Supplemental Benefits Under Medicare Advantage

Medicare Advantage has grown rapidly since the 2003 Medicare Modernization Act, and now covers 17 million or 33 percent of the 54 million Medicare beneficiaries — up from 13 percent a decade ago. This option allows seniors and the disabled to receive their Medicare benefits from a choice of private health care plans, instead of a single benefit structure managed directly by the federal government through the Centers for Medicare and Medicaid Services (CMS).

Much has been written about the relative merits of Medicare Advantage (MA) and Medicare Fee-For-Service from the standpoint of efficiency and care coordination, but less attention has been paid to the supplemental benefits that distinguish MA plans. Policymakers have long been aware of the general categories of supplemental benefits available to enrollees under Medicare Advantage, but little has thus far been done to quantify their specific extent, scope, and availability.

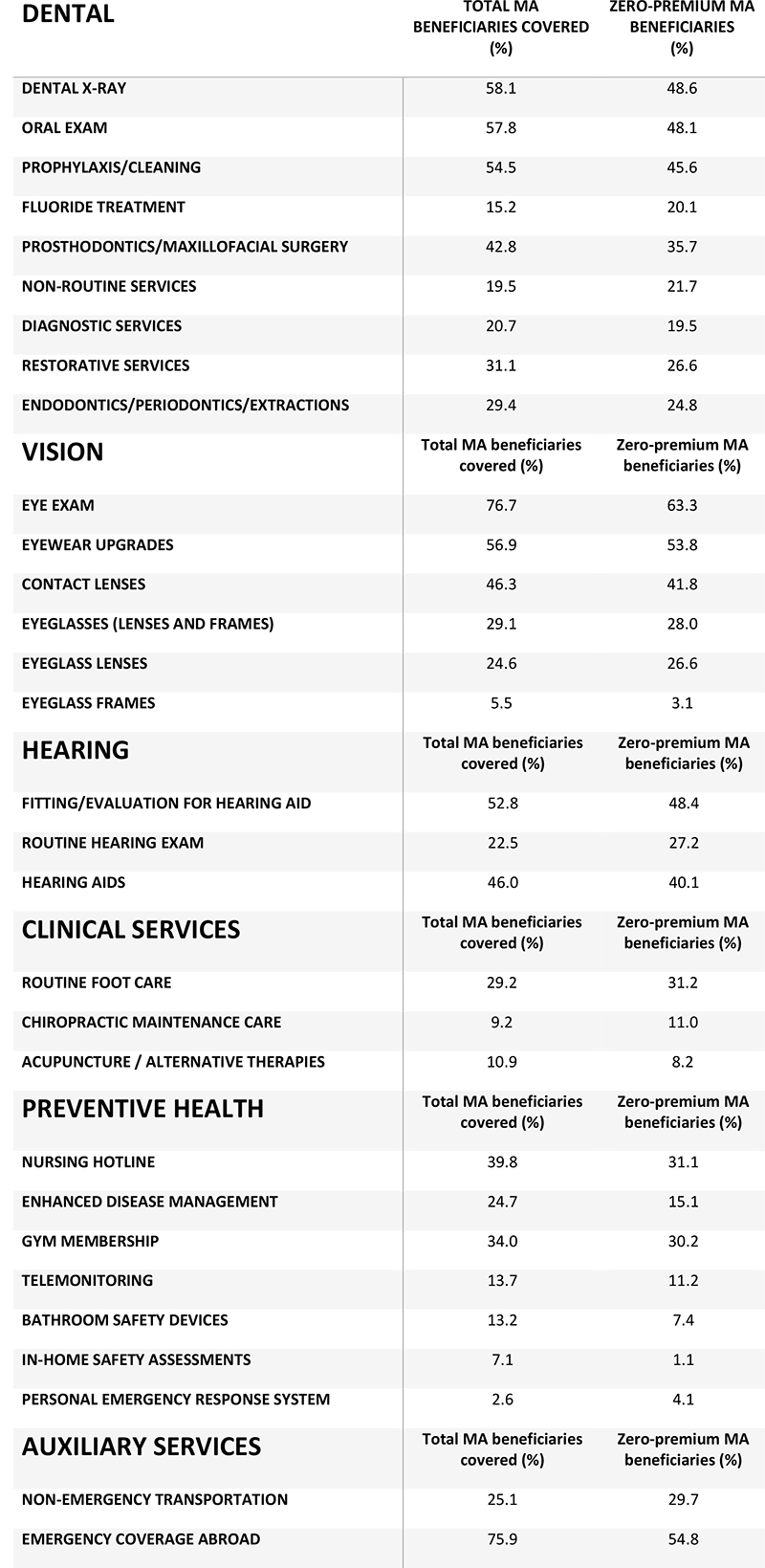

It has been suggested that Medicare Advantage’s supplemental benefits, such as gym memberships, have been designed to attract healthier enrollees. However, CMS data reveals that these are relatively trivial elements of MA supplemental benefit packages. The bulk of supplemental benefits under MA are features of greater value to the sick than to the healthy. In addition to mandatory supplemental protection from catastrophic out-of-pocket costs, the majority of MA plans include preventive dental care, eye care, and hearing assistance.

Moreover, these features are almost as widely available under the subset of MA plans, which charge beneficiaries no supplemental premium — placing them within reach of the poorest beneficiaries, while serving as an indication of the efficiency gain of Medicare Advantage over the traditional fee-for-service structure.

Coverage Gaps Under Medicare Fee-For-Service

Medicare was designed over a half-century ago, along the lines of Blue Cross / Blue Shield health insurance plans of the time. As a result, the program consists of a hospital insurance program (Part A) in addition to a benefit for physician services (Part B), with payments for specific services being hard-wired into statute. Aside from the addition of a (Part D) benefit for prescription drugs, these function to a remarkable degree unchanged — leaving many important elements of modern health care inadequately covered.

