 227% over the same period;[14] so using CPI’s inflation estimate, they appear to have declined in real terms by 6%—but using PCE’s, they appear to have increased by 13%. Regardless of the inflation metric used, the wages of men with less than a college degree have grown more slowly than prices (Figure 1). Especially given the seemingly contradictory answers that the two indexes give on the highly salient question of men’s wage growth overall, a vigorous debate rages over which picture is closest to the “truth.”[15]

How to choose? Understanding what the indexes are saying and why they disagree requires an examination of how they are constructed. But that examination leads toward two conclusions: first, both estimates have shortcomings, and taking the best from each yields a higher inflation estimate than either provides on its own; second, neither measure usefully reflects the pressures on a household budget.

This section proceeds by discussing how CPI and PCE approach each element of inflation estimation: establishing a basket, recording prices, and applying a formula. It then compares the drawbacks of each and shows why an accurate estimate of inflation faced by households is likely higher than what either index suggests.

A. Baskets

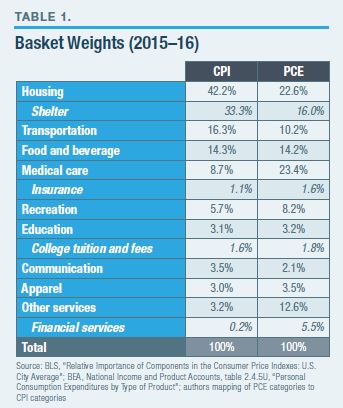

Traditional discussion of an inflation index’s basket uses the term “scope” to refer to those items that are included and “weight” for the relative importance given to each. Here they are combined under a single heading of “weight”—if products not in “scope” are instead thought of simply as ones to which a weight of zero has been assigned, questions of scope and weight collapse into a single one of the weights assigned. Recall that CPI establishes its relative weights based on a survey of consumers, whereas PCE establishes its relative weights based on a survey of producers. Table 1 presents the most recent weights used in each index.

Traditional discussion of an inflation index’s basket uses the term “scope” to refer to those items that are included and “weight” for the relative importance given to each. Here they are combined under a single heading of “weight”—if products not in “scope” are instead thought of simply as ones to which a weight of zero has been assigned, questions of scope and weight collapse into a single one of the weights assigned. Recall that CPI establishes its relative weights based on a survey of consumers, whereas PCE establishes its relative weights based on a survey of producers. Table 1 presents the most recent weights used in each index.

Several dramatic differences are apparent. CPI assigns substantially greater weight than PCE to housing—specifically, shelter. CPI’s estimate that one-third of household spending goes to shelter (i.e., rent and mortgage payments) appears roughly in line with the rule of thumb that households can afford to spend one-third of income in that manner. PCE’s estimate is extraordinarily low, implying that a household with $75,000 of income would spend just $1,000 per month on rent. That amount would cover a three-bedroom unit at the 40th percentile of rents in only the nation’s least expensive real-estate markets.[16]

Conversely, CPI assigns an implausibly low weight to medical care because it considers only expenditures that consumers report making out of pocket. To put its 9% estimate for all health-care spending in context, the Affordable Care Act considers an employer-sponsored insurance plan “unaffordable” only if the employee’s premium contribution alone exceeds 10% of income.[17] Nationwide, health-care spending totals 18% of GDP.[18] Neither CPI nor PCE assigns substantial weight to health insurance per se because both measure instead the cost of underlying goods and services paid for by insurers; the weight given to insurance itself covers only the administrative costs of the insurance provider.[19]

Note also that college education receives very low weighting in both indexes because most households have no one attending college at a given point in time, and many that do have a substantial share of their tuition subsidized by grants and other public spending. Thus, while the weight assigned to the price of college tuition may accurately reflect its importance to trends in economy-wide price levels, it does not reflect the cost faced by a household attempting to save for its children’s future education.

B. Prices

PCE generally relies upon the price estimates created by BLS for use in CPI, so both indexes can be discussed together. Where the nature of a good or service changes substantially over time, an inflation measure must incorporate a fraught determination about how much of the accompanying price increase is inflationary versus how much reflects improvement in quality. In many cases, as technology progresses, price may even decline as quality improves. Several major and illustrative categories are described here, to highlight choices and limitations in BLS methodology.

Medical Care. Health care provides a quintessential illustration of the potential gap between price increases perceived by households and inflation perceived by economists. The BLS estimate for medical inflation appears far lower than the rate at which households are seeing health-care costs rise. BLS reports that medical-care prices have risen 93% from 1999 to 2018;[20] but during the same period, the average family health-insurance premium has increased by 239%.[21]

Two key factors help to explain this gap: first, when medical care increases in price because it has improved in quality—for instance, thanks to the introduction of a superior but costlier procedure, drug, or device—those price increases are not considered inflationary because the patient is getting greater value for the greater cost. This is an example of quality adjustment.

