Getting To Yes: A History Of Why Budget Negotiations Succeed, And Why They Fail

The case for a bipartisan “grand deal” to address the rising national debt is evident from annual budget deficits that are projected to exceed $2 trillion within a decade. Over the next 30 years, Social Security and Medicare’s shortfalls are projected to drive $84 trillion in new government debt. Yet increasing partisanship and polarization—both in Washington and among voters—have significantly diminished the likelihood of bipartisan cooperation to avoid a fiscal calamity.

This report examines 14 major deficit-reduction negotiations since 1980 to determine why some succeeded and others failed. The analysis reveals what I call three “primary ingredients,” some combination of which is necessary to achieve a successful budget deal: 1) a penalty default, or a painful policy that would be automatically implemented if a deal is not enacted by a certain date; 2) general public support for deficit-reduction across parties, with some common ground on the necessary reforms; and 3) healthy negotiations—presidents and lawmakers of both parties establishing positive working relationships based on trust, good faith, and a focus on compromise—seeking “win-win” solutions. The existence of at least two of these primary ingredients has always resulted in a successful deficit-reduction deal. Negotiations that took place with only one, or none, of them has almost always failed.

Secondary ingredients that help to close a successful a deal include an optimal mix of negotiators, an agreement on the problem, a reliance on neutral experts, a united communications front, a divided government, and, at times, a bipartisan commission.

Most successful budget deals over this period were enacted in the 1980s and 1990s. The 2000s have seen mostly failure due to the increasing inability of Republicans and Democrats to overcome their hostility and engage in healthy negotiations. At the same time, there has been an increasing public acceptance of deficits, and an unwillingness of the public to unite around deficit-reduction approaches.

Nearly all the projected growth in budget deficits over the next 30 years comes from Social Security and federal health benefits (particularly Medicare and Medicaid). Yet past deficit-reduction deals relied mostly on cuts to discretionary spending and payments to Medicare providers, which may not be able to sustain additional large reductions. Tax increases on the wealthy have played a modest role in past deals yet cannot fully close more than a small fraction of the fiscal gap. Most deficit reduction in coming years will need to come from entitlements—such as Social Security and Medicare (beyond more provider cuts)—that have often proved resistant to reform.

However, there is a path forward. Lawmakers will have to rebuild new penalty defaults that create an incentive for anti-deficit legislation. Advocates need to better educate the public on causes of consequences of ever increasing deficits. And lawmakers must overcome their mutual distrust of each other, and bring back an integrative negotiating approach that focuses on building win-win solutions rather than relying on deceptive tactics that attempt to take the most of a fixed pie.

Introduction

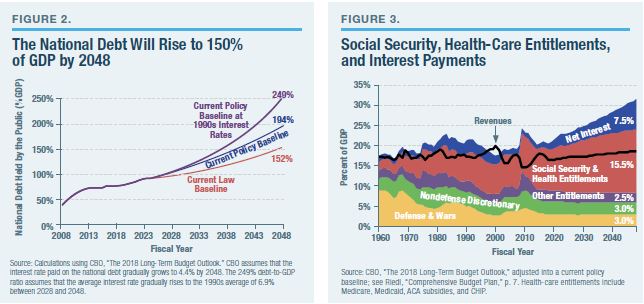

Budget deficits are set to exceed $1 trillion in the next year, on their way past $2 trillion within a decade if current policies continue (Figure 1). Over the next three decades, the Congressional Budget Office (CBO) forecasts $84 trillion in new deficits, which will bring the federal debt to 150% of GDP. And that is the rosy scenario—it assumes peace, prosperity, low interest rates, no new government programs, and the expiration of most of the 2017 tax cuts. More realistically, the debt could surpass 200% of GDP (Figure 2).

While much has been written about the dangers of the ever-growing debt—and the need for a bipartisan “grand deal” to avert a fiscal calamity—the reality is that Congress and the White House are moving in the wrong direction. Republicans are cutting taxes, while Democrats are promising massive new spending. Even if both parties were to finally agree that reducing the flow of red ink is a top priority, there is little reason to believe that they could successfully negotiate a deficit-reduction deal.

This report analyzes 14 budget negotiations during the past three decades to determine what lessons can be applied to future negotiations. Over this period, there were several successful deals between 1983 and 1997 (which, together with strong economic growth, culminated in budget surpluses between 1998 and 2001) and several mostly unsuccessful negotiations since 1998.

The analysis reveals what I call three “primary ingredients,” some combination of which is necessary to achieve a successful budget deal: 1) a penalty default, or a painful policy that would be automatically implemented if a deal is not enacted by a certain date; 2) general public support for deficit reduction across parties, with some common ground on the necessary reforms; and 3) healthy negotiations—presidents and lawmakers of both parties establishing positive working relationships based on trust, good faith, and a focus on compromise—seeking win-win solutions. The existence of at least two of these primary ingredients has always resulted in a successful deficit-reduction deal. Negotiations that took place with only one, or none, of them have almost always failed.

The Case for a Bipartisan “Grand Deal”

The case for deficit reduction is growing even as Congress generally ignores the issue. CBO projects that the budget deficit will rise to 9.5% of GDP over the next 30 years, and that assumes peace, prosperity, low interest rates, and the expiration of most of the 2017 tax cuts.[1]

The driver of this red ink is no mystery. According to CBO, between 2018 and 2048 Medicare will run a $41 trillion cash deficit, Social Security will run an $18 trillion cash deficit, and the interest payments necessary to finance these Social Security and Medicare deficits will cost $41 trillion. In short, over and above payroll taxes and premiums, these two programs alone are set to add $100 trillion to the national debt. Over that 30-year span, the rest of the federal budget is projected to run a $16 trillion surplus.[2] However, unlike the temporary, recession-driven budget deficits a decade ago, Social Security- and Medicare-based deficits will expand permanently (see Figure 3).

There is another way of showing the long-term fiscal dangers. By 2048, the Social Security and Medicare systems are projected to run an annual budget deficit of 12.6% of GDP (including the resulting interest on the debt). Even a projected 3.1% of GDP surplus across the rest of the budget in 2048 will not close that gap.[3]

A national debt that grows to 150% of GDP—which CBO projects in the rosy scenario (i.e., continuing low interest rates, no new spending programs, and the 2017 tax cuts expiring on schedule)—would have severe negative consequences. The interest cost would match Social Security as the largest annual federal expenditure, requiring significant tax increases and spending cuts to finance. In reality, such a large debt would surely raise interest rates from their recent and current low levels, depriving the economy of growth-creating investment. This is especially true, given this country’s low domestic savings rate and the limited ability of other countries to finance such a large U.S. debt.

Primary Ingredients for a Successful Budget Deal

These growing deficits make clear that a new “grand deal” on deficit reduction is absolutely necessary. Yet increased voter polarization, Washington partisanship, and institutional breakdowns have made deficit-reduction deals much more rare over the past 20 years. Is there a plausible path forward toward a deal? This study addresses the question by analyzing 14 major deficit-reduction negotiations since the early 1980s.

An examination of these case studies—which includes both direct research and interviews with participants and experts—reveals several trends that delineate the successes from the failures. Specifically, nearly all successful deficit-reduction deals have included at least two of the following three primary ingredients: 1) a penalty default that lawmakers sought to avoid; 2) public support for the broad elements of a deal; and 3) lawmakers who trust one another and take a good-faith, integrative approach to negotiating. It is possible to secure a deal without two of these ingredients—there is always a human element—but the chances of success substantially increase when they are present.

Primary Ingredient #1: A penalty default. A penalty default occurs if the failure to enact a deal by a certain time will result in the automatic implementation of a policy that the negotiators wish to avoid. In short, the default policy would penalize both parties. In 1983, the White House and Congress moved quickly to enact Social Security reforms because its trust fund was a few months away from insolvency, which would have reduced Social Security checks. The 2013 “fiscal cliff” tax deal was motivated by the upcoming expiration of the “Bush tax cuts,” which would have imposed large across-the-board tax increases that neither party wanted. Past deficit-reduction deals have been tied to legislation raising the debt limit, preventing a government shutdown, or canceling a large spending sequestration. The existence of penalty defaults often results in “must-pass” legislation to avoid the penalty.

