Rejuvenating Social Security: A Better Option for Future Generations

Social Security was established to protect households from poverty due to the loss of earnings resulting from old age, disability, and death. But low-income Americans now typically receive less money from the program in retirement benefits than they previously paid in payroll taxes.

While Social Security spent more than $1.2 trillion in 2021, the program’s spending goes mostly to relatively wealthy seniors. As a result, 9% of seniors are still left with incomes below the poverty level. Among seniors who are over 80, live alone, or are black, the rate is even higher. Although governments in Australia and Canada spend half as much per capita on old-age pensions as the U.S., their poorest senior citizens enjoy substantially higher incomes than their American counterparts.

When Social Security was developed in the mid-20th century, it was deemed politically infeasible to provide equal retirement benefits to elderly Americans (as was typical in other English-speaking countries), due to racial divisions and regional economic disparities. For a while, retirees at all income levels benefited from redistribution from working Americans—receiving benefits that greatly exceeded their prior contributions. But as the program has matured and as the ratio of retirees claiming benefits to contributing workers has increased, subsequent generations have been required to pay for their predecessors’s as well as their own benefits. This has exposed the fundamentally flawed structure of the system.

The present Social Security system is set to run out of money in 2034, after which an across-the-board payroll tax hike of more than 3 percentage points would be required to fund benefits currently promised to retirees. In return for these additional revenues, legislators should insist that Americans be allowed to enroll in a new benefit option more focused on protecting seniors from poverty in old age.

Individuals under 45 should be allowed to opt for a simple benefit of $16,988 per year (indexed for inflation) when they reach retirement age, which would guarantee all participating seniors an income 25% greater than the poverty level (86% greater for couples). In return for forgoing benefits above these levels, individuals would receive a 5-percentage-point payroll tax cut for the remainder of their working years, which they could use or invest privately. Such a reform, called Reliable Predictable Security (RPS) in this report, would provide better protection from poverty in old age while reducing the burden of the program on young workers and the economy.

Historical Introduction: How Politics Triumphed Over Security

Prior to the 20th century, few built up significant savings for retirement. The English Poor Laws and the U.S. equivalents expected families to take care of their elderly relatives as they became unable to support themselves. So long as most Americans lived on farms, this did not greatly infringe on living space, and allowed seniors to contribute to household tasks until they became greatly disabled—which was typically not long before death.

From 1880 to 1930, improvements in nutrition, sanitation, and medical science caused average life expectancy in the U.S. to surge from 39 to 60 years.[1] For the first time, industrialization and urbanization brought material comfort and prosperity to the bulk of the population.[2] But these processes often left the aged and infirm behind. Industrialization and urbanization raised the cost of housing, tended to distance the elderly from relatives who may have been able to support them, and removed the elderly’s ability to lend valued service in agricultural households.[3]

Under such circumstances, many elderly people were reluctant to impose on their children, while those who lacked offspring were often left to the poorhouse.[4] Even those who were not disabled faced difficulty, as they were invariably less efficient than younger workers and struggled to find new jobs.[5] The proportion of almshouse residents over 65 soared from 9% in 1829 to 54% in 1923, even though they remained only 5% of the population.[6] An institution designed in an era of near-universal poverty, as a safety net of last resort to catch those whom no one else would be willing to house, was in an age of affluence becoming a cruel but unavoidable general home for the elderly.

Deeming the “inability to perform remunerative work” the cause of rising poverty amid plenty, progressive-era reformers around the world sought to take advantage of rising prosperity by establishing state-subsidized “social insurance” schemes against the “hazards which constantly threaten to deprive the family of a wage worker of the continuous flow of wages.”[7] Principal among these hazards was old age—which one turn-of-the-century reformer described as “disability under another name, the final and certain phase of it.”[8]

Governments established pension systems for the elderly in Germany in 1889, Denmark in 1891, New Zealand in 1898, Britain and Australia in 1908, and Canada in 1927.[9] In 1927, Abraham Epstein established the American Association for Old Age Security to push legislators “to guarantee the wage-earner and his dependents a minimum of income during periods when, through forces largely beyond his control, his earnings are impaired or cut off.”[10] He coined the term “Social Security,” published a magazine under that name, and renamed his organization the American Association for Social Security in 1933.[11]

