e21 Asks: Economic Growth Industries

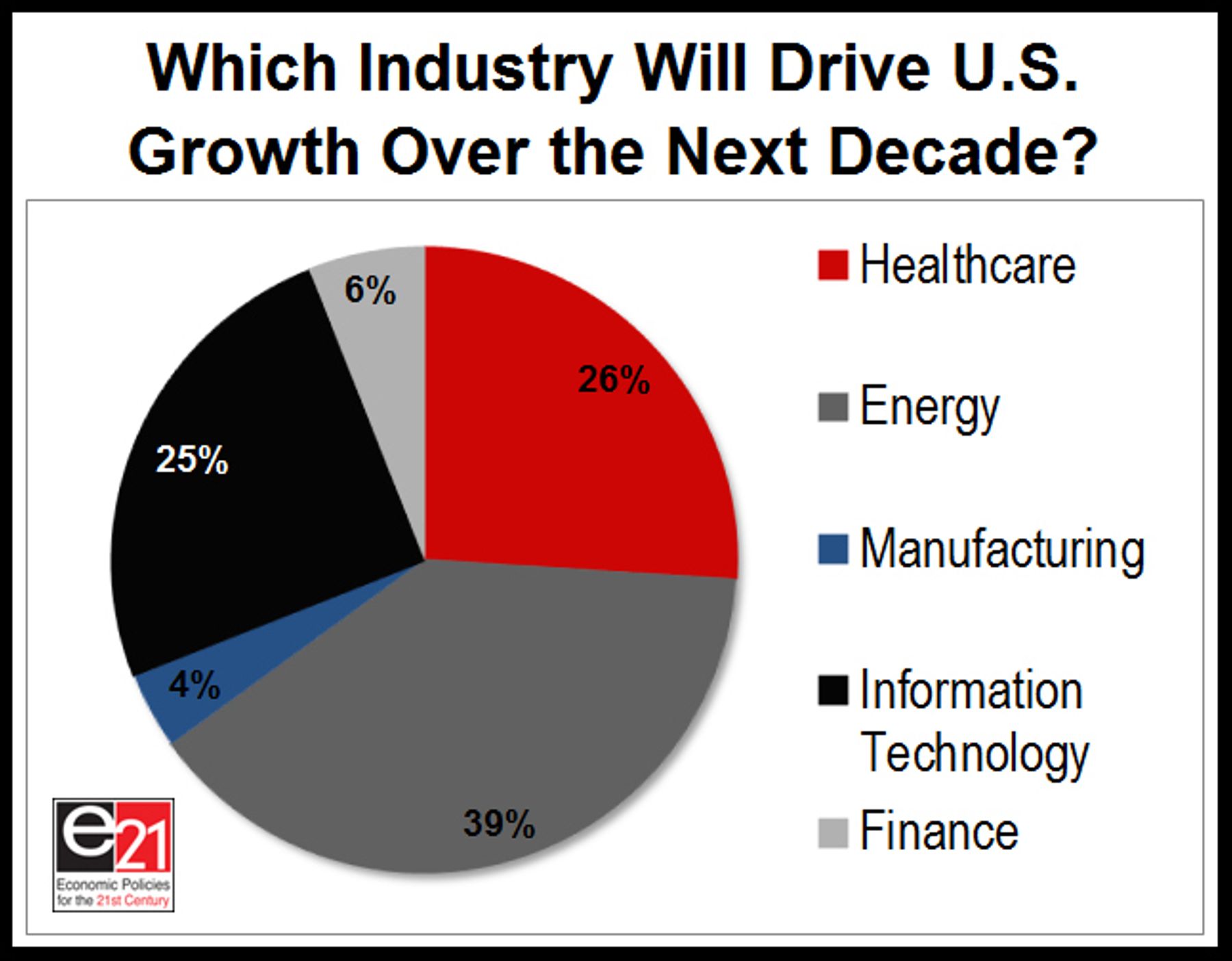

This week we asked e21 readers the following: “Which industry will drive U.S. growth over the next decade?” The most popular response was “energy” which received 39 percent of votes. “Healthcare” and “information technology” both received about a quarter of reader responses. “Manufacturing” and “finance” each received less than five percent of votes.

We agree with our readers that energy production will be the main driver of economic growth in the coming years. The information technology and finance industries are also both essential to economic growth as they facilitate investment that spurs growth Manufacturing is important, and advanced manufacturing is playing a vital role in the American economy. However, it is unlikely that America will return to the manufacturing-based economy of the 1950s. As healthcare costs continue to slowly grow, innovation is essential if the United States is to reach a fiscally-sustainable path.

The United States is in the midst of an energy renaissance, and is projected to be the world’s top oil producer by the end of next year. It is already the world’s largest natural gas producer.

This energy boom is propelled by advances in drilling technology, including hydraulic fracturing and better information systems that increase efficiency. Information technology allows for less waste during the drilling process and new ways to reach previously inaccessible reserves.

Without the $300-$400 billion annual growth in the oil and gas industries, U.S. GDP might well have been negative over the past four years. Access to cheap, reliable energy has had positive ripple effects into other industries, drawing energy-intensive manufacturing from across the globe.

Energy is also a bright spot in the bleak U.S. employment picture. Though overall employment is yet to reach pre-recession levels, employment in the oil and gas sectors has increased 40 percent since 2007. One million Americans now work directly in the oil and gas industry, and ten million additional jobs are associated with the industry. If this growth is allowed to continue, analysts project 3-4 million additional jobs will come from increased domestic hydrocarbon production.

The era of factory jobs as anchors of the middle class is over. In the early 1940s, 39 percent of employment was in manufacturing. This rate has gradually declined down to its current 9 percent. The decline has occurred even as the sector's productivity has grown, as factories switched from human workers to more robotic, automated production.

According to the Center for Medicare & Medicaid Services, national health expenditures as a percentage of GDP have grown over the past two years and will continue to grow in 2014 and 2015. However, the growth of health care expenditures is much slower than projections had been three and four years ago. Projections made in 2009 and 2010 showed health expenditures as a percentage of GDP would rise above 19 percent by 2016, but a September 2013 projection showed 2016 health expenditures well below 19 percent of GDP. Obamacare had no responsibility for the reduced projection – the CMS actually said its projections would be even lower had Obamacare not been implemented.

The financial sector contributed more than a trillion dollars to GDP in 2012, about seven percent. The finance sector helps economic growth in many ways that are not easily seen by the general public. When a small business needs liquidity to jumpstart production, the financial sector steps in. It is unclear how much the Dodd-Frank legislation will discourage lending. Even though the financial sector may not be directly responsible for as much economic growth as the energy sector over the next decade, finance is still a crucial sector for business and securing stable retirement savings.

Similar to finance, technological progress is important for growth in all sectors of the economy. Whether in finance, energy, healthcare, manufacturing, or other sectors, innovation is constantly required to maintain steady growth. Trumpeted by Joseph Schumpeter, this “creative destruction” of old methods replaced by new keeps every business on their feet—if a business does not adapt to changing marketplaces, it will become obsolete. All sectors of the economy needs to find new ways to use technology to improve products and services.