Penalty defaults are a key ingredient to overcoming the strategic disagreement that has resulted from increasing partisanship and polarization. While lawmakers usually have a political incentive to reject compromise, stand with their base constituency, and exploit partisan differences for electoral gains, a penalty default can raise the cost of inaction to an unacceptable level. Neither side wants to risk blame for a government shutdown, debt-limit default, large automatic tax increases or benefit cuts.

While penalty defaults are seen as external factors forcing the hand of lawmakers, nearly all are created by previous laws. Congress and presidents have chosen to have debt limits. The expiration dates of the Bush tax cuts were written into law by previous Congresses (in part to comply with their own Byrd Rule, which prevents reconciliation bills from expanding budget deficits beyond a certain number of years). The inability of certain agencies to spend money in a government shutdown, or Social Security to issue benefits beyond the exhaustion of its trust fund, is based on previously enacted laws. The modern version of sequestration was created by Congress in 1985.

Thus, Congress and the president determine their own penalty defaults. That means that they can also repeal the defaults. Lawmakers in 1983 could simply have required that full Social Security checks continue after trust-fund exhaustion, funded by general revenues. In fact, many penalty defaults have lost their effectiveness. In recent years, Congress has essentially canceled the debt limit for one to two years at a time, and canceled spending sequestrations. While past threats of government shutdowns have been used to motivate deficit-reduction deals, the repeated failure of that approach—with negative political consequences for the party seen as forcing the shutdown—has rendered it ineffective.

Consequently, an effective penalty default must strike a balance. It needs to show a real negative outcome that neither side would want. Yet it also needs at least one side of a divided government that is willing to risk that outcome occurring if a deal is not made. If the penalty is too weak, it will not motivate lawmakers to overcome their strategic disagreement. If the penalty is too strong, the parties are more likely to repeal its enforcement without adding a deficit-reduction deal. The hostage must be valuable, and at least one side of the negotiation must be willing to shoot the hostage if no deal is made.

Primary Ingredient #2: Public support. A second, more obvious, ingredient in a deficit-reduction deal is sufficient public support across both parties. The challenge is that voters typically prioritize deficit reduction in theory yet oppose nearly all tax increases and spending cuts that would significantly accomplish that objective.[4]

Public support for deficit-reduction efforts was notably higher and more bipartisan in the 1980s and 1990s than in the 2000s.[5] After a brief Tea Party interlude between 2009 and 2012, significantly rising budget deficits are no longer seen by conservatives as an impediment to tax cuts, or by liberals as an impediment to single-payer health care, a government jobs guarantee, free college, student loan forgiveness, or a Green New Deal.[6] Some economists argue that low interest rates make rising debt affordable,[7] while adherents to Modern Monetary Theory (MMT) believe that Washington can essentially fund surging deficits with the printing press.

Deficit-reduction deals are less popular today in part because the required solutions are more painful. Deficit deals in the 1980s and 1990s (other than the 1983 Social Security deal) generally focused on significant discretionary spending limits (mostly in defense), smaller mandatory reforms such as some Medicare provider cuts, and occasionally more modest tax increases. Yet discretionary spending is already near historical lows, and rising budget deficits are now driven almost entirely by Social Security and health entitlements—which are much more politically difficult to reform.[8] Democrats (and many Republicans) draw a line at reducing these benefits, while the alternative of substantial across-the-board tax increases—merely taxing the rich is not enough—is a deal-breaker for Republicans (and many Democrats).

Overcoming public opposition to the pain of deficit reduction requires bipartisan credibility and a tangible, understandable payoff for the public. Bipartisan credibility requires bipartisan negotiation and compromise. President Reagan’s initial attempt to offer his own reforms to save Social Security in 1981 encountered strong Democratic opposition, who ran against those reforms in the 1982 elections. Proposals by President Bush to save Social Security in 2005, and by Rep. Paul Ryan (R., Wisconsin) to balance the long-term budget in later years, failed to rally the public partly because Democrats refused to participate. President Clinton’s 1993 deficit-reduction act also remained controversial partly because of unanimous Republican opposition. Deficit-reduction deals often impose large costs on taxpayers, and skepticism among taxpayers that they are shouldering a disproportionate burden can be assuaged only by bipartisan assurances that the burden is distributed fairly and equitably. The last two times a party tried to do a major deficit-reduction deal on its own under unified government—in 1993 and 2005—that party lost the congressional majority the following year.

Beyond bipartisan credibility, popular deals also require an understandable, tangible public payoff. Sometimes simply averting a penalty default is the payoff—Social Security checks will continue, or the government will stay open. In 1997, the payoff was the promise of balancing the budget for the first time since the 1960s. In 1990, President George H. W. Bush emphasized that a deficit-reduction deal would finally encourage the Federal Reserve to lower interest rates, which would save money for families and businesses while also creating jobs.

Unfortunately, sometimes the payoff is not immediately obvious. The current budget deficit is too large to achieve a balanced budget. Keeping the deficit small enough to avert a future fiscal calamity may be seen as too theoretical by voters. Other economic factors are maintaining relatively low interest rates even as the national debt rises steeply. Thus, it may be helpful for lawmakers to emphasize other benefits of deficit-reduction reforms. In 2005, President George W. Bush argued that his Social Security reforms would lead to a better system with possibly even higher benefits. Republicans often emphasize that Medicare premium support would encourage choice and competition. Democrats assert that taxing the rich can reduce inequality and that cutting defense may lead to a more modest foreign policy. The 1996 welfare reforms were promoted as a way to end the cycle of poverty, rather than as a budget-saving exercise.

Primary Ingredient #3: Personal Relationships, Trust, and Integrative Negotiations. Hardened partisans regularly dismiss the importance of building bipartisan trust and relationships as “kumbaya nonsense,” yet the history of bipartisan negotiations shows that it is extraordinarily important. Indeed, the collapse of trust and relationships is perhaps the most important factor in the lack of successful bipartisan deals over the past 20 years.

There are two elements to this ingredient. The first is both sides entering the negotiation in good faith by:

- Maintaining civility and honesty and respecting the other side’s interests as legitimate;

- Bringing a good-faith willingness to compromise for a deal, while recognizing that nothing is agreed to until everything is agreed to;

- Not dominating the discussions, condescending, relitigating the past, or trying to dictate the other side’s interests; and

- Not leaking or publicly undermining the other side’s position.

The second element is utilizing an integrative negotiating strategy—whereby both sides work together to build a win-win deal—rather than a pure distributive negotiation (where both sides begin with extreme positions and then try to bargain the other down), or a negotiation based on deceptive or hardball tactics. Elements of integrative negotiations include:

- Beginning by defining the problem together, expressing each side’s desired outcome (which is not necessarily a legislative position), and exploring creative legislative options to achieve those outcomes;

- After all reasonable options have been defined, both sides listing their “must-haves” and “unacceptables,” and even ranking priorities in order to set the stage for concessions and compromises;

- Seeking trade-offs and compromises with the specific goal of each side’s victories; and

- When facing an impasse, expanding the negotiation by bringing in outside issues that can break the deadlock.

A certain degree of hardball tactics and deception is inevitable in all negotiations (and may provide limited benefits to the side employing them), but a heavy reliance on them will often destroy the negotiations.

Political scientists and social psychologists agree that building the necessary trust for good-faith negotiations usually requires repeated interactions—both personal and professional.[9] Simply getting to know each other leads to increased mutual respect and more honest and trustworthy negotiations. Thus, Presidents Reagan and George H. W. Bush spent considerable time inviting congressional Democrats to the White House for social events as well as calling them to learn their policy concerns (President Clinton reached out to Republicans later in his presidency as well). The importance of repeated interactions also shows the harm of Congress’s more recent evolution of flying into Washington, D.C., on Monday nights and flying out after the final weekly votes on Thursday nights. Finally, this is why seniority (especially on committees) is so important in successful negotiations. It is difficult to act deceptively—or to dismiss the other side’s interests as totally unworthy—when the two sides have gotten to know each other well, both personally and professionally.