The 1942 Beveridge Report, discussing the principles of Britain’s welfare state, declared: “The first fundamental principle of the social insurance scheme is provision of a flat rate of insurance benefit, irrespective of the amount of the earnings which have been interrupted by unemployment or disability or ended by retirement.”[12] Britain maintained this principle, and it was also adopted in Canada and elsewhere in the English-speaking world following World War II. This allowed America’s northern neighbor to guarantee a considerably higher minimum benefit to its elderly than the U.S. would achieve.[13]

From the outset, the Social Security Act of 1935’s Old Age Insurance (OAI) benefit was structured differently and provided higher benefits to those who had previously earned more. Edwin Witte, Social Security’s chief architect under President Franklin Roosevelt, conceded that the “administrative difficulties would be materially lessened if we had a flat-rate benefit system like that of England.” But Witte noted in a 1937 essay that “flat benefits, without regard to earnings, do not appeal to many Americans who are accustomed to wide differentials between urban and rural areas and in different parts of the country between occupations and races.” As a result, he deemed it “probably impossible to establish in this country as simple an old-age insurance system as prevails in England.”[14]

At the state level, Colorado and Washington both adopted universal flat pension schemes, but regional differences across the U.S. were indeed substantial.[15] In 1929, the per-capita income in Massachusetts was $912, but only $287 in Mississippi.[16] Race was an even bigger obstacle in an era where segregationist Southern legislators controlled key congressional committees and fought to avoid the establishment of entitlements to equal federal aid for blacks and whites.[17]

The new OAI system also relied exclusively on payroll taxes—contravening international precedent, the opinion of economists from across the political spectrum, and the pressure of public opinion. It had not been part of the initial design for Social Security, but Treasury Secretary Henry Morgenthau, who was wary of the impact of long-run deficits on the gold market, insisted upon it. At a time when half of workers were excluded from eligibility for OAI benefits because their employment arrangements were not covered, a payroll tax also was an appealing method of limiting payment for the program to those who might eventually draw some advantage from it.[18]

These political compromises led to a furious response from Epstein, who protested in 1933 that “the extensive use of payroll taxes for old age and unemployment insurance not only defeats the very purpose of this legislation, but tends actually to aggravate existing insecurity.”[19] Not only would payroll taxes encourage layoffs and discourage wage increases, but they would relieve “those in the higher income brackets from their share of the social burden of old age dependency which through the poor laws they have helped to carry for centuries”—concentrating the burden of aiding the elderly poor on the working classes.[20]

Epstein noted that “during the first year of lump-sum payments, while persons who were probably in great need received benefits of but a few cents or a few dollars, one New York executive who worked for seven corporations simultaneously (and continued to do so) received $1,001.67 upon reaching the age of 65.”[21] By contrast, “most workers will not receive an annuity adequate to their needs for almost a generation,” and typical farm laborers after 20 years of work would receive benefits of half the levels that they stood to receive without payroll tax contributions under traditional public assistance.[22]

Even though the system was designed to provide slightly lower returns to contributions made by higher-income beneficiaries, because benefits would phase in faster than taxes, the system would redistribute more from later to earlier generations than from rich to poor. Whereas Epstein estimated that a high-income 60-year-old would receive three times more from OAI than by investing his payroll tax contributions in a private annuity, a low-income 20-year-old was projected to receive less.[23]

Epstein noted that the accumulation of trust fund reserves would not generate the returns on investment that had been promised by the Roosevelt administration, so payroll taxes would need to be increased from 6% to 10%. He predicted that funds would be invested in low-interest federal bonds and merely serve as a regressive method of subsidizing general government debt. This would “give tremendous impetus towards increasing the political pressure for benefits larger than socially necessary and beyond the country’s capacity to sustain.”[24]

In 1938, OAI took in $402 million of tax revenue, but spent only $5 million on benefits—a surplus worth 0.5% of GDP, which Epstein argued bore much responsibility for the 1937–38 recession.[25] After Republicans surged in the midterm elections of 1938, they insisted on restructuring the program to eliminate the accumulation of reserves, which they feared would lead to government control of economic investment. Democrats, who feared Americans would shun the program as a terrible deal, agreed to bipartisan legislation to abandon the accumulation of reserves and pay out benefits immediately.

Congress in 1939 turned OAI into a pay-as-you-go program—ditching the attempt to maintain a fixed proportion between benefits and workers’ prior contributions through the accumulation of a reserve.[26] This made the program potentially highly redistributive, without institutionalizing any specific principle to guide redistribution other than the vagaries of political convenience.