Medicare’s separate parts each have their own idiosyncratic cost-sharing structures, imposing potentially unlimited out-of-pocket costs on those suffering from prolonged illness. With cancer drugs now often costing over $100,000 annually, and beneficiaries required to pay 20 percent of these fees, Medicare Part B is an inadequate form of insurance from catastrophic risks. To protect themselves from these expenses, those enrolled in Medicare Fee-For-Service plans may purchase supplemental private Medigap plans, costing an average of an additional $2,196 per year. Yet, though they help limit out-of-pocket costs, Medigap plans also fail to cover services that are specifically excluded from Medicare Parts A and B, such as vision, dental, or hearing.

Changes in vision are a natural consequence of aging — potentially undermining safe driving, mobility, and everyday household tasks. Most seniors will require adjustments to their eyeglass prescriptions, and the American Optometric Association recommends annual eye exams for all aged over 60, but 30 percent of the elderly in Medicare for over five years have not seen an eye care provider. Medicare covers ophthalmological procedures under Parts A and B, but not routine eye exams for eyeglasses or contact lenses.

Hearing problems similarly afflict large numbers of seniors, with 55 percent of those aged 70-79, and 79 percent of those aged 80 and over, suffering hearing loss. Such barriers to communication increase the burden on caregivers, strain relationships, and impede participation in society — yielding isolation with follow on costs for emotional, mental, and physical wellbeing. Although Medicare covers diagnostic hearing exams to see whether medical treatment is required, it does not cover routine hearing exams or hearing aids, or exams for fitting hearing aids.

Routine dental care is also specifically excluded from standard Medicare coverage. Almost a third of those aged over 65 have untreated dental caries, 16 percent suffer from gum disease, while 25 percent lack natural teeth altogether. Aside from the acute pain associated with poor dental health, untreated gum disease can lead to infections, while loss of teeth can yield severe nutritional deficiencies and complications for chronic conditions. A small cavity, which could be treated for $100, can quickly turn into a $1,000 root canal if not dealt with expeditiously. Indeed, when California’s Medicaid program eliminated its comprehensive adult dental coverage between 2006 and 2011, there was a significant spike in visits to hospital emergency departments (EDs) for emergency dental care.