Second, many purchases of medical care are intermediated by insurance, which inflation analyses strive explicitly to disregard. But the presence of insurance has critical implications for a household. Its costs are determined by the behavior of all participants in their risk pool rather than thier own choices. When people across society consume greater quantities of medical care, the cost of health insurance will rise even if the prices of individual medical services have not, and even for households that consume a lower quantity. Both market and regulatory forces will typically preclude a household from consuming its own preferred bundle of health-care services as opposed to the one reflected by the standard set of insurance offerings.

Transportation. A new car, according to BLS, costs no more in 2018 than in 1996.[22] Anyone who has watched car advertisements over the past 20 years, let alone shopped for a car, knows that this is not true. Prices have increased substantially. Typical cars that a family might consider for their primary vehicle are illustrative: the Manufacturer’s Suggested Retail Price (MSRP) for a base-model, four-door Toyota Camry increased by 40%, from $16,800[23] to $23,600;[24] MSRP of the lowest-cost minivan, the Dodge Caravan, increased 47%, from $17,900[25] to $26,300.[26]

BLS reports these prices as flat because today’s base-model vehicle has many more features than one did 20 years ago. In effect, estimates BLS, the 2018 Toyota Camry would have cost $23,600 back in 1996. Put another way, the right comparison for a base-model 2018 Camry is not a base-model 1996 Camry but a mid-range 1996 Camry SE, whose MSRP was $24,100.[27]

In other respects, BLS methodology overstates a household’s costs. The relevant vehicle cost for a family is not a car’s sticker price but rather the “total cost of ownership,” including gas, maintenance, insurance, etc. Some of these items have become more expensive, but others have become cheaper—for instance, higher-quality cars last longer, depreciate less quickly, and require less maintenance each year. This also deepens the market for reliable, less expensive, used cars.

BLS attempts to account for many of these factors, tracking price increases in each category and weighting them by household spending to produce a total price increase for the category called “private transportation.” Even while holding new car prices flat, BLS reports that inflation in the broader category totaled 47% from 1996 to 2018.[28]

By contrast, analysis by the American Automobile Association (AAA), relied upon by the federal Bureau of Transportation, estimates a total cost of ownership that attempts to factor in the various costs of operating a car and also to calculate those costs on a per-mile-driven basis.[29] The federal Internal Revenue Service uses a similar methodology to set the mileage reimbursement rate each year.[30] AAA reports that in 2018, the total cost per mile (averaged across all vehicle types) reached 59.0 cents, up from 42.6 cents in 1996—a 39% increase, which is substantially lower than the BLS private-transportation estimate for price levels.

Electronics. As the pace of innovation increases, the challenges of quality adjustment compound, producing inflation estimates most obviously disconnected from household budgets in areas like electronics. Take televisions, which BLS reports have declined in price by 97% between 1996 and 2018. This is not true in a literal sense—a TV available in 1996 for $500 could not be purchased new in 2018 for $15. Closer to accurate would be the claim that households can now pay $500 for a 55-inch, high-definition, flat-screen, “smart” TV that would have cost $17,000 in 1996, which may technically be true,[31] though, of course, almost no households were indeed footing that bill. From the household’s perspective, a more relevant comparison would be that in 1994, a Best Buy flyer advertised seven televisions with a price range of $150–$1,548 (median of $330);[32] in December 2019, the top seven “Best Match” offerings on the Best Buy website ranged from $90 to $1,000 (median of $280).[33] These are much better televisions, of course, and a savings, too—but a savings closer to $50 than $500 or $15,000.

Similarly, BLS reports that the price of telephone hardware fell by 81% between 1997, the data set’s start, and 2018. Changes to phones over that period make a comparison almost impossible. (As a fascinating analysis of an old Radio Shack ad demonstrates, a modern smartphone contains features that would have cost thousands of dollars if purchased as individual products in the past.)[34] But for a household budget, the question is not how much better an iPhone X is than a cordless land-line handset; it is how much must be spent to keep the family connected in modern society. Few households would say that communications is an area where they can spend less now than they used to, let alone an order of magnitude less.

Children fare no better. BLS reports that toy prices (including electronics and video games) fell 73% during 1994–2018.[35] Yet the actual toys on the market have become more expensive. In 1996, Toys “R” Us advertised a Nintendo 64 for $200.[36] Today, the cheapest Xbox One console sold by Amazon costs $245 (and its list price is $300).[37] The outdated Sega Genesis cost $100 in 1996, whereas the outdated Xbox 360 costs $170 now.[38] A 20-inch boy’s bike cost $100 in 1993[39] and costs at least $100 now.[40]

C. Formulas

Even after all the data on the prices and weights of each basket item have been gathered, substantial work must be done to combine them in a way that produces a useful estimate of inflation. Most differences between PCE and CPI formulas are de minimis, but one matters: PCE accounts for substitution in ways that CPI does not.