After rapid wartime inflation whittled away the real value of contributions already made, the newly elected Democratic Congress in 1950 sought to bail out the system. It hiked benefit payments by 77% (splitting the difference between House and Senate proposals) and increased payroll tax rates across the board, but raised the cap on the payroll tax by only 20%—making the program an engine of enormous redistribution toward earlier generations.[27]

The Social Security Amendments Act of 1950 transformed the program from an unpopular tax linked to a distant promise of meager benefits (which inflation was wiping out) into a seemingly phenomenal return on investment (which no honestly conducted private business could promise). The first generation of retirees under the program would receive a guaranteed return more than 12 times that to be had by investing in Treasury bonds.[28]

Originally, the theoretical bases for Social Security were as a form of insurance and as a safety net for old age. These were abandoned for a new logic, which justified the indiscriminate bloat of the Old-Age, Survivors, and Disability Insurance (OASDI) program as offering individuals at all income levels a good return on investment.[29]

Economist Paul Samuelson argued that so long as the growth of wages and population exceeded the rate of interest, a pay-as-you-go pension system could provide each person with larger retirement benefits than they contributed in payroll taxes.[30] “A growing nation,” Samuelson boasted in Newsweek in 1967, “is the greatest Ponzi ever contrived”—and he predicted that these trends would continue “as far ahead as the eye cannot see.”[31]

That unbridled optimism exacerbated neglect of the net redistributive effect of the program, which economists in the 1960s found impossible to calculate.[32] But it was music to the ears of the post–World War II generation of politicians, who used it to justify the expansion of benefits, funded by the escalation of regressively structured payroll taxes, which would only fully phase in 20 years later (Figure 1).[33]

Figure 1

OASDI Payroll Tax Rates, Revenues, and Expenditures by Year

Rapid economic growth in the decades after World War II generated unanticipated windfalls that made the generous expansion of benefits seem justified under the new logic.[34] This was augmented by the expansion of the program to cover new groups of workers, such as farmers and the self-employed, who would contribute payroll taxes without claiming benefits for many years to come. That was also true of the influx of women into the workforce.

Over time, Congress became accustomed to election-year bidding wars between the parties to hike benefits to make up for inflation and share the proceeds of economic growth with seniors. After compounding benefit increases of 15% in 1969, 10% in 1971, and 20% in 1972 suggested this competition was getting out of hand, Congress and the Nixon administration agreed to legislation that would automatically increase benefits in line with inflation.[35]

By the early 1970s, the program was reaching maturation. The proportion of the elderly entitled to benefits began to approach the share of covered workers contributing to payroll taxes.[36] As it came time to pay out the promised benefits, each of Samuelson’s assumptions quickly fell apart. The general rate of inflation surged beyond the rate of wage growth—causing the program’s costs to compound beyond its payroll tax revenues.[37] Rising unemployment further reduced payroll tax revenues.[38] Demographics also became a problem. As birth rates declined and life expectancy increased, the ratio of workers to retirees declined from five to one in 1960 to three to one in 1980—and the Social Security Administration projects the ratio to fall further, to two to one, by 2040.[39]

In 1975, Social Security’s trustees estimated that the Old-Age & Survivors Insurance (OASI) program, which pays retirement and survivor benefits, would be bankrupt within five years. The Democratic Congress responded in 1977 by hiking payroll tax rates by 25% and raising the cap on taxable income.[40] This quickly proved inadequate as inflation and unemployment surged, and real wages continued to move in the wrong direction. In 1983, a divided Congress made up the shortfall with a package relying more on benefit cuts, phased in over the next four decades.[41]

Since 2009, the OASDI program has received less in tax revenues every year than it has paid out in benefits, and the annual deficit is projected to steadily widen, so the trust fund will be entirely depleted by 2034.[42] By 2040, the cost of paying benefits every year will exceed payroll tax revenues every year by 26%, with the annual disparity projected to continue rising to 36% in 2075.[43]