Positive budgetary examples include Reagan and House Speaker Tip O’Neill (D., Massachusetts) beginning the 1982–83 Social Security commission with a pledge not to publicly attack each other or the commission (which commission chairman Alan Greenspan called the lead factor in enacting a deal).[10] While the 1995–96 Clinton–Gingrich budget negotiations broke down almost exclusively over personal distrust, animosity, and deceptive negotiating, by 1997 they had won a major bipartisan balanced budget agreement simply by dropping the political warfare and deciding to sit down and build a win-win deal—what House Speaker Newt Gingrich (R., Georgia) called “the human touch.”[11] “We’re in this together” trumps the aim to embarrass the other side into unconditional surrender.

While looking back at the 1990 budget deal, former House Speaker Tom Foley (D., Washington) said, “I did have a very good relationship with President Bush. I felt very comfortable in talking with him about any matter related to the agreement. Honestly, I think that did help and made a difference for everyone.” Former Republican Rep. Bill Frenzel (R., Minnesota) added: “In those days, the bad guys were the opposition, not the enemy. There’s a world of difference between those two words. Yes, we had some distrust, but also we had some ability to work with each other, believe each other, and [that] made life easier at that time.”[12] After negotiating that 1990 budget deal, President Bush and Democratic leaders pledged to bypass all government shutdowns, fight unrelated amendments, and seek majority support in each other’s own party in order to ensure congressional passage.

Some budget negotiations have seen participants make additional concessions for the sake of unity. The 1983 Social Security commission probably had the votes to pass a party-line conservative solution on day one if they had wanted—but they continued negotiation and making concessions to win a bipartisan supermajority vote.[13] During the 1997 budget deal, Clinton reportedly gave Republicans additional concessions to ensure that the GOP could declare victory as well. Outside the budget, Republican authors of the 2001 USA PATRIOT Act made additional concessions to Democrats—whose votes were not required for passage—to build nearly unanimous support and bipartisan credibility with the public.[14]

Former high-ranking Rep. Henry Waxman (D., California), in his book The Waxman Report: How Congress Really Works, repeatedly endorses integrative negotiations as the path to most successful deals. Waxman recounts how he negotiated the 1996 Food Quality Protection Act with Rep. Tom Bliley (R., Virginia), chairman of the House Commerce Committee. “We implicitly trusted one another,” according to Waxman. The two lawmakers and their staffs engaged in numerous meetings where they listed their various priorities, sought win-win solutions, and helped each other satisfy their policy needs. Their legislation passed Congress unanimously and was signed into law. Waxman concludes: “The greatest misconception about making laws is the assumption that most problems have clear solutions, and reaching compromise mainly entails splitting the difference between partisan extremes.”[15]

The 1990 Clean Air Act provides another example of a successful integrative solution. “As an observer and a participant in that process,” writes American University political scientist Jeffry Burnam, “I can testify that there was very little bargaining in the sense of ‘horse trading’ in the Senate back room. The discussions there were based on efforts by key leaders to find mutually acceptable solutions that were right for them in accordance with [the] view that politicians have much to gain by seeking common ground and sharing credit for measures that are in their mutual interest to support.”[16]

The increasing utilization of bipartisan congressional “gangs” to negotiate deals is also based on trust and good-faith negotiations. Unlike the usual participants in negotiations—rigid committees, congressional leadership, and White House officials—gangs are self-selecting and private. This makes them more likely to trust one another and safeguard the privacy of negotiations.

Secondary Ingredients for a Deal

While the primary ingredients create substantial momentum for a deficit-reduction deal, secondary ingredients can also push Congress and the White House toward a deal:

An optimal mix of negotiators

Several budget deals over the past several decades have been heavily assisted, or nearly destroyed, by the decision of who is in the room doing the negotiating. All successful bipartisan deals except one—the 1985 Gramm-Rudman-Hollings law—began with private negotiations (or commissions) involving the White House and the congressional leaders of both parties.

Presidential leadership has been vital to all major deals, with the exception of the 1985 Gramm-Rudman-Hollings Act, which began as a popular amendment to a debt-limit bill. However, while White House leadership is extremely important, some dispute whether the president should be in the room negotiating the final deal. In his book recounting the 1997 budget deal, Clinton’s assistant for legislative affairs, John Hilley, writes that one key to success was limiting the president’s direct involvement in the initial meetings that set broad budget goals. While Clinton remained heavily engaged and in control of the negotiation details, “it was better to have the ultimate decisionmaker above the fray, one step removed from all the bumps and bruises that are part of the day-to-day engagements among strong-willed partisans. When things got rough, or a change of direction was required, it was always good to be able to ‘take it back to the president’—giving everyone time to assimilate, think anew, calm down.”[17]

Hilley adds that the earlier 1995 budget negotiations failed partly because Clinton was too directly engaged in the discussions. President Obama also directly led the detailed negotiations with congressional Republicans during the failed 2011 grand-deal negotiations (although he was able to negotiate the smaller Budget Control Act). Additionally, Reagan and George H. W. Bush had top aides negotiate the final details of the 1983 Social Security deal and 1990 Andrews Air Force Base deal. The president should surely direct the administration’s bargaining position, but he need not necessarily sit at the bargaining table.

A perennial challenge has been the trade-off between building a large group of negotiators that ensures that all interests are represented, versus having a smaller group that is more likely to build a consensus. In the 1983 Social Security reforms, a 15-member commission made progress, yet the final deal required breaking off into an informal “Gang of Nine” that began meeting at the home of James Baker, White House chief of staff. In the 1990 budget deal, Bush originally hosted a group of approximately two dozen at Andrews Air Force Base for 11 days to negotiate in private. Progress was made, yet the deal was sealed when a smaller group of eight top White House and congressional leaders met in the office of House Speaker Foley for several days after the Andrews negotiations broke up. The 1997 budget deal was negotiated by a small group of administration and congressional leaders who were open to compromise.

These examples suggest that a smaller group of six to nine negotiators is optimal. The problem is that limiting the number of congressional leaders at the table increases the pressure on those leaders to adequately represent the diverse factions of their conference. However, successful leaders must inspire loyal followers. A major reason the 2011 Obama–Boehner negotiations continued breaking down was that House Speaker John Boehner (R., Ohio) was not seen as someone who could bring the “Tea Party” Republican faction with him on a deal. House Majority Leader Eric Cantor’s (R., Virginia) presence was often considered a reflection of Tea Party opinion, yet Boehner was driving the Republican negotiations, and the two reportedly did not get along with each other.

Ultimately, a successful budget negotiation should consist of two negotiating factions, rather than several partisan sub-factions. This requires a minimum degree of party consensus before entering negotiations. The president and congressional leaders must also be able to deliver their rank-and-file lawmakers.

Two successful models have emerged. The 1983 and 1990 model begins with a larger group of negotiators (15–22) that includes the key administration aides, congressional leadership, relevant committee chairpersons, and top staff. Once the larger group has moved toward a general framework, they shrink the room to six to nine top congressional and administration leaders to finish the deal. Still, this approach is not perfect—by isolating the 22 members at Andrews Air Force Base, rank-and-file Republicans still felt left out, and ultimately voted against the deal.

The other model, from 1997, is to begin with a relatively small group of negotiators who also maintain contact with relevant factions and committee leaders—even cycling them into the negotiations when their issues of jurisdiction were addressed.

The choice of administration negotiators matters as well. In the chaotic 2011 negotiations, both Republican and Democratic members of Congress complained that Obama and his top negotiators were rarely on the same page, leading to repeatedly contradictory negotiating positions.