When the price of a product increases, consumers are likely to buy less of it and spend more on something else (with less or no price increase) instead. So if the average rise in prices over a period is calculated based on the weights assigned to each product at the start of the period, those products that see the largest price increases will be overrepresented relative to how much consumers ended up spending on them. PCE attempts to take this into account by creating an average weighting from the beginning and end of the period. CPI does not.[41] This helps to explain why CPI tends to report higher levels of inflation than PCE.

D. Choosing an Inflation Measure

The common argument favoring PCE as superior to CPI emphasizes its approach to substitution, which proponents say does a better job reflecting the prices that consumers actually pay in the market.[42] This is not, however, the primary difference between the two measures. “The discrepancy,” note Federal Reserve economists Yifan Cao and Adam Hale Shapiro, “is actually small.”[43] Their colleagues Joseph Haubrich and Sara Millington explain: “The largest difference tends to be the weight effect, which contributes to bigger changes in the CPI, while the scope effect tends to lessen the difference.”[44]

Because the prices of housing, health care, and college have risen much faster than overall inflation in recent decades (even in CPI data), underweighting any one of them in an index would lead to a downward bias in its inflation estimate. Comparison of CPI and PCE estimates allows for isolation of the bias created by underweighting health care and housing, respectively. According to a BEA analysis of just that, by far the largest difference between CPI and PCE estimates is PCE’s underweighting of housing costs.[45]

BEA reports that from 2002 to 2018, CPI inflation averaged 2.1% while PCE inflation averaged 1.8%. The “Formula Effect” caused by PCE’s accounting for substitution contributed a 0.2% gap, roughly half the total. The “Scope Effect” caused by the differing treatments of medical care was similar in size to the Formula Effect but cut the other direction, raising the PCE estimate by 0.2% compared with CPI. Other miscellaneous effects also tended to push the PCE estimate higher, by 0.1%. Yet PCE lands substantially lower than CPI because of the “Weight Effect,” which is caused by the different weights assigned to housing, with PCE’s major underweighting of housing costs pushing its estimate down 0.4% compared with CPI’s.

Put another way: accounting for the ways in which PCE might provide a better estimate than CPI (incorporating substitution and properly weighting health care, accepting miscellaneous other changes) would produce an estimate higher than CPI. Only because PCE gives such low weight to housing costs does it ultimately yield a lower inflation rate (Figure 2).

Given all these countervailing effects, seizing on the Formula Effect—which accounts for substitution—as a basis for preferring PCE over CPI makes little sense. A better approach, based on what is known and understood about each index, would be to use PCE as a baseline—accepting its use of substitution and relying on its coverage of medical care and its choices with respect to minor variations—but then to adjust for its underweight of housing. The portion of the gap between PCE and CPI that is accounted for by housing represents a reasonable first approximation of the necessary adjustment to PCE[46] and can be added back to the PCE estimate, creating a modified index called PCE+. Stated in plain English, PCE+ represents the inflation estimate that PCE methodology would produce if it took account of the housing-driven inflation reported by CPI.

During 2002–18, PCE+ averaged 2.2%, or 0.1 percentage points higher than CPI. While men’s wages over the period have been flat against CPI and up 5% against PCE, they are down 1% against PCE+ (Figure 3).

While PCE+ may be preferable to either CPI or PCE when an inflation adjustment must be used, no genuine “inflation” estimate will capture the extent to which wages are better or less able to cover a household budget, because that is not what inflation describes. The decisions made at BLS and BEA about CPI and PCE are defensible as efforts to measure the economy-wide price inflation that might be of concern to macroeconomic policymakers. Indeed, because of challenges in accounting for both substitution and quality adjustment, most of the criticisms leveled by macroeconomists at inflation indexes lament that they overstate the level of actual price inflation in the economy.[47] For example, researchers worry that because new breakthroughs like tablet computers can take years after their introduction to appear in consumer-expenditure data and then count in the basket weighting, rapid initial price declines are never captured.[48] For households, the problem looks quite different.

II. The Conceptual Problem

Recall Federal Reserve economist Michael Bryan’s observation that “the cost of living is a real concept, and changes in the cost of living will occur even in a world without money. It is a description of how difficult it is to buy a particular level of well-being. Indeed, to a first approximation, changes in the cost of living are beyond the ability of a central bank to control.”