Social Security Today: Weak Protection and a Bad Deal

U.S. private-sector workers are subject to a 12.4% payroll tax on earned income up to a cap ($147,000 in 2022), whose revenue is reserved for funding OASDI benefits. After 10 years of contributions, covered workers become entitled to receive monthly OAI payments from the age of 67 until they die, after which their dependents may become entitled to smaller monthly Survivors Insurance (SI) payments. Individuals can begin receiving monthly OAI benefits earlier, from the age of 62, or later, from the age of 70, with a proportionate adjustment to benefit levels.[44] After a smaller number of payroll tax contributions (typically 5 of the previous 10 years), individuals under 62 can qualify for monthly Disability Insurance (DI) payments if they are deemed “unable to engage in substantial gainful activity” for at least a year or if the disability is expected to result in death (Table 1).[45]

Table 1

Social Security Overview as of April 2022

Regardless of prior payroll tax contributions, Americans are eligible for Supplemental Security Income (SSI) payments of $841 per month if they are 65 or older, blind, or disabled, with incomes and assets below official thresholds. SSI payments are reduced dollar-for-dollar for any other sources of income, such as OASDI.[46] SSI payments are not funded out of Social Security taxes or trust funds.

Benefit levels for OASDI are related to average career earnings. The amount a single person would receive if he or she begins receiving retirement benefits at the full retirement age (Americans born in 1960 and later have a full retirement age of 67) is called the primary insurance amount (PIA) (Figure 2).[47] Monthly OASDI and SSI benefit payments are automatically increased in line with inflation every year. Dependents of living OASDI beneficiaries may be entitled to additional payments.[48]

Figure 2

How Standard OASDI Benefits (PIAs) Are Calculated

As a result of this arrangement, those who have earned the least over their careers receive the smallest monthly OASDI benefits. The maximum monthly Social Security benefit that higher-income Americans could receive is roughly three times greater than the benefit that would be received by an individual who had worked for at least 35 years full-time at the minimum wage. Offsetting that, the higher-income American’s average monthly payroll tax contribution would have been roughly 10 times higher than the minimum wage worker’s contribution.

Yet additional factors mean that OASI (retirement and survivors’ components of OASDI) now typically even redistributes away from low-income households.[49]

Average lifetime earnings do not directly correspond to wealth in old age. Average lifetime earnings are often greatly reduced by time taken out of the labor force for higher education, to be homemakers, or for government jobs, which are not covered by the OASI system. Due to additional payments for spouses, the OASDI benefit formula is hardwired to provide a higher ratio of monthly benefits to monthly contributions for high-income single-earner couples than for low-income single-person households.[50] This skews the program’s redistributive effect to wealthier households since marriage rates among middle- and upper-class adults are more than twice as high as among poor adults.[51]

As a result, more than half of the progressivity of the OASI monthly benefit formula disappears when income is assessed on a family basis rather than an individual basis. Among similar two-worker households, there is very little redistribution from high to low earners.[52]

Furthermore, wealthier individuals tend to live longer and therefore receive many more monthly OAI and SI payments. For instance, the life expectancy of the wealthiest quintile of men reaching 50 and born in 1960 is 12.7 years longer than that of the poorest quintile.[53] This gap has grown over recent years to more than offset the progressivity of the benefit formula—redistributing income away from relatively poor households within the baby-boom age cohort.[54] African Americans tend to lose on balance due to relatively shorter life expectancy and lower marriage rates, while Hispanics lose even more because they are more concentrated in younger birth cohorts.[55]

OASI’s most systematic redistribution is toward early generations of beneficiaries, away from current generations, including most of the poor. While initial cohorts of retirees obtained a fantastic deal from Social Security, receiving benefits greatly in excess of prior payroll tax contributions, subsequent generations were required to pay for the largesse to the initial beneficiaries as well as their own benefits. Americans reaching 65 since 1997 are scheduled to receive less than they paid in—even if they don’t pay a penny to make up the program’s current deficit. The ratio of benefits to tax contributions, which was 12 to 1 for the generation born prior to 1901, has fallen to 0.7 to 1 for those born in the 1950s (Figure 3).[56]

Figure 3

Lifetime Benefit-to-Tax Contribution Ratio of OASI by Birth Cohort

In most cases, redistribution within generations falls short of making up for redistribution toward the initial cohort, so most Americans will receive less from OASI than they paid in, regardless of their income levels (Figure 4).[57]

Figure 4

Lifetime Benefit-to-Tax Contribution Ratio of OASDI by Income Percentile—1960s Birth Cohort

In 2006, the Congressional Budget Office noted that “the progressivity of Social Security is driven mainly by disabled-worker and auxiliary benefits.”[58] (Auxiliary benefits are payments to eligible relatives of covered workers.) DI benefits go to people earlier in their life, when they have contributed less in payroll taxes, and are distributed disproportionately to low-income workers, who tend to work in more physically demanding professions and stand to lose less income by dropping out of the workforce.[59] Eligibility for DI requires the cessation of “substantial gainful activity” and is therefore inherently correlated with lower career earnings.