A united front to overcome outside interests and communicate to the public

Even a bipartisan agreement on an optimal set of policy reforms does not guarantee that the public or influential interest groups will support the deal. The president and congressional leaders may have the wind at their back when announcing a bipartisan agreement, but they still need to sell it to the rest of Congress and the voters. An obvious tactic is to emphasize the bipartisan nature of the deal. In the 1997 budget agreement, President Clinton made sure to include Republican leaders at the Rose Garden ceremony announcing the deal. The 1998 Social Security pact between Clinton and House Speaker Gingrich would have been rolled out in a series of coordinated speeches, commissions, and events (had it not collapsed because of the Lewinsky scandal). In 1983 and 1990, the White House and congressional leaders coordinated communications and pledged to work together knocking down political obstacles.

Addressing skeptical interest groups is trickier. The 1983 Social Security reforms reportedly enraged AARP—yet the parties simply chose to ignore the organization, whose own preference for a general revenue bailout was seen by negotiators as a wild overreach. AARP was more successful fighting President Bush’s 2005 Social Security reforms because Democrats joined their opposition from the start. Past deals that capped defense spending, reduced payments to health providers, and raised user fees had too much bipartisan momentum for the affected interests to block.

One approach is to bring the most important outside stakeholders into the process. Including them as part of a bipartisan commission to solve the problem alongside lawmakers can give these stakeholders a voice and an investment in seeing the problem solved. At minimum, keeping in close consultation during the policy process can build support from outside organizations that are acting in good faith.

An agreement on the scope of the problem, the data, and a reliance on neutral experts

One common aspect of failed negotiations is that neither side may agree on the exact nature of the problem to be solved, and both sides may bring their own contradictory experts and data. The most famous example is the 1995–96 Clinton–Gingrich budget negotiations that resulted in a 21-day government shutdown over whether to rely on Congressional Budget Office (CBO) or Office of Management and Budget (OMB) scoring of the budget proposals. During the 2011 Obama–Boehner negotiations, both sides also brought wildly divergent analyses of the budgetary savings and effects of various proposals.

Creating a bipartisan commission has been shown to address these issues. The 1983 Social Security commission was professionally staffed with technical experts who drafted a long series of memos explaining the scope of the problem and the savings and ramifications of various proposals. The 1998 Breaux-Thomas commission, 2010 Simpson-Bowles commission, and 2011 “Super Committee” also included highly trained, technical staff that helped both sides frame the problem, create reform options, and analyze their pros and cons. There is considerable nonpartisan technical expertise at CBO, OMB, Government Accountability Office (GAO), and across federal agencies. It is just a matter of negotiators agreeing on a group of experts, bringing them in, and accepting their expertise.

A bipartisan commission

A bipartisan deficit-reduction commission can serve several purposes. First, it can break the partisan logjam and focus both parties on finding a solution. For example, after a year of partisan warfare over the soon-to-be insolvent Social Security system, Reagan in late 1981 created a bipartisan Social Security commission that brought Republicans, Democrats, and outside experts together to define the policy challenge, focus on solutions, and craft reform options. Although the deal was finalized outside the official commission negotiations, the creation of a commission made those civil, bipartisan negotiations possible.

Second, a commission can bring bipartisan credibility to a deficit-reduction plan and thus encourage public support. The 1983 Social Security commission’s recommendations were much more widely accepted than previous Social Security reform proposals. The 2010 Simpson-Bowles commission gave some credibility to deficit-reduction efforts, even if the commission itself did not approve the final plan. In the 1980s and 1990s, a defense-base-closing commission was able to build support in Congress for closing more than 100 obsolete military bases—a solution that never could have occurred through regular congressional politics. A commission does not guarantee success, but it can break some of the partisan gridlock and get the ball rolling on reform. Furthermore, several “failed” commissions, such as the 1998 Breaux-Thomas commission and the 2010 Simpson-Bowles commission, had several of their key proposals enacted over the next five years.

Brookings Institution’s Stuart Butler and Timothy Higashi have noted that successful commissions require several factors.[18] First, they must be created by a White House and Congress that is truly dedicated to solving the problem at hand. A commission is a tool, yet it cannot motivate a disinterested Congress.

Second, a commission usually requires current members of Congress who have a direct stake in the politics. Lawmakers will not give credibility to a group of (only) outside experts who have no political skin in the game.

Third, commissions should reserve additional spots for respected former lawmakers and outside experts, as well as interest-group stakeholders whose support may ultimately be necessary for a deal. While membership should include a diversity of opinion, it helps to include individuals who are capable of working across the aisle.

Fourth, requiring a commission supermajority to approve the plan is wise because fiscal consolidation recommendations are unlikely to be approved by a partisan and polarized Congress unless they have successfully brought several diverse factions on board.

Finally, there should be some automatic mechanism to bring the approved commission recommendations to the House and Senate floor for a guaranteed vote, so that the report does not simply collect dust on a shelf.

Commissions have historically been more successful when used for discrete issues, such as Social Security solvency or closing military bases. Broader budget agreements usually require more direct congressional and White House involvement. Stuart Butler and Maya MacGuineas have proposed having a commission initiate the deficit-reduction planning and craft default proposals to meet the long-term budget targets, while also empowering Congress and the White House to replace those reforms with alternatives that can achieve equal savings.[19]

Divided government

It may be counterintuitive to observe that deficit-reduction deals are more likely to occur under divided government than unified control. As difficult as forging bipartisan agreement can be, unified party control of the White House, House, and Senate is even less likely to result in deficit-reduction legislation. One reason is lack of interest. When one party has finally achieved the long-dreamed-of trifecta of the White House combined with a House and Senate majority, fiscal consolidations are often not on the priority list (1993 Democrats are an exception). Republicans typically seek to cut taxes and enact other popular parts of the conservative agenda. Democrats typically aim to create and expand government programs and enact other popular parts of the Democratic agenda. Also, during the last two periods of unified government, the party in power focused on alleviating a national crisis (the terrorist attacks for the 2001–06 Republican trifecta[20] and the great recession for the 2009–10 Democratic trifecta).

Unified government also fails to produce major bipartisan deals because the minority party sees little political benefit in helping the majority enact controversial policies. In that situation, the majority party may find it too risky to impose consolidations without the support of the minority party—and the minority party will see its aggressive opposition to these painful reforms as its key back into power. Thus, congressional Republicans unanimously opposed the 1993 Democratic tax increases, and congressional Democrats aggressively opposed Bush’s 2005 Social Security reforms. The minority party’s aggressive opposition rendered the reforms politically toxic; indeed, both parties lost their congressional majorities the following year. At this point, any major deficit-reduction deal is much more likely to be enacted under divided government.

Case Studies

The following 14 case studies constitute the largest grand-deal deficit negotiations since 1983. Six of them resulted in enacted legislation (summarized in Figure 4 and Figure 5), and eight did not. The vast majority of these case studies show that a large bipartisan deal requires at least two of the three primary ingredients described earlier.

1983 National Commission on Social Security Reform (“Greenspan Commission”)[21]

The Social Security system was heading toward insolvency, and by summer 1983 it would be unable to pay full benefits. Ronald Reagan came into office in 1981 proposing his own solvency reforms (mostly benefit savings) ran into bipartisan opposition and were harshly attacked as a war on seniors. Reagan responded with a new approach: the creation of a 15-member bipartisan commission in September 1981, which was chaired by Alan Greenspan and included lawmakers and outside experts appointed by both parties. The commission would report after the 1982 elections.

The commission’s main contributions were depoliticizing Social Security reform, collectively defining the problem in terms of solvency goals to be met without fundamentally altering the program’s structure—with a unanimous vote—and building reform options. However, after the commission deadlocked on solutions, an agreement was reached by a smaller “Gang of Nine” congressional leaders and administration leaders who met at the home of James Baker, the White House chief of staff. Their solution—which funded a short-term fix and approximately two-thirds of the 75-year long-term shortfall—was endorsed by the broader commission on a 12–3 vote. Congress then tweaked and even expanded the reforms (adding a future increase in the full retirement age from 65 to 67), before it passed with bipartisan support and was signed by the president in April 1983.