Bryan also cites research conducted by Nobel laureate Robert Shiller, who surveyed economists as well as the general public about their “biggest gripe about inflation.” Whereas more than three-quarters of the public chose “inflation hurts my buying power, it makes me poorer,” fewer than one in eight economists said the same. Roughly half chose that “inflation causes a lot of inconveniences. I find it harder to comparison shop. I feel I have to avoid holding too much cash, etc.,” and the rest chose other issues entirely.[49]

“I wonder,” muses Bryan, “if, in the minds of most people, the Federal Reserve’s price-stability mandate is heard as a promise to prevent things from becoming more expensive. . . . But this is not what the central bank is promising to do.”[50]

Certainly, this misconception seems widely held among policy analysts: if inflation is low, that must mean that things are not becoming much more expensive. So in a world with no inflation, for instance, someone should be indifferent between living in 1970 and earning $10,000 or in 2015. The $10,000 has exactly the same “value” and, by implication, purchasing power. If inflation caused prices to double over the period, the person would much prefer the $10,000 in 1970 to $10,000 in 2015; he would need $20,000 in 2015 to be comparably situated. But as Bryan notes, this is not necessarily what inflation means. As the aforementioned methodological review showed, it means something quite different. Even if inflation were exactly zero, households might vastly prefer $10,000 in 1970 to the same amount in 2015, or vice versa.

From a material living standard perspective, many analysts argue that a household would prefer the $10,000 in 2015—or, put another way, that inflation overstates the effect on the material living standard experienced by a household. Products improve in countless ways that inflation ignores but people recognize. Consumers might benefit from better and more varied foods in the supermarket, brought to them by safer and more reliable supply chains. They might be able to communicate instantly with friends and family around the world using FaceTime, when in the past it would be a treat to see those relations once every few years. The material gains, viewed through this lens, seem endless; how could anyone say, holding money constant, that he would rather live in an earlier generation?[51]

That may all be true, but it remains incomplete. Also required is an affordability perspective, which emphasizes whether people are able to support themselves on a contemporary wage at a contemporary standard of living. From that perspective, standard inflation understates the challenge that rising prices may pose to households in three ways.

A. Quality Adjustment

Inflation measures assume that the market offers households whatever they want in whatever increments they want. If a product that costs $100 is replaced by one that costs $200 but is determined to be twice as valuable, its price is considered unchanged for purposes of inflation. But a household that can afford to spend only $100 on the product will perceive that the price has doubled.

In theory, we might expect an efficient market to continue offering the $100 option for households that cannot afford or see less value in the new and improved version. In practice, this may not happen for a variety of reasons. One problem is that firms prefer to avoid the complexity of maintaining countless product lines and instead target their product development and marketing toward what they expect will be a market’s most profitable segments—often higher-income households with more disposable income.[52] New firms can hypothetically enter to exploit the gaps created, but they may lack the scale and expertise to deliver a reliable product at a low price. In some cases, regulatory forces may eliminate the availability of lower-cost options, as when safety and environmental standards affect the design of vehicles.

Another problem is that a market’s evolution may preclude the combination of certain features. Housing provides the most obvious example: a home built with 1940s style, size, and quality in a neighborhood of middle-class families can simply cease to be available at the price paid for it in the 1970s. Health care, with the structure of its insurance market, faces a similar constraint. Even supposing that a product could be designed that offered a family gold-plated access to the quality of care available in the 1970s for the price paid in the 1970s, providers would have no idea how to deliver such service and would be unlikely to accept such patients and give them comparable priority to those seeking 2019-level care.

These limitations have important implications for how economists think about substitution. The assertion that substitution improves a household’s well-being rests on the assumption that the same basket of goods available in Year 0 remains available in Year 1—thus, any change must reflect the household preferring the Year 1 basket. But if quality adjustment leads to a situation where dramatic price increases are accompanied by changes in the available baskets of goods, households can face a situation where no inflation occurs—yet their consumption changes in ways that reduce their well-being. If large and costly necessities become unaffordable while other components of the consumption basket plummet in price and become ubiquitous, inflation can seem tame and households better off, even as they find it increasingly difficult to provide their children with building blocks like a good neighborhood or education. Perversely, in an inflation index that accounts for substitution, necessities will garner ever less weight in the official statistics as their price increases move them out of reach for more of the population.

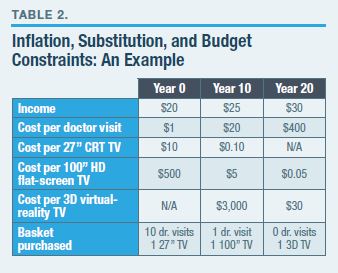

Consider the concrete, if oversimplified, example of an economy with just two goods: health care and TVs (Table 2). Suppose that in Year 0, a typical household has income of $20 and purchases a 27-inch CRT TV for $10 and 10 doctor visits for $1 each. Note that a 100-inch flat-screen TV was also on the market, for $500. In Year 10, income has increased by $5. Flat-screen TVs have fallen 99% in price, and doctor visits have increased 20-fold in price. The household purchases one flat-screen TV and one doctor visit. Another 10 years pass, income rises by another $5, and the cost trends persist. New TVs that did not even exist in Year 0 are available and affordable in Year 20, but doctor visits are out of reach.