The absence of significant net redistribution to the poor by OASI is still more striking when the availability of other potential sources of assistance to the needy is considered. Even by the late 1970s, when OASI still offered a positive return, low-income working seniors received net benefits that were barely higher than those then provided by SSI, after payroll tax contributions are considered.[60]

The payroll tax increased over time and falls heaviest on low-income working Americans. In 2017, the poorest quintile paid 9.4% of its income in payroll taxes, while the highest quintile paid only 6.5%. By contrast, SSI is funded primarily through the federal income tax, which imposes no net burden on the poorest two quintiles but takes 16.6% from the highest-earning quintile.[61]

OASDI’s dependence on prior contributions means that it does little to help the poorest Americans, who have often been kept out of the labor force by the most severe and prolonged cases of disability. Around 20% of American seniors in the poorest income quintile are ineligible for OASDI benefits, while a third of those who do qualify receive retirement benefits less than the federal poverty level.[62] In 2012, the income of seniors in the poorest decile came 30% from SSI and 55% from OASDI, even though federal spending on OASDI was more than 17 times greater than on SSI, and SSI payments themselves averaged only 56% of the federal poverty level (Figure 5).[63]

Figure 5

Income Sources of Americans Age 65+ in 2012 by Decile

The separate growth of OASDI has likely drained political support and resources that otherwise would have flowed into bolstering the floor on retirement income provided by SSI—and aided the poor in a more effective and targeted way. When SSI began in January 1974, the average monthly OASI benefit for retired workers was only 19% higher than the federal SSI benefit for individuals. Because OASI increases in line with wage growth as well as inflation, by 2021, the average OASI benefit was 111% higher than SSI.[64]

Figure 6

Share of Average Disposable Income Transferred as Net Benefits in Western Europe

![]()

Bloated publicly financed retirement benefits for the middle class serve both to inflate taxes on lower-income workers and to draw funds away from programs that are targeted at aiding the poor. A 2021 study by the European Commission’s Joint Research Centre found a close negative correlation between the amount that nations redistributed to wealthy retirees and levels of assistance, net of taxes, to the working poor (Figure 6).

Figure 7

Disposable Income for Adults Age 65+ in OECD Countries

American seniors enjoy the highest median incomes of any nation, but the nation’s elderly poor fare much worse (Figure 7). According to the Census Bureau, 9% of Americans over 65 lived on incomes less than the poverty line in 2019. The rate was even higher among seniors who were 80 and older (11%), unmarried (15%), or black (20%).[65] This is because America’s public pension system is poorly focused on those in need: 64% of OASDI’s expenditures went to seniors with incomes above the median.[66]

Table 2

Pensions Systems Comparison

The maximum benefit that OASDI provides to the wealthiest seniors is two to three times higher than that under national pension systems in Australia and Canada.[67] But the disposable income of the poorest decile of seniors in the U.S. is considerably less—even though those nations have lower levels of GDP per capita and spend a substantially smaller share of it on public pensions for retirees (Table 2).[68]

There is little need for the state to redistribute from the young to upper-income seniors. Affluent households do not just have an ability to save and invest to provide for old age; they can purchase durable goods (such as housing), annuities, and various forms of private insurance to spread incomes to retirement and defray longevity risks where they are given the responsibility for doing so. In 2019, while the median income of American households headed by adults over 75 was slightly lower than that for adults younger than 35 ($43,100 vs. $48,600), their median net worth was much higher ($254,800 vs. $14,000).[69]

By ensuring a stream of income in retirement, public pensions are estimated to reduce personal savings nearly dollar-for-dollar—with crowd-out concentrated among higher earners, who have the capacity to save and invest.[70] This lowers overall social welfare by diminishing capital accumulation, productive investment, and the creation of good-paying jobs. Furthermore, every $1 of payroll taxes collected is estimated to cost $1.50 to the economy through reduced labor supply.[71] Providing elevated benefit levels further reduces work and economic output, particularly by hastening retirement.[72]

OASDI is currently very difficult for people to plan around. Few Americans understand how their future benefits are calculated, most greatly overestimate the impact of increased earnings on future benefits, and the majority have little sense of the magnitude of the payments they will receive in retirement.[73] It is clear the U.S. needs a better system.

