Better to Split Up than Prop Up Troubled Multiemployer Pension Plans

Congress’s Joint Select Committee on Solvency of Multiemployer Pension Plans is due to consider recommendations by the end of this month. The chief problem the committee faces is that the impending insolvency of several private-sector multiemployer pension plans is projected to drive the pension insurance program of the Pension Benefit Guaranty Corporation into insolvency as well. This situation threatens U.S. workers’ vital pension benefits, as I explained in my last piece, where you can also find more background information on multi-employer pensions and the crisis they face.

The committee is between a rock and a hard place, as there is no obvious path to stabilizing multiemployer pensions. On the one side, sponsors of underfunded plans are demanding an expensive, taxpayer-financed bailout. Such a course is ill-advised for several reasons: first, it would be vastly expensive (between $30-$100 billion over the first ten years alone, depending on how many plans receive assistance); second, it would establish a terrible precedent and incentives for future bailouts (potentially spreading to state/local public plans); third, the problem’s origin lies in pension sponsors’ own failures to accurately measure and fund their benefit obligations.

“A taxpayer-financed bailout would be vastly expensive, set a terrible precedent and fail to address sponsors’ own failures to accurately measure and fund their obligations.”

On the other hand, doing nothing is also irresponsible, as it would lead to pension insurance insolvency and the loss of crucial worker benefits. Moreover, at this late stage of the crisis, many plans are so dramatically underfunded that if legislation is limited solely to requiring that sponsors fully fund their pension obligations, many sponsors will simply terminate their plans and dump their unfunded liabilities on the PBGC. Legislators therefore have little choice but to consider creative alternatives to these different paths to disaster.

One idea being pushed aggressively by the sponsor community is actually no solution at all, and should be taken off the table as soon as possible: namely, propping up insolvent multiemployer plans with taxpayer-financed loans. To put it bluntly, the loan approach is unfair, irresponsible, and it wouldn’t work. Such loans would essentially be a continuation of ill-considered policies that to date have failed, and would only cause the costs of pension underfunding to soar still further.

“Taxpayer-financed loans to prop up insolvent plans are unfair, irresponsible, and a continuation of failed policies that would only cause the costs of underfunding to soar still further.”

The basic framework of these loan proposals is that taxpayers would lend money to troubled pension plans at subsidized (below-market) interest rates. Then, instead of accurately measuring their benefit promises and aligning them with what employers’ contributions can actually fund, sponsors would gamble on high investment returns rescuing the plans. Advocates are blunt as to what is intended: “The entire premise of the loan program is to allow a Plan to borrow enough money at 1% and invest at a higher rate that will allow the Plan to earn their way through the funding problems that they face.”

The loan approach is a terrible idea. For one thing, no responsible lender would make this deal. Even in the unlikely best case scenario in which the pension pays back the loan, taxpayers would still lose because the interest rate charged would be well below the government’s own borrowing costs. Second, instead of sponsors being required to responsibly address imbalances between their inadequate contributions and their excessive benefit promises, they would be given an incentive to take irresponsible investment risks -- receiving the upside if those risks pay off, while sticking the taxpayer with the cost if they don’t. Third, these plans are in such deep trouble that any such loans likely wouldn’t be paid back.

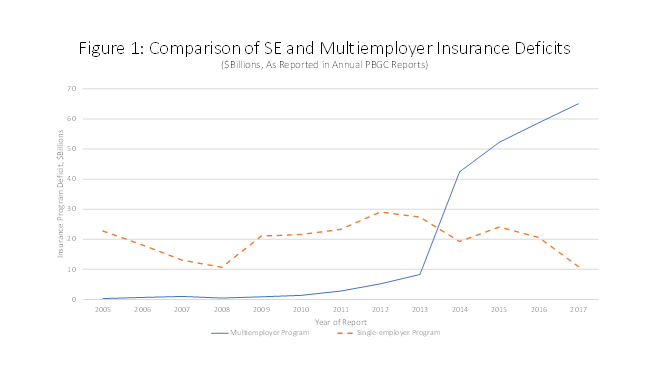

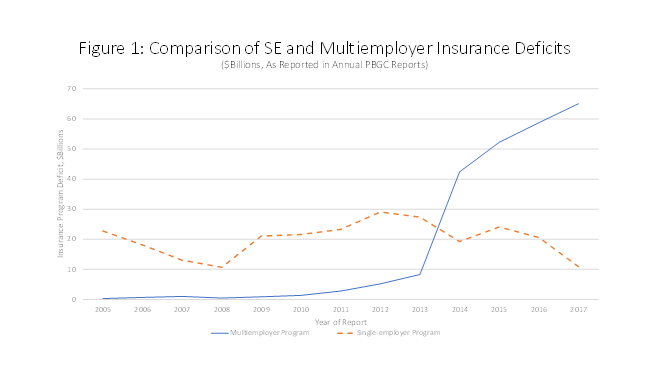

Significantly, current policy has in effect already implemented the loan approach, and it hasn’t worked. Under current law, when a multiemployer plan becomes insolvent, the financial assistance it receives from PBGC comes in the form of a loan – and is in practice almost never repaid. Moreover, the 2006 Pension Protection Act (PPA), while reforming the funding rules for single-employer plans, basically gave many multiemployer plans a pass on making sufficient contributions to become adequately funded, permitting them to gamble by chasing investment windfalls instead. The result has been that the shortfall in the multiemployer insurance program has grown at the same time the single-employer program has stabilized (Figure 1). A larger loan program would simply continue and expand the recent failed policy approach to a much greater, vastly more expensive scale, causing multiemployer plan underfunding to further metastasize.