Consider the concrete, if oversimplified, example of an economy with just two goods: health care and TVs (Table 2). Suppose that in Year 0, a typical household has income of $20 and purchases a 27-inch CRT TV for $10 and 10 doctor visits for $1 each. Note that a 100-inch flat-screen TV was also on the market, for $500. In Year 10, income has increased by $5. Flat-screen TVs have fallen 99% in price, and doctor visits have increased 20-fold in price. The household purchases one flat-screen TV and one doctor visit. Another 10 years pass, income rises by another $5, and the cost trends persist. New TVs that did not even exist in Year 0 are available and affordable in Year 20, but doctor visits are out of reach.

Is the family better off? How would we know? Have wages grown faster than inflation? What does that question even mean? Has there even been any inflation? Macroeconomists might look at these trends one way, while technologists would look at them in another. But if regular, reliable access to a family doctor is simply more important to the household, life became less affordable, and then it became unaffordable.

B. Risk-Sharing

Products that spread risk offer everyone value in formal economic terms, but only those who suffer the risky outcome receive a tangible benefit. If health-insurance premiums rise because conditions present in 1% of families can now be treated with new and extremely expensive procedures, prices have not increased for inflation purposes. But 99 out of every 100 households that have to pay more for their insurance will never experience any perceptible change in the quality or quantity of their health care. Good analyses of economic well-being are usually careful to focus on outcomes at the median, rather than the mean; yet when it comes to the asserted improvement in material living standards associated with higher health-care spending, the gains are present only on average and are concentrated in a very small fraction of the distribution.

Thus, while the average family health-insurance premium has risen from $5,791 in 1999 to $18,764 in 2017,[53] median spending on actual health care for a family of four (two adults, two children) has risen from $2,122 to $4,380.[54] That is, the typical household is paying almost $13,000 more to get health care that costs $2,200 more (Figure 4). The family is, in fact, better protected from a wide range of rare conditions, but both their material living standard and financial flexibility may be far lower.

Thus, while the average family health-insurance premium has risen from $5,791 in 1999 to $18,764 in 2017,[53] median spending on actual health care for a family of four (two adults, two children) has risen from $2,122 to $4,380.[54] That is, the typical household is paying almost $13,000 more to get health care that costs $2,200 more (Figure 4). The family is, in fact, better protected from a wide range of rare conditions, but both their material living standard and financial flexibility may be far lower.

Safety improvements exhibit a similar dynamic. The higher costs associated with stricter building codes and more resilient vehicles reflect real gains in quality and should not be considered inflationary. Yet the median consumer would not have died in a car accident or house fire but for the changes. For that person, the changes reduce affordability without providing any tangible improvement in his material living standard.

C. Social Norms

Societal changes can dramatically alter the need for, and value of, goods and services, independent of their objective quality. Whether and how to account for these changes is especially controversial because doing so injects a seemingly subjective element into the process. If people feel differently about their consumption, that can seem less economically valid than a measure of the absolute amount they consume. It is not. The value or utility of a basket of goods is a function not only of its absolute size but also the context in which it is used and the effects that it has.

For instance, social norms implicate tangible economic value when evolving technological standards destroy and create network effects, reducing the utility of some products and services while increasing it for others. If widespread adoption of cell phones leads to decommissioning the nation’s pay phones, or an assumption of access to a navigation app ends the practice of invitations including directions, or vendors convert to accepting only mobile payments, then a smartphone and wireless subscription become necessities to engage in both community and commerce. Yet the introduction of such products is not inflationary; to the contrary, the rapidly developing technologies produce the effect of price decreases.

Social norms can also act through expectations. Hosting a Super Bowl party in 2019 with a 1979 TV is not an option. Purchasing a 1970s-era toy is unlikely to deliver the desired result for children who have just sat through an hour of 2010s-era television advertising, let alone spent time with friends whose own toys are more up-to-date. Evolving standards of personal appearance with respect to hygiene and attire ensure that merely maintaining a bygone consumption pattern is unlikely to deliver the value it once did.

Looking beyond their formal economic descriptions, dismissing the salience of social norms is an obvious denial of human nature. This might be contested when comparing expectations across a couple of decades, but the fallacy becomes apparent when the time frame gets longer. It seems almost plausible to say that people can derive the same utility or value from a 1980 standard of living in 2018 that they could in 1980. But if social norms are irrelevant, why stop there? Does the assertion hold for an 1880 standard of living? If economists wish to argue that an 1880 middle-class life-style should equally satisfy a household striving for the “middle class” in 2018, they can try. Their subsequent analysis will obviously be unhelpful.