Building Better Security

Federal law prohibits the payment of full Social Security benefits after the trust fund is depleted,[74] and 84% of American adults expect the program to be unable to pay currently promised benefits when they retire.[75]

Because the budget reconciliation process cannot be used to alter Social Security, bipartisan legislation will likely be required to continue delivering payments as promised.[76] Additional aid will surely be provided for existing retirees. But working taxpayers and their elected representatives will want to ensure that they are getting good value for the additional money. What reforms should they demand in return?

Proposal: Reliable Predictable Security

A new Reliable Predictable Security (RPS) option should be established, allowing adults under 45 to forgo higher OASDI benefits in return for an increased minimum OASI benefit and a 5-percentage-point reduction of the employee-side payroll tax.

The PIA for all beneficiaries opting for RPS would be set at 125% of the federal poverty level ($16,988 in 2022)[77] and subsequently increased in line with the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), a measure of inflation.[78]

All legal permanent U.S. residents would be eligible to receive this benefit after meeting the current OASI eligibility criteria of 10 years of contributions. The PIA would be reduced for those with fewer than 40 years of legal residency, in proportion to the amount of years they have not been present filing U.S. taxes. As under the current system, OASI benefits under RPS would be reduced proportionately for early retirees.

|

Reliable Predictable Security (RPS) Option Adults under 45 may opt in to receive: • Uniform OASI benefit (at 125% of federal poverty level, $16,988 in 2022) • DI benefits capped (at 125% of federal poverty level, $16,988 in 2022) • Benefits indexed by CPI-W • OASI tax reduced by 5 percentage points |

Dependents of workers opting for RPS would also retain additional eligibility for up to 50% of workers’ benefits—though elderly spouses’ own benefits would likely be higher in a larger proportion of cases, such that this option would be exercised less frequently. Eligibility for survivor benefits would similarly remain, but would be calculated as a proportion of the RPS system’s uniform PIA.

DI benefit levels would remain tied to prior contributions and subject to current restrictions on eligibility, but would become capped at the uniform RPS benefit level.

Newly hired state and local government workers under 45 at the time of the system’s establishment would be made eligible for RPS old-age and survivor benefits and subject to a 7.4% payroll tax. All other workers opting for RPS benefits would benefit from a 5-percentage-point reduction of the current OASI payroll tax.

Justification

Social Security offers value to the extent it combines insurance, paternalism, and redistribution to prevent households from falling into poverty due to the old age, death, or disability of the breadwinner.[79] However, the present OASDI system fails to secure this guarantee against poverty in old age, while providing unnecessarily higher benefits for more affluent retirees, which inflates payroll taxes and crowds out private provisions for retirement by those able to take it upon themselves.

The uniform OASI benefit under the proposed RPS option would provide a stronger guarantee against falling into poverty due to the old age or death of the head of a household. And it would establish an income floor at a monthly benefit more than twice the current value of SSI, without restrictions on other incomes or assets.[80] Being indexed to the cost of living rather than to wages, benefits would remain focused on this core purpose and protected from partisan politics by the Byrd Rule, which prohibits legislation crafted in the reconciliation process from making changes to Social Security.[81]

The provision of a well-known and understood benefit level would make it easier for beneficiaries to plan additional provisions for retirement. This greater uniformity would also help make the system less vulnerable to wage, unemployment, and demographic shocks.

The present link of DI benefit levels to prior contributions is justified insofar as they allow an asset-test-free benefit of higher income to be provided to disabled adults of working age, without the system becoming an open-ended handout. But there is no need for Social Security to provide additional higher benefits to relatively affluent individuals, as the more accurate disability determination systems of private DI are able to generate significantly greater benefits at half the cost.[82]

SSI would remain as under present law, though its enrollment would likely be greatly reduced, as the higher generosity of RPS benefits would mean that fewer elderly Americans and their dependents would have income and asset levels low enough to qualify.

No substantial reason remains for providing above-average benefits to those with higher prior earnings histories, beyond the ill-founded belief that they have previously been paid for. As this sentiment frustrates attempts to directly reform benefit levels, it can be accommodated by allowing people to pay proportionately lower taxes during their career in return for eliminating above-standard benefits when they reach old age or become disabled.