As only 21 percent of Medicare beneficiaries purchase standalone dental insurance, while coverage for the 14 percent also eligible for Medicaid is threadbare to non-existent in most states, the majority of seniors lack dental coverage. Because of this, Americans aged over 65 incurring dental expenses spent an average of $375 on dental care in 2012—71 percent out-of-pocket—with Medicaid accounting for only 1 percent of total costs.

This being the case, some groups have pushed for an expansion of Medicare to include dental coverage, with Democratic presidential candidate Bernie Sanders introducing legislation to cover dental care under Medicare Part B. However, with standard dental insurance in an average market costing around $750 in an average market, adding similar coverage to Medicare could be expected to cost $40 billion per year — with utilization increasing, patients becoming less price sensitive, and existing expenses being taken onto the federal balance sheet.

The addition of a new entitlement of this magnitude is likely not politically realistic. The addition of a Part D prescription drug benefit during an era of budget surpluses was enough of a struggle and only barely succeeded. With the total cost of the Medicare program expected to double over the coming decade, and expenditures projected to continue rising as the baby boomers age thereafter, policymakers seeking to add service to the Medicare benefit must pursue alternatives to attaching new entitlements onto an open-ended fee-for-service system.

Supplemental Benefits Under Medicare Advantage

Every year, Medicare Advantage plans must submit bids denoting the cost at which they propose to provide the standard package of Medicare Part A and B benefits. For 2015, the average bid was 94 percent of the cost of Medicare services being procured directly by the federal government. Plans are therefore able to use these savings to provide “supplemental benefits” to attract enrollees. (Although benchmark amounts provided to MA plans are set slightly above equivalent fee-for-service spending levels, they must bear an additional Health Insurance Tax and implicit 30-50 percent taxes on funds returned to beneficiaries in supplemental benefits.)

MA plans are required to cap yearly out-of-pocket costs for beneficiaries, and must do so no higher than $6,700 — with 56 percent of beneficiaries in plans with out-of-pocket maximums lower than $5,000. The majority of MA beneficiaries are enrolled in plans charging zero additional premium, so they are essentially able to receive the central element of Medigap for no extra charge. Adding a similar cap for beneficiaries outside of MA would likely cost an additional $380 billion over a 10-year budget window, and is therefore also unlikely to be much more politically palatable than was the hastily-repealed Medicare Catastrophic Coverage Act of 1988.

It is possible to employ publicly available CMS data to quantify the specific nature, scope, and availability of other supplemental benefits under Medicare Advantage. Specifically, by combining the 2015 MA Contract Year Plan Benefits Package file with the September 2015 dataset of Enrollment By Plan, it is possible to assess how many MA enrollees are covered by each specific type of supplemental benefit. It is also possible to examine the extent to which these supplemental benefits are covered by the standard benchmark cost of the MA benefit, or merely provided in return for an additional premium.

Summing Up Supplemental Benefits

Supplemental benefits under Medicare Advantage mostly consist of items such as dental, vision, and hearing coverage that are of more value to the sick than the healthy, rather than features such as gym memberships targeting the healthy. And because supplemental benefits are almost as prevalent in zero-premium MA plans as in plans that require an extra premium, they are available to lower-income Medicare beneficiaries.

The relatively small difference in supplemental benefits available in zero-premium and other MA plans suggests that supplemental premiums at the margin might be employed more to reduce cost-sharing than to enhance supplemental benefits. It may also be the case that associated cost-sharing makes supplemental benefits less generous than immediately apparent, as beneficiaries remain required to cover most of the cost out of pocket.

An investigation of the interaction of cost-sharing and supplemental benefits is therefore an appropriate subject for future research, as would be an exploration of the relationship of supplemental benefits to plan bid and enrollment levels.

This piece originally appeared at Health Affairs

______________________

Chris Pope is a senior fellow at the Manhattan Institute.

This piece originally appeared in Health Affairs