An effort to understand how well households are doing and how far a wage will stretch must therefore establish as its point of comparison a moving target that defines at each point in time the basket that a family would need in order to be full and dignified participants in their society. Defining the basket will always be an inherently political process, and methodologies will differ. So long as analysts state their assumptions clearly, policymakers and the public can make their own determinations of what standards they consider reasonable and what conclusions they should draw.

III. A New Approach: The Cost-of-Thriving Index

Instead of “how much has the money supply affected price levels in the economy,” an economic analysis that sought to understand whether a changing wage left a worker more able or less able to cover an average middle-class family’s needs would ask: Does this wage cover a middle-class family’s needs? In contrast to inflation, it would ignore substitution: the question is not what the family chooses to buy, given its budget constraints. It would ignore quality adjustment: the question is not how great are the things the family does manage to buy. It would account for social as well as economic changes: the question is not how much a family needed in an arbitrarily chosen year of the past (that no one needed a car in 1819 says little about its importance in 2019). And it would look at changes in the price of pooled-risk insurance products: the question is how much it costs the family to acquire insurance, not how much the family would pay out of pocket if uninsured.

Note that the question posed here refers specifically to a family. Economy-wide inflation measures take averages across all household units, substantially diluting the “signal” from the costs of highest concern to young people forming families.[55] The selective focus is not “discriminatory”—everyone will be a child in a household at one point in life, and most will be the adults in households with children. Rather, it argues for focusing on a point in everyone’s life cycle where budget constraints may be especially salient and where those constraints are most likely to be of societal concern because they influence decisions about labor-force participation and family formation and because they define the conditions in which children are raised.

Highly sophisticated models could—and should—be designed to analyze these issues in detail and examine how answers differ across demographic groups and regions. As a starting point in addressing the gap in policymakers’ understanding and to underscore just how different the answer is from an answer about inflation, this paper creates the COTI, consisting of the largest expenditures that a middle-class family of four might face each year: rent for a three-bedroom house, a health-insurance premium, a car, and a semester of public college tuition. It compares the cost of this basket with median weekly earnings for men working full-time, yielding the number of weeks required to cover these costs.

The COTI aims to capture the relative size of the bills and paychecks that a household would have encountered in a particular year, which removes the need to make assumptions about inflation over time. All figures reported in the COTI are stated in nominal (or “current”) dollars, meaning that the dollar amounts are those measured in the economy at those points in time.

A. Index Components

At first glance, some of the items chosen for the COTI basket will puzzle modern analysts: Do we really expect middle-class households to afford all the costs associated with home ownership, a car, a college education, and a health plan? This reflects the bias built in to standard inflation analyses, which work from what households are buying at the current moment in time. In the past, as the COTI demonstrates, it was perfectly plausible to afford all these things. And all are things that a typical middle-class family might want to have confidence that it can afford. By recalibrating to focus on what households buy at each point in time, standard inflation measures intentionally disregard the possibility that households can no longer afford what they need. The COTI suggests that this is exactly what has happened.

Basket Component: Annual Rent for Three-Bedroom Residence

Source: The COTI uses the federal Department of Housing and Urban Development (HUD) estimate of Fair Market Rent for a three-bedroom housing unit in Raleigh, North Carolina.[56]

Rationale: Three bedrooms is both the median and mode for American housing units[57] and a logical number for a family with two children. Rent provides a more reliable estimate of total cost than assembling the disparate elements of home ownership, and HUD estimates of “Fair Market Rent” (FMR) are at the 40th percentile in each housing market, making the reference unit one that is near the distribution’s middle but also slightly below average.[58] The Raleigh market is used here as representative of markets nationwide: roughly half of Americans live in metropolitan areas larger than Raleigh and half live in areas smaller; roughly half live in areas with a higher FMR and half live in areas with one lower. The median hourly wage in Raleigh, $18.97 per hour in 2018, is similar to the nationwide median of $18.58.[59]

While the size, quality, and amenities of the 40th percentile unit in 2018 may differ from those in 1985, holding constant the percentile comes closest to approximating a unit of comparable quality on dimensions like location, neighborhood, community, and schools which are of central importance to families in choosing their housing. Put another way, if the specific house at the 40th percentile of the rent distribution in 1985 were at the 20th percentile in 2018, it would be unlikely to offer a family a living experience of comparable quality, regardless of the square footage and appliances inside.

1985 cost: $5,560 | 2018 cost: $15,924

Basket Component: Annual Family Health-Insurance Premium

Source: The COTI combines estimates from the Kaiser Family Foundation[60] and the federal Centers for Medicare & Medicaid Services[61] for the annual cost of employer-sponsored health insurance for a family. Kaiser provides a cost estimate per year for 1999–2018. Data for 1987–98 are imputed from Kaiser’s 1999 value and the CMS estimate for the annual growth rate in per-enrollee employer-sponsored private health-insurance expenditures for each year. The 1987 estimate is repeated for 1986 and 1985, which conservatively understates the likely growth of insurance costs in those years.