Eligibility for RPS benefits should be limited to individuals who opt in before the age of 45, to prevent opportunistic participation or nonparticipation according to anticipated personal OASDI benefit levels. This limit would also make sure that payroll tax revenues from higher-earning older cohorts of workers continue to support existing OASDI benefits during a transition phase before beneficiaries predominantly claim standard benefits. Beyond then, it would provide younger workers who are foregoing higher benefits in the future with an opportunity to accumulate private savings and investments to more than make up for them.

This arrangement is preferable to carve-out private accounts in OASI by avoiding the “double-payment problem” associated with paying already promised, pay-as-you-go benefits while also establishing private reserves. It would set a guaranteed income for seniors above the poverty level and would avoid incurring a liability to regulate or bail out private investments. But this reform would also increase work incentives, reduce regressive taxes on the young, and increase the resources that households could privately control, save, and invest.

Cost Considerations

The cost of establishing an RPS benefit option cannot be precisely estimated without a model of the complex provisions of the OASDI program, its dynamic impact on private economic choices and tax revenues, and its effects on eligibility for other public entitlements. Yet a ballpark estimate of the magnitude of potential savings when fully phased in, and an understanding of the cost implications associated with full adoption, can be produced by adjusting the OASDI Trustees Report’s projected estimate of program costs for proposed changes in benefit levels (Table 3).

The impact of a full immediate switch of all beneficiaries to RPS is therefore estimated before considering complex additional factors associated with the transition, which would initially limit eligibility and skew the appeal of the new option.

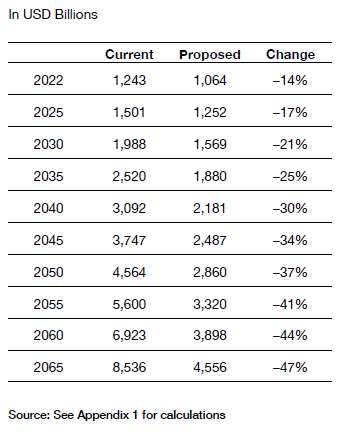

Table 3

Annual OASDI Expenditures if All Benefits Are on RPS

A full immediate switch to RPS benefits would be expected to reduce OASDI expenditures by 14% in the first year, with increased benefits for low earners offsetting much of the savings from reduced benefits for higher earners. However, savings from the switch to RPS would grow to be much more substantial over time, as expenditures on benefits increase according to inflation, without additional upward adjustment for wage growth. Younger workers would benefit for more years from the reduction of the payroll tax, but they would also give up the most in terms of the absence of higher wage-indexed benefits.

If all retirees after 2060 were enrolled in RPS, savings to Social Security would amount to more than 44% of OASDI costs—enough to pay for a 5-percentage-point cut to the OASDI payroll tax.[83] The magnitude of the proposed OASDI payroll tax cut to be obtained by switching to the RPS option should be calibrated to take full account of the dynamic effects of this change (e.g., if the tax on work is cut, employment would increase, offsetting some of the revenue loss) so that the long-term net reduction in expenditures would balance the long-term net reduction in revenues.

Any change in benefit levels, eligibility, payroll taxes, or general revenues to balance OASDI’s annual revenues and expenditures should be considered separately from the transition to RPS and applied to both RPS and the traditional benefit on actuarially equivalent terms. If all of OASDI’s currently promised benefits were covered by increasing taxes, those remaining in the traditional option would pay the full tax increase, while most of those opting for RFS would still enjoy a net tax reduction.

Impact Scenarios

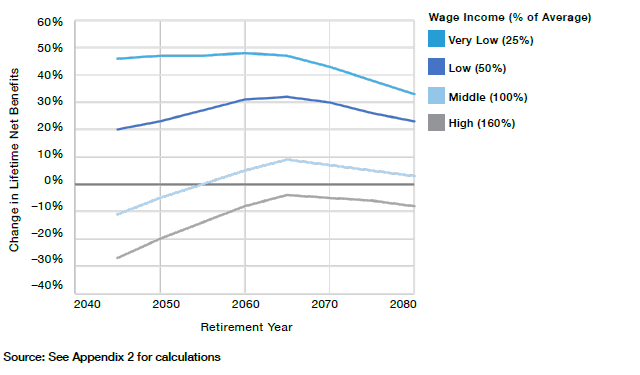

For modeling purposes, the RPS option and associated payroll tax cut are assumed to become available from 2022. Individuals 45 and older would not be able to opt for RPS. But many median- and higher-earning individuals aged 30 to 44 (i.e., reaching the age of 67 before 2060) would also initially likely opt against RPS, because the value of future benefits forgone would substantially exceed the potential gain from a payroll tax reduction during their remaining years of employment (Figure 8). Low earners retiring in any year would profit from increased benefits as well as reductions in the payroll tax by opting for RPS.