Even preemptively terminating insolvent multiemployer pension plans would be preferable to a loan program. Such terminations would cause great hardship for affected workers, who would lose any benefits exceeding PBGC’s very modest benefit guarantees ($12,870 for a worker employed for thirty years), while the terminations would subject PBGC’s insurance program to great financial strains. The cost of preemptive terminations, however, would ultimately be far less than if insolvent plans were propped up with loans and permitted to worsen their shortfalls still further (Figure 2).

“ Preemptive terminations would ultimately be far less costly than if insolvent plans were propped up with loans and permitted to worsen their shortfalls further.”

The responsible course is to require multiemployer plans, as has largely but not completely been done with single-employer plans, to accurately value their assets and liabilities, and to progress toward full funding. Multiemployer plan trustees (employer and union representatives), not taxpayers, should bear responsibility for funding the benefits they promised to workers. My recent study explains various ways lawmakers could go about this.

“The responsible course is to require multiemployer plans to accurately value their assets and liabilities, and to progress toward full funding.”

All this said, there is a reasonable case to be made that the federal government should devise a creative solution to the problem of “orphan worker liabilities” -- basically, benefits for workers in multiemployer pension plans who were previously employed by companies that have since withdrawn from sponsoring those plans. In theory the continuing sponsors of a plan have accepted full responsibility to pay such workers’ benefits, and in theory the withdrawing sponsor was supposed to make a withdrawal payment covering its share of the plan’s unfunded vested liabilities. But in practice, loopholes in the federal rules have caused withdrawal payments to be insufficient, such that plans carrying larger numbers of orphan workers are now more likely to be underfunded. Because the federal government bears responsibility for these lax withdrawal rules, and because there is some evidence that orphan liability relief could help some troubled plans to stabilize, partitioning plans to remove their orphan liabilities is an approach that carries both more promise and more justification than proposals to bail them out with taxpayer-subsidized loans.

“Removing orphan liabilities is an approach that carries both more promise and more justification than proposals to bail out plans with taxpayer-subsidized loans.”

The partition approach has pitfalls, however. Having the PBGC partition plans and assume their orphan liabilities won’t stabilize the system if plan sponsors aren’t simultaneously given tightened requirements to fully fund their benefit promises to non-orphan workers. This means requiring pension liabilities to be properly measured, strengthening funding requirements, and making offsetting changes to promised benefits, so that on balance net projected claims on the PBGC are reduced after it assumes responsibility for benefit payments to orphan workers. Without such stipulations, using PBGC resources to provide orphan liability relief would be irresponsible.

| To understand how a partition might work, imagine a highly simplified scenario in which employers A, B, and C cosponsor a multiemployer plan. Employer C goes out of business and thereafter no longer sponsors the plan. Employer C makes a withdrawal liability payment on its way out, but it’s not enough to cover the future benefits of C’s former workers. Under current law, the plan would remain responsible for paying benefits to C’s former workers, which A and B would now share the obligation to pay. A’s and B’s contributions aren’t by themselves enough to fund the benefits of their own workers plus C’s former workers, so plan finances are destabilized and the whole plan threatens to go under, making substantial claims upon the PBGC. Under a partition, PBGC would assume responsibility for paying the benefits of C’s former workers who are not rehired by A or B, while employers A and B would continue as joint sponsors of a now-smaller multiemployer plan. To enable PBGC to shoulder the cost of C’s orphan worker benefits, offsetting changes would be made to the remaining plan jointly run by employers A and B, to reduce its projected claims on the PBGC by at least as much as the new costs PBGC has taken on. |

In summary, as lawmakers search for a creative way out of the multiemployer pension solvency crisis, they should steer clear of bailout or loan proposals that would throw good money after bad, and focus their attentions instead on solving the orphan worker liability problem -- while at the same time tightening multiemployer pension measurement and funding rules, and requiring plan sponsors to fully fund the benefits they promise to their workers.

Charles Blahous is the J. Fish and Lillian F. Smith Chair and Senior Research Strategist at the Mercatus Center, a visiting fellow with the Hoover Institution, and a contributor to E21. He recently served as a public trustee for Social Security and Medicare.

Interested in real economic insights? Want to stay ahead of the competition? Each weekday morning, e21 delivers a short email that includes e21 exclusive commentaries and the latest market news and updates from Washington. Sign up for the e21 Morning eBrief.