Rationale: The most reliable historical data on health-insurance premiums are available for the employer-sponsored market, which should provide a reasonable proxy for all comprehensive private health-insurance policies. Historically, direct-purchase plans have had lower premiums than employer-sponsored insurance (ESI) because they could exclude people with preexisting conditions and because they could offer narrower networks. A direct-purchase plan of comparable quality to ESI, however, would likely have a higher cost because an individual buyer lacks the scale of a large-group purchaser and because insurers fear adverse selection. Since passage of the Affordable Care Act (ACA), which forced direct-purchase plans to behave more like ESI, premiums have converged[62]—so a focus on such plans would cause the index to report a more dramatic cost increase than has occurred market-wide.

Individuals covered by employer-sponsored plans do not bear their full cost, but the share of the nonelderly population covered by employers has fallen to less than 60%. Among full-time workers with income up to 250% of the federal poverty line ($62,000 for a family of four), fewer than half have employer coverage.[63] The share that will lack such employment at some point in time is substantially higher, and access to coverage in the event of job-switching is often a major concern. Even among those with coverage, the share of premium costs borne by the worker has been growing, and spending to meet deductibles has more than tripled in the past decade—the typical covered household incurred almost $8,000 in expenses in 2018.[64] Despite skyrocketing costs, the share of compensation paid as employer contributions for pensions and insurance has barely increased, from 11% in 1985 to 13% in 1993. The share in 2018 was slightly lower than in 1993.[65]

It is an anachronism of the modern market that the idea of a middle-class family taking on its own health-insurance premium might seem implausible. From 1987 to 2013, the final year before implementation of ACA, the number of directly insured Americans fell from 13.7 million to 12.8 million, even as the uninsured population rose from 27.3 million to 44.1 million. In 2018, with ACA’s exchanges and subsidies firmly established, the share of Americans purchasing their own insurance remains below its (unsubsidized) 1987 level.[66]

A variety of government programs, including Medi-caid and the subsidies available under ACA, now seek to close the gap between what insurance costs and what families can afford. The COTI ignores these for two related reasons. First, in principle, government provision is not a substitute for self-sufficiency. Part of what has historically defined the American middle class is the ability for a family to meet its own needs without resort to government benefits. Second, in practice, if families find themselves reliant on government support regardless of whether a household member is working at the median wage, the value of working declines, as does the rationale for forming a stable family supported by a worker. If policy analysts are seeking to understand what has changed in the nation’s economic arrangement, the vanishing ability of a worker to provide for essentials like his family’s health care is surely relevant.

1985 cost: $2,343 | 2018 cost: $19,616

Basket Component: One Semester of Public College

Source: The COTI uses the federal National Center for Education Statistics estimate for total tuition, fees, room, and board at a four-year public institution.[67]

Rationale: Two children pursuing four-year degrees would require a combined 16 semesters of college, so a household preparing for those costs would need to save roughly one semester’s worth of cost per year before the children reached college age. (While the savings might ideally earn a positive return in the interim, that return would need to be quite strong just to keep pace with the rate of increase in tuition over the same period.)

The one-semester estimate may overstate costs in some respects—for instance, a family would likely have 20 or more years between the birth of a first child and the college graduation of a second. And in practice, many children do not ultimately attend college (though a small and, it seems likely in recent decades, declining share has chosen from a young age not to consider that path). But it also understates costs by considering only public college costs; private college costs are more than twice as high.[68] Note also that the cost of public college tuition already incorporates the substantial public subsidy provided by the state government.

Inescapable in any discussion of college costs is the question of whether sending all kids to college, especially where the return on investment might be poor, makes sense. The answer to that question is no.[69] But here the question is what costs a household faces and, so long as the nation’s education policy continues to advance a message of “college for all,” saving for college will remain at the forefront of parents’ minds.[70]

1985 cost: $1,841 | 2018 cost: $10,025

Basket Component: Annual Operation of a Vehicle

Source: The COTI uses the federal Bureau of Transportation Statistics (BTS) estimates for the average cost of owning and operating an automobile driven 15,000 miles per year, which are taken from the estimates produced by the American Automobile Association.[71]

Rationale: Most households have one or two vehicles and drive them between 10,000 and 20,000 miles per year.[72] The COTI adopts the 15,000-mile figure used by BTS to report the total cost of ownership, holding this figure constant over time. A more refined analysis could account for changes in vehicle usage over time for particular household types and, especially, particular regions. Generally speaking, vehicle-miles-traveled (VMT) per capita rose 37% from 1985 to 2005 and then fell 2% from 2005 to 2018.[73]

1985 cost: $3,484 | 2018 cost: $8,849

Income Measure: Men’s Median Weekly Full-Time Earnings

Source: The COTI uses BLS estimates for the median usual weekly earnings of men over age 25 employed full-time as wage and salary workers.[74]

Rationale: BLS data for weekly earnings isolates full-time wage and salary workers and provides breakdowns by gender and education level. The use of a weekly, rather than an hourly, wage also holds constant changes in typical working hours for full-time employees.