The final deal resulted in budget savings (estimated at the time of enactment) of $165 billion over seven years, consisting of $88 billion in taxes, $23 billion in revenues from bringing in new populations such as nonprofit and new federal employees, $39 billion in benefit savings from delaying an annual COLA by six months, and an estimated $15 billion in lower interest costs. An additional $18 billion transfer of general revenue into Social Security improved program solvency but did not alter the unified federal budget. Future benefit savings would come from raising the full retirement age to 67. In terms of the primary ingredients:

Penalty Default? Yes. Unless reforms were enacted, the Social Security system would stop paying full benefits in summer 1983.

Public Support? No. While the public understood that Social Security was facing a crunch that would render it unable to pay full benefits, most Americans still opposed the necessary reforms to save the system—even if the opposition was softer in 1983 than in previous years.[22] It is also worth noting that AARP opposed virtually all plausible reforms, a position that led to both parties dismissing their opposition.

Healthy Negotiations? Yes. At the time the commission was formed, Reagan and House Speaker Tip O’Neill privately pledged not to publicly oppose the commission’s recommendation—which Greenspan later declared the most important reason that the reforms were enacted.[23] Republicans put taxes on the table, and Democrats agreed to spending cuts. The “Gang of Nine” got along well, trusted one another, and tried to make both sides a winner. Leaks were minimized. Congress accepted most recommendations and even worked on a bipartisan basis to expand the savings. Bob Dole (R., Kansas) implored Senate colleagues not to oppose savings provisions unless they had better alternatives. Ultimately, the 1983 Social Security reforms showed how both parties can collaborate on a controversial issue in a manner that hurts neither party politically.

Result: With a penalty default and healthy negotiations, the result was the most ambitious entitlement reforms in more than three decades.

1985 Balanced Budget and Emergency Deficit Control Act (“Gramm-Rudman-Hollings”)[24]

Amid public concern over rising deficits, the Democratic House and Republican Senate both wanted a deficit-reduction deal. Reagan had pledged to veto any tax increases, and Democrats (seeking defense cuts) took Social Security reform off the table. After the negotiations within the regular budget process broke down, a bipartisan group of senators offered an amendment to a bill in September to increase the debt limit that would create annual (and declining) caps on the budget deficit, to be enforced by across-the-board spending cuts (aka sequestration).

To the surprise of most, the Senate passed the proposal 75–24. From there, congressional leaders of both parties—seeing the proposal’s momentum—set aside their concerns and worked together to make the caps acceptable to the rest of Congress. Democrats were able to exempt most mandatory spending from any sequestration and require that defense cuts would constitute half of any sequestration. Republicans kept tax increases out of the automatic reforms and received assurance that sequestrations would not occur until after the 1986 elections. While neither side loved the compromise, it passed the House and Senate overwhelmingly and was signed by the president on December 12, 1985 (the legislation as signed would be struck down by the Supreme Court).

In the final deal, yearly deficit-reduction targets spared both tax increases and major entitlement cuts. While the previous CBO baseline projected a budget deficit rising from $212 billion in 1986 to approximately $300 billion by 1991, this law required that the deficit fall incrementally from $172 billion in 1986 to zero by 1991. If Congress failed to stay within the targets, automatic across-the-board cuts (sequestrations) would take place—half from defense and the other half from nondefense discretionary spending (plus a small portion of non-exempt entitlement spending).

Penalty Default? No.

Public Support? Yes. Polls and lawmaker town halls showed that the public was increasingly concerned about rising deficits, which resulted in immediate legislative momentum for the proposal.[25] Democrats were especially interested in reining in the defense budget, and Republicans wanted to protect earlier tax cuts from falling prey to rising red ink.

Healthy Negotiations? Yes. The proposal originated with a bipartisan amendment to a bill. Congressional leaders who were skeptical decided that it would be more effective to shape the legislation—and remove what Democrats and Republicans separately regarded as its worst provisions—than to stand on the sidelines and vote no. Both sides were able to exempt key priorities from the final provisions governing sequesters.

Result: Public support and good-faith negotiations led to success. This was a rare bipartisan budget deal that began as regular legislation—rather than a commission or set of top-level negotiations—and gained momentum. In 1986, the Supreme Court declared the law unconstitutional (Bowsher v. Synar, 478 U.S. 714, 1986) on separation-of-powers grounds: the law transferred executive functions to the U.S. comptroller general (who is director of the General Accountability Office, an agency within the legislative branch). A tweaked (and constitutional) version of the law, 1987 Balanced Budget and Emergency Deficit Control Reaffirmation Act, was enacted in 1987.

1990 Omnibus Budget Reconciliation Act (“Andrews Air Force Base Summit”)[26]

In 1990, the mounting budget deficit again had the attention of both parties. An automatic sequestration was looming, the economy was weakening, and the Federal Reserve would not lower interest rates without a deficit-reduction deal.

Democrats had been drafting their own deficit-reduction plans when President George H. W. Bush announced on June 26, 1990, that he would be willing to break his “no new taxes” campaign promise as part of a bipartisan budget deal. From September 7 through September 18, Bush, his aides, and a bipartisan group of approximately a dozen congressional leaders negotiated at Andrews Air Force Base. Although progress was made, the final deal was not sealed until a smaller “Gang of Eight”—White House and congressional leaders—began meeting in House Speaker Tom Foley’s office in late September.

Despite pledging to work together to pass their budget deal through Congress, a Republican rebellion in the House defeated the plan. From there, negotiators moved the proposal leftward to win more Democratic support. It passed Congress in late October, and the president signed the bill on November 5, 1990.

The final deal projected deficit reductions of $495 billion over five years, consisting of $158 billion in new taxes, $197 billion in defense cuts, $80 billion in mandatory program savings (of which $33 billion was to be cut from reimbursement to Medicare providers), and $60 billion in interest savings. The act also replaced the Gramm-Rudman-Hollings sequester with five years of discretionary spending caps and new, pay-as-you-go (PAYGO) rules, requiring that new tax cuts or entitlement expansions be offset.[27]

Penalty Default? Yes. A spending sequestration was looming. Bush had threatened to veto a continuing resolution and shut down the government if no deal was struck by October 1. The president also wanted to persuade the Federal Reserve to lower interest rates on a fragile economy.

Public Support? Yes. The public was generally worried about the rising deficit. Both parties feared a public backlash if they failed to complete a deal.

Healthy Negotiations? Yes. Bush had long invested significant effort into building personal relationships with Democratic leaders. In addition, his OMB director, Richard Darman, had a particularly strong relationship with Democrats. The Andrews Air Force Base negotiations were generally collegial and suffered minimal leaks. After leaving Andrews, a smaller “Gang of Eight” finished the deal. Negotiators of both parties worked together to sell the deal to Congress and fight poison-pill amendments. However, rank-and-file Republicans felt excluded by the private negotiations at Andrews and generally opposed the deal.

Result: With all three primary ingredients secured, the bargain was sealed. Ironically, the income-tax rate increases were not in the original deal struck at Andrews and at Foley’s office. A rebellion of House Republicans against the bill ultimately led to more taxes, which was not their intention.[28] Major defense savings were made possible by the collapse of communism.

1993 Omnibus Budget Reconciliation Act (“Deficit Reduction Act of 1993”)[29]

After running for president on the promise of a middle-class tax cut, Bill Clinton quickly determined that rising deficits required both tax increases and spending cuts. With Democrats controlling the House and Senate, Republicans quickly made clear that they would oppose the president’s plan. This left the president needing the overwhelming support of congressional Democrats. Clinton’s congressional relations were rocky (with both parties), and Congress defeated a $16 billion stimulus plan that was attached to the deficit-reduction proposal. However, the rest of the deficit-reduction package was passed by a razor-thin margin of 218–216 in the House, 51–50 in the Senate (with Vice President Al Gore breaking the tie), and then signed into law on August 10, 1993.