Figure 8

Projected Change in Benefit Levels for Single Adults Opting for RPS Over OASDI by Income and Year Turning 67

Participation in RPS would therefore be expected to be limited to lower earners and younger workers in its early years. This would likely reduce much of the up-front payroll tax revenue loss from the transition. Nonetheless, even though higher-earning households retiring after 2060 might see reductions of benefits that slightly exceed the payroll tax cuts they gain by opting for RPS, the disparity would likely be more than offset by the perceived value of greater control over earnings and investment options. All Americans reaching 67 after 2060 are therefore assumed to participate.

Reductions in spending from the transition to RPS would lag reductions in payroll tax revenues because no benefits would be paid at RPS levels until 2045, and those subject to the most substantial potential benefit cuts would not be among the early adopters. But over time, as the number of years subject to payroll tax cuts increases and the proportion of high earners opting for reduced benefits under RPS rises, so the maturation of benefit cuts would generate net fiscal savings. We can call these savings the “RPS option net fiscal impact” (Figure 9).

Figure 9

Projected Fiscal Impact of RPS Package and Transition

![]()

With (1) a tax increase to bring the existing OASDI system into annual fiscal balance and (2) the establishment of the RFS option, the net impact of such a legislative package deal would be expected to increase the federal budget deficit by no more than 0.2% of annual GDP at its peak and to eventually reduce it by 2.8% (“Fiscal impact net of solvency tax hike,” Figure 9).

As with the Social Security Amendments of 1983, the net impact of such a package deal on the size of government would be deliberately open to interpretation. That would allow Democrats to claim that they are making OASDI solvent through revenue increases without cutting any benefit promises previously made, while Republicans could claim that they are reducing the long-term net tax burden on anyone who wishes to avoid it.[84]

Conclusion

“Social security is not something that can ever be devised once and for all,” Edwin Witte noted in 1948. “What is a sound program for social security depends upon the conditions prevailing in a given nation at a given time”—specifically “both economic and political considerations.”[85] The nation’s economic, regional, and racial relations have changed enormously, making possible policy approaches that the program’s early advocates saw as initially more desirable but were then practically unattainable.

Political constraints in the mid-20th century meant the OASI program was excessively regressive at the outset, and this tendency has been exacerbated over much of the subsequent three-quarters of a century. Now the program has become so bloated and inflexible that it serves neither insurance nor investment purposes in a cost-effective manner.

Entitlements are hard to reform, as voters resist changes to benefits they believe they have paid for and expect to receive in the future.[86] Social Security therefore cannot be made a more cost-effective form of protection against the risks of poverty in old age, disability, and death simply by altering benefit levels. But its trajectory can be altered over time through the infusion of new principles.[87] Medicare Advantage has demonstrated that it is possible to establish a new benefit option, which internalizes the advantages of more cost-effective insurance arrangements in Medicare, so individuals can opt for it voluntarily.[88] The same can and should be done for Social Security.

About the Author

Chris Pope is a senior fellow at the Manhattan Institute. Previously, he was director of policy research at West Health, a nonprofit medical research organization; health-policy fellow at the U.S. House Committee on Energy and Commerce; and research manager at the American Enterprise Institute. Pope’s research focuses on health-care payment policy, and he has recently published reports on hospital-market regulation, entitlement design, and insurance-market reform. His work has appeared in, among others, the Wall Street Journal, Health Affairs, U.S. News & World Report, and Politico.

Pope holds a BSc in government and economics from the London School of Economics and an MA and PhD in political science from Washington University in St. Louis.

Acknowledgment

Thanks to Andrew Biggs for many thoughtful comments and assistance with modeling transition scenarios.

Appendix 1. Cost Savings Estimates by Year

Appendix 2. Scenario Calculations

Appendix 3. Phased-In Fiscal Impact Projections

Endnotes

Photo: Bill Oxford/iStock

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).