The COTI uses men’s earnings for sociological as well as statistical reasons. Sociologically, a substantial body of empirical research has identified the unique importance of work to men’s well-being and to both family formation and stability.[75] Recent work by David Autor, David Dorn, and Gordon Hanson has found not only that the declining economic fortunes of men contribute to various social maladies but also that the effect on women is the reverse:

While Americans see traits like “be caring and compassionate,” “contribute to household chores,” and “be well educated,” as of nearly equivalent importance to being a “good husband” or a “good wife,” they are far more likely to describe “be able to support a family financially” as a very important trait for a good husband. This finding holds across education level, race, and gender. Seventy-two percent of men and 71% of women say that the ability to support a family financially is very important for a man to be a good husband, compared with 25% of men and 39% of women saying the same about being a good wife.[77]

Statistically, the median male wage was higher than the overall median wage in past decades and remains higher today. Data for all earners, and for women, are provided in the Appendix, alongside data for men; in every case, these wages have more difficulty than the male wage in covering the cost of major expenditures. A focus on men also has the benefit of holding constant the economic experience of a group that traditionally has been recognized as the family breadwinner. By contrast, a median wage across all earners experiences downward pressure from a “mix shift” as women account for more of the workforce. Measures of median household income across all earners credit the additional earnings of sending another worker into the market but cannot make an offsetting debit for the loss of nonmarket work that person might otherwise have performed for the household.

The normative question of whether we should care if the typical man can confidently provide for his family is beyond the scope of this paper. The information presented here establishes only the descriptive reality that once he could and now he cannot.

1985 weekly earnings: $443

2018 weekly earnings: $1,026

B. Index Calculation

The COTI for each year is equal to the sum of the basket component costs in that year divided by the median weekly wage in that year. The result is an estimate of the number of weeks that a primary wage earner would need to work in that year to cover those costs.

In 1985, the basket cost totaled $13,227, which, at a weekly wage of $443, would require 30 weeks of work to cover. In 2018, the basket cost totaled $54,414, which, at a weekly wage of $1,026, would require 53 weeks of work to cover. This is a problem, as there are only 52 weeks in a year.

In 1985, the basket cost totaled $13,227, which, at a weekly wage of $443, would require 30 weeks of work to cover. In 2018, the basket cost totaled $54,414, which, at a weekly wage of $1,026, would require 53 weeks of work to cover. This is a problem, as there are only 52 weeks in a year.

Figure 5 shows the COTI in each year from 1985 to 2018. Figure 6 shows the total basket cost in each year and the annual income implied by the weekly wage.

Conclusion

The COTI shows a declining capacity of a male full-time worker to meet the major costs of a typical middle-class household. As the COTI basket has become unaffordable, families have found workarounds, such as having more household members work more hours, making do without, borrowing, and relying on government support. Each of these workarounds comes with its own costs, undermines the stability of families and the rationale for their formation, and creates high levels of stress and uncertainty. While some may celebrate the increased role played by government in filling these gaps, the continued drift in this direction threatens to strip from the middle class the pride of earned success and self-sufficiency; it also serves to reorient society toward dependence on government support.

The COTI tells only one part of the story of the economy’s evolution in recent decades—there is much it ignores, and many of its assumptions run counter to ones useful in answering questions about, for instance, monetary policy or technological innovation. The same, however, can be said for standard measures of macroeconomic inflation and the adjustments that they suggest to nominal wages, as well as for qualitative assessments of material living standards and technological progress. If we want to place price levels in historical context, inflation indexes are the closest approximation. If we want to know how much consumer surplus our households are capturing, evaluations of product quality can help.

But if we want to understand what has happened to people’s ability to provide for their families, the COTI provides the more reliable guide. The widening gulf that it depicts between what American life costs and what American jobs pay is a central fact of American political economy that the public appears to have understood long before economists. Policymakers should prefer it to standard inflation adjustments for interpreting the nature and quality of the nation’s economic progress.

Establishing basic facts is only the first step in formulating effective solutions, and the COTI does not automatically validate any specific policy agenda. To the contrary, it highlights two very different pathways that each deserve much greater study: What can be done about low wages? And what can be done about high costs? Reforms aimed at making college less necessary, or health insurance less expensive, for instance, might achieve just as much as ones aimed at raising wages—if they genuinely reduced cost rather than merely introducing additional subsidies that deepen dependence on government largess. Recent decades of economic growth have eroded, rather than reinforced, the American model of thriving, self-sufficient families. The decades to come will need to do better.

Endnotes

Photo: zoranm / iStock

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).