Clinton was concerned about rising deficits, particularly the effect on interest rates and economic sluggishness. He also wanted to preempt more aggressive Republican deficit reforms.[30] As the debate heated up, the White House became more motivated to simply avoid an embarrassing legislative defeat. On the flip side, Republicans, fully out of power, opposed the tax increases but were also motivated to deny the president a major victory. Thus, moderate congressional Democrats—many of whom favored aggressive deficit reduction, including entitlement cuts—had the most leverage because their overwhelming support was required for passage.

At the time it was enacted, the new budget law was estimated to trim the budget deficit by $433 billion over five years. This included $241 billion in new tax increases, led by raising the highest income-tax rate from 31% to 39.6% ($115 billion), raising transportation fuel taxes by 4.3 cents per gallon ($31 billion), removing the earnings cap on Medicare payroll taxes ($29 billion), and raising the percentage of Social Security benefits (from 50% to 85%) subject to income taxes for upper-income seniors ($25 billion). It also saved $145 billion in federal spending by various measures, including extending the discretionary spending caps through 1998 ($69 billion), Medicare provider cuts ($48 billion), tweaking benefits for military and federal retirees ($12 billion), raising Medicare premiums ($8 billion), Medicaid reforms ($7 billion), and new spectrum auctions by the Federal Communications Commission ($7 billion). The bill included a $19 billion expansion of the Earned Income Tax Credit (EITC). Finally, the law saved an estimated $47 billion in lower interest costs on the national debt.[31]

Penalty Default? No.

Public Support? No. While the public supported the proposal by a 58%–27% margin when it was unveiled in February 1993, support continued to fall closer to an even split, with Republicans especially hostile.[32] Clinton’s approval rating also continued to fall throughout the summer of 1993 as the budget debate heated up.[33] Voters did not consider the bill a top priority, and even many Democratic lawmakers determined that opposing the bill was good politics.[34]

Healthy Negotiations? No. Most congressional Republicans initially made clear they would not support the plan.[35] Republicans who did reach out were dismissed by a White House that also demanded that congressional Democrats not work with (or even speak with) any Republicans regarding the bill.[36] Rather than involve congressional Democrats in drafting the proposal, the White House handed a complete plan to Congress with demands not to amend it.[37] A bipartisan Senate alternative proposal was dismissed.[38] The president and other White House officials—needing nearly unanimous Democratic votes for unpopular tax increases—relied heavily on bullying, intimidating, pleading, lying, and making legislative promises to fellow Democrats that were later broken after the votes were secured.[39]

Clinton repeatedly complained that he did not understand the rhythms and motivation of Congress.[40] The final deciding vote for the package came from Sen. Bob Kerrey (D., Nebraska), who endured verbal abuse from Clinton before reluctantly voting for the legislation to keep the new presidency from sinking (and in return for a promise to create a new commission to address entitlement spending growth).[41]

Result: This was the only deal in this study to have been enacted without two of the three primary ingredients for a successful negotiation. That was a luxury of single-party control of the House, Senate, and Congress that eliminated the requirement for bipartisan negotiations. Still, passing the unpopular reforms on a party-line vote played a role in the Democrats losing control of Congress the following year.

1994 Bipartisan Commission on Entitlement and Tax Reform (“Kerrey-Danforth”)[42]

A few months after the Deficit Reduction Act was enacted, the president fulfilled a promise to Kerrey and created the Bipartisan Commission on Entitlement and Tax Reform by executive order.[43] Cochaired by Kerrey and Republican senator John Danforth, the commission included 10 senators, 10 House members, 8 private-sector leaders, a governor, and a mayor, as well as 27 professional staffers. Of the 32 members, 30 voted for an interim report defining the budget challenge, and 24 voted for a set of broad principles supporting immediate action to limit long-term deficits. However, the commission deadlocked and was unable to issue a final report with any consensus recommendations. The commission staff created a computer game whereby the public could try to balance the budget.

As no recommendations reached the necessary three-fifths threshold for approval by the commission, Kerrey and Danforth instead issued a joint proposal, as did a few other members introduce proposals. Most of these proposals did not include detailed scoring.

The commission was created as a favor to Kerrey and had the strong support of Danforth. Neither the White House nor House or Senate leaders were significantly invested in the commission’s success—in fact, some opposed the commission’s purpose.

Penalty Default? No.

Public Support? No. Despite public outreach and hearings televised on C-SPAN, the commission received little broad media coverage or public engagement. And while most Americans generally supported deficit reduction, there was little demand for major entitlement cuts or tax increases. AFL-CIO, NAACP, and AARP publicly attacked draft plans to pare back entitlement spending.

Healthy Negotiations? No. The failure even to issue a report of consensus policy recommendations (despite a modest three-fifths threshold for approval) suggests that the members lacked either the motivation or capability to compromise. When Kerrey and Danforth issued a joint proposal that would reform Social Security and Medicare, commission member Rich Trumka (president of United Mine Workers) publicly shrieked that it was “the most fundamental attack on Social Security and Medicare since their beginning.”

Incoming House Speaker Newt Gingrich warned commission Republicans that any proposal to reform Social Security—a program whose future shortfalls the commission was created in part to address—would be unacceptable. In short, Congress and even commission members were openly hostile to the reforms that the commission was created to examine.

Result: The lesson of this experience is that successful commissions require, at the very least, a Congress and president committed to solving the underlying problem. Absent this commitment, commission members will not make the required investment or compromises. The lack of any requirement that Congress vote on a commission-approved proposal made the exercise relatively academic. Finally, the commission’s coverage of all tax and entitlement programs was too broad to make agreement realistic.

1995–96 Government Shutdown[44]

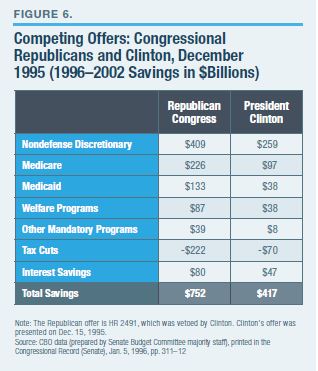

Emboldened by what it considered a voter mandate, the new Republican congressional majority passed a reconciliation bill in November 1995 that would balance the budget in seven years by cutting spending by $974 billion and taxes by $222 billion (for a net $752 billion in deficit reduction). Clinton opposed these reforms and vetoed bills to raise the debt limit that included many of the Republican provisions. The result was a government shutdown.

After finally pledging to negotiate a seven-year balanced budget, the president signed legislation reopening the government after five days. However, Republicans later determined that the president’s pledge was insincere, and this led to a second shutdown on December 16 that lasted 21 days. During that time, Clinton pushed a more modest budget blueprint and Republican leaders committed public gaffes (such as Senator Dole making comments that were construed as preferring that Medicare “wither on the vine”), culminating in the public moving toward the president’s position. In early January 1996, the Republicans surrendered and passed clean legislation, reopening the government. The budget talks ended soon after, without a balanced budget deal.

Figure 6 shows that H.R. 2491, the original budget reconciliation bill passed by the Republican Congress and vetoed by the president, would have saved $752 billion over seven years. Clinton offered a counterproposal that would have saved $417 billion.[45] Republicans used the debt limit and a government shutdown to push Clinton into supporting their budget. A public backlash against these GOP tactics, plus the public’s preference for the president’s budget proposals, allowed him to eventually block the Republican approach.

Figure 6 shows that H.R. 2491, the original budget reconciliation bill passed by the Republican Congress and vetoed by the president, would have saved $752 billion over seven years. Clinton offered a counterproposal that would have saved $417 billion.[45] Republicans used the debt limit and a government shutdown to push Clinton into supporting their budget. A public backlash against these GOP tactics, plus the public’s preference for the president’s budget proposals, allowed him to eventually block the Republican approach.

Penalty Default? Yes. Republicans had used the threat of a government shutdown and hitting the debt limit as leverage against President Clinton. He vetoed the budget reform legislation anyway, but the shutdown did not lead to a deal.

Public Support? No. The public wanted a deficit-reduction deal. However, Republican and Democratic voters were harshly split on how to balance the budget, and most voters opposed using the debt limit and government shutdown as leverage for a budget deal. Ultimately, the public sided against the more aggressive Republicans.

Healthy Negotiations? Emphatically no. Democrats ran millions of dollars in television issue-ads against the Republicans during the negotiations.[46] Republican lawmakers asserted that they did not want to be in the same room with Clinton.[47] Republicans portrayed the president as a dishonest negotiator, and the president portrayed Republicans as hostage-takers.

Clinton and House Speaker Gingrich attacked each other in the press daily. Clinton and Senate Majority Leader Dole were already gearing up for the 1996 presidential election and in little mood for compromise. House Republican freshmen did not trust the party leadership negotiating on their behalf. Similarly, deficit-reduction plans by moderate congressional Democrats were dismissed by their own party leaders.

Result: The penalty default, a government shutdown, was not enough to bring about a deal. There was a deal to be made—the disagreement was over the magnitude of the spending cuts—yet animosity between the sides resulted in failure.

1997 Balanced Budget and Taxpayer Relief Acts (“1997 Budget Deal”)[48]

Following the contentious 1996 election, President Clinton and the Republican congressional leadership decided to give balancing the budget another try. With Dole no longer in the Senate and House Speaker Newt Gingrich weakened, the Clinton White House sought a fresh start by reaching out to the Republican chairmen of the House and Senate Budget Committees.

Thanks to strong economic growth, the rapidly closing budget deficit meant that both parties could achieve the long-sought goal of a balanced budget without as much political sacrifice as earlier deals required. Starting essentially with the policy frameworks from the 1995–96 failed negotiations, new CBO budget estimates continually reduced the amount of required savings for a balanced budget. The president and congressional Republican leaders announced a package of spending and tax cuts on May 2, 1997, worked out the details over the summer, and enacted the final reforms in August.

This grand bargain yielded net estimated savings of $816 billion over 10 years. The spending savings of $1,036 billion consisted of discretionary spending caps ($520 billion); Medicare reimbursement cuts to health providers ($297 billion); Medicare savings from beneficiaries, such as premium increases ($88 billion); and $142 billion in resulting net interest savings—and an $11 billion cost of other provisions. Revenues were cut by $220 billion. The deal provided for a $500 per-child tax credit and a new entitlement, the Children’s Health Insurance Program (CHIP).[49]

Both sides wanted credit for a balanced budget. Republicans wanted to show that they could govern after the bruising government shutdowns of 1995–96, while Democratic leaders wanted to combat their image as tax-and-spend liberals. Liberal Democratic Rep. Charles B. Rangel (D., New York) triumphantly declared at the White House ceremony that “we have now shattered the myth that we Democrats are spending Democrats and taxing Democrats.”[50]

Penalty Default? No.

Public Support? Yes. The public wanted a balanced budget. Republicans had campaigned on a balanced budget. Clinton and congressional Democrats wanted to build their deficit-hawk credibility with the public.

Healthy Negotiations? Yes. In a complete reversal from the 1995–96 negotiations, both sides worked well together, trusted each other, and negotiated in good faith. Negotiators focused on ranking each side’s preferences, delineating must-haves and unacceptables, and seeking win-win solutions.

Neither side sought to embarrass the other. Clinton even decided to give the Republicans a “win” on tax cuts (even though the public shared Clinton’s skepticism) as a good-faith gesture to keep Republicans on board. Both sides also reduced the number of negotiators and excluded those who were seen as overly partisan or difficult. Gingrich credited the “human touch” for making the deal possible.

There were tense moments. Late one evening, Rep. John Kasich (R., Ohio) called Clinton aide John Hilley at home and asked for his address because, he said, “if we don’t get a deal by the beginning of the recess, I’m [expletive] coming over and burning your house down!” Yet Kasich later raved that “Hilley was the whole key to this because whenever things got crazy I’d talk to Hilley.”[51]

Result: With public support and healthy negotiations, a deal was to be had. The law included significant tax cuts and spending hikes up front, paid for by vague automatic cuts in the future. After surging economic growth revenues surprisingly balanced the budget by 1998, many of those future automatic cuts were canceled. This was the last successful budget negotiation that showed significant trust and good faith on both sides.

1998 Clinton–Gingrich Social Security Meetings[52]

After completing the 1997 bipartisan budget agreement—and seeing the budget balance one year later—Clinton and Gingrich held secret meetings to craft a deal that would bring personal investment accounts and consider other structural reforms to Social Security, such as slowing the growth of benefits. Clinton wanted to protect the new budget surplus from tax cuts. Gingrich wanted to introduce market reforms into Social Security. The group began small and included Erskine Bowles, White House chief of staff, and Bill Archer, chairman of the House Ways and Means Committee.

The group mapped out a full process of speeches, events, and legislation to be rolled out beginning with the January 27, 1998, State of the Union address. Six days before the speech, news of the president’s relationship with Monica Lewinsky broke. Republicans went to war against the White House; Democrats geared up to defend their leader; and the Social Security reform was an instant casualty.

Penalty Default? No. Social Security benefits faced no immediate threats.

Public Support? Yes. Social Security personal accounts were popular with Republicans, and Clinton’s pollster found that 73% of Democratic voters wanted some form of personal account system as well.

Healthy Negotiations? Not by the end. Clinton and Gingrich began negotiating in secret and seemingly in good faith. There were no leaks, and a full bipartisan rollout was choreographed. That short era of good feelings evaporated.

Result: The meetings began with the primary trust ingredient, but that evaporated. Granted, the plan still may have faced challenges in Congress. However, the Lewinsky scandal showed the importance of outside political constraints on Washington deal-making.

1999 National Bipartisan Commission on the Future of Medicare (“Breaux-Thomas)[53]

As part of the 1997 budget agreement, the White House and Republican Congress created a commission to reduce Medicare’s long-term liabilities. The 17 commission members included lawmakers and outside experts of both parties. It was cochaired by Sen. John Breaux (D., Louisiana) and Rep. Bill Thomas (R., California).

Negotiations began well, leading to proposals that favored raising the Medicare eligibility age from 65 to 67, merging Parts A and B, introducing a premium support option,[54] and adding a Medicare drug benefit. However, as the Lewinsky scandal gained momentum, Clinton aimed to shore up his liberal base. Hours before the commission’s final vote, the president gave a press conference publicly opposing the deal. Top commission advisors of both parties agree that the president’s late opposition drove several commission Democrats to oppose the final deal, leaving them just shy of the 11 of the 17 required votes for approval.

Penalty Default? No.

Public Support? No. The federal surplus made the public less interested in seeking budget savings. Furthermore, the backlash against managed-care approaches (such as HMOs) to health care undermined support for the direction the commission was headed.

Healthy Negotiations? Ultimately, no. The commission did generally get along, worked together, and built trust. But the Lewinsky scandal eventually pushed most commission Democrats against compromise.

Result: These negotiations had none of the three primary ingredients typically necessary for success. Breaux and Thomas continued to support the proposal. A version of the commission’s Medicare drug benefit was enacted in 2003 (which added costs to the Medicare system, in conflict with the commission’s overall goal).

2005 Social Security Reform[55]

George W. Bush ran on Social Security reform in the presidential election of 2000, and again in 2004. In 2001, he created a bipartisan Social Security reform commission (with no current members of Congress) that congressional Democratic leaders reportedly refused to meet with.[56] In early 2005, Bush proposed adding personal accounts to Social Security and later endorsed “progressive indexing” of benefits (slowing the growth of benefits for upper-income seniors). Other details were open to negotiation.

Congressional Democrats and liberal organizations—many of whom had previously supported addressing Social Security’s fiscal challenges—instead repudiated their past openness and refused to engage in the process.[57] Bush was relentlessly attacked as anti–senior citizen. Many Democrats (save for a few moderates in Congress) denied that Social Security faced any solvency issues and misrepresented the proposals as eliminating all benefit guarantees and radically cutting benefits. This scared off the congressional Republican majority, who had concluded that Social Security reform was too controversial to do without bipartisan support. The reforms faded away, never reaching a vote in Congress.

Penalty Default? No. The projected insolvency of the Social Security trust fund was a few decades away.

Public Support? No. Polling showed support for fixing Social Security and some sympathy for personal accounts.[58] Yet the public was not invested in the issue, and Democratic attacks successfully made reform toxic.

Healthy Negotiations? No. Partisan tensions were high after the 2004 presidential campaign. Democrats and AARP harshly attacked the president’s proposals. When asked when the Democrats would propose their own plan to avert Social Security’s eventual insolvency, House Democratic leader Nancy Pelosi (D., California) responded: “Never. Is never good enough for you?”

Result: With none of the three primary ingredients for a successful grand bargain, Bush’s desire to reform Social Security had no traction. This episode also raises another political problem for budget deals: unified government. When the White House and both branches of Congress are in the hands of one party, the prospect for grand bargains does not increase—more likely, it makes such deals less likely. The minority party, hoping to regain some power, has no motivation to help the majority secure a victory, and refuses to provide the needed bipartisan cover to get a deal done. The 1993 legislation was barely enacted under these circumstances, but the 2005 efforts failed.

2010 National Commission on Fiscal Responsibility and Reform (“Simpson-Bowles”)[59]

With budget deficits exceeding $1 trillion, congressional Republicans supported the creation of a bipartisan deficit commission—and then voted it down when President Obama endorsed it.[60] In response, Obama created his own deficit commission, cochaired by Democrat Erskine Bowles and former Republican senator Alan Simpson. The 18 commission members consisted of 12 Republican and Democratic congressional leaders, two chairpersons, and four nongovernmental experts.

After nine months of mostly ineffective negotiations, Bowles and Simpson drafted a chairman’s mark. Between 2012 and 2020, their proposal would have saved $4.124 trillion from sources including tax reform and gas-tax revenues ($996 billion), discretionary spending caps ($1.661 trillion), health-care mandatory savings ($341 billion), other mandatory savings ($215 billion), Social Security revenue and benefit changes ($238 billion), and resulting interest savings ($673 billion). The underlying baseline also assumed extension of the “2001 Bush tax cuts,” a cancellation of upcoming Medicare provider cuts that were required by the sustainable growth rate (SGR) law (which was created in the 1997 deal), and a gradual reduction in Overseas Contingency Operation (OCO) spending in Iraq and Afghanistan. The long-term target was to balance the budget with taxes and spending at 21% of GDP by 2035.[61]

The chairman’s mark failed to get the support of 14 of the commission’s 18 members. The strongest opposition came from the House Republicans and Democrats. Republicans asserted that the plan did not sufficiently reform Medicare and Medicaid, raised taxes too high, and would push workers into Affordable Care Act health exchanges (by paring back the tax exclusion for employer-provided health premiums).[62] Obama also opposed the blueprint for eliminating too many tax deductions and cutting defense spending too deeply.[63] Congress broadly criticized the deal as well, and outside groups attacked any reforms that affected them.

Penalty Default? No.

Public Support? No. In 2010, conservative voters were focused on rising deficits. Yet Republicans did not want to raise taxes, and Democratic voters were wary of most major spending cuts. Both parties’ leaders considered it politically safe to oppose the final commission recommendations.

Healthy Negotiations? No. Republican and Democrat factions often refused to negotiate directly, communicating through cochairmen Bowles and Simpson. Senators Kent Conrad (D., North Dakota), Judd Gregg (R., New Hampshire), and Tom Coburn (R., Oklahoma) pushed for a deal, although most commission members did not want to be the first to move off their talking points or offer concessions. The prospect of a chairman’s mark—drafted by Bowles and Simpson—finally gave members a document to modify and shape, rather than just argue talking points. The length of the commission—nine months—marginally helped developed trust.

Result: With none of the three primary ingredients necessary for a deal present, negotiations led nowhere. However, many of the commission’s proposed savings within discretionary spending caps and small entitlement savings reforms were later enacted as part of the 2011 Budget Control Act and the 2013 and 2015 “Ryan-Murray” deals that altered the Budget Control Act.[64]

2011 Obama–Boehner Grand Deal[65]

With Simpson-Bowles in the rearview mirror, the debt limit needed to be raised, and a Tea Party Congress demanded deficit reduction. The president wanted to avoid hitting the debt limit and risking a federal default on its obligations. Republicans wanted to cut the deficit, yet also feared blame if the negotiations failed.

White House and congressional leaders began a lengthy series of negotiations. The 25-person “Biden Group”—led by the vice president and Republican House Majority Leader Eric Cantor—began talking in May 2011. Despite progress on small deficit-reduction reforms, this group disbanded when it was discovered that Obama and House Speaker John Boehner were engaging in their own negotiations. Figure 7 shows a sample of the leading offers from Obama and Boehner. Taxes as well as the size and pace of major entitlement reforms divided the two sides. The Obama–Boehner group—which expanded to include other congressional and administration leaders—eventually failed to reach a grand deal. It foundered on the fundamental division between Republicans and Democrats over taxes and entitlements. The group would move on to a discretionary spending deal that is taken up below.

White House and congressional leaders began a lengthy series of negotiations. The 25-person “Biden Group”—led by the vice president and Republican House Majority Leader Eric Cantor—began talking in May 2011. Despite progress on small deficit-reduction reforms, this group disbanded when it was discovered that Obama and House Speaker John Boehner were engaging in their own negotiations. Figure 7 shows a sample of the leading offers from Obama and Boehner. Taxes as well as the size and pace of major entitlement reforms divided the two sides. The Obama–Boehner group—which expanded to include other congressional and administration leaders—eventually failed to reach a grand deal. It foundered on the fundamental division between Republicans and Democrats over taxes and entitlements. The group would move on to a discretionary spending deal that is taken up below.

Penalty Default? Yes. Republicans threatened to vote against raising the debt limit without a deal.

Public Support? No. A Gallup poll showed that a plurality of voters preferred not raising the debt ceiling at all.[66] The public also lacked consensus on reform options: a September 2011 Bloomberg poll showed that 38% of adults wanted spending cuts only, 31% wanted tax increases only, and 17% preferred both.[67] Surveys showed a record 64% of voters considered reducing the budget deficit as a top priority,[68] yet strong majorities also expressed an unwillingness to pay more in taxes or accept significant spending cuts.[69]

Healthy Negotiations? No (see sidebar, The Obama–Boehner Negotiations: An Autopsy). Neither the Republican nor Democratic leaders had the full trust of their rank-and-file lawmakers; within the negotiations, neither party trusted the other, both parties leaked to the media, and both parties attacked the other publicly. The negotiations themselves were unstructured, containing too many “red lines” and too few policy concessions.

Result: With only one of the three primary ingredients, the deal never happened.

|

The Obama–Boehner Negotiations: An Autopsy |

|

The “Biden Group,” 25 negotiators led by the vice president and the House majority leader (Eric Cantor), disbanded when they learned that President Obama and House Speaker Boehner had formed a separate negotiation. Obama and Boehner were close to a deal that fell apart when they learned of a bipartisan “Gang of Six” in the Senate that was closing in on their own deal. Whenever a new group formed, the earlier group would disband out of a belief that at least one side must be getting a better deal from the new group. For example, Obama abandoned a potential agreement with $800 billion in higher taxes as soon as he heard a rumor that the Gang of Six had agreed to $1.2 trillion in revenue.[79]

Boehner and Cantor had a personal rivalry and strong disagreements over whether to agree to tax increases (Boehner was more tax-friendly). Rank-and-file House Republicans did not trust their leaders at all and strongly opposed any deal raising taxes. In the Senate, John Kyl focused on moving a deal to the right, while Majority Leader Mitch McConnell was skeptical of the negotiations. Some rank-and-file senators formed a Gang of Six, which rendered it impossible for Republicans to negotiate with one voice, or for Democrats to trust that Republicans could follow through on a promised deal.